The SpaceX IPO Was a Stress Test for Space Stocks, Not a Catalyst

45 mins ago

The trade that has defined global equity markets for two years, long U.S. AI and technology names and short Europe, is now so crowded that any partial unwind mechanically forces capital back into European stocks. That is the assessment Barclays strategists published on 10 June 2026, in a report titled “More than just AI.” Led by Emmanuel Cau, the Barclays European Equity Strategy team framed European equities not as a growth bet but as a structural hedge against the unwinding of AI-momentum exposure. The positioning backdrop is the starting point: hedge funds and trend-following strategies have built one of the most lopsided long-U.S., short-Europe setups in recent memory, and the mechanics of that crowding create a specific, observable asymmetry. What follows is an examination of how that asymmetry works, which catalysts could trigger it, and which small-cap sectors are best positioned to capture the resulting capital flows.

The positioning picture is not a static snapshot. It has been building pressure in one direction for months. Hedge fund and CTA positioning has shifted to net short Europe and net long the United States, reversing from the stance held at the start of the conflict period. Barclays frames this reversal as an “improving technical backdrop” for European equities, and the logic is straightforward: the further positioning stretches in one direction, the more violent the snapback when it reverses.

This is the “pain trade” dynamic. When positioning is this one-sided, a sharp European rally forces systematic strategies to cover shorts in a self-reinforcing loop. Short-covering drives prices higher, which triggers further covering from trend-following systems calibrated to momentum signals, which drives prices higher still.

The catalyst does not need to be dramatic. Three types of shifts are sufficient to set the unwind in motion:

Any one of these can begin the covering cycle. The signal to monitor is the extreme long AI, short Europe setup itself; once that begins to normalise, Europe is the mechanical beneficiary.

