Mid-2026’s Biggest Market Risks, Ranked by Actual Probability

3 mins ago

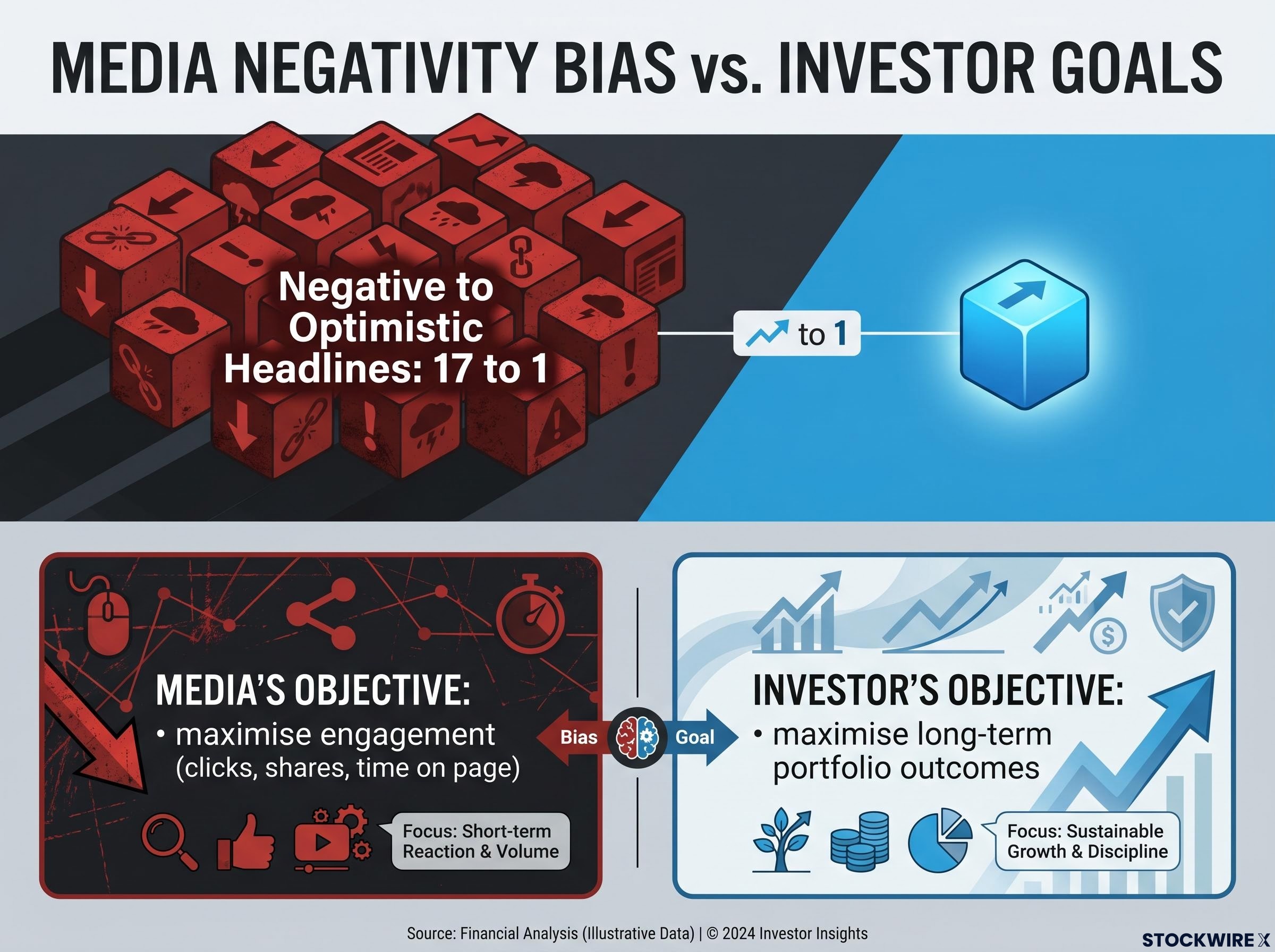

Negative financial headlines outnumber optimistic ones by a ratio of roughly 17 to 1. That asymmetry is not an accident, and it is not neutral. It reflects a structural feature of the media industry: fear drives engagement more reliably than optimism, and engagement is the metric that pays the bills. For investors, this creates a chronic information problem. The daily flow of financial content is meaningfully more pessimistic than actual market outcomes warrant, and the human brain is wired to treat that pessimism as signal rather than noise. What follows is a breakdown of why that wiring exists, how it damages portfolio decisions in measurable ways, and what a practical, evidence-based approach to financial media consumption looks like. Readers who finish the piece will carry one durable mental model: how to separate the media’s job from their own.

