Mid-2026’s Biggest Market Risks, Ranked by Actual Probability

18 hrs ago

Most investors spend their energy trying to maximise returns. The investors who stay wealthy over decades tend to be those who engineered their portfolios to survive the scenarios that wipe everyone else out first. Three major crisis periods, 2008, March 2020, and 2022, each destroyed capital through a different mechanism: credit collapse, pandemic panic, and an inflation-driven simultaneous drawdown in both bonds and equities. A multi-asset ETF portfolio that survived all three could not have relied on any single asset class. It had to be built around regime diversification from the start. This guide walks through three proven allocation frameworks, explains how tail-risk hedging instruments like TLT and GLD fit into each, and provides a decision rubric for choosing the framework that matches an investor’s actual risk tolerance and time horizon.

Combining multiple ETFs does not automatically produce a diversified portfolio. Deliberate weighting across genuinely different economic regimes is what separates a portfolio designed for survival from one that merely looks diversified on a spreadsheet.

The 2022 drawdown exposed the gap. For decades, the standard 60/40 allocation relied on a historically negative correlation between equities and bonds: when stocks fell, Treasuries rose, cushioning the blow. That relationship broke when inflation surged and the Federal Reserve raised rates aggressively. Both equities and bonds declined simultaneously, punishing the very pairing most investors treated as their safety net.

The 60/40 correlation assumptions that went untested for four decades were stress-tested all at once in 2022, when inflation running above 8% forced the Fed into the fastest rate-hiking cycle in a generation and both legs of the classic pairing declined simultaneously.

Contrast that with 2008 and March 2020, when long-duration Treasuries did exactly what they were supposed to do, appreciating sharply as capital fled to safety during a credit crisis and a pandemic shock respectively. The lesson is not that bonds are broken. It is that no single correlation assumption holds across every regime.

“The investors who consistently outperform over time tend to be those with superior risk management frameworks rather than superior stock-picking or forecasting ability.”

The three frameworks in this guide are all built on the same design philosophy: optimise for risk-adjusted survival across growth, recession, inflation, and deflation rather than for maximum gain in any single environment. Understanding why conventional diversification fails in specific regimes is the prerequisite to understanding why each framework is structured the way it is.

Not all safe havens protect against the same kind of disaster. A portfolio that holds both TLT (long-duration Treasuries) and GLD (physical gold) is not holding redundant positions. It is holding insurance against two structurally different crisis types.

Tail-risk hedging refers to positions designed to gain value or preserve capital during the most extreme negative market conditions. These are not return engines in normal markets. They are positions sized to matter when everything else is falling apart.

TLT hedges deflationary recessions and financial panics, the scenarios where interest rates fall and capital rushes into government debt. It appreciated during the 2008 financial crisis and the March 2020 market disruption. Its weakness is inflation. When rates rose aggressively in 2022, TLT fell alongside equities, failing precisely the investors who expected it to provide shelter.

GLD hedges a wider range of crises: inflation spikes, currency debasement, geopolitical stress, and broad loss-of-confidence episodes. Gold performed during 2008, March 2020, the 2022 inflation spike, and a 2024 banking sector stress event. Its versatility across crisis types makes it a more broadly reliable hedge than TLT alone.

The structural gold thesis has gained institutional backing well beyond tactical price momentum: central banks purchased 244 tonnes of gold in Q1 2026 alone, and BlackRock, JPMorgan, and Swiss pension funds have each explicitly shifted allocations toward gold as bond diversification has eroded in high-debt environments.

“Think of TLT and GLD as insurance against different crisis types, not as return engines.”

A combined TLT/GLD allocation of 3-10% of total portfolio value represents a reasonable tail-risk hedging range. One note on alternatives: VIX-based products carry structural rolling costs from VIX futures contracts that erode value over time, making them unsuitable as long-term holdings.

| Dimension | TLT (Long-Duration Treasuries) | GLD (Physical Gold) |

|---|---|---|

| Crisis type hedged | Deflationary recessions, financial panics | Inflation spikes, currency debasement, geopolitical stress |

| 2008 performance | Appreciated as rates fell | Appreciated as confidence collapsed |

| March 2020 performance | Appreciated during pandemic flight to safety | Appreciated during broad market sell-off |

| 2022 performance | Declined alongside equities | Held value during inflation spike |

| Key weakness | Inflation shocks and rate-hiking cycles | Can lag in strong equity bull markets |

These three frameworks sit on a spectrum. At one end, equities dominate and the portfolio accepts larger drawdowns in exchange for long-run growth. At the other, equal-weight allocation across four asset classes sacrifices upside to keep volatility low. The right answer depends on where an investor’s own risk tolerance places them, not on which framework backtests best over a cherry-picked window.