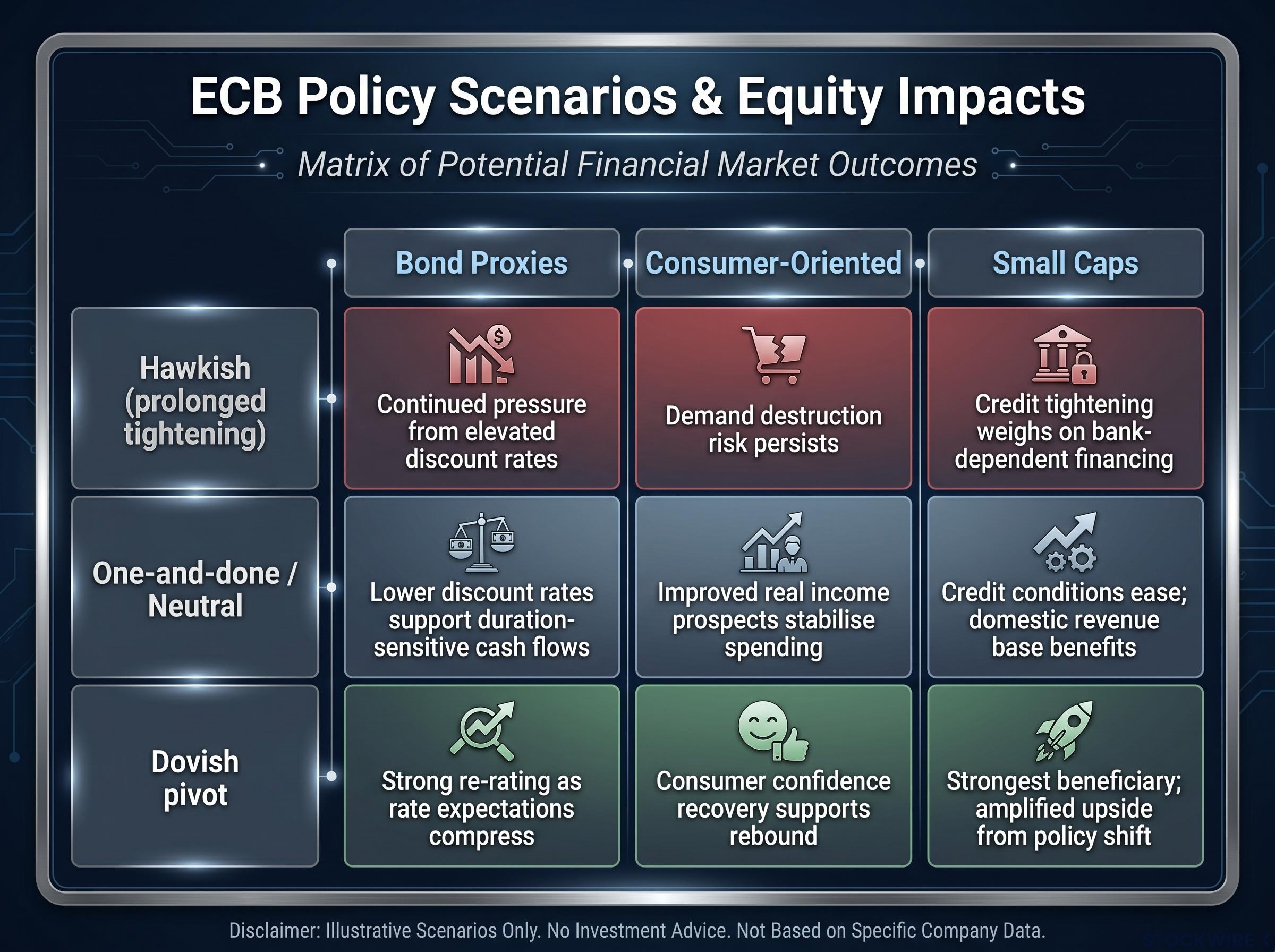

The positioning unwind has its own catalyst, but it is not the only pathway. The European Central Bank (ECB) provides an independent trigger that does not require the AI trade to fall apart at all. Barclays frames a less-hawkish ECB path, described as a “one-and-done” or moderated tightening scenario, as a near-term catalyst that lowers the perceived terminal rate and eases concerns about prolonged restrictive policy.

The equity categories that respond most directly to this shift vary by their sensitivity to rates and domestic conditions.

| ECB Scenario | Bond Proxies | Consumer-Oriented | Small Caps |

|---|---|---|---|

| Hawkish (prolonged tightening) | Continued pressure from elevated discount rates | Demand destruction risk persists | Credit tightening weighs on bank-dependent financing |

| One-and-done / Neutral | Lower discount rates support duration-sensitive cash flows | Improved real income prospects stabilise spending | Credit conditions ease; domestic revenue base benefits |

| Dovish pivot | Strong re-rating as rate expectations compress | Consumer confidence recovery supports rebound | Strongest beneficiary; amplified upside from policy shift |

Small caps warrant particular attention here. Their financing is more bank-dependent than large caps, their revenue is more domestically oriented, and their responsiveness to changes in credit conditions is higher in both directions. ECB policy is a discrete, observable variable; investors who track ECB signalling closely can use it as a timing mechanism for building European exposure rather than waiting for a broader AI unwind.

For the better part of two years, hedge funds and commodity trading advisors (CTAs), which are systematic trend-following funds, expressed bullish AI views by going long U.S. technology and momentum stocks. Those positions needed funding. Europe, with its weaker growth profile, higher energy dependence, and absence of large-cap AI leadership, became the natural short-funding vehicle.

That arrangement was not primarily a judgement on European corporate earnings. It was a positioning artefact: the cheapest, most liquid way to fund a concentrated long bet on one side of the market was to short the other. Europe fit the role structurally, and capital flowed accordingly.

Barclays characterised European equities as potentially serving as an “anti-momentum hedge or portfolio diversifier” in the current environment.

The consequence is an asymmetry that works in Europe’s favour on any reversal. When a fund decides to reduce AI exposure, it must simultaneously cover the European short that funded the position. That covering produces mechanical buying pressure in European markets regardless of whether the macro backdrop has changed. Euro area equity valuation multiples have compressed by roughly one turn since the onset of the conflict referenced in the Barclays analysis, and the EU versus U.S. price-to-earnings ratio remains near historic lows on a sector-adjusted basis as of June 2026. Europe is not just cheap; it is structurally positioned to benefit from any rotation out of crowded AI longs.

