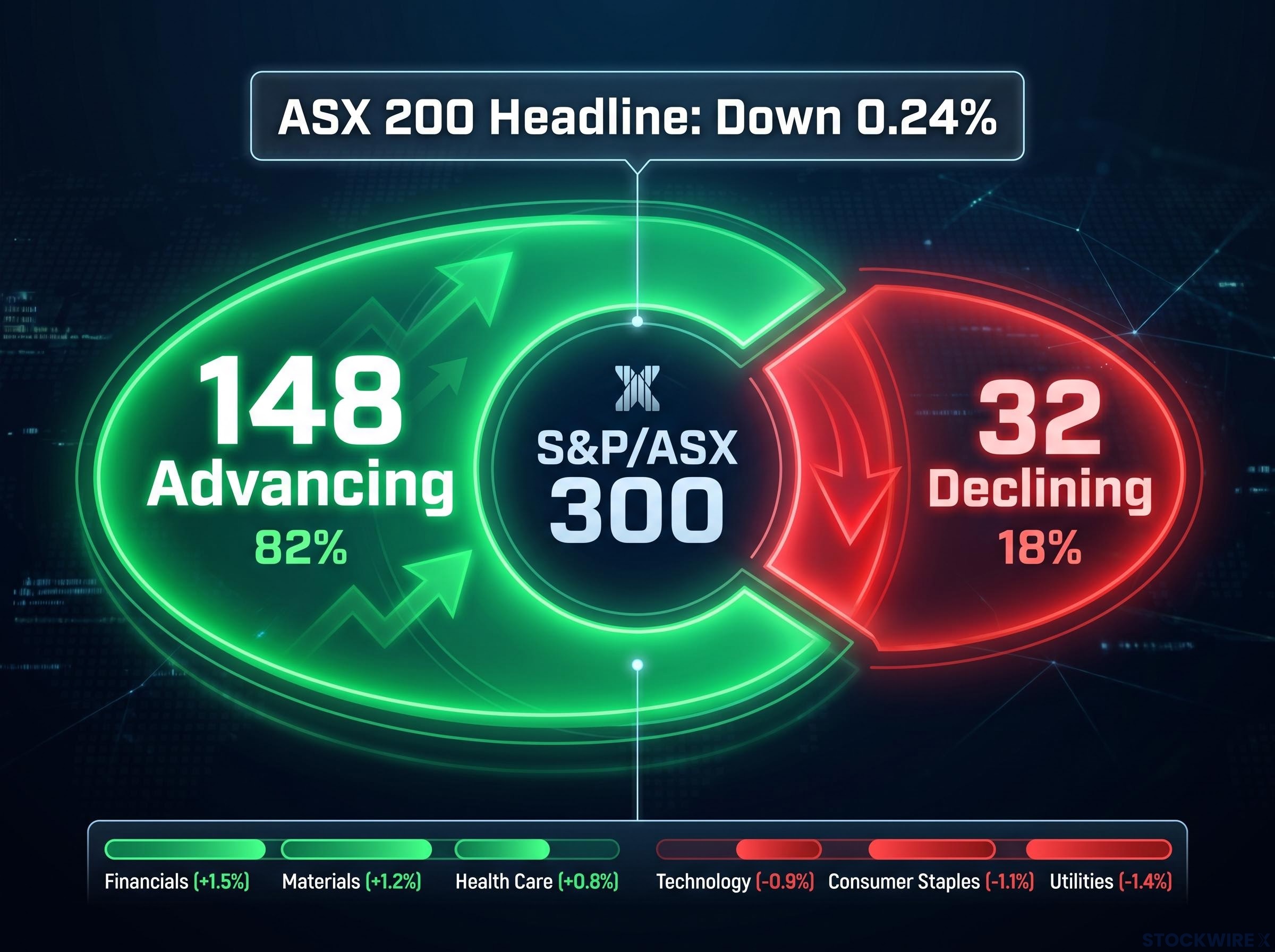

The ASX 200 fell just 0.24% on 9 June 2026, closing at 8,604.2. Behind that near-flat headline, one of the more decisive sector rotations of the year was taking shape. Two domestic sentiment surveys landed simultaneously: Westpac consumer confidence tumbled to 80.6, its deepest pessimistic reading in years, while NAB business confidence sat at negative 14, with NAB’s own economists calling time on further RBA rate hikes this cycle. Markets read both figures not as cause for panic but as confirmation of a specific thesis: rates are going nowhere, and possibly lower.

