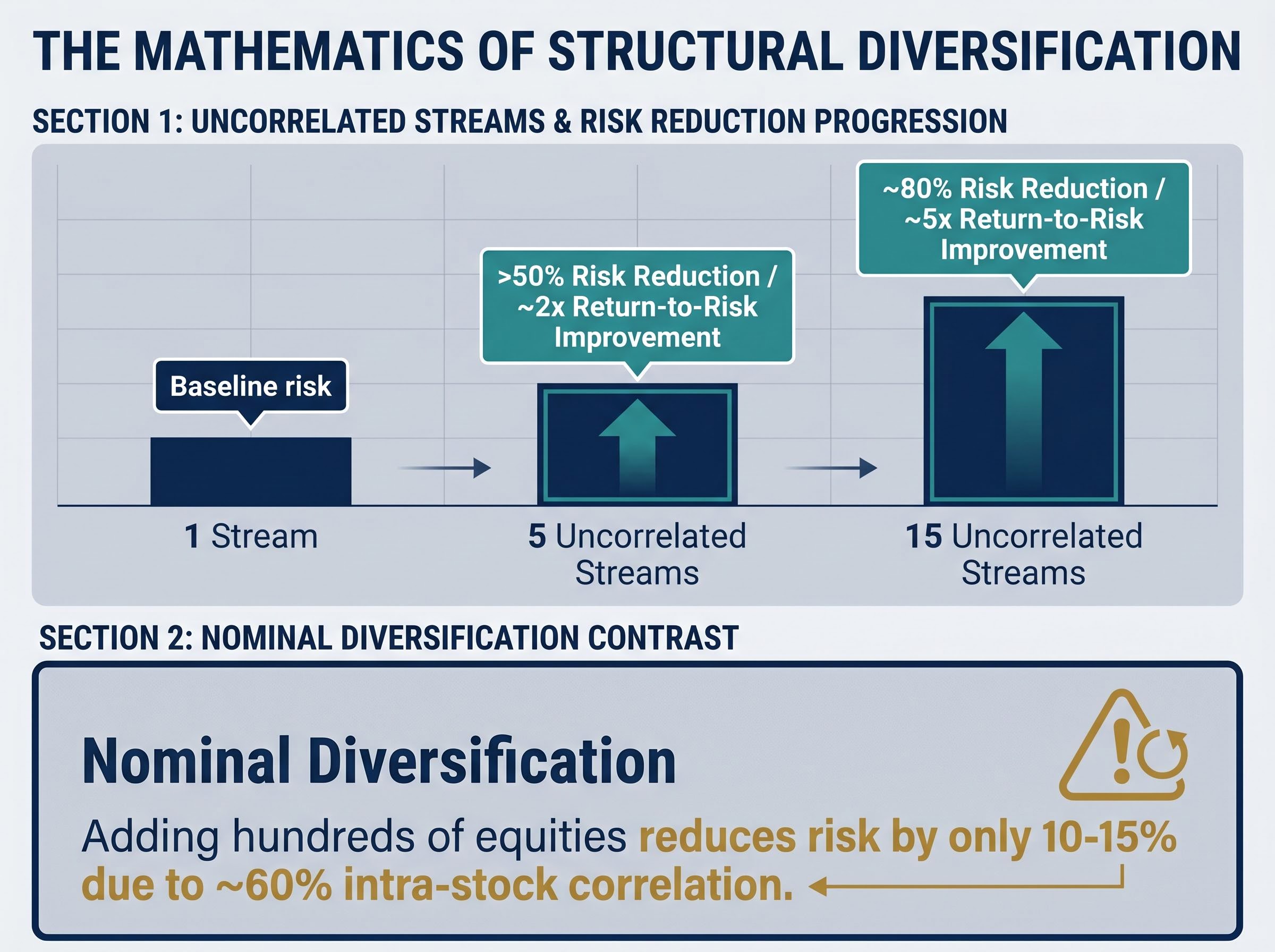

A portfolio of 15 uncorrelated return streams can reduce risk by approximately 80% and improve the return-to-risk ratio by roughly five times. Yet the overwhelming majority of investors diversify within a single asset class, capturing almost none of that mathematical benefit. Ray Dalio built Bridgewater Associates into one of the world’s largest hedge funds on this insight, and the All Weather Portfolio is its public expression: a framework designed to hold value across any combination of economic growth and inflation conditions. What follows is a clear walk through the four-quadrant philosophy that underpins the approach, the mechanics of risk balancing (which are not the same as nominal allocation), the canonical asset mix with its real-world performance record including the 2022 stress test, and the specific refinements that contemporary portfolio constructors are applying to modernise the strategy.

