On 9 June 2026, Marvell Technology fell more than 7% in a single session, NVIDIA slipped nearly 1.1%, and AI-related names broadly extended losses triggered by Broadcom’s disappointing quarterly results three sessions earlier. For investors who built concentrated positions in a handful of semiconductor and AI stocks over the past two years, weeks like this are expensive reminders of a problem that bull markets obscure: conviction in a theme is not the same as sound portfolio construction.

The AI investment theme has been one of the most powerful, and most volatile, forces in US equities since 2023. A Morningstar basket of 34 AI names gained approximately 50.8% in 2025, dwarfing the broader market’s 17.3% return. But the same basket produced extreme dispersion: some names posted triple-digit gains while others fell double digits. With UBS now recommending that investors with concentrated AI positions reduce single-name risk while staying exposed to the broader buildout, the strategic question has shifted from “should I own AI?” to “how should I structure that ownership?”

This guide explains what concentration risk looks like in an AI portfolio, why it is unusually elevated right now, and five practical strategies for staying invested in the AI buildout without letting any single stock derail an allocation.

Why your AI portfolio may be less diversified than it looks

Owning five AI stocks instead of one feels like diversification. In practice, it often is not. If every name in the portfolio responds to the same set of earnings drivers, what looks like a spread of bets is a single correlated position wearing different name tags.

The shared drivers binding most AI holdings together include:

- AI data-centre capital expenditure commentary from hyperscalers

- GPU demand cycles and pricing trends

- Big-tech spending plans and margin guidance

- Policy shifts and interest rate path changes

When Broadcom reported weaker-than-expected results on 6 June 2026, the reaction did not stay contained. By 9 June, Marvell Technology had fallen approximately 7.22% to $267.99, while NVIDIA declined roughly 1.09% to $206.36. Different companies, different business models, same catalyst.

CFA Institute research on correlation during drawdowns demonstrates that asset correlations tend to rise precisely when markets are falling, which is why a portfolio of five AI names with different ticker symbols can behave like a single position when a negative sector catalyst hits.

A Morningstar basket of 34 AI-related names gained approximately 50.8% in 2025, compared with 17.3% for the broader US market. The outperformance was real, but so was the dispersion: names like Micron and Lam Research posted triple-digit gains, while Adobe and Salesforce fell double digits over the same period.

That dispersion matters. US private AI investment reached $109.1 billion in 2024, illustrating the scale of capital chasing the theme. A narrow cluster of companies has absorbed a disproportionate share of those flows, making the crowding problem structural rather than incidental.

Recognising this correlation is not a bearish view on AI. It is a portfolio architecture issue. Every risk-management step that follows starts with this diagnostic: adding more names from the same narrow stratum of the AI stack does not reduce risk.

Index fund concentration compounds this problem for investors who pair individual AI names with broad market ETFs, since a cap-weighted US total market fund and an S&P 500 fund held simultaneously can produce near-identical top-five exposures rather than genuine diversification across the portfolio.

