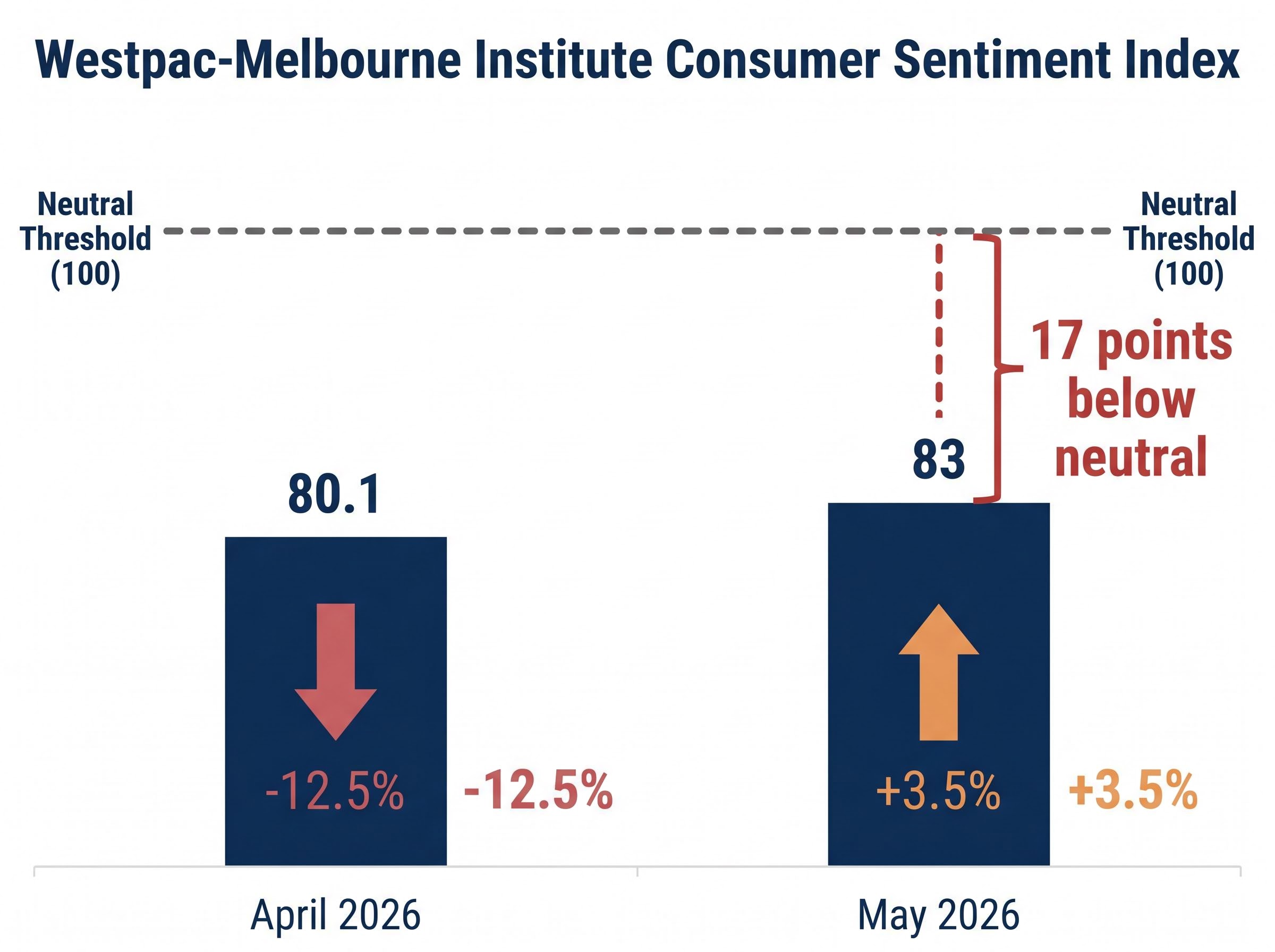

The Westpac-Melbourne Institute Consumer Sentiment index rose 3.5% in May 2026, lifting to 83 from April’s 80.1. That single number looks like good news. It is not. The May reading follows April’s 12.5% collapse and leaves sentiment more than 17 points below the neutral threshold of 100, firmly in territory Westpac senior economist Matthew Hassan has described as “recessionary.” More troublingly, the sub-indexes measuring economic expectations over the next 12 months and five years both fell further in May, reaching their weakest combined reading since November 2022. For Australian investors, the question is not whether the headline bounced but what the data underneath it signals about household spending, corporate earnings, and the durability of the ASX recovery. This analysis disaggregates the May sentiment data, explains why forward-looking sub-indexes matter more than the headline for equity investors, examines which ASX sectors carry the most direct exposure to household pessimism, and sets out the specific macroeconomic conditions required before a genuine and sustained confidence recovery becomes plausible.

A bounce that changes almost nothing

The May index reading of 83 sits 17 points below the neutral threshold of 100. April’s 12.5% decline dragged the index to 80.1; a 3.5% rebound from that deeply depressed base does not come close to unwinding the damage. Arithmetically, recovering a 12.5% fall requires a gain of more than 14% from the lower base, meaning the May result represents roughly a quarter of the ground lost.

| Month | Index Reading | Monthly Change | Distance from Neutral (100) |

|---|---|---|---|

| April 2026 | 80.1 | -12.5% | -19.9 points |

| May 2026 | 83 | +3.5% | -17.0 points |

Westpac characterised the May move as a “partial and fragile recovery” that does not signal a turning point. Hassan noted the April shock “has not been unwound.”

Westpac Economics Sentiment remains in “recessionary territory,” with the May improvement described as “not convincing” by senior economist Matthew Hassan.

Investors who anchor to the headline percentage change risk misreading the macro signal entirely. The absolute level of the index, not the direction of the monthly move, is what matters for forward spending and earnings forecasts.

When big ASX news breaks, our subscribers know first