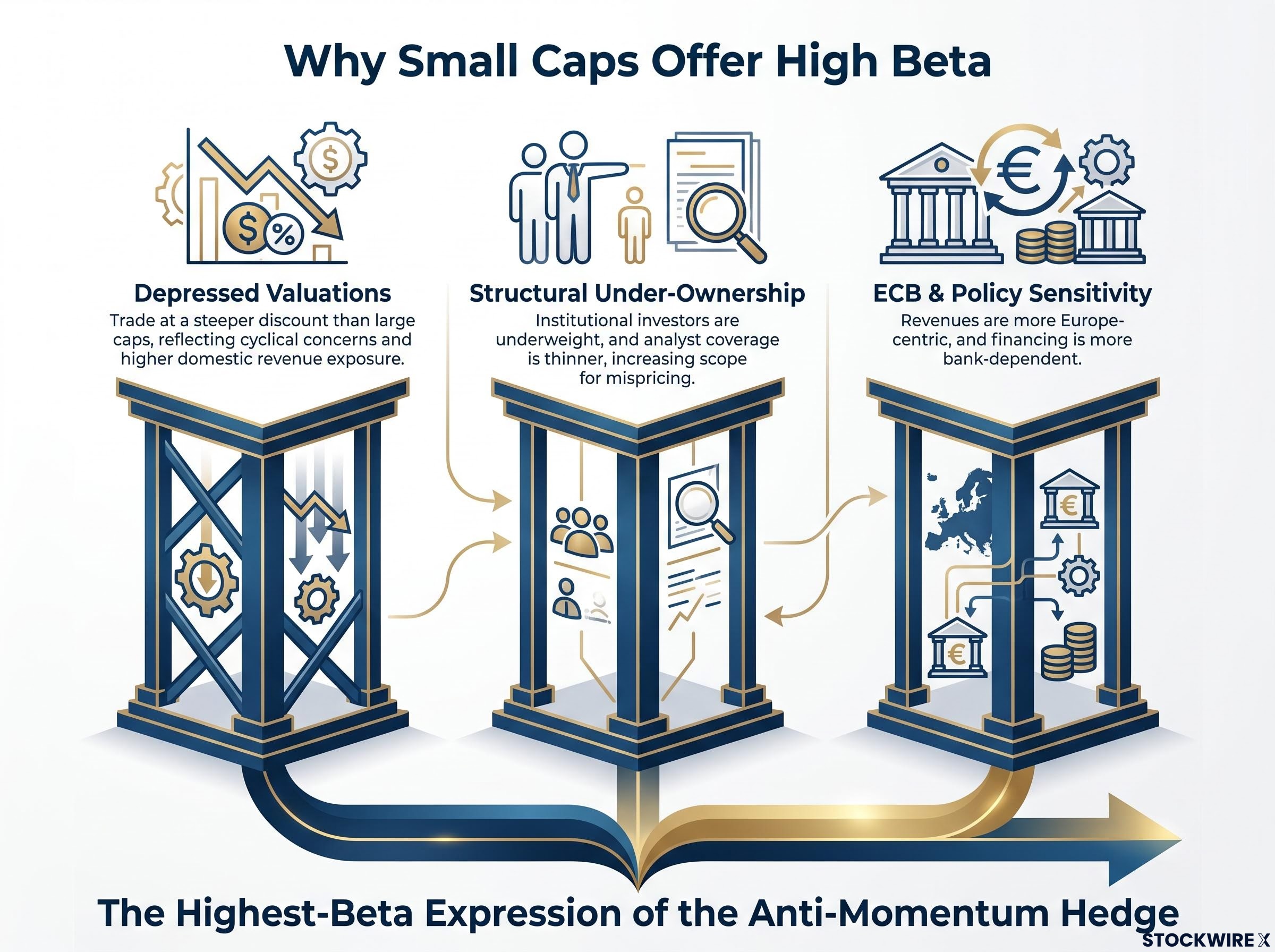

Small caps are not simply another beneficiary within the European opportunity set. They are the most concentrated expression of every compounding factor identified so far, which is why Barclays singles them out rather than treats them as a footnote.

Three factors compound in small caps simultaneously:

Barclays characterises the European small-cap opportunity as cheap, under-owned, and policy-sensitive, with positive factor exposure to small caps alongside cyclicals in the 2026 outlook.

The combination produces high beta to any European re-rating. Whether the catalyst is an AI-momentum unwind, an ECB dovish pivot, or both arriving simultaneously, small caps offer leverage to the thesis that large-cap European indices do not provide. For investors looking to express this hedge with maximum sensitivity to the re-rating catalyst, small caps are the instrument.

