Samsung and SK Hynix Plunge 12% in Global AI Markets Rout

1 hr ago

A global equity selloff struck on 23 June 2026, with no earnings miss, no rate shock, and no regulatory announcement to blame. The cause was something more structural: a crowded trade unwinding at speed.

AI-linked semiconductor stocks had become among the most concentrated institutional positions in global equity markets. When that positioning reversed, it did so simultaneously across Seoul, Frankfurt, and New York within a single trading session. That synchronisation is what distinguishes this from routine sector rotation.

What follows tells you whether 23 June was a positioning flush with a defined shelf life or something with more runway, and where the risk actually sits for investors holding AI-exposed portfolios.

The warnings arrived before the losses did. Citi strategist David Chew had flagged extended bullish positioning in U.S. technology stocks and the Nasdaq 100 in a note issued prior to 23 June. Separately, UBS strategist Gerry Fowler had identified similar risks in the crowded AI and data-centre trade.

Gerry Fowler, UBS, warned of concentrated risk in AI and data-centre positioning prior to the selloff, noting the trade had become crowded enough that a sentiment shift could produce outsized price moves regardless of fundamentals.

No single news event, earnings report, or macroeconomic data print has been identified as the trigger. That absence is itself the explanation. When no catalyst exists, positioning is all that remains, and when a large number of institutions hold the same thematic bet, exit attempts amplify price moves even when the underlying investment thesis has not changed.

The fact that two major bank strategists had already named this risk means investors cannot treat 23 June as an unforeseeable shock. The question was always when the unwind would come, not whether.

The Bank of America June 2026 Global Fund Manager Survey had already put a precise number on the AI crowding in global semiconductors: 80% of institutional managers named long semiconductors the most crowded trade ever recorded in the survey’s history, a reading that escalated from 24-25% in April to 73% in May before hitting that all-time high just days before the 23 June session.

