On 23 June 2026, South Korea’s benchmark KOSPI index posted its steepest single-session decline since the COVID pandemic, shedding approximately 10% in one trading day, and the damage arrived on Australian screens within hours. The KOSPI collapse was not a localised accident. It drove a broad repricing of how much global investors are prepared to pay for exposure to AI and technology, and that repricing moved through Asian markets, US futures, and straight into the ASX Information Technology sector, which posted a 4.04% loss for a second day running. The names hit span enterprise software, sports analytics, hospitality platforms, and accounting tools. The connective tissue is not their businesses. It is their valuations. What follows breaks down where the selloff started, how it reached Australian markets, which stocks bore the worst of it, and what signals matter most in the sessions ahead. This is what you need to know before markets open tomorrow.

What broke in Korea, and why it matters globally

The KOSPI’s 10% single-session fall on 23 June 2026 was large enough to trigger market-wide circuit breakers. Korea’s index had already been under pressure in earlier June sessions, with prior declines linked to higher-for-longer US rate expectations and a derating of expensive AI hardware stocks. Monday’s crash was an escalation, not an isolated event.

Korea Times reporting on the KOSPI collapse confirmed that the sell-off was concentrated in heavyweight chipmakers, driven by intensified profit-taking by foreign institutional investors in semiconductor stocks, a pattern consistent with a broad repricing of AI hardware exposure rather than a localised Korean market event.

Korea sits at the centre of the global AI hardware and memory cycle. Its heavyweight semiconductor sector means the KOSPI functions as both an early indicator and an amplifier when AI sentiment shifts. When the index falls this hard, it is telling you something about how global investors are repricing the entire AI trade.

The MSCI classification decision compounds the selling mechanics: by declining to place South Korea on the Developed Market watchlist, MSCI removed both the near-term and medium-term passive inflow catalyst in a single announcement, eliminating a structural buyer that markets had been pricing in across the preceding rally.

US futures confirmed the message was not confined to Asia:

- Nasdaq futures: down 2.02% to 30,033.5

- S&P 500 futures: down 1.13% at 7,455.75

- Dow Jones futures: down 0.42% at 51,900.0

The gap between Nasdaq futures (down 2.02%) and Dow Jones futures (down 0.42%) is the clearest signal in the data. Technology and growth stocks are being sold; the broader economy is not. The question this selloff is asking is not “is a recession coming?” It is “what are AI stocks actually worth at these interest rates?”

When big ASX news breaks, our subscribers know first

How a Korean crash becomes an ASX problem

The XIJ Information Technology sector dropped 4.04% on 23 June 2026, marking back-to-back sessions as the single worst-performing segment on the Australian bourse. No Australian earnings were released. No local news broke. The damage arrived through the same channel it always does when global growth sentiment turns.

Global institutional investors do not treat Xero, WiseTech, Technology One, REA Group, CAR Group, and Seek as mid-cap Australian industrials. They bucket them with global growth and tech peers. When those institutions reduce exposure to expensive growth as a theme, they sell across the entire factor basket regardless of geography.

Why elevated multiples amplify the damage

ASX software and platform names trade on high earnings or revenue multiples that embed assumptions about years of sustained growth and benign funding conditions. These are long-duration cash flow assets, meaning their value today depends heavily on profits that arrive many years from now.

When discount rates shift, or when investors doubt the AI and growth narrative, the present value of those distant cash flows falls disproportionately. You are paying today for profits that arrive in 10 years, so anything that changes the cost of waiting hits the price hard.

For an Australian investor holding Xero or Technology One, this means the stock price can move sharply without any change in the underlying business. The “growth premium” you paid is itself being repriced by global events outside your control.

The stocks that took the worst of it

The breadth of the damage tells the story. Technology One, an accounting and enterprise software provider, fell 7.1%. Catapult Sports, a sports analytics platform, fell 6.1%. SiteMinder, a hospitality SaaS business, fell 6.0%. These companies have almost nothing in common operationally. What they share is a growth premium, and that premium is what got sold.

The ASX Information Technology sector blends structurally profitable SaaS platforms carrying gross margins of 75-90% with loss-making speculative names, meaning index-level data understates how different the risk profiles are across the names caught in this selloff.

| Stock | Ticker | Sector | Day’s Move | Price / Note |

|---|---|---|---|---|

| Technology One | TNE | Information Technology | -7.1% | $27.73 |

| Catapult Sports | CAT | Information Technology | -6.1% | $2.77 |

| SiteMinder | SDR | Information Technology | -6.0% | $3.79 |

| Xero | XRO | Information Technology | -5.3% | $65.00 |

| WiseTech Global | WTC | Information Technology | -4.4% | Five-year low |

| CAR Group | CAR | Communication Services | -3.4% | |

| REA Group | REA | Communication Services | -3.1% | |

| Seek | SEK | Communication Services | -2.6% |

The Communication Services names at the bottom of the table are worth noting. CAR Group, REA Group, and Seek sit in a different GICS sector, but the market treats them as high-multiple growth equities. Sector classification provided no protection when global growth sentiment turned. The range from Catapult Sports to Xero to REA tells you this was a broad withdrawal from anything priced for growth.

