The S&P/ASX 200 closed on 2 June 2026 at 8,724.4, down just 5.0 points or 0.06%. On paper, nothing happened. Beneath the surface, one of the year’s most aggressive capital reallocations was already underway.

The Reserve Bank of Australia’s cash rate, held at 4.35%, has capped the appeal of crowded, yield-sensitive defensive positions for months. Institutional portfolios built around major bank dividends and consumer staples are now being actively dismantled. The capital is not sitting idle. It is flowing into globally exposed technology equities, base metals producers riding structural supply deficits, and gold miners benefiting from both geopolitical fear and corporate activism.

What follows is a dissection of the three distinct forces driving ASX sector rotation on a day the headline index barely moved, and why the implications extend well beyond a single session.

Unmasking the illusion of a flat headline index

A 0.06% decline in the S&P/ASX 200 tells investors almost nothing about what actually occurred on 2 June 2026. Market breadth told a different story entirely. Within the S&P/ASX 300, 184 stocks declined against just 99 advancers. Nearly twice as many names fell as rose, yet the index held steady.

The explanation lies in what was being sold and what was being bought. Institutional capital moved aggressively out of domestically exposed, rate-sensitive sectors, including major banks, consumer staples, and real estate investment trusts. These positions had been crowded for months, and brokerage commentaries noted that earlier rallies in domestic consumer stocks had run ahead of earnings fundamentals. The major banks, in particular, are increasingly viewed as fully valued with limited scope for positive earnings revisions.

The Small Ordinaries Index, a gauge of smaller domestic names, closed at 3,505.0, down 0.18%, confirming that the selling pressure concentrated in locally focused equities.

| Index | Closing Level | Change (%) |

|---|---|---|

| S&P/ASX 200 | 8,724.4 | -0.06% |

| All Ordinaries | 8,966.0 | -0.04% |

| Small Ordinaries | 3,505.0 | -0.18% |

The gains that offset these declines came from a narrow cohort of globally exposed names in technology, materials, and gold. The headline index masked the violence of the internal rebalancing.

