Why Seeing Machines Trades Below 5p Despite EU Mandate Wins

10 hrs ago

US luxury spending has accelerated from 6% in Q1 2026 to 17% quarter-to-date as of mid-June, according to Barclays strategist Emmanuel Cau. At the same time, the largest FIFA World Cup in history kicked off across North America on 11 June 2026, bringing 48 teams and 104 matches to three host nations over six weeks. For European consumer stocks, two catalysts are now arriving simultaneously.

European consumer-facing equities have underperformed since geopolitical stress began reshaping portfolio allocations. Investors rotated toward defensives, energy, and defence, leaving luxury, leisure, sportswear, and food names under-owned and still trading below pre-conflict price levels. That light positioning is creating a setup where even moderate positive surprises could force disproportionate repositioning by benchmark-tracking investors.

What follows is a breakdown of exactly which European consumer sectors stand to benefit from the World Cup and the luxury spending recovery, why each sector could surprise to the upside, and what the “pain trade” concept means for investors currently underweight these names.

Luxury, leisure, food, and general retail have all underperformed since the onset of the conflict and remain below pre-conflict price levels, according to Barclays. Capital has concentrated in defensives, energy, and defence names, leaving consumer-facing sectors structurally under-owned relative to benchmarks.

Contrarian buy signals embedded in record-low consumer sentiment readings have historically coincided with market bottoms rather than the start of sustained declines, a pattern visible in the 2022 Michigan Consumer Sentiment trough, where the index hit its lowest reading as equity markets were already beginning their recovery.

That underperformance is not simply a warning. It is the mechanism that creates the opportunity.

The compression in consumer discretionary, luxury, and travel names is part of a broader pattern: the STOXX Europe 600 has lagged the S&P 500 by roughly 9 percentage points since February 2026, and the mechanics of European equity sector rotation, including elevated short positioning and the specific catalysts that could force a rapid unwind, are directly relevant to how quickly the current setup could resolve.

Barclays’ Emmanuel Cau has characterised European consumer-facing sectors as presenting the most compelling catch-up opportunity within Europe, given still-low investor positioning and evidence that market leadership is beginning to broaden.

