In 2022, a typical 60/40 portfolio lost around 20%. The strategy was not poorly executed. The macroeconomic regime that had made it work for four decades had quietly shifted underneath it, and both sides of the allocation fell at the same time.

The stock-bond correlation, long the invisible engine of conventional diversification, turned positive when inflation spiked and central banks responded with the fastest rate rises since the early 1980s. Bond prices fell alongside equities rather than offsetting them. That episode did not kill the 60/40 portfolio, but it exposed a structural dependency that many investors had never tested and should now think carefully about.

What follows is an examination of why the 60/40’s diversification engine is regime-dependent rather than permanent, what a genuinely diversified portfolio requires in the current environment, and how time horizon and behavioural discipline shape outcomes at least as much as asset allocation ratios do.

The mechanism that made 60/40 work for decades was regime-dependent, not universal

For the better part of four decades, the 60/40 portfolio felt like financial physics. Equities provided growth. Bonds cushioned the falls. When recessions hit, central banks cut rates, pushing bond prices up just as equity prices dropped. The two asset classes moved in opposite directions, and the portfolio absorbed shocks with remarkable consistency.

Three specific macroeconomic conditions sustained that negative correlation:

- Inflation was low and relatively stable.

- Recessions were predominantly demand-driven, allowing rate cuts to act as an automatic stabiliser.

- Central banks retained significant capacity to lower rates in downturns, giving bonds room to rally.

Then 2022 arrived. Inflation spiked to multi-decade highs. Central banks responded with rapid rate hikes, the fastest since the early 1980s. Higher yields simultaneously compressed equity valuations and pushed bond prices down, so both sides of the 60/40 fell together. The correlation flipped positive precisely when diversification was needed most.

The BIS analysis of stock-bond correlation regimes documents how the relationship between equity and bond returns shifted from reliably negative to positive as inflation accelerated, providing an authoritative empirical account of exactly why the diversification engine that powered the 60/40 for decades became conditional rather than structural.

BlackRock has noted that in the current regime of higher, more uncertain inflation and supply-driven shocks, bonds have been less reliable as diversifiers when equities sell off.

The forces driving the current persistent inflation regime extend well beyond the 2021-2022 supply shock, with analysis of 150 years of inflation cycle data suggesting that inflation moves in sustained generational phases rather than mean-reverting quickly toward central bank targets.

The approximately 20% loss a typical U.S. 60/40 portfolio suffered was not a one-off anomaly. It was what happens when the assumption underneath the strategy, that stocks and bonds move in opposite directions, no longer holds. What broke was an assumption, not the concept of diversification itself.

When big ASX news breaks, our subscribers know first

Why bonds still belong in most portfolios, just not as the only defence

The temptation after 2022 was to abandon fixed income entirely. That impulse overcorrects.

The long-run record of the 60/40 is genuinely strong. From the mid-1980s onward, a 40% bond allocation materially reduced volatility while preserving most of the return of an all-equity portfolio. That history should not be dismissed, even if it should no longer be treated as an unconditional guarantee.

What has changed since the shock is worth noting. Bond yields are now meaningfully higher than in the 2010s, which improves prospective returns and provides more income cushion. There is also some evidence that stock-bond correlations are partially normalising as the 2022 shock recedes.

The institutional consensus has settled in a specific place: do not discard bonds, but do not treat them as the sole diversification mechanism, particularly against inflation and supply shocks.

When bonds still do their job

High-quality government bonds retain their traditional defensive role in specific scenarios:

- Demand-driven recessions, where central banks cut rates and bond prices rally as equities fall.

- Deflation or growth scares, where flight-to-quality flows push government bond prices higher.

- Equity valuation shocks, where quality sovereign bonds benefit from risk-off positioning.

Duration calibration matters within these scenarios. Longer duration provides more recession hedge but amplifies rate risk in inflationary environments. The case for bonds is conditional, and investors who understand those conditions are better positioned to calibrate, not eliminate, their fixed income exposure.