Negativity bias is not a quirk. It is a foundational feature of human cognition. Bad news captures attention faster, persists longer in memory, and weighs more heavily on decisions than equally significant good news. From an evolutionary standpoint, this made sense: the ancestor who overreacted to a rustling bush survived more often than the one who shrugged it off.

The weight that bad news carries is not imaginary: loss aversion in investing has been formally documented since Kahneman and Tversky’s 1979 prospect theory research, which found that losses register as roughly twice as painful as equivalent gains, a ratio that maps almost precisely onto how negative financial headlines disproportionately capture investor attention.

The foundational academic case for this asymmetry is laid out in Bad Is Stronger Than Good, a landmark synthesis by Baumeister, Bratslavsky, Finkenauer, and Vohs, which documents across multiple domains of psychology how negative events, emotions, and information carry disproportionately greater weight on attention and decision-making than equivalently positive ones.

The problem is that modern financial media activates this same wiring deliberately. Content featuring disaster, distress, and negativity generates significantly higher social media engagement than upbeat material.

Engagement asymmetry: Research consistently shows that content framed around distress, disaster, and negativity outperforms upbeat material on social media by a wide margin, reinforcing editorial incentives to lead with fear.

Eye-tracking studies confirm the pattern at the individual level. User attention gravitates toward negative content, with terms like “crash” ranking among the highest-attention words in financial headlines. The click-data pattern around terms such as “Warren,” “Buffett,” and “crash” illustrates the dynamic in miniature: the word “crash” does not appear because it is analytically useful. It appears because it pulls eyeballs.

This is not a personal failing. It is a predictable collision between ancient psychology and a profit-optimised content machine. Recognising the mechanism is the first step toward neutralising it, because investors who understand why their attention snaps toward negative headlines can begin to separate the emotional reaction from the analytical one.

The scale of the imbalance is worth sitting with.

The ratio: Negative financial headlines are published approximately 17 times more frequently than optimistic ones, based on survey data.

That is not a slight editorial lean. It is a structural feature of the industry. And social platforms compound the raw publishing asymmetry by algorithmically amplifying alarmist content, because that content drives the engagement metrics the platforms are optimised to maximise.

The result is a persistent misalignment between two objectives:

These are not the same goal. They are not even loosely aligned. A headline engineered to provoke a fear response and a headline engineered to inform a capital allocation decision will almost never look the same. Investors who internalise the 17-to-1 ratio stop expecting financial media to function as a balanced source of market intelligence. That single recalibration changes how every subsequent headline is processed.

The psychological phenomenon described above is not merely uncomfortable. It has a direct, measurable cost, and that cost compounds over time through three distinct damage pathways.

The permanent avoidance trap differs from normal risk aversion. Risk aversion is a calibrated decision about how much volatility to accept. The avoidance trap is a fear-driven posture in which rare, memorable market events (a crash, a prolonged bear market) are treated as the default expectation rather than the historical exception.

Cognitive biases at market extremes do not operate in isolation: loss aversion, herd behaviour, recency bias, and overconfidence form an interlocking feedback loop that intensifies precisely when media coverage is most alarmist, amplifying each individual bias through the social proof of observing others panic-sell.

Investors caught in this trap are effectively paying a continuous cost, the foregone equity premium, to insure against discomfort rather than against ruin. Occasional unexpected adverse outcomes are an unavoidable aspect of investing and should be accepted as such, not used to justify permanent market avoidance. The volatility that triggers the avoidance response is uncomfortable but historically survivable. The cost of never participating is not.

Most investor anxiety is generated not by reports of what has happened but by forecasts of what might happen. A headline reporting a 3% market decline is unsettling. A confident prediction of a 40% crash over the next two years is paralysing. The distinction matters because the forecast carries an authority it has not earned.

Markets are complex adaptive systems affected by unknown future events, technologies, and policies that cannot be modelled with confidence over a one-to-ten year horizon. Confident long-term forecasts, especially dire ones, have been characterised by experienced market practitioners as “self-deceptive.” They are narratives designed to attract attention, not tools for building an investment plan.

The practical discipline is straightforward. Commentators making long-term market predictions should be treated with calibrated scepticism, not deference. When encountering a forecast that triggers the urge to act, two questions slow the cognitive jump from “this sounds bad” to “I must change my portfolio”:

The calibration test: 1. How often has this kind of event actually occurred historically? 2. How many similar predictions in the past proved accurate?

In most cases, the answers are “rarely” and “very few.” That does not mean the forecast is impossible. It means the forecast does not warrant the level of certainty it was written with, and it certainly does not warrant an immediate portfolio change.

