KOSPI Drops 10% as Crowded AI Trade Unwinds Across Global Markets

1 hr ago

AI-linked stocks at the centre of the global equity supply chain just had one of their worst single sessions in years. The shockwave started in Seoul, crossed into Frankfurt before European traders had finished their morning coffee, and was dragging Nasdaq futures lower before New York opened.

This is not a routine bout of volatility. The selling originated in the specific companies that physically build AI infrastructure: Samsung Electronics and SK Hynix, the world’s dominant suppliers of the memory chips that power every major AI system in production. That makes this a direct pricing event for the AI investment thesis, not a macro scare or a rate-driven wobble.

What follows covers which markets were hit, what drove the move, and the specific signals that will determine whether today’s session was a one-day flush or the opening act of a deeper de-risking cycle in AI equities.

The speed told the story. What began as concentrated selling in two Korean semiconductor names before most global investors were at their desks had, within hours, repriced AI-linked equities across three continents.

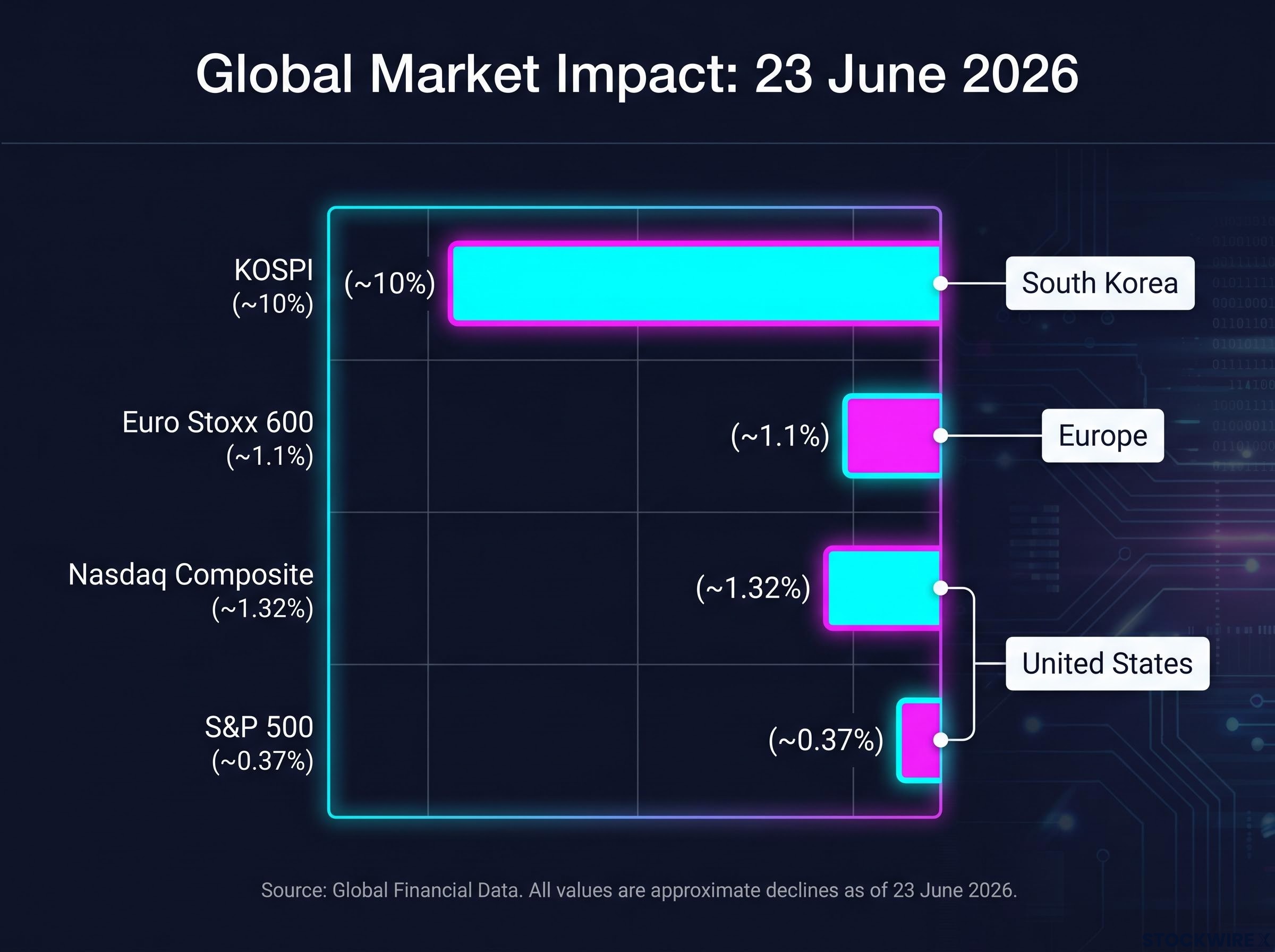

The KOSPI fell as much as 10% intraday on 23 June 2026, one of its steepest single-session declines in years. Samsung Electronics and SK Hynix each dropped approximately 12%, dragging the index lower as foreign investors dumped semiconductor holdings.

Losses then spread into the European session, where the Euro Stoxx 600 shed roughly 1.1% as semiconductor and technology names absorbed the heaviest selling. U.S. futures tracked the deterioration throughout the morning, putting Wall Street on course for a weak open before the first bell.

The Nasdaq Composite fell approximately 1.32%, while the S&P 500 declined a more modest 0.37%. That gap matters. A 1.32% Nasdaq drop versus 0.37% on the S&P 500 tells you this was a sector-specific event concentrated in technology and AI names, not a signal of broad economic deterioration. If you hold a diversified portfolio, the damage was far less severe than the headlines suggested. If you hold concentrated AI positions, the headlines understated it.