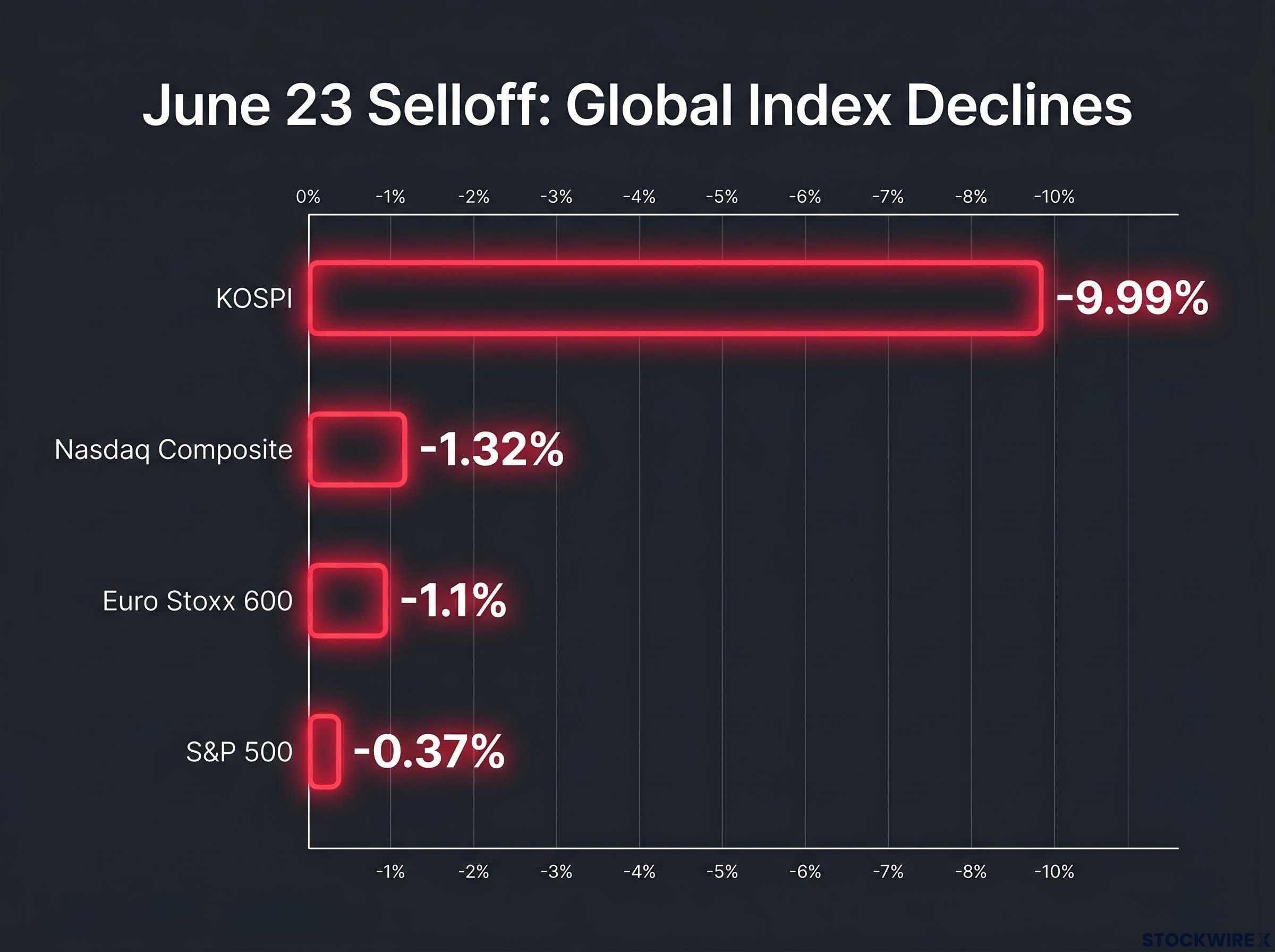

The KOSPI closed down 9.99% at 8,203.84, its sharpest single-day decline in months, amid heavy foreign selling. The damage concentrated in the two names most exposed to the AI hardware supply chain.

| Asset | Single-Day Decline | Note |

|---|---|---|

| KOSPI | ~9.99% | Closed at 8,203.84 |

| Samsung Electronics | ~12.3% | Key HBM supplier |

| SK Hynix | ~12.5% | Key HBM supplier |

Samsung Electronics and SK Hynix are not peripheral to the AI theme. Both dominate the production of high-bandwidth memory (HBM), the chip architecture that powers AI training infrastructure globally. Their share prices function as a proxy for institutional sentiment on the entire AI hardware build-out.

Losses of this magnitude in the two dominant HBM suppliers tell you the market is repricing not just near-term earnings expectations but the entire premium attached to AI infrastructure exposure. The speed and concentration of the selling points to institutional, not retail, activity.

The chip stocks that collapsed hardest on 23 June share a common thread: they make the memory that AI cannot function without. High-bandwidth memory is worth understanding because it explains why a positioning unwind in one corner of the semiconductor sector rippled across every major index.

Here is what you need to know:

That concentration is the key. When the AI trade became crowded, Samsung and SK Hynix became disproportionately vulnerable to any sentiment shift. The distinction matters: 23 June reflected a change in the positioning premium priced into AI-linked stocks, not necessarily a change in the fundamental outlook for AI spending. For anyone holding a fund with semiconductor exposure, that distinction is the difference between panic and perspective.

The distinction between positioning risk and fundamental risk matters here because the AI memory demand architecture has structural features that differ from prior semiconductor cycles: hyperscaler capital expenditure from the four largest US cloud operators is projected at $725 billion in 2026, SK Hynix has shifted to foundry-style multi-year supply agreements extending through 2028-2030, and new manufacturing lines are not expected to reach mass production until after 2027.

Asian weakness typically softens as it travels west. On 23 June, it did the opposite.

The Euro Stoxx 600 dropped roughly 1.1% through the European morning session, despite the absence of any continent-specific negative news. Rather than treating the Asian declines as a buying opportunity, European traders amplified them. The absence of dip-buying was itself a signal: institutional conviction behind the de-risking was genuine and cross-regional.