One caution before the detail: pick one framework as a base. Blending elements of all three at once tends to produce a mushy, unfocused allocation that inherits the weaknesses of each without the coherence of any.

This is the growth-leaning end of the spectrum. It fits investors with a time horizon of 10-plus years whose primary goal is wealth accumulation and who can tolerate large drawdowns along the way.

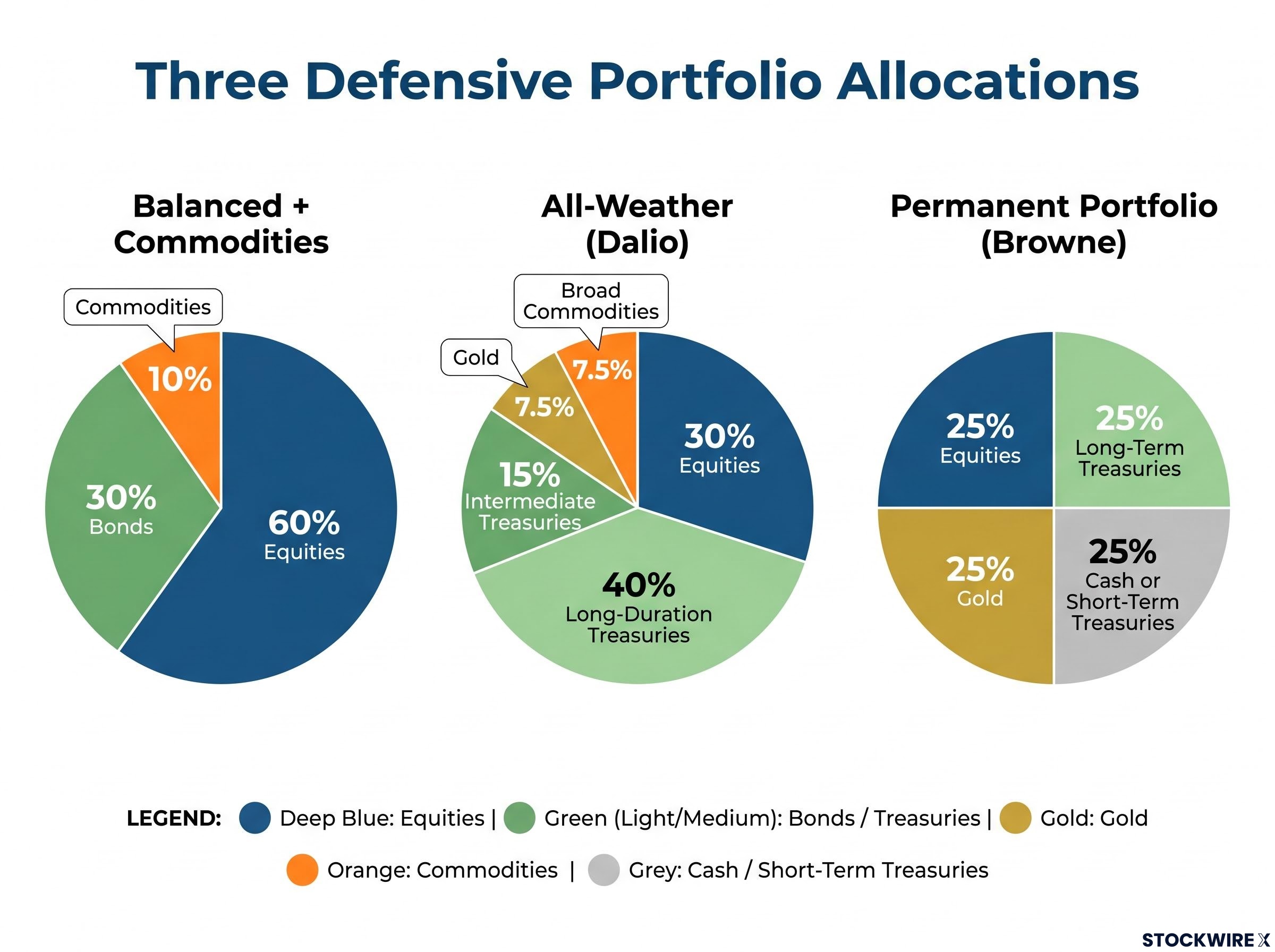

The typical allocation runs 60% equities, 30% bonds, and 10% commodities in the standard variant, or 75% equities, 15% bonds, and 10% commodities for a more aggressive tilt. Commodities add an inflation-protection element that a standard 60/40 allocation lacks. The core vulnerability remains equity dependence: when stocks fall hard, the portfolio falls hard with them.