Investors wanting to translate these principles into specific fixed income decisions will find our dedicated guide to bond duration calibration in a normalising rate environment, which covers how duration affects price sensitivity, where major institutional managers are currently positioning on the yield curve, and the specific instruments available for shortening duration without exiting fixed income entirely.

True diversification is about behaviour under stress, not the number of holdings

A portfolio can hold dozens of line items and still be concentrated in a single risk. This is the difference between genuine diversification and its cosmetic counterpart: owning assets that behave differently under specific macro scenarios versus owning more assets that all respond to the same underlying forces.

Multiple equity funds, whether domestic, international, or thematic, are still predominantly equity beta under the hood. In a major equity bear market, almost all of them fall together. Many labelled “alternatives” and private strategies end up highly correlated with equities during crises, often paired with higher fees and lower liquidity. Research indicates that many portfolios, despite appearing diversified across holdings, remain concentrated in the same underlying risk factors and macroeconomic sensitivities.

Cosmetic diversification is risk concentration in disguise.

The more productive question is not “what should I add?” but “does this actually behave differently when I need it most?” Three evaluative questions sharpen the diagnosis:

- Does this holding tend to move in the opposite direction to the core portfolio in the specific scenarios that matter most (inflation, recession, liquidity crisis)?

- Is it liquid and accessible when rebalancing or raising cash becomes necessary?

- Do the fees and structure leave enough net benefit to justify inclusion?