By the time New York opened, S&P 500 and Nasdaq 100 futures were pointing decisively lower. The session confirmed the pattern.

| Index / Region | Approximate Decline | Session |

|---|---|---|

| Euro Stoxx 600 | ~1.1% | European morning |

| Nasdaq Composite | ~1.32% | U.S. close |

| S&P 500 | ~0.37% | U.S. close |

The divergence between the Nasdaq and S&P 500 tells you precisely where the risk sat. The Nasdaq, with its heavier tech and semiconductor weighting, absorbed more than three times the damage of the broader S&P 500. Diversified broad-market exposure weathered this session far better than concentrated tech or AI positioning.

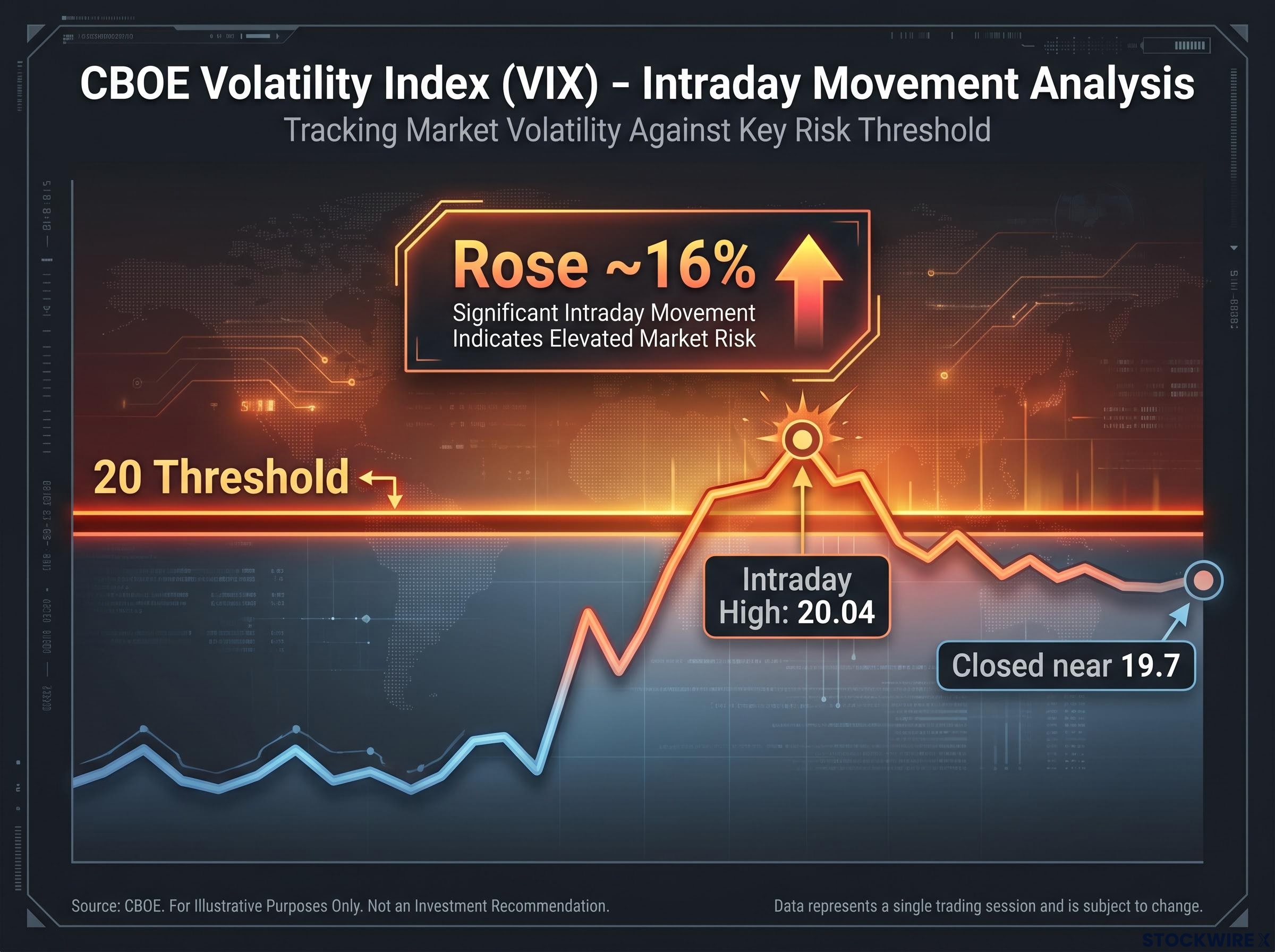

The CBOE Volatility Index (VIX), a measure of expected near-term volatility in the S&P 500 derived from options pricing, rose approximately 16% on the day, hitting an intraday high of 20.04 before closing near 19.7.