When big ASX news breaks, our subscribers know first

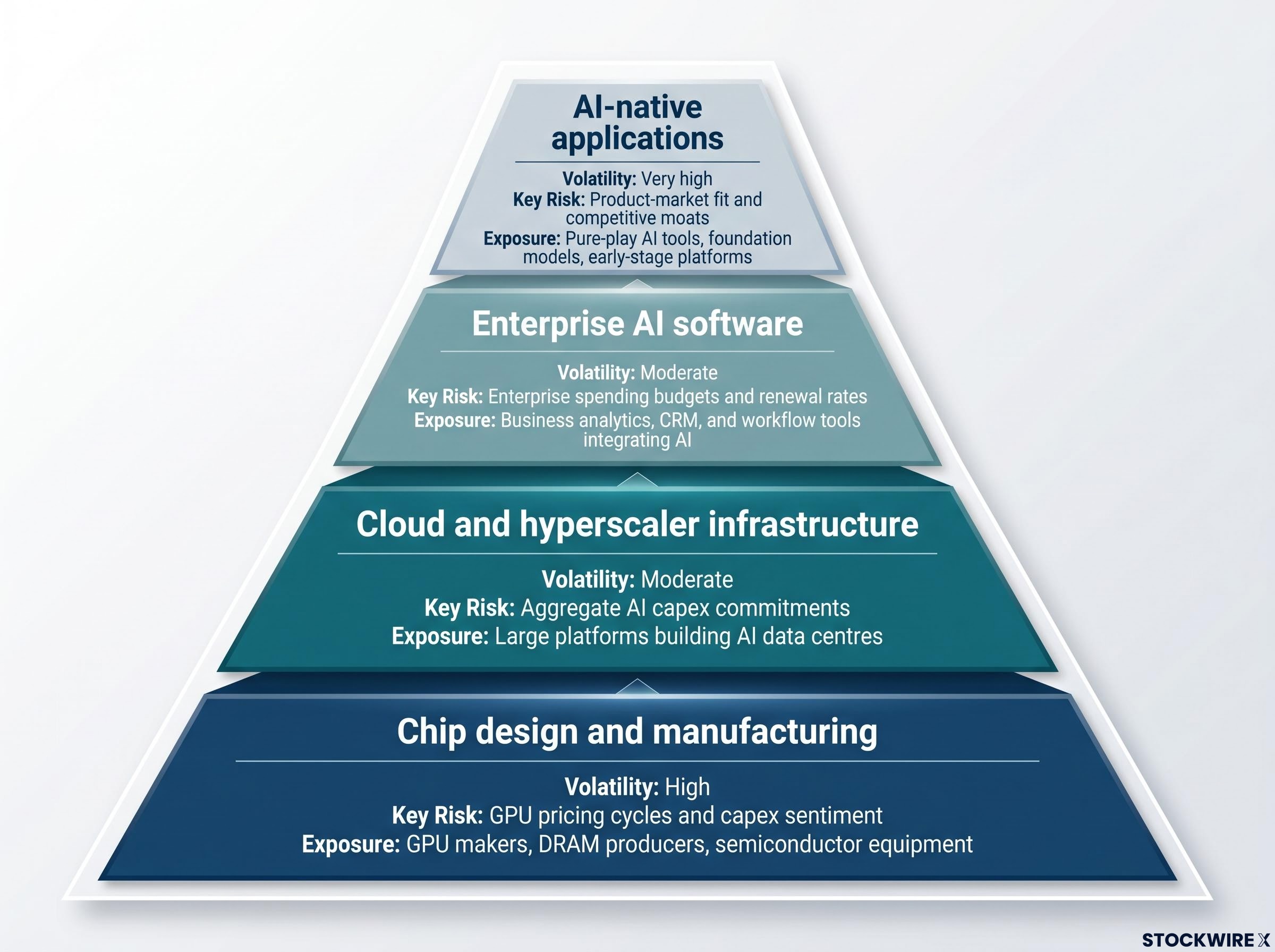

The AI stack has four layers, and most retail portfolios only own one

The AI buildout is not a single industry. It is a stack of interconnected layers, each with its own risk profile, return characteristics, and sensitivity to different catalysts. Most retail portfolios sit heavily in one layer, typically the chip layer, because GPU makers have attracted the most attention and generated the most dramatic returns.

The full value chain looks like this:

| Layer | Representative Exposure Types | Volatility Profile | Key Risk Driver |

|---|---|---|---|

| Chip design and manufacturing | GPU makers, DRAM producers, semiconductor equipment | High; sharp drawdowns on earnings misses | GPU pricing cycles and capex sentiment |

| Cloud and hyperscaler infrastructure | Large platforms building AI data centres | Moderate; diversified revenue streams buffer AI-specific shocks | Aggregate AI capex commitments |

| Enterprise AI software | Business analytics, CRM, and workflow tools integrating AI | Moderate; tied to SaaS adoption cycles | Enterprise spending budgets and renewal rates |

| AI-native applications | Pure-play AI tools, foundation models, early-stage platforms | Very high; outcomes path-dependent | Product-market fit and competitive moats |

The chip layer delivered the most spectacular gains, but it also absorbed the Broadcom selloff most acutely on 6 June 2026. Enterprise software names and cloud infrastructure platforms experienced less severe reactions because their earnings are driven by different rhythms. Adding exposure across these layers reduces sensitivity to a single bottleneck without abandoning the AI theme.