Developed by Harry Browne in the 1980s, the Permanent Portfolio takes the capital-preservation philosophy to its logical conclusion: 25% equities, 25% long-term Treasuries, 25% gold, and 25% cash or short-term Treasuries.

The equal-weight design means no single regime can devastate the portfolio. The 25% gold and 25% cash allocations also make it psychologically easier to hold through crises, because one or both of those positions is almost always performing well when equities are falling. The explicit tradeoff: the Permanent Portfolio produces more modest long-run returns than a 60/40 allocation but with significantly lower realised volatility. Investors who choose it are accepting underperformance in boom times in exchange for resilience.

Developed by Ray Dalio and Bridgewater Associates, the All-Weather Portfolio is designed to deliver adequate performance across four major economic regimes: growth, recession, inflation, and deflation. Bonds tend to outperform during deflation and recessions; commodities provide inflation protection; gold benefits from currency debasement and periods of heightened uncertainty.

The typical allocation is approximately 30% equities, 40% long-duration Treasuries, 15% intermediate Treasuries, 7.5% gold, and 7.5% broad commodities. It suits mid-career investors approaching retirement who want smoother drawdowns and a single set-and-rebalance allocation.

The important nuance: All-Weather performed strongly in 2008 but struggled in years when equities and bonds declined simultaneously. Its 55% combined Treasury allocation made it particularly vulnerable to the 2022 inflation-and-rate-hike combination, a reminder that even regime-diversified frameworks have specific failure modes.

Investors drawn to the Dalio framework who want to understand its four-quadrant construction in depth before committing capital will find our full explainer on the All-Weather Portfolio covers the original risk-balancing logic, the 2022 failure mode in detail, and how the March 2025 ALLW ETF launch translates the approach into a single accessible vehicle.

| Framework | Equity allocation | Bond/rate allocation | Inflation hedge | Best crisis fit |

|---|---|---|---|---|

| Balanced + Commodities | 60-75% | 15-30% aggregate bonds | 10% broad commodities | Long-horizon growth with inflation buffer |

| All-Weather (Dalio) | 30% | 55% (long + intermediate Treasuries) | 15% (gold + commodities) | Deflationary recessions and financial panics |

| Permanent Portfolio (Browne) | 25% | 25% long Treasuries + 25% cash | 25% gold | Broad resilience across all regimes |