What followed was a session of concentrated selling in materials, gold and uranium, and concentrated buying in communication services, staples, healthcare and REITs. This article unpacks where the money moved, why it moved there, what was sold, and what today’s rotation signals about how professional capital is positioning for the months ahead on the ASX.

The index fell slightly but the real story was underneath the surface

The ASX 200 closed at 8,604.2, down 20.9 points or 0.24%. On its own, that number suggests a forgettable session. It was anything but.

The benchmark plunged roughly 1.5% intraday to a low of 8,490.9 before staging a sharp recovery, finishing 1.3% above its trough and within 0.2% of the session high. The closing print masked the severity of the morning’s selloff and the strength of the afternoon’s rebound.

Smaller company indices told a different story. The All Ordinaries fell 0.35% to 8,824.8, the Small Ordinaries dropped 0.51% to 3,430.2, and the Emerging Companies index declined 2.01% to 2,925.4, consistent with elevated risk premia in a cautious macro environment.

- ASX 200: 8,604.2, down 0.24%

- All Ordinaries: 8,824.8, down 0.35%

- Small Ordinaries: 3,430.2, down 0.51%

- Emerging Companies: 2,925.4, down 2.01%

Across the S&P/ASX 300, advancing stocks outnumbered decliners 148 to 32, a ratio that directly contradicts any reading of this session as a broad selloff. The selling was concentrated, not widespread, and the buying was even more so.

When big ASX news breaks, our subscribers know first

Weak sentiment data locked in the RBA hold narrative and set the rotation in motion

Westpac consumer sentiment fell 2.9% to 80.6 in June, extending May’s 3.5% decline. The medium-term economic outlook sub-index hit a three-year low, driven by cost-of-living anxiety and deteriorating household finance expectations. For a second consecutive month, consumers signalled deepening financial stress.

The consumer sentiment sub-indexes tracking economic expectations over the next 12 months and five years had already reached their weakest combined reading since November 2022 before June’s 80.6 headline print, meaning the Westpac data released on 9 June deepened a deterioration that institutional allocators had been watching build for weeks.

NAB business confidence improved 10 points to negative 14, but remained in negative territory across all industries. The partial improvement did little to shift the broader reading: domestic demand is soft, cost pressures remain elevated, and the outlook is subdued.

The RBA’s May 2026 monetary policy decision set the cash rate target at 4.35% and outlined forward guidance emphasising data dependence, the backdrop against which both the Westpac and NAB surveys were interpreted by markets as confirmation that further tightening was off the table.

Michael Hayes, NAB Economist, noted that NAB no longer expects another RBA rate increase this cycle, with the next move likely lower.

| Survey | Latest Reading | Change From Prior | RBA Implication |

|---|---|---|---|

| Westpac Consumer Sentiment | 80.6 (June 2026) | Down 2.9% (prior: 83.0) | Household stress reduces mandate for further hikes |

| NAB Business Confidence | -14 points | Improved 10 points from prior | Still negative; NAB calls end to rate-hike cycle |

Markets read the combination not as a risk-off trigger but as a tactical signal. With the RBA increasingly unlikely to tighten further, capital began moving toward sectors that benefit from a stable or declining rate environment. The Australian dollar, at USD 0.7055 (up 0.14%), reflected the same offsetting forces: weaker commodities on one side, reduced rate-hike risk on the other.

What defensive rotation actually means and why it happens when rates plateau

Defensive rotation is a deliberate reallocation within equities, not a retreat from them. When monetary policy is expected to remain stable or ease, capital shifts from cyclical or commodity-linked sectors toward lower-volatility, income-generating names. The distinction matters because the two moves carry opposite implications for investor positioning.