What the Westpac-Melbourne Institute Consumer Sentiment index actually measures

The Westpac-Melbourne Institute survey is a monthly telephone and online survey of approximately 1,200 Australian households. It measures views across five core dimensions, producing a composite index where 100 represents the neutrality point: readings above 100 indicate optimism, readings below indicate pessimism. Historically, sustained readings below roughly 85-90 have correlated with reduced discretionary spending across the Australian economy.

The survey’s sub-indexes each capture a distinct aspect of household confidence:

- Family finances vs. a year ago: how households assess their current financial position relative to the prior year

- Family finances, next 12 months: expectations for near-term personal financial conditions

- Major purchase timing: whether households consider now a good or bad time to buy large items such as furniture, appliances, or vehicles

- Economy, next 12 months: short-run expectations for the broader Australian economy

- Economy, next 5 years: longer-run expectations for economic conditions

- Unemployment expectations: the degree to which households fear rising joblessness (a higher reading indicates greater concern)

The unemployment expectations index is currently well above its long-run average, reflecting elevated job-loss fears across Australian households.

How investors should read the sub-indexes

The “economy, next 12 months” and “economy, next 5 years” sub-indexes are the most forward-looking components and therefore the most relevant for equity market implications. When these sub-indexes deteriorate even as the headline index recovers, they signal that households expect conditions to worsen, a leading indicator for spending pullbacks that eventually flow through to corporate revenue.

The “major purchase timing” sub-index is the most direct leading indicator for Consumer Discretionary sector revenues. A weak reading here signals that households are deferring large purchases, which translates into softer sales for retailers, travel operators, and home furnishing companies within two to three quarters.

Three structural headwinds keeping sentiment depressed

Three forces are simultaneously suppressing household confidence. Any one in isolation would weigh on sentiment; their convergence makes a quick recovery structurally implausible.