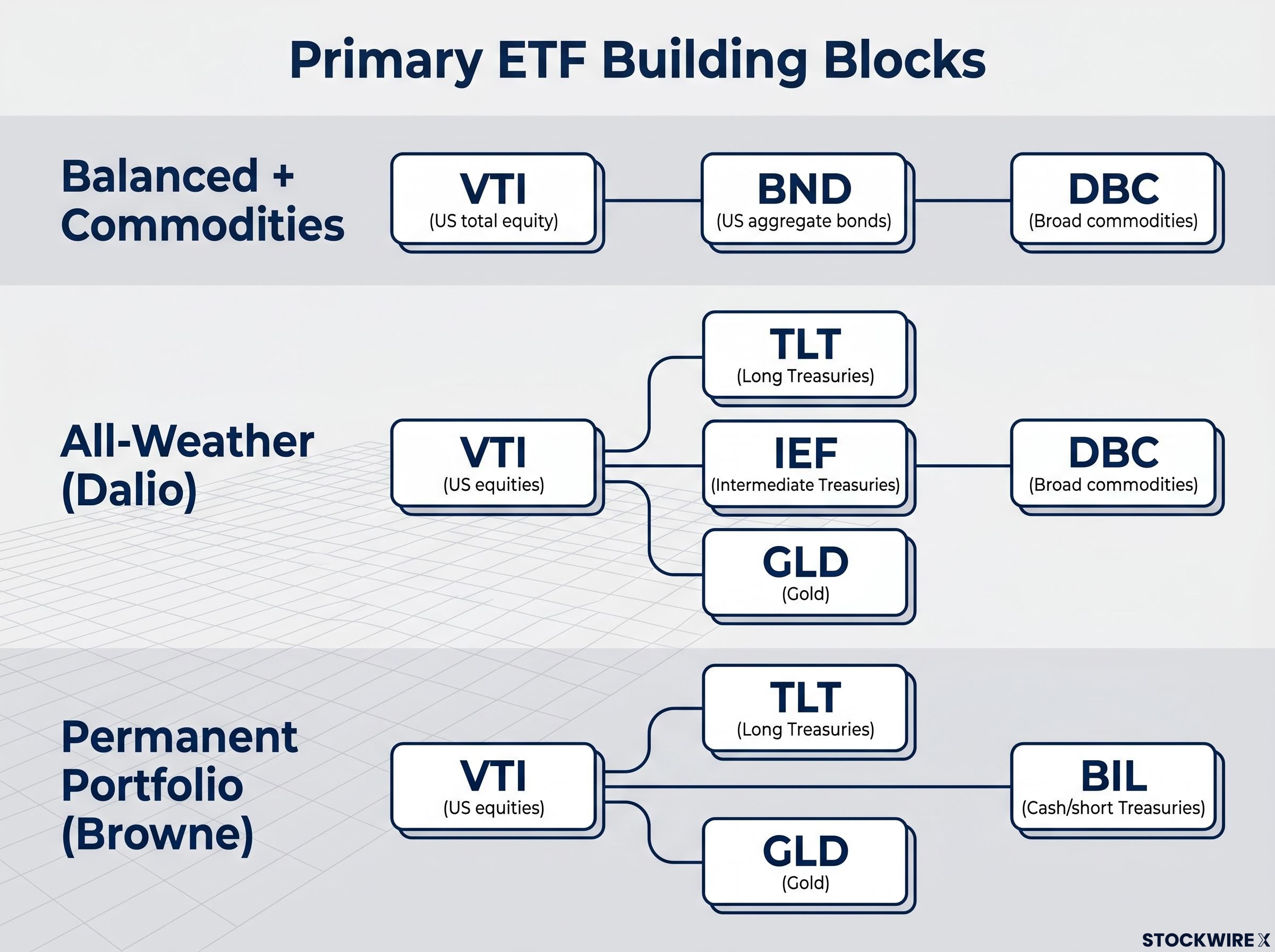

Abstract allocation percentages only become actionable when matched to specific funds. The preferred approach uses 3-5 funds total rather than 10-15 overlapping positions. Fewer holdings means cleaner rebalancing, lower costs, and less temptation to tinker.

All ETFs listed below are US-listed exchange-traded funds. Each asset class slot includes a primary choice and alternatives, because flexibility within the framework matters more than any single correct ticker.

| Framework | Asset class | Primary ETF | Alternatives |

|---|---|---|---|

| Balanced + Commodities | US total equity | VTI | SPY, IVV, VOO |

| US aggregate bonds | BND | AGG | |

| Broad commodities | DBC | COMT, PDBC | |

| All-Weather (Dalio) | US equities | VTI | SPY |

| Long Treasuries | TLT | ||

| Intermediate Treasuries | IEF | VGIT | |

| Gold | GLD | IAU, SGOL | |

| Broad commodities | DBC | COMT, PDBC | |

| Permanent Portfolio (Browne) | US equities | VTI | SPY |

| Long Treasuries | TLT | ||

| Gold | GLD | IAU, SGOL | |

| Cash/short Treasuries | BIL | SHV, SGOV |

The difference between a hedge that matters in a crash and one that barely registers is sizing. Too small, and the protection is cosmetic. Too large, and the hedge drags on returns in every normal year. The right size depends on which core framework is already in place, because the three frameworks carry very different levels of built-in crisis exposure.

There are two ways to implement the hedge layer: build the TLT and GLD positions into core target weights and rebalance them alongside everything else, or treat them as a separate insurance sleeve (for example, 90% core allocation, 10% hedges) rebalanced on its own schedule. The separate sleeve approach makes it easier to adjust hedge sizing without disrupting the core framework.

The overall reasonable range for tail-risk hedging across any framework is 3-10% of total portfolio value in TLT and GLD combined, calibrated so the positions matter in a severe drawdown but do not dominate portfolio behaviour in normal markets.