- Risk-off selling involves broad liquidation across equities, typically pushing the majority of stocks lower and sending capital into cash or government bonds

- Defensive rotation keeps capital deployed in equities but redirects it from sectors sensitive to economic momentum toward sectors offering income stability and lower earnings volatility

- The evidence on 9 June: advancing stocks outnumbered decliners 148 to 32, confirming that money was moving within the market, not out of it

- The trigger: a rate-hold signal, not an economic crisis signal

The sector rotation mechanics that institutional capital follows across business cycle phases place defensives, including Consumer Staples, Healthcare, and Utilities, structurally ahead of cyclicals when late-cycle signals emerge, which is precisely why the breadth data on 9 June, 148 advancers against 32 decliners, reads as a deliberate reallocation rather than random noise.

Why rate-hold expectations improve the maths on dividend-paying stocks

When the cash rate is no longer rising, the gap between a REIT yield or telco dividend and the risk-free rate stabilises or widens in the investor’s favour. The present value of those income streams improves because the discount rate applied to future cashflows stops increasing.

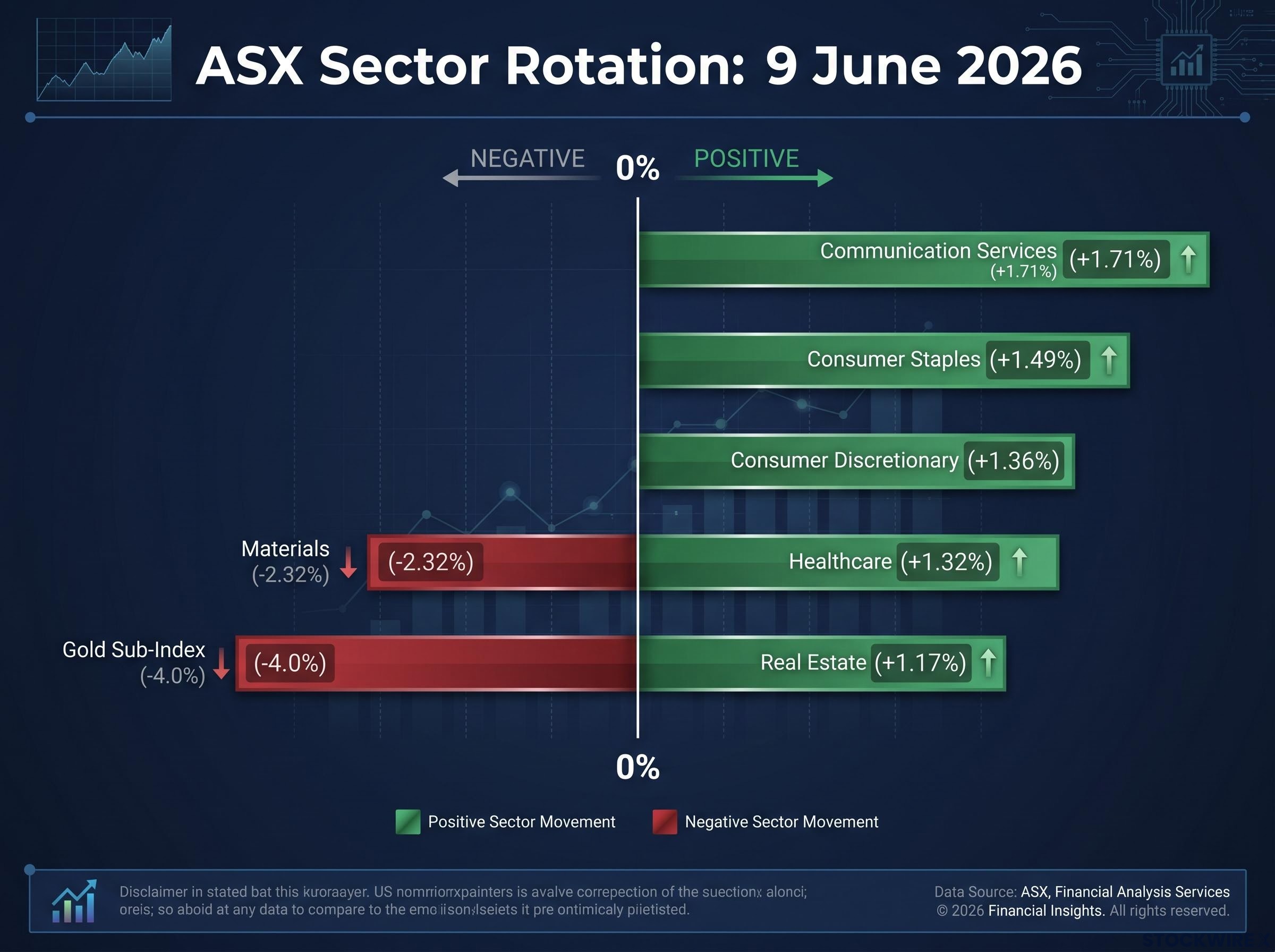

This does not require the economy to be strong. It only requires that rates are not going higher. The Real Estate sector’s 1.17% gain on the session reflected precisely this mechanism: lower expected discount rates lifting the present value of property income streams.