| Index | Region | Decline | Date |

|---|---|---|---|

| KOSPI | South Korea | ~10% | 23 June 2026 |

| Euro Stoxx 600 | Europe | ~1.1% | 23 June 2026 |

| Nasdaq Composite | United States | ~1.32% | 23 June 2026 |

| S&P 500 | United States | ~0.37% | 23 June 2026 |

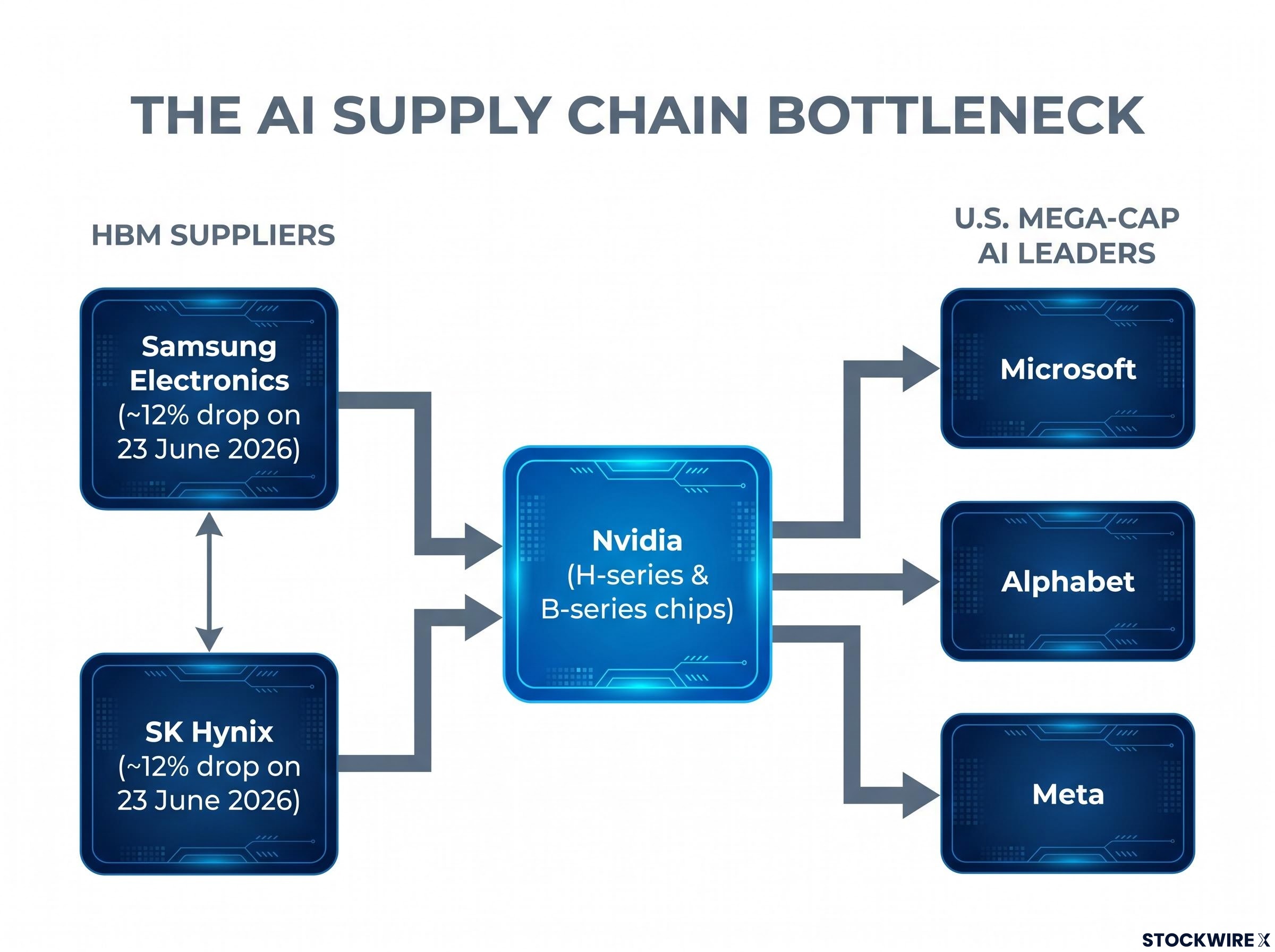

These are not ordinary chip makers. Samsung Electronics and SK Hynix are the primary global suppliers of high-bandwidth memory (HBM), the specialised component that sits at the core of every major AI chip’s performance. Without HBM, the processors powering AI workloads cannot retrieve data fast enough to function at scale.

Both fell approximately 12% on 23 June 2026. The size of the move reflected something more than profit-taking.

The HBM4 qualification cycle for Nvidia’s next-generation Vera Rubin platform, confirmed by Jensen Huang on 5 June 2026, placed SK Hynix at an estimated 60-70% of volume allocations and Samsung at a secondary 25-30% share, a distribution that reflects each supplier’s relative standing with Nvidia before today’s selloff introduced fresh questions about order trajectory.

The market is questioning whether the large cloud providers, the hyperscalers, will sustain their current pace of AI infrastructure spending. When that doubt lands on the companies that physically manufacture the components, the AI supply chain is being repriced from the bottom up.

High-bandwidth memory is a specialised memory architecture designed to let AI processors access large datasets without being bottlenecked by data retrieval speed. Standard memory cannot feed data to AI chips quickly enough for the workloads they run. HBM solves that by stacking memory layers and connecting them through ultra-fast pathways directly to the processor.

Samsung and SK Hynix together hold dominant global supply of this component. Nvidia’s H-series and B-series chips, which power the majority of enterprise AI deployments worldwide, rely on HBM. That concentration means any signal of softening demand for HBM ripples outward immediately.

Three reasons this supply concentration makes these two companies global bellwethers for AI spending sentiment:

The severity of today’s move was not irrational. It was structurally predictable.

Institutional portfolios had built large, concentrated positions in AI-linked equities across semiconductors and U.S. mega-cap technology. Citi strategists led by David Chew and UBS strategists led by Gerry Fowler had each warned in notes issued before today’s session that this concentration created vulnerability to a positioning-driven unwind.