A structured approach to AI infrastructure allocation separates the chip layer, cloud platforms, and software into distinct sleeves with explicit weighting targets, which matters because each layer responds to different earnings catalysts and carries a meaningfully different drawdown profile during episodes like the June 2026 Broadcom selloff.

The OpenAI IPO: a preview of AI-native application risk

OpenAI has confidentially filed for an initial public offering with a potential listing targeted for late 2026 or 2027. It remains private and unlisted.

As a concrete illustration of the AI-native applications layer, OpenAI sits at the highest-idiosyncratic-risk tier of the stack. Its correlation to broader AI sentiment is likely to be very high in the early post-listing period, and the hype premium at entry could be substantial. For investors considering participation, defining the position’s role, whether it is a small satellite bet or a larger allocation, before capital is committed is the first risk-management decision to make.

What position-sizing discipline actually looks like in practice

Diagnosis is useful. But the most immediately applicable tool for managing AI concentration risk is position sizing: setting explicit limits on how large any single name or theme can become within a portfolio.

The practical framework involves three parameters. First, a per-stock maximum weight: commonly 3-5% of total portfolio value for volatile names, with many investors using the lower end for semiconductor cyclicals. Second, an optional theme-level cap: total AI-related exposure capped at roughly 20-25% of portfolio value depending on risk tolerance. Third, a rebalance trigger: trim winners back to target weights when thresholds are breached rather than waiting for an annual review.

- Audit current weights: list each AI-related holding and its percentage of total portfolio value. Flag any name above the chosen cap.

- Identify names above threshold: any position that has grown beyond 3-5% through appreciation is a candidate for trimming.

- Set a rebalance schedule: quarterly or semi-annual reviews ensure drift does not recreate concentration over time.

The Broadcom selloff provides the live stress test. An investor holding 10-15% of their portfolio in a single name like Broadcom or Marvell experienced an outsized drawdown from a single earnings miss. At a 3-5% weight, the same event would have been a manageable drag rather than a portfolio-defining episode.

UBS has recommended that investors with concentrated AI exposure reduce single-name concentration while sustaining broader thematic exposure. This is a risk-management adjustment, not an anti-AI call.

Position sizing requires no forecasting ability. It works regardless of whether the stock rises or falls after the adjustment.

Rules-based chip stock discipline, including pre-set rebalance triggers and a hard single-name cap, is the mechanism that converts position-sizing principles into actual behaviour during drawdowns, since the Broadcom and Marvell selloffs of June 2026 produced exactly the kind of short-duration panic window in which investors without pre-committed rules are most likely to make permanent errors.