VIX intraday peak: 20.04. The 20 level is widely recognised by professional risk managers as a threshold between low-stress and elevated-stress regimes. Crossing it tends to activate mechanical de-risking by volatility-sensitive strategies, including risk-parity and volatility-targeting funds.

That mechanical layer matters. Volatility-targeting strategies automatically reduce equity exposure when volatility rises above preset thresholds. A VIX approaching 20 means those automated processes are now potentially active, which could extend the selloff into subsequent sessions even without a new fundamental trigger.

For hedging, the picture is more nuanced. Options-based protection is more expensive than it was a week ago but remains far from crisis-level pricing. The environment calls for selective, cost-conscious hedging rather than broad portfolio insurance.

One layer of context for the 23 June VIX reading is the persistent gap between VIX and realised volatility that has characterised 2026: implied volatility has run above 23% for much of the year while realised volatility has stayed below 14%, meaning options-based protection has been systematically priced for more turbulence than the daily price movements have delivered.

The most actionable insight from 23 June is not the magnitude of the losses but the gap between those who held concentrated AI exposure and those who did not. The KOSPI fell nearly 10%; the S&P 500 fell 0.37%. That spread is the clearest signal about where portfolio risk actually resides.

The spread between the KOSPI’s near-10% decline and the S&P 500’s 0.37% loss on 23 June is a live illustration of AI stock concentration risk: UBS has recommended that investors with concentrated AI positions reduce single-name exposure while maintaining broader thematic participation, and a position-sizing discipline capping individual AI names at 3-5% of total portfolio value converts that recommendation into actual behaviour during short-duration selloffs.

What has genuinely changed: the low-volatility conditions that made concentrated AI positioning feel comfortable have shifted. The VIX is near 20. Strategists at both Citi and UBS had already identified this risk, which means further de-risking cannot be ruled out.

What has not changed: the fundamental case for AI infrastructure spending. The session’s losses are a story about positioning becoming too concentrated, not a judgement on whether AI capital expenditure keeps growing. Keeping those two narratives distinct is the starting point for a clear-headed response.

Here is what to monitor in the sessions ahead:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Forward-looking statements regarding market conditions and positioning are speculative and subject to change based on market developments.

The selloff was caused by the rapid unwinding of heavily concentrated institutional positions in AI-linked semiconductor stocks, not by any earnings miss, interest rate change, or regulatory announcement. Both Citi and UBS strategists had flagged this crowding risk before the event.

High-bandwidth memory is a specialised chip architecture that stacks memory layers vertically to feed AI accelerator chips the data volumes they require at the speeds AI model training demands. Samsung Electronics and SK Hynix dominate global HBM production, making their share prices a direct proxy for institutional sentiment on AI infrastructure spending, which is why they absorbed the largest single-day losses.

A VIX at or above 20 is widely recognised by professional risk managers as the boundary between low-stress and elevated-stress market regimes. When it crosses that level, volatility-targeting and risk-parity funds automatically reduce equity exposure, which can extend a selloff into subsequent sessions even without a new fundamental trigger.

No. The session reflected a repricing of the positioning premium built into AI-linked stocks, not a change in the underlying investment thesis. Hyperscaler capital expenditure from the four largest US cloud operators is still projected at $725 billion in 2026, and multi-year supply agreements for HBM extend through 2028-2030.

The most direct check is measuring how much of your portfolio's recent performance depended specifically on AI semiconductor names. UBS has recommended reducing single-name exposure while maintaining broader thematic participation, with a position-sizing discipline that caps individual AI names at 3-5% of total portfolio value.