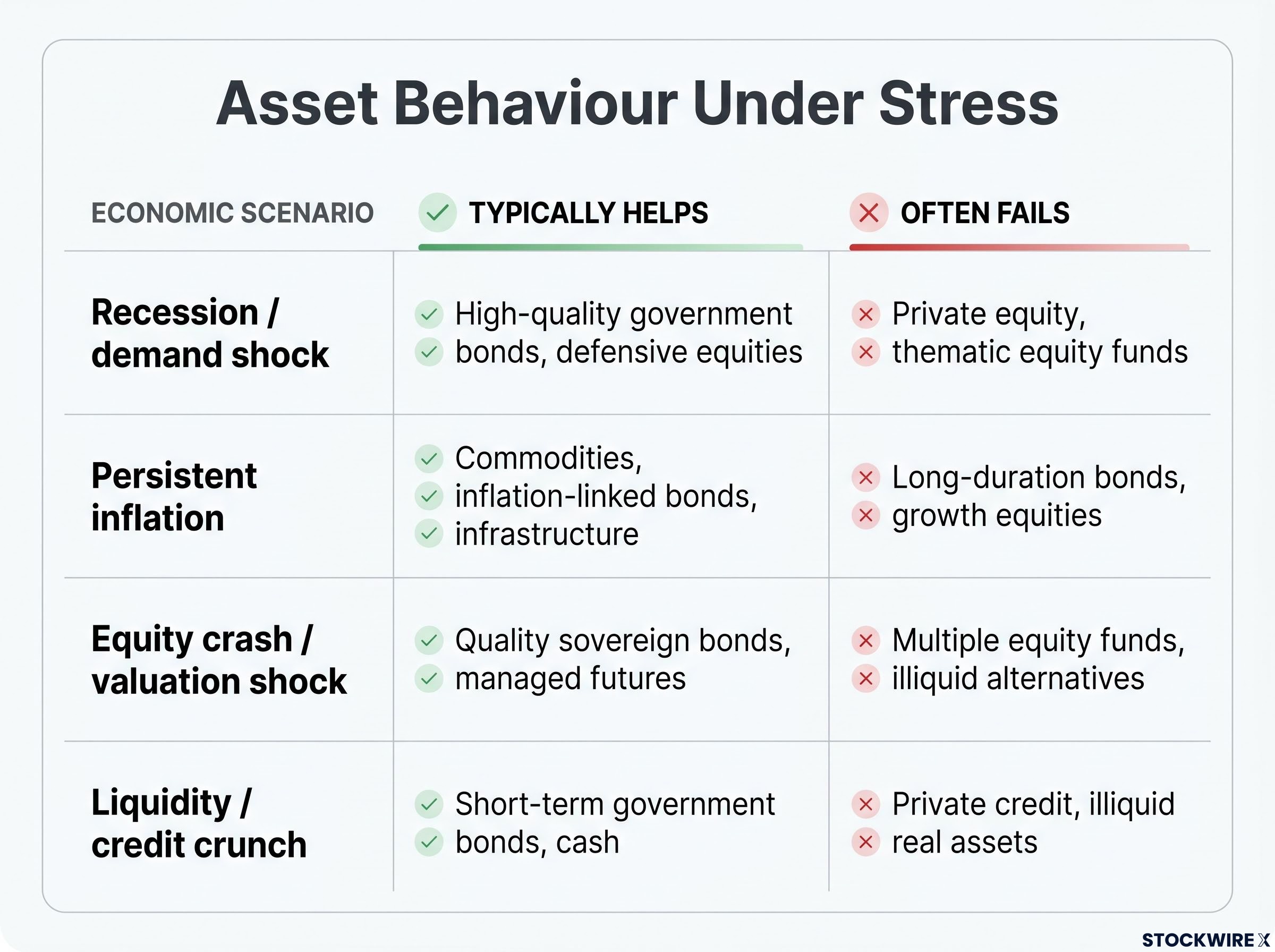

| Scenario | Typically Helps | Often Fails to Diversify |

|---|---|---|

| Recession / demand shock | High-quality government bonds, defensive equities | Private equity, thematic equity funds |

| Persistent inflation | Commodities, inflation-linked bonds, infrastructure | Long-duration bonds, growth equities |

| Equity crash / valuation shock | Quality sovereign bonds, managed futures | Multiple equity funds, illiquid alternatives |

| Liquidity / credit crunch | Short-term government bonds, cash | Private credit, illiquid real assets |

This framework offers a more durable analytical lens than simply counting holdings or asset classes.

Building a portfolio designed for multiple regimes, not just recessions

The limitation of the traditional 60/40 is not that it fails, but that it is primarily a recession hedge. It protects best when growth slows and central banks can cut rates. It does not inherently hedge inflation or policy-regime shifts.