- Rate policy: The RBA raised the cash rate by 25 basis points to 4.35% at its 5-6 May 2026 meeting. The decision had been widely anticipated, and the absence of a larger increase provided limited relief rather than genuine support. Rates at 4.35% continue to constrain household cash flows, particularly for mortgage holders on variable rates.

- Budget: The federal budget was assessed by survey respondents as a mild net negative, with more households expecting it to worsen their finances than improve them. This removes what might otherwise have served as a policy tailwind for confidence.

- Job-loss fears: The unemployment expectations sub-index remains well above its long-run average. Westpac has flagged this as a primary brake on discretionary spending and household risk appetite, with consumers reluctant to commit to large purchases while job security feels uncertain.

The RBA’s May 2026 Statement on Monetary Policy confirms the 25 basis point increase to 4.35% alongside projections showing the cash rate remaining restrictive through most of 2026, a forward guidance posture that directly informs why household confidence in the interest-rate outlook remains suppressed.

Luci Ellis, Westpac Chief Economist The May rebound is “only a small step away from extremely weak levels.”

These three headwinds are not short-lived noise. The RBA rate outlook, budget fiscal settings, and labour market confidence all operate on multi-month timescales, meaning the conditions for pessimism are likely to persist well into the second half of 2026.

The headline GDP figure has obscured a parallel deterioration: Australia has been in a per capita recession for much of the past year, with real output per person falling approximately 0.7% across 2025 even as aggregate growth remained positive, a distinction that helps explain why household confidence readings have remained so far below the neutral threshold.

What the forward sub-indexes reveal about near-term consumer outlook

The May sub-index values tell a more troubling story than the headline. The “economy, next 12 months” and “economy, next 5 years” sub-indexes both declined further in May, reaching their weakest combined reading since November 2022. Detailed May 2026 values for these sub-indexes were not publicly available at time of publication. April 2026 values were 75.3 (“economy, next 12 months”) and 91.4 (“economy, next 5 years”).

| Sub-Index | April 2026 Value | May 2026 Value | Monthly Change |

|---|---|---|---|

| Economy, next 12 months | 75.3 | Not yet publicly available | Not yet publicly available |

| Economy, next 5 years | 91.4 | Not yet publicly available | Not yet publicly available |

The combined forward-looking reading is the weakest since November 2022, a period when inflation was accelerating, the RBA was mid-tightening cycle, and the ASX 200 was pricing in the possibility of a domestic recession. That historical parallel gives the current reading meaningful context: households are as pessimistic about the future as they were at the worst point of the post-pandemic inflation shock.

Matthew Hassan, Westpac Senior Economist The sub-indexes reflect “persistent anxiety about the macro backdrop, particularly unemployment risks and the interest-rate outlook.”

Forward sub-indexes falling even as the headline bounced is the most analytically significant aspect of the May release. When these two signals diverge, the sub-indexes have historically been the more reliable guide to where household spending is heading in the next two to three quarters.

Which ASX sectors carry the most exposure to household pessimism

Consumer Discretionary: direct exposure, lagged earnings impact

Consumer Discretionary is the most mechanically exposed sector to weak sentiment. Its revenues depend on exactly the household behaviours the “major purchase timing” sub-index captures: decisions to buy furniture, upgrade electronics, book holidays, or renovate homes. ASX-listed retailers, travel companies, and home furnishing operators sit directly in the path of consumer pullback.