Communication services, staples, healthcare and REITs attracted the rotation buyers

Each winning sector on 9 June offered some combination of defensive earnings, income yield, or recovery value that made the RBA-hold thesis actionable at the individual stock level.

Communication Services led the session, rising 1.71% to 1,652.1. Telstra (TLS) gained 2.2%, its utility-like cashflow profile making it a natural destination when rate risk subsides. Platform and classified names also benefited: Seek (SEK) rose 2.9%, CAR Group (CAR) gained 2.2%, News Corp (NWS) added 2.3%, and Superloop (SLC) advanced 2.5%, all supported by subscription-driven, mission-critical revenue that is less sensitive to discretionary spending cuts.

Consumer Staples advanced 1.49% to 12,185.4, the clearest defensive expression of the day. Woolworths (WOW) rose 2.2% and Coles (COL) gained 1.8%, functioning as earnings havens: households under pressure still buy groceries, and the easing of rate-hike risk removes an overhang from valuations.

Healthcare climbed 1.32% to 23,534.8, extending its recovery for a second consecutive session. The sector had previously experienced a trough-to-recent-low contraction of approximately 47%, and the buying reflected a value-recovery trade as much as a pure defensive play. CSL (CSL) rose 1.6%, Cochlear (COH) gained 2.2%, Ramsay Health Care (RHC) climbed 2.8%, and Sonic Healthcare (SHL) advanced 2.1%.

Real Estate gained 1.17% to 3,576.1, the most mechanically rate-sensitive sector. Lifestyle Communities (LIC) surged 4.6%, Charter Hall (CHC) and Cromwell Property (CMW) each added 3.5%, and Vicinity Centres (VCX) rose 2.9%.

| Sector | Change | Representative Stocks |

|---|---|---|

| Communication Services | +1.71% | Telstra +2.2%, Seek +2.9%, CAR Group +2.2% |

| Consumer Staples | +1.49% | Woolworths +2.2%, Coles +1.8% |

| Consumer Discretionary | +1.36% | Temple & Webster +5.2%, Nick Scali +3.2%, Harvey Norman +2.7% |

| Healthcare | +1.32% | CSL +1.6%, Cochlear +2.2%, Ramsay +2.8% |

| Real Estate | +1.17% | Lifestyle Communities +4.6%, Charter Hall +3.5%, Vicinity +2.9% |

Consumer discretionary’s gain was a bet on the future, not the present

Consumer Discretionary’s 1.36% advance to 3,573.0 stands apart from the pure defensive plays. Temple & Webster (TPW) surged 5.2%, Nick Scali (NCK) rose 3.2%, Harvey Norman (HVN) gained 2.7%, and Super Retail Group (SUL) added 2.7%. The logic was forward-looking: if rates have peaked and the worst of the cash-flow squeeze is past, discretionary spending names should re-rate before spending actually recovers. It is a higher-risk expression of the same rate-hold thesis, positioning for a bottoming in consumer weakness rather than reacting to current strength.

Materials, gold and uranium absorbed the selling as commodity momentum reversed

The same macro logic that directed capital into defensives had a rational exit point. Materials, gold and uranium provided the source of the rotation capital, pressured by both domestic and offshore forces.

The Materials sector (XMJ) fell 2.32% to 23,918.5, squeezed by two converging pressures: the domestic rotation away from cyclicals, and external commodity price weakness following the prior Friday’s strong US payrolls report. That data repriced Federal Reserve rate-cut expectations, lifting real yields and pressuring dollar-denominated commodities. BHP fell 1.9%, Rio Tinto dropped 1.8%, Fortescue declined 3.8%, Mineral Resources lost 2.6%, Capstone Copper fell 6.1%, and Lynas Rare Earths dropped 4.8%.