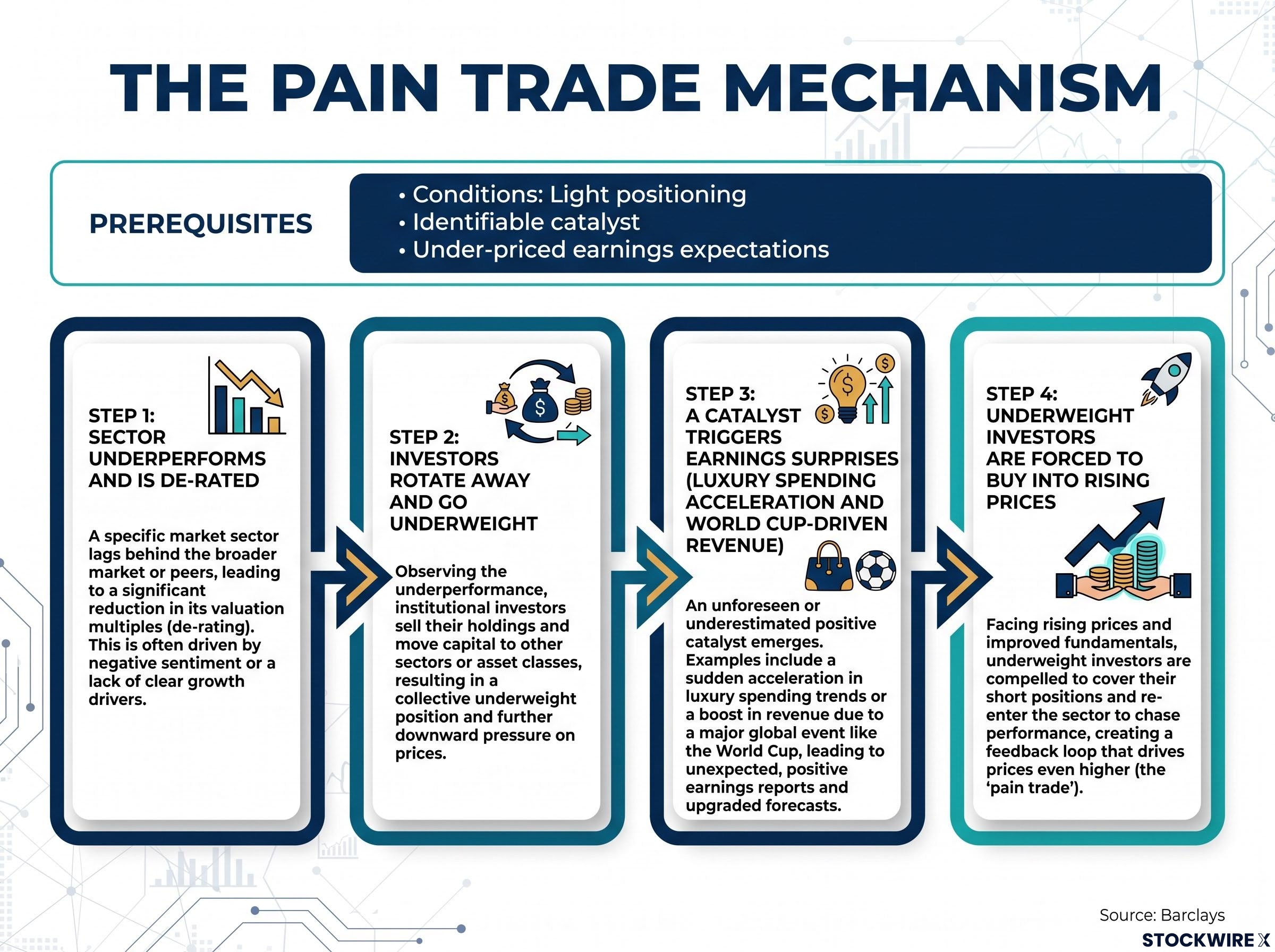

When positioning is this light, a dynamic known as the pain trade can emerge. Three conditions define the setup:

When all three conditions are present, underweight investors who see prices rising are forced to buy into the move to avoid falling further behind their benchmarks. This amplifies price appreciation beyond what the fundamental improvement alone would justify. For European consumer sectors, all three conditions currently hold.

The 2026 FIFA World Cup is not a repeat of prior tournaments at a larger venue. It is a structurally different event. The expansion from 32 to 48 teams produces 104 total matches (72 group stage plus 32 knockout), co-hosted across Canada, Mexico, and the United States. The tournament began on 11 June 2026, with the final scheduled for 19 July 2026.

| Feature | 2022 (Qatar) | 2026 (North America) |

|---|---|---|

| Teams | 32 | 48 |

| Matches | 64 | 104 |

| Duration | 4 weeks | ~6 weeks |

| Host region | Middle East | North America (3 nations) |

More matches mean more viewership hours, more merchandise windows, more betting events, and a longer consumption occasion across every market where fans are watching.

FIFA’s Socioeconomic Impact Analysis projects up to $40.9 billion in additional GDP for North America from the tournament.

That figure flows through to individual corporate revenue lines across hospitality, retail, media, payments, and advertising. For European companies with heavy exposure to North American and global consumer markets, the tournament registers as a measurable earnings catalyst, not a sentiment story.

The FIFA-WTO socioeconomic impact study, conducted by OpenEconomics, estimates that the 2026 tournament could generate up to $40.9 billion in additional GDP for North America and create nearly 824,000 jobs globally, giving corporate revenue projections across hospitality, retail, and media a concrete macroeconomic foundation.

Seven European consumer sectors sit in the path of these dual catalysts. They range from the most directly event-linked plays through to second-order volume beneficiaries, and each carries a different exposure profile.

| Sector | World Cup exposure | Key revenue driver | Positioning signal |

|---|---|---|---|

| Sportswear / Athleisure | Direct | Kit sales, branded merchandise, collaborations | Minimal optimism priced in |

| Luxury goods | Direct | US spending acceleration, East Asian momentum | Under-owned, below pre-conflict levels |

| Travel and leisure | Direct | Transatlantic traffic, hotel pricing | Limited positive expectation |

| Food and beverages | Indirect | Match-day consumption, branded mix shift | Cyclical upside underpriced |

| Media and advertising | Indirect | Ad revenue, subscriptions, broadcast rights | Low positioning |

| Gaming / Sports betting | Direct | Betting volume from 104 matches | Minimal optimism embedded |

| Payments / Fintech | Second-order | Aggregate transaction volume across all categories | Volume sensitivity underestimated |

Sportswear and athleisure represent the most direct equity expression of the World Cup cycle. Replica kit sales, limited-edition footwear, and brand collaborations create a front-loaded revenue surge that can also clear existing inventories and lift operating leverage. Barclays specifically identifies sportswear as a beneficiary with minimal optimism currently priced into valuations.

Luxury goods carry the most structurally significant opportunity. US luxury spending at 17% quarter-to-date, up from 6% in Q1 2026, signals accelerating demand. Parts of East Asia are also showing continued spending momentum, driven by wealth effects from AI-related and equity market gains. European-listed luxury groups, with heavy exposure to both geographies, stand to deliver better-than-feared revenue growth if these trends hold.

Travel and leisure groups participate through transatlantic air traffic, global hotel chains with assets in host cities, and online booking platforms. A strong summer of sports supports broader leisure sentiment globally, not just in host countries.

World Cups are proven consumption occasions. With 104 matches across six weeks, the match-day spending window for beer, soft drinks, snacks, and ready-to-eat foods is unusually extended. European food and beverage groups with global brands typically see volume uplifts and a favourable mix shift toward higher-margin branded products.

Media groups benefit from the advertising and subscription spike that live sports reliably delivers. Broadcast rights, highlight packages, and ad-supported platforms can all exceed short-term expectations even in a sector often treated as structurally challenged.