Why spreading across assets is not the same as being diversified

A typical stock carries approximately 60% correlation with the average of other stocks. In practical terms, that means adding hundreds of equities to a portfolio reduces risk by only 10-15%. The positions move together. The diversification is nominal, not structural.

The payoff changes dramatically when the return streams are genuinely uncorrelated. Five uncorrelated streams reduce risk by more than half. Fifteen reduce it by roughly 80%, improving the return-to-risk ratio by a factor of approximately five.

| Number of Uncorrelated Streams | Approximate Risk Reduction | Return-to-Risk Improvement |

|---|---|---|

| 1 | Baseline | Baseline |

| 5 | More than 50% | Approximately 2x |

| 15 | Approximately 80% | Approximately 5x |

The core mathematics: fifteen uncorrelated return streams can reduce portfolio risk by approximately 80% and improve the return-to-risk ratio by roughly five times, a benefit that no amount of intra-asset-class diversification can replicate.

This is the foundational insight behind the All Weather design. The goal is not to accumulate more positions. It is to identify return streams that do not move together, then balance risk across them. Bridgewater’s institutional implementation reflects this directly, with more than 100 distinct alpha strategies and approximately 130 different market positions at any given time.

Diversification, then, is a correlation problem, not a counting exercise. Readers evaluating their own portfolios can start here: how many genuinely uncorrelated return streams are present, and are they sized large enough to affect outcomes?