When big ASX news breaks, our subscribers know first

Understanding the mechanics of capital reallocation

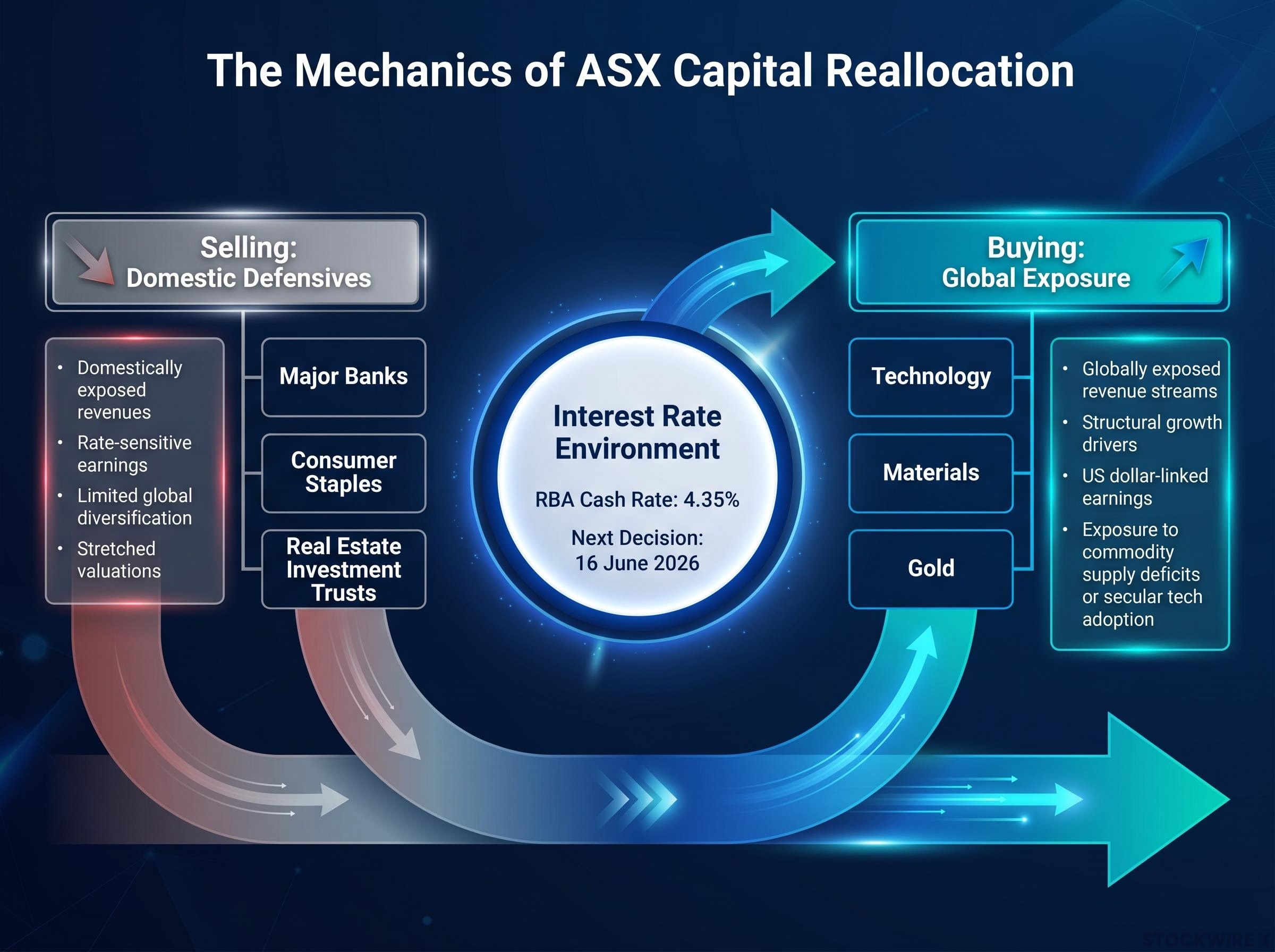

Capital reallocation, often called sector rotation, is the process by which institutional investors shift money from one group of stocks to another based on where they expect the best risk-adjusted returns. Capital flows toward areas offering the highest prospective reward for the level of risk taken, and away from areas where that reward has diminished.

Interest rate expectations sit at the centre of this process. With the RBA’s cash rate at 4.35% and market expectations pointing to the end of the hiking cycle, the trade that dominated Australian portfolios for the past two years, owning high-yield domestic banks and defensive dividend payers, is losing its relative attraction. These stocks benefited from a rising-rate environment that made their yields competitive. With rates now expected to plateau or decline, the yield premium shrinks, and capital begins to search elsewhere.

The RBA’s third consecutive hike to 4.35% was passed with an 8-1 Board vote, with the single dissent signalling that the threshold between hiking and holding is narrower than the headline margin implies, and forward guidance language deliberately preserved full optionality ahead of the July 2026 meeting.

The upcoming RBA decision on 16 June 2026 represents a near-term horizon point. If the central bank signals rate stability or a pivot toward easing, the rotation out of domestic defensives could accelerate further.

RBA monetary policy decisions have kept the cash rate at 4.35% through mid-2026, with the central bank’s next scheduled announcement on 16 June 2026 representing the clearest near-term signal for whether the plateau in rates will hold or shift toward an easing bias.

The characteristics of the two sides of this rotation are distinct:

- Stocks being sold: Domestically exposed revenues, rate-sensitive earnings, limited global diversification, stretched valuations relative to earnings growth

- Stocks being bought: Globally exposed revenue streams, structural growth drivers, US dollar-linked earnings, exposure to commodity supply deficits or secular technology adoption

This framework explains why a portfolio heavily weighted toward Australian bank yields may underperform even on days when the broader market appears stable. The money is not leaving the market. It is changing address.

Technology equities bridge the offshore valuation gap

The ASX’s technology sector delivered its strongest single-session advance in several months on 2 June 2026. The All Technology Index closed at 3,062.7, up 3.89%. The ASX 200 Information Technology sub-index gained 4.71%.