Gaming and sports betting operators are high-beta to the expanded format. The jump from 64 to 104 matches amplifies betting volumes relative to prior tournaments. Barclays identifies gaming as a beneficiary sector with minimal optimism currently embedded in valuations.

Payments and fintech firms sit at the second-order level, benefiting from the aggregate transaction volume generated across all other categories: ticketing, travel, hospitality, retail, and betting. Their operational leverage runs to transaction volumes rather than any single spending category, making them a broad-based play on event-driven economic activity.

The pain trade is not a fundamental re-rating. It is not an argument that these stocks are deeply mispriced on a standalone valuation basis. It is a positioning phenomenon, and it follows a specific sequence.

Investor crowding within European consumer segments remains light, according to Barclays, with limited speculative excess that would need to be unwound before a recovery can gain traction. This is a distinction worth noting: sectors where speculative positioning has already built up tend to stall or reverse on good news, as early buyers take profits. Sectors where positioning is genuinely light tend to accelerate.

European small-cap under-ownership has a structural dimension beyond the conflict-driven rotation: Barclays strategists published a June 2026 report showing that extreme hedge fund short positioning in European equities has created a mechanical snap-back trade whenever AI-momentum longs are unwound, with domestic industrials, regional financials, and consumer discretionary names identified as the clearest sector-level expressions of the thesis.

The clearest pain trade candidates, according to Barclays, are luxury goods, sportswear, selected travel and leisure, beverages and food, and gaming and sports betting, with media and payments as additional angles depending on risk appetite and time horizon.

The thesis is specific. So should the monitoring framework be. Confirmation and risk signals both deserve attention before any repositioning decision.

Three data points carry the most weight in validating the dual-catalyst setup:

Earnings guidance language from European luxury, sportswear, and leisure companies will also matter. Management commentary on whether they are seeing confirmation of the spending acceleration can move positioning quickly.

Barclays has indicated that further recovery is possible if the broadening of market leadership continues. The converse also holds: if leadership narrows again toward defensives and energy, the pain trade may take longer to play out.

For investors wanting to stress-test the luxury spending acceleration data against the broader macro picture, our full explainer on US consumer spending durability examines the divergence between strong April 2026 retail figures and historic lows in consumer optimism, covering the savings depletion dynamic and the K-shaped divide between affluent and mass-market households that is currently inflating aggregate spending metrics.

The World Cup runs through 19 July 2026. US luxury spending is tracking at 17% quarter-to-date, up from 6% in Q1. FIFA projects up to $40.9 billion in additional GDP for North America from a 104-match tournament. These are not abstract tailwinds. They are time-bounded, measurable catalysts converging on a set of sectors where investor positioning is at its lightest in years.

The same light positioning that has kept European consumer stocks under-owned is the mechanism that could make any recovery self-reinforcing. Underweight investors who wait for confirmation risk buying into prices that have already moved, which is precisely the pain trade dynamic that Barclays has flagged.

Two catalysts are arriving simultaneously in a defined six-week window. Investors underweight European consumer sectors face a specific, identifiable risk: being forced to buy at higher prices if the recovery broadens further.

The opportunity is not a general call on European equities. It is a specific, time-sensitive case for reassessing exposure to luxury, sportswear, travel, food, media, gaming, and payments names within a window that closes on 19 July.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements regarding spending trends and sector performance are subject to market conditions and various risk factors.

The pain trade refers to a positioning phenomenon where investors who are underweight a sector are forced to buy into rising prices to avoid falling behind their benchmarks, amplifying returns beyond what fundamental improvement alone would justify. Barclays has flagged this dynamic for European consumer stocks given light positioning, identifiable catalysts, and under-priced earnings expectations.

The 2026 World Cup features 104 matches across six weeks, up from 64 matches in 2022, creating an extended consumption window for sportswear, food and beverages, media, gaming, and travel names. FIFA projects up to $40.9 billion in additional GDP for North America from the tournament, which translates into measurable revenue uplifts for European companies with exposure to those markets.

Barclays identifies luxury goods, sportswear, selected travel and leisure, beverages and food, and gaming and sports betting as the clearest beneficiaries, with media and payments as additional angles. Each sector combines light investor positioning with direct or indirect exposure to both the luxury spending acceleration and World Cup-driven demand.

US luxury spending has accelerated from 6% in Q1 2026 to 17% quarter-to-date as of mid-June 2026, according to Barclays strategist Emmanuel Cau. Parts of East Asia are also showing continued momentum driven by wealth effects from AI-related and equity market gains, providing a second geographic demand pillar for European luxury groups.

Key risks include a deterioration in consumer confidence driven by macroeconomic data or geopolitical escalation, a reversal in East Asian equity markets that removes the wealth-driven luxury spending momentum, and gaming regulatory developments that could cap betting volumes in major markets. If market leadership narrows back toward defensives and energy, the positioning unwind could also take longer to materialise.