When big ASX news breaks, our subscribers know first

The two variables that drive every asset class

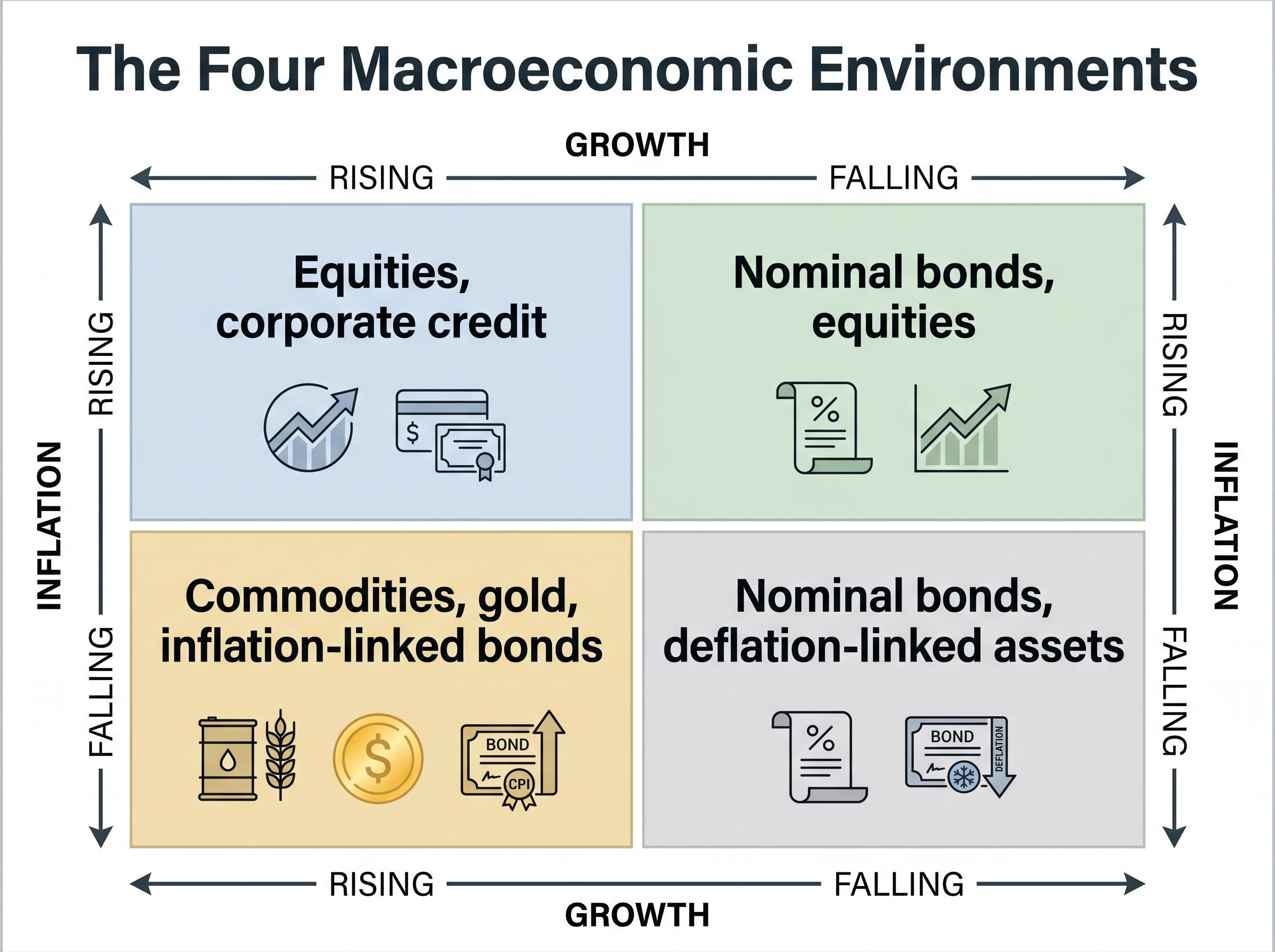

Asset class returns are primarily driven by two macroeconomic variables: growth and inflation. Each can either exceed or fall short of market expectations, producing four distinct environments that a portfolio must survive, not just the ones it prefers.

The logic has a structural foundation. Interest rates function as the universal discount rate applied across all asset classes. When rates rise, the present value of future cash flows falls regardless of what those cash flows represent, whether they come from equities, bonds, or real assets. After accounting for growth expectations, inflation expectations, discount rates, and liquidity premiums, what remains is the residual risk premium specific to each asset class.

The two-variable model works because growth and inflation each shift the discount rates and real cash flows that determine asset prices; inflation and purchasing power erosion act as a structural tax on nominal returns across equities, bonds, and cash simultaneously, which is precisely why a portfolio built to handle only one inflationary regime will underperform when price pressures become persistent.

Dalio and Bridgewater’s leadership continue to position this four-environment framing as the foundation of All Weather construction through 2024-2025, emphasising risk allocation by economic environment rather than fixed static weights.

What each economic season rewards

The four macro quadrants map directly to the asset classes that historically perform well within each regime.

| Economic Environment | Asset Classes That Historically Perform Well |

|---|---|

| Rising Growth | Equities, corporate credit |

| Falling Growth | Nominal bonds, deflation-linked assets |

| Rising Inflation | Commodities, gold, inflation-linked bonds |

| Falling Inflation | Nominal bonds, equities |

A conventional 60/40 portfolio is heavily weighted toward the rising-growth and falling-inflation quadrants. It carries little or no exposure to the environments where inflation exceeds expectations or growth disappoints simultaneously. That concentration is the structural vulnerability the All Weather approach was designed to address: not to predict which season is coming, but to hold meaningful exposure to all four.

The canonical All Weather allocation and the logic behind each position

The widely cited retail approximation of Dalio’s framework follows a 30/40/15/7.5/7.5 split across five asset classes. Each position fulfils a specific environmental role within the four-quadrant structure.

| Asset Class | Nominal Weight | Environmental Role | Macro Regime It Hedges |

|---|---|---|---|

| Equities | 30% | Growth exposure, long-term real returns | Rising growth, falling inflation |

| Long-term Treasuries | 40% | Deflation protection, growth disappointment hedge | Falling growth, falling inflation |

| Intermediate Treasuries | 15% | Lower-duration bond ballast | Falling growth |

| Gold | 7.5% | Inflation hedge, monetary disorder insurance | Rising inflation |

| Commodities | 7.5% | Broad inflation sensitivity | Rising inflation, rising growth |

The heavy bond weighting is the most frequently misunderstood element. Equity volatility is approximately twice bond volatility, so a 30% equity weight and a 55% combined Treasury weight do not represent a lopsided allocation toward bonds in risk terms. Once volatility is accounted for, the risk contribution from equities and bonds moves closer to balance. This is the distinction between nominal allocation and risk allocation, and it is the single concept that separates a coherent All Weather implementation from a naive copy of the percentage weights.