The scale of today’s reversal is sharpest when viewed against the rally that preceded it: memory chip positioning had driven combined gains exceeding 250% across Micron, Sandisk, and SK Hynix in the 30 days ending 12 May 2026, with HBM capacity sold out through 2026-2027 and a prospective Samsung labour strike adding further supply-tightness assumptions that bulls had embedded in valuations.

The VIX rose approximately 16% on 23 June 2026, reaching 20.04. That level is not just a fear gauge reading. It is a mechanical threshold at which volatility-targeting and risk-parity strategies begin cutting equity exposure automatically, meaning selling can continue even without new negative news.

Three conditions under which positioning-driven selling becomes self-reinforcing:

Understanding this mechanical dimension helps you avoid misreading continued price declines as fresh fundamental deterioration when they may simply reflect rules-based de-risking working through the system.

The next 24-48 hours of market data matter more than the day itself. Here is what to watch:

Placing today’s session inside broader 2026 volatility context matters for interpretation: nearly a century of S&P 500 data shows the year has produced only modestly above-average daily move frequency despite several headline-generating episodes, and the persistent gap between elevated implied volatility and lower realised volatility has been a defining feature of the year’s risk environment well before today’s Korean semiconductor shock.

These four signals collectively tell you whether you are watching a temporary repricing of crowded AI positions or the beginning of a genuine rotation that would require a portfolio response.

The structural AI narrative, productivity gains, infrastructure buildout, new business model creation, remains intact as a long-term thesis. Nothing in today’s session altered the fundamental economics of AI adoption.

What today did reveal is how aggressively that thesis had been priced and how concentrated portfolios had become around it. This was a positioning event, not a thesis event. The Nasdaq-versus-S&P 500 divergence confirms it. The absence of acute credit spread widening or dramatic dollar strength confirms it further.

The appropriate response depends on where you sit:

For investors with concentrated semiconductor or AI mega-cap positions reassessing their exposure after today’s session, our dedicated guide to AI stock concentration risk walks through a five-strategy framework for staying exposed to the AI buildout while managing single-name and sector-level downside, including UBS-recommended position-sizing disciplines and a quarterly rebalance trigger designed for exactly this kind of short-duration selloff.

When a market’s leadership is dominated by a single theme, sentiment and positioning shifts produce outsized, rapid price moves. Risk management is as important as stock selection. Today made that concrete.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

These statements are speculative and subject to change based on market developments and company performance.

—

High-bandwidth memory (HBM) is a specialised memory architecture that allows AI processors to retrieve large datasets without speed bottlenecks. Samsung and SK Hynix together dominate global HBM supply, meaning any signal of softening HBM demand ripples immediately into AI chip makers, cloud providers, and technology-heavy indices worldwide.

The KOSPI fell approximately 10% on 23 June 2026 after Samsung Electronics and SK Hynix each dropped roughly 12%, driven by investor concerns over whether hyperscale cloud providers would sustain their current pace of AI infrastructure spending, compounded by crowded institutional positioning that amplified the selloff.

The Nasdaq Composite fell approximately 1.32% while the S&P 500 declined just 0.37% on 23 June 2026. That gap confirms this was a sector-specific event concentrated in technology and AI names rather than a signal of broad economic deterioration.

The four key signals are: whether the VIX closes back below 20, whether Nasdaq mega-caps like Nvidia, Microsoft, Alphabet, and Meta stabilise, whether selling spreads beyond technology into financials and industrials, and whether credit spreads and the dollar remain calm. Sustained VIX elevation above 20 and multi-day declines in those four mega-caps would indicate deeper de-risking is underway.

Nvidia's AI chips rely directly on HBM supplied by Samsung and SK Hynix, so any repricing of HBM demand flows through to Nvidia's order outlook and, by extension, to any AI-infrastructure ETF or fund holding Nvidia, Microsoft, Alphabet, or Meta. The Korean session on 23 June 2026 was not a remote event but a direct signal about the economics underpinning those positions.