The Gold Sub-Index (XGD) fell 4.0% in a single session, one of the sharpest daily reversals in the sub-index’s recent rally.

Gold’s vulnerability was specific. As a non-yielding asset, gold loses relative appeal when real yields rise. The repricing of US rate-cut expectations after stronger jobs data provided the trigger. Emerald Resources (EMR) fell 9.0%, Southern Cross Gold (SX2) dropped 6.2%, Newmont (NEM) declined 4.8%, and Northern Star Resources (NST) lost 3.3%. Gold spot traded at USD 4,352 per ounce, down 0.3%. LME copper fell 0.5% to USD 13,661 per tonne and aluminium dropped 1.8% to USD 3,669 per tonne.

Uranium stocks extended their near-term correction. Paladin Energy (PDN) fell 8.8%, Bannerman Energy (BMN) dropped 8.2%, Deep Yellow (DYL) declined 7.6%, NexGen Energy (NXG) lost 6.2%, and Boss Energy (BOE) fell 5.5%. The moves reflected momentum-driven selling and near-term commodity risk-off sentiment rather than a structural shift in the longer-term nuclear energy thesis.

| Sector / Sub-Index | Change | Key Stock Moves |

|---|---|---|

| Materials (XMJ) | -2.32% | BHP -1.9%, Rio Tinto -1.8%, Fortescue -3.8% |

| Gold Sub-Index (XGD) | -4.0% | Emerald Resources -9.0%, Newmont -4.8%, Northern Star -3.3% |

| Uranium (select names) | -5.5% to -8.8% | Paladin -8.8%, Bannerman -8.2%, Deep Yellow -7.6% |

What today’s rotation signals about where the ASX stands heading into the second half of 2026

The session’s message was specific. Capital rotated within equities toward income and stability, not away from equities entirely. That distinction signals a market that believes the economic slowdown is manageable and the RBA rate-hold path is credible.

According to Michael Hayes at NAB, the next RBA move is likely lower, not higher. That view underpinned the entire session’s rotation.

The unresolved tension sitting underneath today’s positioning is whether commodity weakness represents a tactical correction within a broader uptrend or the beginning of something more persistent, driven by softer Chinese demand, higher real yields, and slowing global growth.

Per capita recession conditions were already embedded in the Australian economy before today’s session, with per capita output falling approximately 0.7% across the full year of 2025, corporate insolvencies reaching their highest level since the 1990-91 recession, and consumer confidence at a 50-year low, which frames the Westpac and NAB data not as a sudden deterioration but as the continuation of a structural demand contraction that makes the RBA’s pivot to holding rates an economic necessity rather than a choice.

The risk profile heading into the second half is asymmetric:

- If the RBA holds or cuts: defensives, REITs and income names can continue to outperform, validating today’s rotation

- If US data softens and real yields decline: materials and gold could recover sharply, reversing the session’s selling

- If commodity weakness deepens on demand deterioration: today’s defensive positioning looks well-timed, but broader index-level risk rises

US equity futures pointed mildly positive at the ASX close (S&P 500 futures up 0.29%), offering some near-term support to global risk sentiment. The AUD at USD 0.7055 reflected the same tension: weaker commodities pulling one way, reduced rate-hike risk pulling the other.

A session of two markets, and what each half is telling investors

The ASX 200’s 0.24% decline on 9 June 2026 masked a meaningful realignment of capital, from cyclical and commodity-exposed sectors toward defensive, income-generating, and rate-sensitive names. The driving logic was straightforward: deteriorating domestic sentiment is simultaneously bad news for the economy and confirmation of the macro conditions that support defensives.

The session establishes the current dominant market thesis, that the RBA is done hiking and the next move is lower, and maps the stocks and sectors where that thesis is being expressed most concretely. Whether that thesis proves correct will depend on the variables identified above: the RBA’s actual path, the trajectory of commodity prices, and the direction of global growth signals in the months ahead.

The rotation out of domestic banks and rate-sensitive defensives that characterised the 2 June session moved in the opposite direction to today’s trade, with institutional capital at that point chasing globally exposed technology, base metals, and gold names that are among the biggest losers on 9 June, illustrating how quickly the dominant thesis can reverse as macro signals shift.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.