A few clarifications on what this allocation represents and what it does not:

- What it is: a retail approximation of the All Weather philosophy, widely circulated in investment-education materials through 2024-2025.

- What it is not: Bridgewater’s actual institutional implementation, which is proprietary, leveraged, and continuously refined. The firm does not publish detailed asset-class weights.

- What the ALLW ETF represents: launched in March 2025 by State Street in partnership with Bridgewater, the ALLW ETF is the first publicly accessible, officially Bridgewater-linked All Weather vehicle in ETF form.

The SPDR Bridgewater All Weather ETF launch announcement confirmed that the fund invests across domestic and international equities, nominal and inflation-linked bonds, and commodities, with Bridgewater co-CIO Karen Karniol-Tambour describing the vehicle as a way to broaden access to risk-balanced portfolio construction for a wider investor base.

What the 2022 stress test revealed about the strategy’s real limits

The 2022 environment delivered the precise scenario that exposed the framework’s structural vulnerability. Aggressive rate hikes in response to elevated inflation drove simultaneous equity and bond sell-offs, meaning the strategy’s two largest components moved together rather than providing the expected offset.

The performance record across 2022-2024 traces a clear three-phase arc:

- 2022 stress: a representative All Weather backtested implementation returned approximately -19%. The RPAR Risk Parity ETF recorded a drawdown of approximately -22.8%. The traditional 60/40 portfolio also suffered one of its worst years in decades, confirming this was not an All Weather-specific failure but a breakdown in the negative stock-bond correlation assumption that underpins most balanced portfolio designs.

- 2023 stabilisation: equities recovered and bonds provided partial ballast. RPAR recorded returns of approximately +6.0-6.3%. Diversification benefits began to re-emerge, though full recovery depended heavily on implementation details.

- 2024 plateau: RPAR returned approximately 0% to +0.1%. Results remained sensitive to leverage levels, commodity exposure, and duration choices. Renewed rate volatility confirmed that implementation specifics continued to drive outcomes.

Building portfolio resilience beyond the 60/40 framework has become the defining challenge for institutional and individual allocators alike, as the stock-bond negative correlation that underpinned both traditional balanced portfolios and the All Weather canonical weights has turned persistently positive during inflation-driven rate shocks.

Resonanz Capital risk parity performance analysis of the 2022 inflation shock records that the HFR Risk Parity Index dropped nearly 19.5% while the Bloomberg Aggregate Bond Index fell approximately 13%, providing third-party corroboration that the simultaneous equity and bond sell-off was a systemic breakdown rather than an All Weather-specific anomaly.

When inflation drives rates higher, equities and nominal bonds fall together, and the strategy’s core diversification assumption fails at the moment it is most needed. This is not a theoretical risk; it materialised in 2022 and persisted through the rate-hiking cycle.

Portfolios reliant primarily on nominal Treasuries for diversification suffered most. Those with larger commodity and TIPS (Treasury Inflation-Protected Securities, bonds whose principal adjusts with inflation) allocations performed relatively better during the same period. The lesson is not that the framework failed; it is that the specific implementation choice of concentrating 55% of nominal capital in Treasuries created a vulnerability that became visible under inflation-driven stress.

How the framework holds up, and where practitioners are updating the implementation

The four-quadrant logic for constructing balanced portfolios remains widely endorsed by portfolio construction specialists. What is contested is whether the canonical weights adequately express that logic when real yields are structurally higher than the environment in which the original allocation was popularised.

The 55% combined Treasury allocation (40% long-term plus 15% intermediate) was the primary source of underperformance during the 2021-2023 rate shock, and this exposure may remain unattractive if real yields stay elevated. The critique is structural, not cyclical.

Duration risk in bond portfolios is the mechanical reason the 55% Treasury allocation became the primary drag during 2021-2023: a bond with a duration of 7 loses approximately 7% in price for every 1 percentage point rise in rates, meaning the All Weather framework’s heaviest nominal allocation became its most rate-sensitive position precisely when inflation was accelerating.