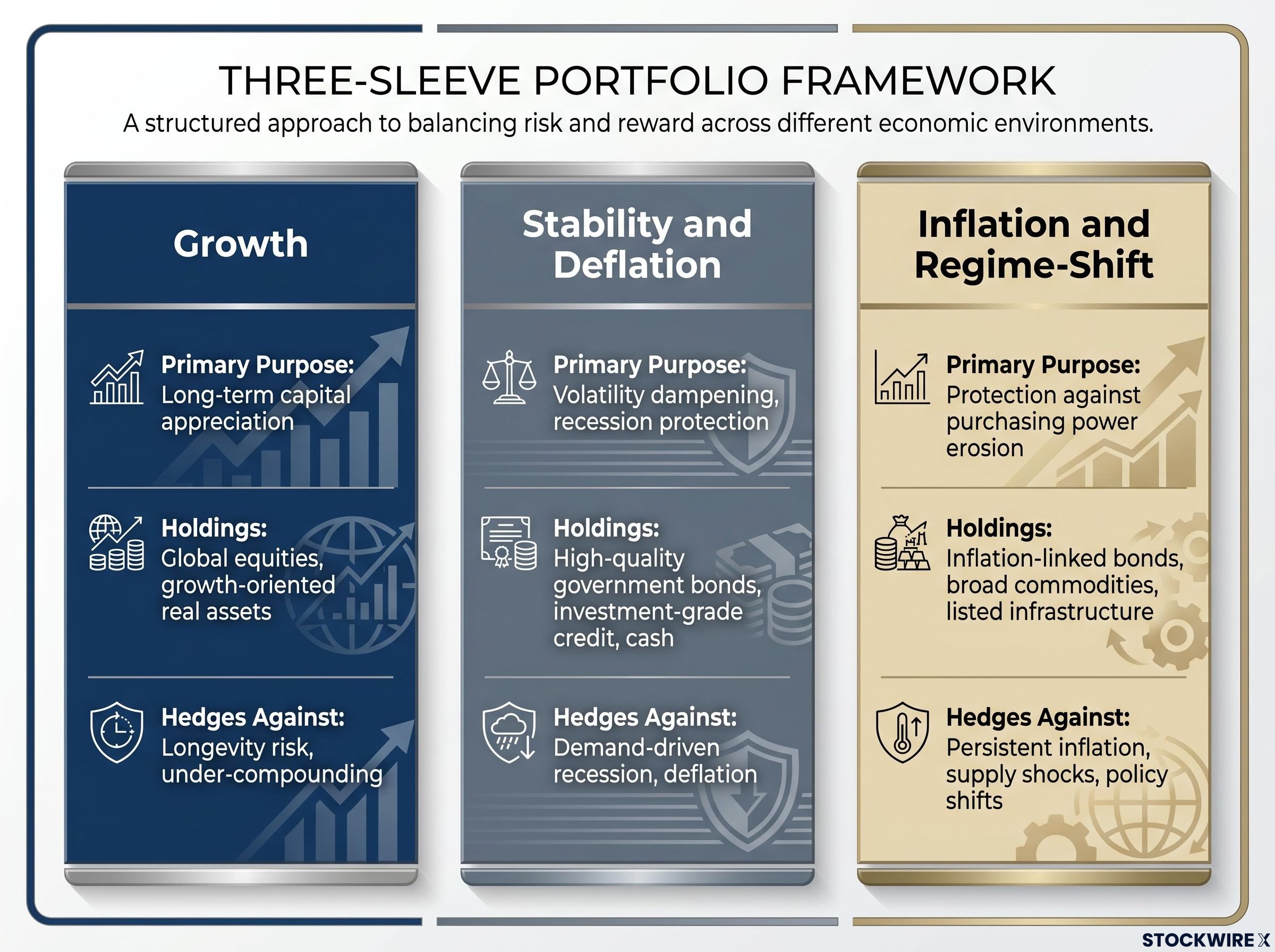

A three-sleeve framework offers a design logic, not a fixed allocation, that addresses this gap:

| Sleeve | Primary Purpose | Representative Holdings | Scenario It Hedges |

|---|---|---|---|

| Growth | Long-term capital appreciation | Global equities, growth-oriented real assets | Longevity risk, under-compounding |

| Stability and Deflation | Volatility dampening, recession protection | High-quality government bonds, investment-grade credit, cash | Demand-driven recession, deflation |

| Inflation and Regime-Shift | Protection against purchasing power erosion | Inflation-linked bonds, broad commodities, listed infrastructure | Persistent inflation, supply shocks, policy shifts |

The third sleeve is the structural addition that the traditional 60/40 lacks. Inflation-linked bonds, broad commodities, and listed infrastructure serve a specific role in this framework.

The design goal is not to bet on inflation, but to avoid having the entire portfolio impaired by it.

Alternatives such as managed futures or market-neutral strategies may warrant inclusion, but only when they demonstrate clear low correlation to core stock and bond risk, offer reasonable liquidity, and deliver net-of-fee value. Complexity should be added sparingly and deliberately. The proportions of each sleeve depend on an individual investor’s goals, horizon, and circumstances.

Time horizon is not a detail; it is the answer to almost every asset allocation question

Two investors can look at the same macro environment and need genuinely different portfolios. The difference is not opinion. It is time horizon.

| Dimension | Younger Accumulator (30s-40s) | Pre-Retiree / Early Retiree |

|---|---|---|

| Primary Risk | Under-compounding over decades | Large early drawdowns during withdrawals |

| Portfolio Priority | Long-term growth capture | Stability, income, and liquidity |

| Allocation Orientation | Growth-heavy with modest inflation hedges | Bucketed: 3-5 years of withdrawals in cash/short bonds, remainder in bonds and growth |

| Key Behavioural Risk | Market timing and constant tinkering | Panic selling growth assets during drawdowns to fund spending |

For investors with multi-decade horizons, elevated valuations may be of lesser consequence because long-term compounding remains the primary return driver. For retirement-phase investors drawing regular income, the emphasis shifts toward stability and downside protection, with a bucketed approach (approximately 3-5 years of withdrawals in cash, short bonds, or equivalent instruments) providing a structural solution to sequence-of-returns risk.