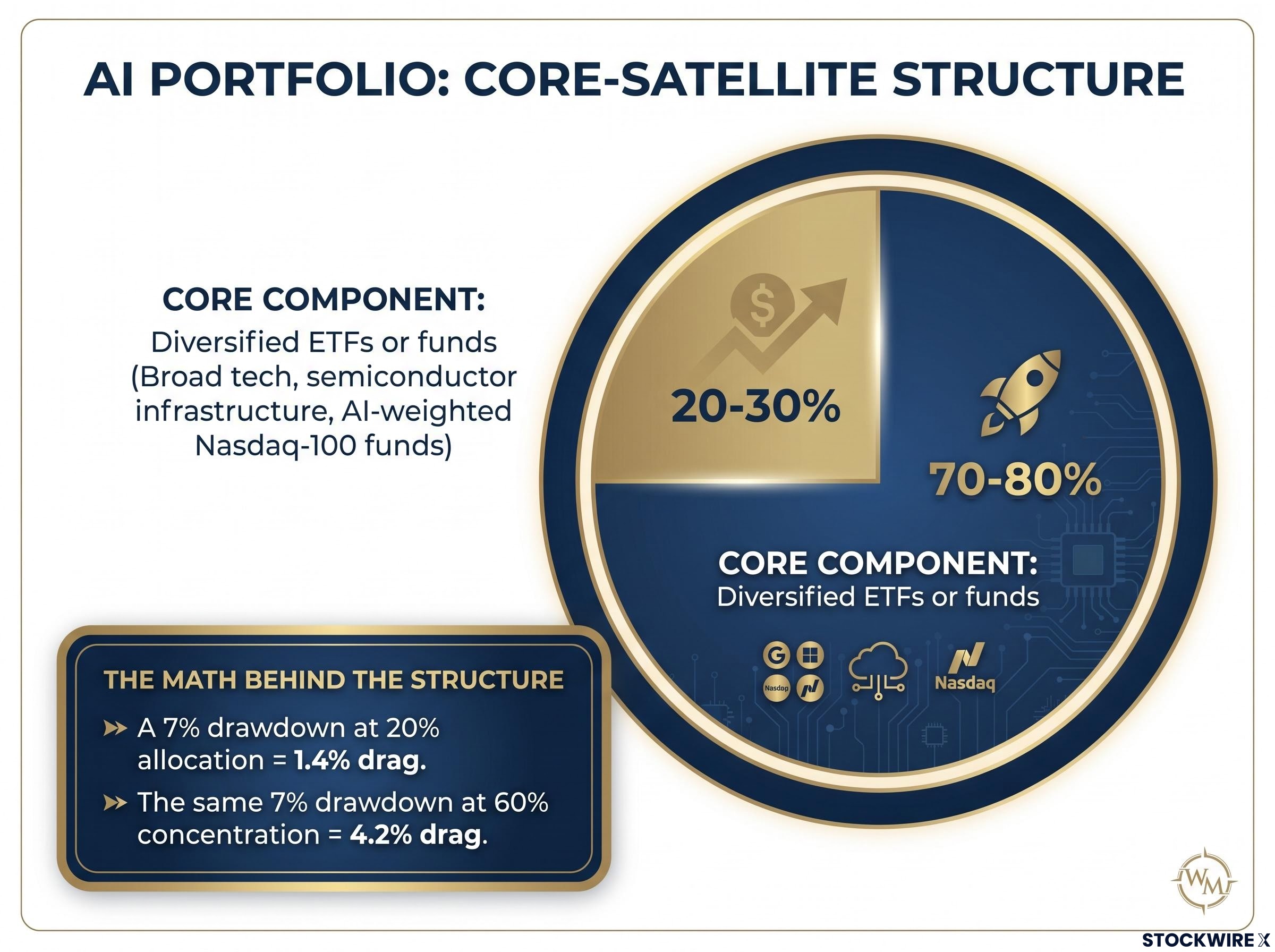

Using the core-satellite structure to stay in the theme without overexposing to it

The tension many investors feel is real: they want meaningful upside from AI but do not want a single earnings miss to define their year. The core-satellite structure resolves that tension with architecture rather than vague principles.

The core component, approximately 70-80% of the total AI allocation, sits in diversified ETFs or funds. Broad tech, semiconductor infrastructure, or AI-weighted Nasdaq-100 funds automatically spread exposure across dozens of names. When evaluating these vehicles, three criteria matter:

- Diversification: No single holding should dominate the fund’s weight

- Breadth across the AI value chain: Exposure should span chips, cloud, software, and applications, not only GPU vendors

- Cost discipline: High expense ratios erode returns over time, particularly in a long-duration theme

The distinction between broad tech or Nasdaq-100 ETFs (which are AI-heavy by construction) and narrower sector-thematic funds focused exclusively on semiconductors or AI infrastructure is worth noting. Broader funds provide more natural diversification; narrower ones concentrate the same risks the core is designed to diffuse.

Defining your satellite positions before you add them

The satellite component, approximately 20-30% of the AI allocation, is where higher-conviction single stocks sit. These are names where the investor has done deeper research and explicitly accepts higher volatility in exchange for alpha potential.