These portfolio frameworks only behave as designed with disciplined rebalancing. Without it, allocations drift. A portfolio that started at 25% equities can quietly become 40% equities after a strong bull run, undermining the very regime-diversification logic it was built on.

Portfolio drift is the silent risk that regime-diversified frameworks are most vulnerable to: after the three-year equity rally from 2022 lows, a portfolio that started at the All-Weather’s 30% equity target could have drifted to 40% or beyond without a single deliberate trade, fundamentally altering its crisis behaviour.

Rebalancing forces selling what just performed well and buying what just got hurt. That is emotionally difficult, which is precisely why it works: it mechanically enforces the contrarian discipline most investors cannot maintain on their own.

Three approaches, in order of simplicity:

For US investors, a tax efficiency note: more active rebalancing should be conducted inside tax-advantaged accounts (IRA, 401k) where possible. Rebalancing in taxable accounts can trigger capital gains events that erode the strategy’s after-tax returns.

No framework is universally superior. The right choice maps to an investor’s specific time horizon, risk tolerance, and willingness to accept underperformance in certain environments.

| Framework | Best fit investor profile | Primary strength | Main tradeoff |

|---|---|---|---|

| Balanced + Commodities | 10-plus year horizon, tolerates large drawdowns, primary goal is wealth accumulation | Highest long-run growth potential | Largest drawdowns during equity bear markets |

| All-Weather (Dalio) | Mid-career or approaching retirement, values smoother returns over maximum upside | Regime-balanced design for consistent performance | Vulnerable when inflation and rate hikes coincide; lags in strong bull markets |

| Permanent Portfolio (Browne) | Near or in retirement, very risk-averse, willing to accept lower returns for high resilience | Lowest volatility, psychologically easiest to hold | Underperforms equity-heavy approaches over long horizons |

The decision is not about which framework produced the best historical backtest over a single period. It is about which allocation an investor will actually hold through the environments that make it temporarily look wrong.

Four operating principles apply regardless of which framework is chosen:

Catastrophic drawdowns reset compounding. A 50% loss requires a 100% gain just to return to breakeven. The frameworks in this guide are designed to keep an investor in the game through 2008-type crashes, 2020-type panics, and 2022-type inflation shocks, so that returns can actually compound across decades rather than being periodically destroyed.

No single framework is universally superior. The choice depends on time horizon, risk tolerance, and whether the investor can hold their chosen allocation through the environments that make it temporarily look wrong. The first step is choosing one of the three frameworks as a base, then sizing the TLT and GLD hedge layer to match risk profile, and committing to annual or threshold-based rebalancing from there.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. The allocation frameworks and hedge-sizing ranges discussed are educational examples, not personalised recommendations.

A multi-asset ETF portfolio deliberately allocates across equities, bonds, commodities, and gold to provide resilience across different economic regimes, including growth, recession, inflation, and deflation. A standard 60/40 portfolio relies on a single correlation assumption between stocks and bonds that can break down when inflation surges, as it did in 2022.

The All-Weather Portfolio, developed by Ray Dalio and Bridgewater Associates, typically allocates 30% to equities, 40% to long-duration Treasuries, 15% to intermediate Treasuries, 7.5% to gold, and 7.5% to broad commodities, using ETFs such as VTI, TLT, IEF, GLD, and DBC. It is designed to deliver adequate performance across growth, recession, inflation, and deflation regimes rather than maximising returns in any single environment.

The Permanent Portfolio, developed by Harry Browne in the 1980s, allocates equally 25% each to equities, long-term Treasuries, gold, and cash or short-term Treasuries. It is best suited to near-retirees or very risk-averse investors who are willing to accept lower long-run returns in exchange for low volatility and broad resilience across all economic regimes.

The recommended range for combined TLT and GLD tail-risk hedging is 3-10% of total portfolio value, with the exact split depending on whether an investor is more concerned about deflationary recessions (favouring a larger TLT position) or inflation and currency risk (favouring a larger GLD position). Investors using the Permanent Portfolio typically need no additional hedging, as 25% gold and 25% long Treasuries are already embedded in the structure.

Annual rebalancing is the default approach for most investors, resetting all positions to target weights once per year, while threshold-based rebalancing triggers a reset whenever any major asset class drifts more than plus or minus 5 percentage points from its target. More frequent rebalancing activity is best conducted inside tax-advantaged accounts such as an IRA or 401k to avoid triggering capital gains events in taxable accounts.