MIT Sloan research on sequence-of-returns risk demonstrates that the timing of poor returns relative to withdrawal events, not average portfolio performance alone, is the primary threat to retirement portfolio sustainability, which is why the bucketed approach described here addresses a structurally different problem than standard volatility reduction.

Sebastian Mullins, Head of Multi-Asset and Fixed Income at Schroders Australia, noted at the Morningstar Investment Conference that professional multi-asset managers typically operate within shorter time horizons and focus on limiting drawdowns and smoothing return profiles, objectives that differ substantially from those of most individual investors.

This distinction matters. Individual investors should exercise caution when drawing on professional investors’ portfolio positioning, as those decisions reflect materially different mandates and constraints.

The behavioural edge may matter more than the allocation ratio in a lower-return world

A technically well-diversified portfolio that cannot be held through a drawdown will underperform a simpler portfolio that the investor actually stays with.

Action bias, the psychological drive to trade or rebalance in response to volatility, typically generates more damage than the market environment itself would have caused. A genuinely diversified portfolio will always contain something that appears to be underperforming at any given moment. That is a structural feature, not a signal to change course.

Panellists at the Morningstar Investment Conference observed that behavioural discipline may become an increasingly significant determinant of outcomes if future returns are more subdued, because the cost of major mistakes rises in a lower-return environment.

Investors wanting to quantify what this costs in practice will find our full explainer on loss aversion and investor returns, which draws on Morningstar’s ‘Mind the Gap’ research to document a consistent 1-2 percentage point annual return shortfall and walks through the three pre-commitment tools that interrupt the bias before it reaches the sell button.

Three practical safeguards help contain action bias:

- Pre-define target ranges for each sleeve (growth, stability, inflation) and establish specific rebalancing triggers before volatility arrives.

- Automate contributions and rebalancing where possible, removing the decision point that invites emotional interference.

- Judge diversification by its behaviour during periods of market stress, not by how every holding performs during a rally. In a truly diversified portfolio, something will always look disappointing.

The redesign imperative: scenario-based thinking over fixed ratios

The real upgrade from a mechanical 60/40 is not a new magic ratio. It is a different design process.

- Start with goals, horizon, and withdrawal needs to establish risk capacity.

- Map the economic scenarios that threaten those goals: recession, persistent inflation, geopolitical shock, policy shift.

- Build a portfolio with distinct sleeves that each help in different scenarios, rather than relying solely on bonds to offset equity risk.

- Use alternatives sparingly and deliberately, only where they add clear diversifying risk exposures net of fees and liquidity costs.

- Put a simple behavioural framework around the portfolio so it can be held through drawdowns without panicked changes.

Macro regime shifts driven by structural forces beyond the business cycle, including the re-emergence of mercantilist industrial policy and the concentration of AI capital expenditure, are compressing the windows in which any single portfolio configuration remains optimal, reinforcing the case for explicit regime-awareness in allocation design.

The 60/40 is not dead. It remains a useful reference point and starting place for portfolio construction. The critique is not that the ratio is wrong, but that it should be treated as one point on a design continuum rather than a terminal destination. Exact allocations must be tailored to individual circumstances, and the five-step process above provides a framework for that tailoring.

What the 60/40’s limits reveal about the future of portfolio design

The assumptions beneath the 60/40 portfolio must now be actively managed rather than passively inherited. The negative stock-bond correlation that powered four decades of returns was a product of specific macroeconomic conditions, not a permanent feature of markets.

Three factors are likely to separate stronger portfolio outcomes from weaker ones in the current environment: explicit inflation sensitivity built into portfolio structure, time-horizon-anchored design that matches allocation to actual goals and withdrawal needs, and behavioural discipline that allows a well-constructed portfolio to survive the drawdowns it was built to withstand.

The investors most likely to navigate this environment well are those who treat diversification as an ongoing analytical process rather than a fixed product. The 60/40 asked one question: how much in stocks, how much in bonds? The question now is broader: which risks threaten my specific goals, and does my portfolio have a distinct response to each of them?

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.