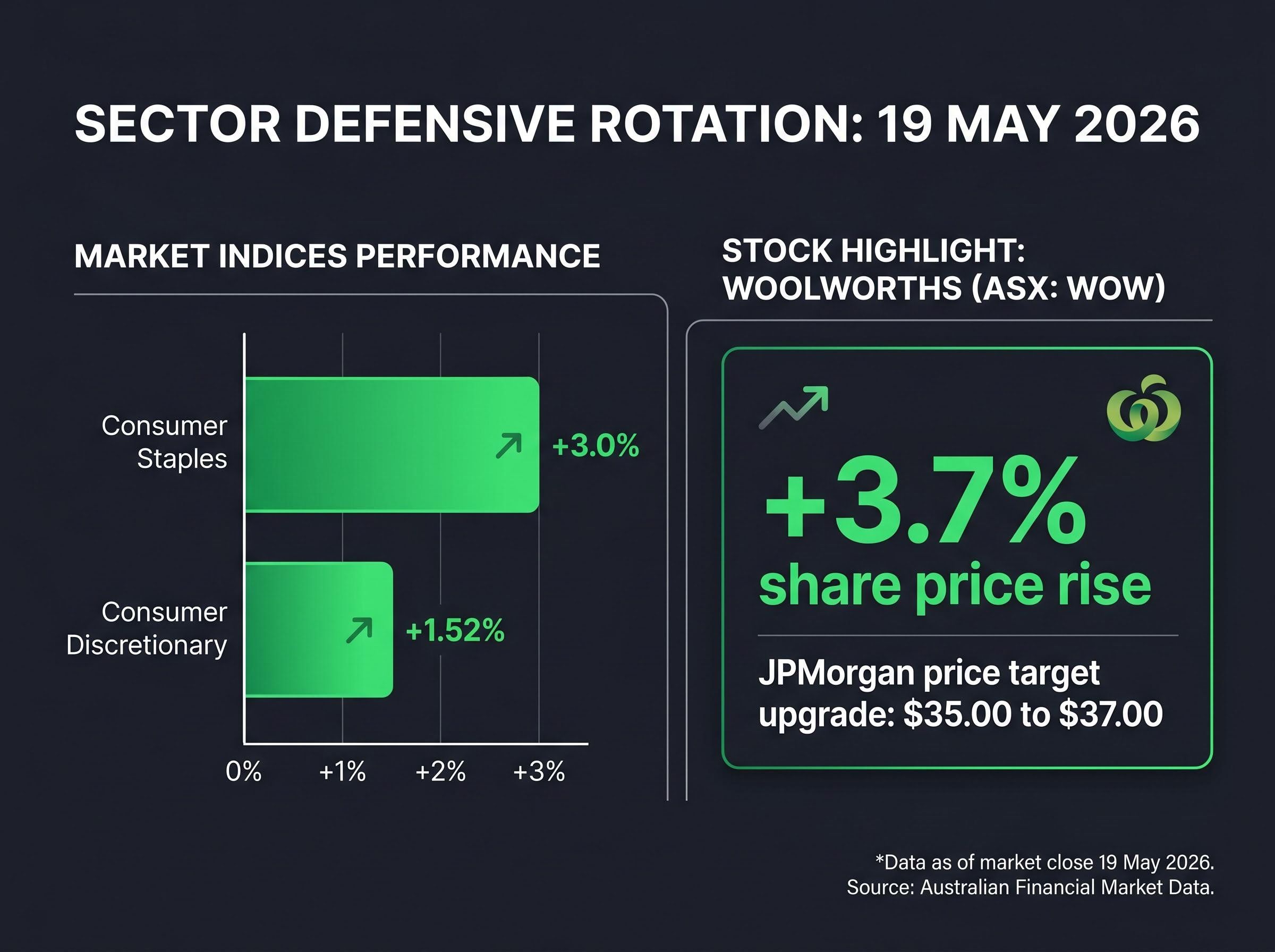

The relationship between sentiment and ASX discretionary earnings is not instantaneous. It operates with a lag of one to two reporting periods, meaning the current readings are more relevant to FY27 earnings forecasts than FY26 results. On 19 May 2026, the Consumer Discretionary sector index rose 1.52%, notably lagging the defensive rotation visible elsewhere in the market.

Consumer Staples: defensive positioning and the supermarket paradox

Consumer Staples companies occupy a different position. Supermarkets, food producers, and essential goods retailers are less exposed to sentiment-driven revenue pullback because households continue purchasing groceries and household essentials regardless of confidence levels. In a pessimistic environment, a flight-to-defensive positioning can actually support staples’ relative share price performance.