WiseTech Global is a different kind of problem

WiseTech Global shed 4.4% on 23 June 2026, sliding to a five-year low amid elevated trading volumes. That decline is superficially in line with the broader sector. The risk profile is not.

WiseTech is not merely participating in a sector selloff. It is absorbing sector-level pressure and company-specific overhangs simultaneously. On 23 June 2026, executive chairman Richard White disclosed publicly that he was unaware of any investigation by the Australian Federal Police, a statement that underscores the character of the speculation and news flow weighing on the stock:

The WiseTech governance crisis has been accumulating across three distinct pressures since early 2026: an ASIC inquiry and Federal Police investigation into co-founder Richard White, margin compression from the August 2025 e2open acquisition, and the same broad software sector de-rating now hitting every name in the XIJ, with analyst price targets ranging from A$78 to A$138 against a price that has already fallen roughly 58% from its January highs.

Richard White, WiseTech’s executive chairman, made a public statement on 23 June 2026 indicating he had no awareness of any Australian Federal Police investigation into the company, a disclosure that speaks directly to the rumours and media attention surrounding the stock at this time.

When both the macro factor and the company-specific narrative are simultaneously adverse, the result is often capitulation-style price action before any durable base forms. For investors holding WiseTech, the usual logic of “wait for the sector to recover” may not be sufficient. Recovery from the global tech derating does not automatically resolve whatever is happening at the company level. WiseTech requires separate monitoring from the rest of the sector.

Valuation correction or something worse? What the evidence says

Two consecutive days of 4%+ sector declines look alarming. The question is whether the underlying earnings thesis has actually broken.

The evidence on 23 June 2026 leans toward a valuation and sentiment correction rather than a structural collapse. Pressure is concentrated in high-multiple tech and AI names, not distributed across defensives or credit markets. Nasdaq futures fell 2.02% while Dow futures fell only 0.42%, confirming sector-specific stress rather than economy-wide strain. Current-period earnings have not broken; the pressure is on multiples and sentiment, not revenue.

That reading is conditional. It holds only if fundamentals continue to deliver.