Diagnosis without prescription is incomplete. The question after understanding the bias is: what does a better daily habit look like?

The core principle is a structured daily review focused on one diagnostic question: what actually happened that affects existing holdings? This question separates news (concrete events that alter fundamentals) from commentary (opinions about what might happen). Almost all commentary should drive further analysis, not immediate trades. On most days, existing investment positions will not require modification because the underlying conditions that justified them remain intact.

The threshold for portfolio action is a genuine change in fundamentals, not a change in the emotional temperature of media coverage. The following decision framework translates this principle into specific situations:

| Situation | Correct Response |

|---|---|

| Scary headline appears | Check whether fundamentals have actually changed |

| Confident long-term forecast (especially dire) | Treat as narrative, not actionable data |

| Strong urge to sell during a downturn | Ask whether the investment case has changed, not how bad the coverage feels |

| Social media amplifying a “crisis” | Recognise engagement incentives; seek base-rate data |

| No genuine fundamental change detected | Do nothing; periodic rebalancing only |

Information diet curation reinforces the habit. Prefer sources that:

The final layer is portfolio resilience built before the next scary headline arrives. Align allocation with risk tolerance, time horizon, and concrete goals. Diversify properly. Plan for occasional drawdowns in advance. Once that structure is in place, most days require doing nothing, periodic rebalancing, and reviewing whether goals or life circumstances have changed, not whether the media’s emotional temperature has shifted.

For investors who want to move from the diagnostic framework above to a concrete allocation structure, our dedicated guide to building portfolio resilience examines how the breakdown of the stock-bond correlation has changed what diversification actually means in practice, and what a three-tier adaptive portfolio looks like across different economic environments.

Every section of this article points toward a single structural observation.

The media’s job is to maximise engagement. The investor’s job is to maximise long-term outcomes. These are not aligned objectives.

That misalignment is not temporary. It is built into the business models on both sides. Recognising it is the foundational mental move, because it changes the default posture toward every alarming headline from “this is a signal to act” to “this is a prompt to think.”

Thinking means checking fundamentals. It means checking historical probabilities. It means checking the plan that was built when emotions were calm. It does not mean ignoring the news. It means processing it through a filter calibrated to the investor’s actual objective, not the publisher’s.

The investors who perform best over time are not those who consume the most news or make the boldest calls. They are those who consistently dampen their emotional reactions to a chronically negative information environment. That discipline is quieter than conviction and less dramatic than a market call. It also compounds.

The historical case for long-term investment strategies rests on a simple but easily forgotten fact: the S&P 500 has returned approximately 9.43% annually over 150 years with dividends reinvested, a return that was available only to investors who remained in the market through every alarming news cycle, not those who exited at the moments of peak media fear.

Structural negativity bias in financial media is a documented, quantifiable phenomenon. It is not a perception problem, and it is not going away. The media environment is, if anything, likely to become more attention-competitive and more fear-framed over time as platforms optimise further for engagement.

The practical framework is simple to state and difficult to sustain: audit the information diet, apply the fundamental-change test before acting on any headline, and treat the emotional temperature of media coverage as a signal about the publisher’s engagement incentives, not about portfolio risk.

Investors who build this discipline early hold a compounding advantage. Not because they know more, but because they react less. Every headline that fails to trigger an unnecessary trade is a small act of portfolio preservation. Over years, those small acts add up to the most consequential investment decision most people never realise they are making: the decision to stay invested through discomfort.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Negativity bias in investing is the tendency for investors to give disproportionate weight to bad financial news over equally significant good news, a cognitive pattern rooted in evolutionary psychology that causes fear-driven reactions such as panic selling or avoiding equities altogether.

Financial media publishes far more negative headlines because fear-framed content generates significantly higher engagement through clicks, shares, and time on page, and engagement is the core metric that drives advertising revenue, creating structural incentives to lead with alarm rather than balance.

Negativity bias damages portfolios through three pathways: it causes inexperienced investors to sell into downturns at a loss, it misallocates mental bandwidth away from genuine opportunities, and in its most severe form it keeps investors out of equities entirely, forfeiting the long-term equity premium.

Investors can apply a fundamental-change test before acting on any headline, asking whether the underlying investment case has actually changed rather than whether media coverage feels alarming, and treating confident long-term forecasts as narrative rather than actionable data.

The permanent avoidance trap occurs when rare but memorable market events such as crashes are treated as the default expectation rather than historical exceptions, causing investors to stay out of equities indefinitely and pay a continuous cost in foregone returns rather than a calibrated cost for genuine risk management.