The macro and positioning case creates the backdrop, but returns are realised at the sector and stock level. Barclays’ framework and typical factor sensitivities point to four European small-cap sectors where the compounding factors, cheap, under-owned, and ECB-sensitive, concentrate most clearly. Each sector connects back to the same underlying logic rather than standing as an isolated opportunity.

The positioning and policy case provides the directional view. Bottom-up stock selection is still required to separate genuinely mispriced businesses from structurally weak ones. Barclays’ overarching message is that the AI trade remains intact but frothy, and risk management increasingly argues for owning the other side of that crowding.

| Sector | Key Tailwind | Connection to Hedge Thesis | Risk to Watch |

|---|---|---|---|

| Domestic industrials and specialty manufacturers | European infrastructure, defence, and energy-transition capex with fiscal support | Absent from AI-momentum baskets; pure domestic revenue exposure benefits from ECB easing and growth stabilisation | Fiscal support may slow if deficit concerns escalate |

| Regional financials and payment platforms | Normalised rate levels and improved credit demand | Under-owned relative to large universal banks; higher sensitivity to domestic credit conditions | Credit quality deterioration if recession materialises |

| Consumer discretionary (European revenue) | Rebound option if consumer confidence stabilises | Depressed by demand pessimism; predominantly domestic revenue means ECB policy has a direct impact | Prolonged wage stagnation or further rate tightening |

| Specialty healthcare and diagnostics | Multiple compression despite idiosyncratic growth drivers | Less tied to global AI narrative; fits the diversifier role while retaining structural growth potential | Regulatory delays or reimbursement changes |

All four sectors are largely absent from AI-momentum baskets, which reinforces their function as diversifiers rather than correlated growth bets. The selection criteria are consistent: each sector benefits from at least two of the three compounding factors (depressed valuations, under-ownership, ECB sensitivity), and none carries meaningful exposure to the AI-momentum trade that the hedge is designed to offset.

The Barclays thesis is not a prediction that AI will collapse. It is a portfolio construction argument. Adding European exposure, particularly small-cap and rate-sensitive names, can offset risk from crowded AI and momentum longs rather than express a pure bullish view on European growth. The distinction matters: this is a hedge with identifiable mechanics, not a directional bet on a European recovery.

The signalling and action framework reduces to three steps:

Barclays’ report title, “More than just AI,” signals the broader diversification argument. The AI trade remains intact but is characterised as frothy as of June 2026, and risk management increasingly argues for owning the other side of that crowding. European small-cap and rate-sensitive segments are natural candidates for that role.

Selectivity remains the operative word. The macro and positioning case creates the backdrop, but realising upside still requires separating genuinely mispriced businesses from structurally weak ones. The mechanism is clear; the execution is where discipline matters.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The AI trade short Europe setup refers to hedge funds and systematic trend-following strategies going long U.S. technology and AI stocks while shorting European equities as the funding vehicle. Because the two positions are paired, any reduction in AI exposure mechanically forces short-covering in European markets, creating buying pressure regardless of changes in the underlying macro backdrop.

European small caps combine three compounding factors: depressed valuations relative to large caps, structural under-ownership by institutional investors, and high sensitivity to ECB policy and domestic credit conditions. This combination means they offer the highest leverage to any European re-rating catalyst, whether from an AI unwind, an ECB dovish pivot, or both occurring simultaneously.

A one-and-done or dovish ECB scenario would most benefit European small caps because their financing is more bank-dependent and their revenues more domestically oriented than large caps. Easier credit conditions and lower perceived terminal rates directly reduce financing costs and improve the domestic demand outlook for these companies.

Barclays recommends tracking ECB communication for signs of a moderated or less-hawkish tightening path, since a shift in rate expectations provides an independent catalyst for European equity re-rating that does not require the AI trade to unwind. Investors can use each ECB policy signal as a timing input to build or scale exposure in rate-sensitive and domestically oriented small-cap sectors.

Barclays highlights four sectors: domestic industrials and specialty manufacturers, regional financials and payment platforms, consumer discretionary companies with European revenue exposure, and specialty healthcare and diagnostics. Each sector benefits from at least two of the three compounding factors (depressed valuations, under-ownership, and ECB sensitivity) while carrying little or no exposure to the AI-momentum trade.