Portfolio-construction specialists and asset managers in 2024-2025 have proposed several refinements:

- Reduce long-duration nominal bond exposure in favour of shorter-duration bonds plus TIPS

- Increase commodity and inflation-linked bond allocations to better hedge persistent inflation

- Add systematic macro and CTA (Commodity Trading Advisor) sleeves as additional uncorrelated return streams

- Incorporate global ex-US equities more explicitly rather than relying on a US-centric equity sleeve

- Implement dynamic risk budgets that reduce duration exposure when inflation shocks dominate

- Add value-tilted or resource-heavy equities as inflation-sensitive equity exposure

The core principle, balancing risk across macro environments, is retained across all of these proposals. What changes is the implementation, particularly the mix of nominal versus real assets.

The difference between the philosophy and the recipe

The four-quadrant risk-balancing philosophy is Dalio’s enduring contribution. The 30/40/15/7.5/7.5 weights are one expression of that philosophy at a particular moment in time, and treating the recipe as fixed misunderstands what the framework is.

Bridgewater’s institutional implementation has always been dynamic, proprietary, and leveraged. The retail approximation was always a simplification rather than a faithful replica. Dalio’s own 2024-2025 public commentary reinforces this distinction, emphasising high global debt levels, inflation-linked assets, real returns, and geopolitically diversified portfolios as extensions of the All Weather philosophy rather than departures from it.

The next major ASX story will hit our subscribers first

Building toward balance: what the All Weather logic means for real portfolio decisions

The practical takeaway from the All Weather framework is not a set of weights to copy. It is a diagnostic question: across the four macroeconomic environments, how exposed is a given portfolio to each, and where are the gaps?

The alpha-versus-beta distinction is directly relevant here. Beta returns arise from structural economic relationships and are accessible to any investor. Assets are structurally expected to outperform cash over long time horizons; without that premium, the economic system would not function.

Alpha generation is a zero-sum activity. Outperforming the market requires extracting returns from other participants. The All Weather framework emphasises diversified beta construction as the primary objective precisely because beta is structural, while alpha depends on being better than the other side of every trade.

The most common investor error is interpreting recent strong performance as evidence of quality rather than recognising it as a signal of elevated price. Systematic, rules-based decision-making, tested across all historical periods and geographies, provides a more reliable foundation.

A three-step diagnostic process translates the framework into practical evaluation:

- Identify current regime exposures. Map existing holdings to the four quadrants. A portfolio concentrated in equities and nominal bonds is effectively positioned for rising growth and falling inflation, with limited coverage elsewhere.

- Assess correlation structure rather than nominal weights. Two positions with 60% correlation contribute less diversification benefit than two positions with near-zero correlation, regardless of how they are sized.

- Evaluate whether uncorrelated streams are sized to matter. A 2% commodity allocation does not meaningfully affect portfolio outcomes during an inflation shock. Uncorrelated return streams, whether commodities, inflation-linked bonds, global equities, or systematic macro strategies, need to be present in sufficient size to influence results.

For readers ready to move from the All Weather diagnostic to active portfolio adjustment, our dedicated guide to portfolio rebalancing after equity drift covers how to identify when equity gains have shifted a portfolio beyond its intended risk level, the tax-efficient order of execution, and alternative destinations including private credit and market-neutral funds that offer genuinely lower correlation to public equities.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The principle endures; the implementation is yours to refine

The intellectual contribution of the All Weather framework is the four-quadrant risk-balancing logic and the mathematics of uncorrelated diversification, not a fixed set of weights to be replicated. Fifteen uncorrelated return streams reducing risk by approximately 80% is a mathematical relationship, not a market opinion. That relationship does not expire.

The 2022 lesson deserves honest acknowledgement rather than dismissal. The strategy experienced real drawdowns when its core diversification assumption broke down, and the appropriate response is to interrogate the implementation rather than abandon the philosophy.

Readers are now equipped to apply this logic to their own situation, whether that means adapting the canonical weights toward TIPS and commodities, incorporating systematic macro strategies as additional uncorrelated streams, or simply using the four-quadrant diagnostic as a lens for evaluating existing holdings. The natural next steps from here include deeper reading on risk parity implementation, TIPS as an inflation hedge, and the distinction between nominal and real asset allocation, each of which extends the framework explored in this guide.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.