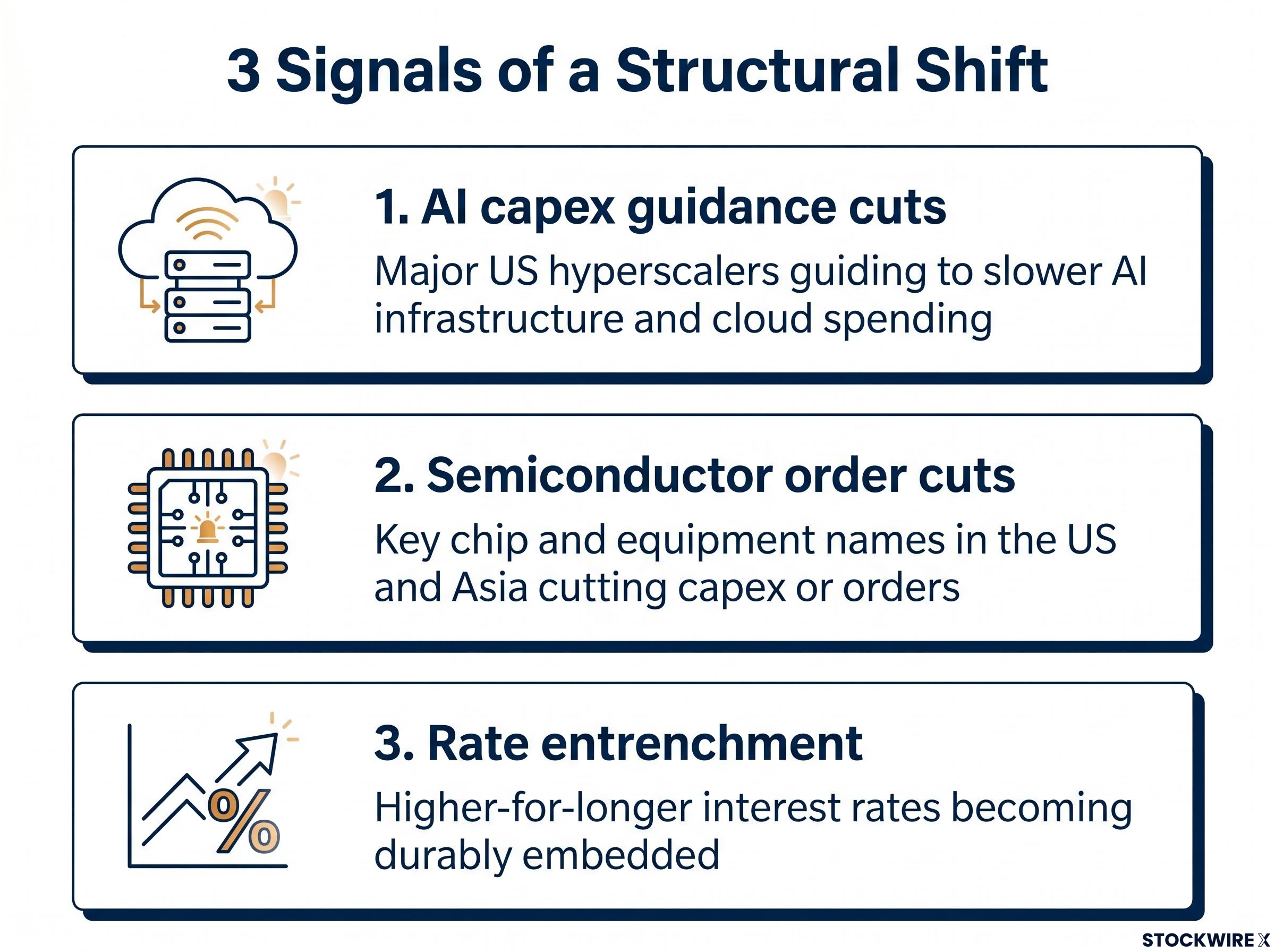

Three signals that would confirm a structural shift

- AI capex guidance cuts: Major US hyperscalers guiding to slower AI infrastructure and cloud spending, breaking the thesis that AI demand can justify elevated multiples.

- Semiconductor order cuts: Key chip and equipment names in the US and Asia cutting capex or orders, confirming a cyclical peak in AI hardware demand rather than a temporary pause.

- Rate entrenchment: Higher-for-longer interest rates becoming durably embedded, mathematically compressing fair value for long-duration growth assets and making current multiples untenable.

IDC semiconductor and AI capex forecasts project the global semiconductor market surpassing $1 trillion in 2026, underpinned by hyperscaler capital expenditure expected to rise approximately 70% year on year to around $600 billion, which is precisely the spending trajectory that current equity multiples across ASX technology names are pricing in and that any guidance cut from major platforms would immediately undermine.

The honest read for Australian investors is that this looks more like the market deciding “we overpaid” than “these businesses are broken.” But that distinction only holds if upcoming earnings confirm that AI demand and revenue growth remain intact.

What to watch before the next session, and the one after

The most actionable thing you can take from this session is a watchlist, not a prediction.

- US big-tech AI earnings guidance: What major platforms and chipmakers report about AI capex plans is the single most important near-term signal

- KOSPI stabilisation: Korea is a proxy for global AI hardware sentiment; continued free-fall signals something worse than a sentiment reset

- US market leadership breadth: Whether non-tech sectors durably assume leadership, or whether the rotation is temporary

- Local earnings season: How Technology One, Xero, WiseTech, CAR Group, REA Group, and Seek deliver versus consensus

- WiseTech-specific news flow: Any company disclosures, regulatory developments, or credible press around investigations

The WiseTech FY26 full-year results, scheduled for 26 August 2026, represent the next hard catalyst for the stock, with organic revenue growth rate, EBITDA margin trajectory, and any governance disclosures the three metrics that will determine whether the current price reflects a genuine reset or a value trap.

Map how your portfolio behaves under two distinct scenarios. Scenario one: AI spending continues strongly, but multiples stay lower, meaning solid growth with compressed valuations and lower returns than the prior cycle. Scenario two: AI spending itself disappoints and earnings slow, producing a double derating of both the multiple and the earnings base. Different ASX names will fare very differently under each.

Two consecutive days of 4%+ declines in a single theme is not background noise. It is information about how much volatility your current positioning actually carries. Now is the moment to check whether that matches what you signed up for.

What the next earnings season will actually settle

The evidence on 23 June 2026 points to a valuation and sentiment reset, not a confirmed structural collapse, but that reading is conditional on fundamentals holding. Upcoming US and local earnings seasons will settle the open question. ASX investors have a narrow window to review exposure before those results arrive.

The selloff has provided real information. It has told you something concrete about concentration risk, about how much of your portfolio’s returns depend on a single growth narrative, and about the volatility that comes with that exposure. Using that information is more valuable than predicting tomorrow’s open.

This article is intended for general informational purposes only and does not constitute financial advice of any kind. Readers should undertake their own due diligence and seek guidance from a qualified financial professional before making any investment decisions. Prior returns are not a reliable indicator of future performance. Any forward-looking statements are subject to prevailing market conditions and a range of risk factors that may cause actual outcomes to differ materially.

—