Each satellite position requires three parameters defined before capital is committed: a role (core versus satellite), a target weight, and an entry plan (lump sum versus staged). Without these pre-defined parameters, satellite positions tend to migrate toward core-sized weights after strong performance, which recreates the concentration problem the structure was designed to solve.

The maths illustrates why this works. A 7% drawdown in a satellite position representing 20% of the AI allocation produces a 1.4% drag on total AI allocation. The same move at 60% concentration produces a 4.2% drag. Structure absorbs the shock that concentration amplifies.

How to stage entries into new AI names, including high-profile IPOs

New AI opportunities will continue to emerge, including potential marquee listings. The enthusiasm around these additions is understandable; the risk is that enthusiasm compresses all decision-making into a single moment of peak market sentiment.

Staged entry, or dollar-cost averaging, is the default approach for high-profile AI additions. Spreading purchases over a defined period distributes the timing risk across multiple data points rather than concentrating it on one day.

Before adding any new AI name, a correlation check serves as the critical pre-entry discipline. If the new stock responds to the same capex, regulation, and earnings headlines as existing holdings, it may increase correlation risk more than it increases diversification.

- Define whether the new position is core or satellite

- Set a target weight consistent with the chosen framework

- Run a correlation check against existing holdings: does this name move on the same catalysts?

- Determine the entry plan: lump sum for high-conviction, uncorrelated additions; staged buying over a defined period for names with higher hype premiums

Correlation risk is often more dangerous than valuation risk for investors adding into an already AI-heavy portfolio. Paying a fair price for a name that doubles existing exposure accomplishes less than paying a modest premium for genuine diversification.

The OpenAI IPO example illustrates why staging matters for AI-native listings specifically. Hype and correlation to broader AI sentiment tend to be highest immediately after listing, making the first available trading day the riskiest moment to commit full capital. The macro signals to monitor when timing any AI addition include AI capex commentary from hyperscalers, GPU demand trends, profit margins across the AI complex, and policy and rate-path shifts.

The AI buildout is a multi-year story; your portfolio architecture should reflect that

US private AI investment of $109.1 billion in 2024 underlines the scale and durability of this buildout. The investors most likely to capture the full multi-year return are not the ones with the highest concentration today, but the ones who have built a structure resilient enough to hold through volatile episodes without being forced to sell at the wrong moment.

The five strategies in this guide distil into a single checklist that can be actioned this week:

- Audit current weights: list every AI-related holding and its percentage of total portfolio value

- Trim oversized names back to the chosen per-stock cap (3-5%), redeploying proceeds rather than exiting the theme

- Reallocate the core of AI exposure to diversified vehicles (broad tech ETFs, Nasdaq-100 funds, or AI-infrastructure funds with value-chain breadth)

- Define and cap satellite positions with explicit role, target weight, and entry plan parameters

- Set a quarterly rebalance schedule to prevent drift from recreating concentration over time

The macro factors worth monitoring remain consistent: AI-related capex commentary from hyperscalers, profit margins and demand trends across the AI complex, GPU pricing cycles, and policy and rate-path shifts that affect high-multiple equities.

The UBS recommendation and the strategies outlined here are explicitly not a bearish call on AI. They are a structural upgrade to how that exposure is held: broader, more deliberate, and built to endure the kind of single-session drawdowns that concentrated portfolios absorb as damage and diversified portfolios absorb as noise.

For investors who want a rigorous framework for assessing how much of the multi-year thesis remains intact before committing to the long-horizon positioning this article recommends, our deep-dive into AI bull market runway and risk signals examines Paul Tudor Jones’ 1-2 year horizon estimate, current semiconductor valuation multiples against dot-com era peaks, and the specific hyperscaler capex growth rate below which GPU name valuations become structurally unsupportable.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Investors with concentrated holdings or IPO participation decisions should consult a qualified financial adviser who can evaluate their overall portfolio, time horizon, and risk tolerance.