On 19 May 2026, the Consumer Staples sector index rose 3.0%, nearly double the discretionary sector’s gain. JPMorgan upgraded Woolworths (ASX: WOW) to Overweight on the same day, raising its price target to $37.00 from $35.00. Woolworths shares rose 3.7%. That upgrade reflects the logic in real time: in an environment of depressed household confidence, investors rotate capital toward companies whose revenue base is insulated from discretionary spending cuts. Coles operates within a similar defensive framework, though the JPMorgan upgrade specifically targeted Woolworths as the preferred exposure.

ASX sector rotation in May 2026 is running in two speeds simultaneously: breadth data from Week 20 shows 14 combined new lows appearing in healthcare and consumer discretionary while materials, energy, financials, and utilities recorded 11 new highs in the same period, a divergence that reflects the capital reallocation dynamic the sentiment data is driving in real time.

Matthew Hassan, Westpac Senior Economist A meaningful improvement in sentiment requires “clear evidence that inflation is returning to target without a material rise in unemployment.”

For investors positioning around macro data, understanding the distinction between sentiment-exposed and sentiment-insulated sectors within the consumer universe is the difference between reactive and anticipatory portfolio management.

What would it take for confidence to genuinely recover

Westpac’s outlook for the second half of 2026 is a “gradual and fragile improvement,” contingent on three conditions materialising in sequence:

- Inflation returning toward the 2-3% target band without triggering further rate increases, giving the RBA room to signal an eventual easing cycle

- Unemployment holding in the low-4% range, with the April employment data (forecast at +15,700 positions, unemployment rate steady at 4.3%, due Thursday 22 May 2026) serving as the next near-term test

- The RBA rate outlook shifting toward easing, with Westpac Chief Economist Luci Ellis noting a more meaningful improvement is not anticipated “until markets are confident the RBA easing cycle is underway and unemployment has stabilised”

Westpac has explicitly flagged the downside scenario: if unemployment rises materially above the low-4s, any improvement in sentiment would likely stall or reverse, with direct implications for Consumer Discretionary earnings forecasts.

For investors wanting to model the scenario where conditions align more quickly than Westpac’s base case, our full explainer on the RBA rate cycle peak examines oil futures backwardation, historical supply shock timelines, and Oxford Economics modelling that points to potential back-to-back GDP contractions in June and September 2026 as the mechanism that could force a faster pivot from tightening to easing.

| Indicator | Current Status | What to Watch |

|---|---|---|

| Inflation | Tracking toward 2-3% band but not yet confirmed | Quarterly CPI prints and RBA trimmed mean readings |

| Unemployment | Forecast steady at 4.3% (April data due 22 May 2026) | Monthly ABS labour force data; any move above low-4s |

| RBA Rate Outlook | Cash rate at 4.35%; expected to remain restrictive through most of 2026 | RBA forward guidance and market pricing for rate cuts |

Sentiment data becomes most actionable for investors when read alongside the employment and inflation sequence. Together these three data streams form a forward composite that is more predictive of consumer sector earnings direction than any single release.

The partial rebound has not changed the macro story for investors

The May index at 83 remains 17 points below neutral. The forward sub-indexes sit at their lowest combined reading since November 2022. The headline moved; the investment-relevant signal did not.

In an environment where the ASX 200’s technical structure remains challenged and upcoming employment data carries binary implications for household confidence, consumer sentiment is one component of a macro mosaic, not a standalone buy or sell signal.

Westpac’s near-term outlook is “flat-to-soft,” pending inflation and labour market data. The next test arrives Thursday 22 May 2026 with the April employment figures.

Westpac Economics Outlook Near-term sentiment is expected to remain “flat-to-soft,” with any sustained recovery conditional on inflation, unemployment, and the RBA rate trajectory aligning in households’ favour.

The practical interpretive principle for investors: watch the forward sub-indexes and the unemployment expectations index, not the headline number, as the leading indicators of where consumer sector earnings revisions are heading.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.