The rally was a catch-up trade. Over recent months, Australian technology names had materially lagged their US mega-cap peers, weighed down by concerns over domestic growth and compressed local valuations. Quality names like WiseTech Global and Xero were trading at discounts relative to both their historical multiples and US equivalents.

Fund managers appear to be closing underweight positions in these globally exposed names, supported by resilient earnings guidance. The common thread across the session’s biggest movers is US dollar-linked global revenue and recurring subscription models: pricing power that does not depend on the Australian domestic economy.

| Company | Ticker | Closing Price | Gain (%) |

|---|---|---|---|

| Life360 | 360 | $23.07 | +13.3% |

| Pro Medicus | PME | $160.08 | +10.8% |

| WiseTech Global | WTC | $42.23 | +7.9% |

| Xero | XRO | $87.00 | +7.5% |

The global artificial intelligence capex catalyst

The broader context for this re-rating is the global artificial intelligence capital expenditure cycle. US mega-cap technology companies have committed hundreds of billions to AI infrastructure, and that spending is cascading through supply chains and valuation frameworks worldwide.

Australian technology companies with exposure to digital infrastructure, cloud services, and data management stand to benefit from this capital cycle. Some analysts have noted that local infrastructure plays still lag the global AI rally, suggesting further scope for valuation compression. The implication for Australian investors is that local technology stock pricing is increasingly tethered to global valuation benchmarks rather than domestic economic conditions, offering a form of geographic diversification within an ASX portfolio.

Earnings quality and rate sensitivity have been the two variables that most reliably separated ASX tech winners from losers since August 2025, with Morgan Stanley cutting price targets by approximately 20% on AI disruption risk and the RBA’s tightening cycle ensuring that further multiple expansion in high-growth names must be earnings-driven rather than rate-relief driven.

Base metals capitalise on structural supply deficits

The ASX 200 Materials sector index rose 1.25% on 2 June 2026, propelled by overnight surges in base metal prices on the London Metal Exchange (LME), where aluminium reached a new multi-year high.

BHP closed at an all-time record of $63.37, up 1.4%. Mid-tier copper producers followed: Capstone Copper gained 3.7%, and Sandfire Resources rose 2.5%.

COMEX copper futures added 1.2% in Asian trade, reaching US$6.63 per pound after an overnight jump of 2.6%. The price action reflects a collision between accelerating demand and constrained supply that has been building for over a year.

The sequential factors compounding the copper supply deficit are now well documented:

- Visible exchange inventories on the LME and Shanghai Futures Exchange have fallen to critically low levels

- Logistics bottlenecks and aggressive manufacturer restocking have tightened physical availability

- Key Latin American mining operations in Chile and Peru face permitting delays and labour disruptions, reducing expected output

- Structural demand from electric vehicle manufacturing, electricity grid expansion, and AI data centre construction continues to increase annual copper consumption

This is not a speculative price spike driven by financial positioning alone. The supply constraints are physical, tied to mine output that takes years to replace. For investors, the materials sector offers exposure to a structural deficit that connects abstract macroeconomic themes, such as energy transition and AI infrastructure, to tangible, measurable commodity shortages.

COMEX-LME price dynamics complicate the supply-deficit narrative: while physical tightness is real, global exchange-held copper inventories exceeded 1 million tonnes in May 2026, a 20-year high driven by tariff front-loading in the US, raising questions about how much of the record price reflects genuine structural scarcity versus financial positioning ahead of potential tariff changes.

Safe havens and corporate activism fuel the gold bid

The ASX Gold Sub-Index advanced 2.8% on 2 June 2026, lifted by two converging forces: geopolitical safe-haven demand and a company-specific activist catalyst that sent one stock sharply higher.

COMEX gold futures rose 1.3% to US$4,566 per ounce. COMEX silver futures climbed 2.5% to US$77.11 per ounce. Brent crude pushed above US$100, driven by Middle East instability including incidents near the Strait of Hormuz and ongoing US-Iran tensions.

Multi-asset funds have been broadly increasing allocations to gold and energy as a hedge against geopolitical shocks, sticky inflation, and potential oil supply disruptions. Gold is additionally supported by renewed US rate-cut expectations, which reduce the opportunity cost of holding non-yielding assets.

Vault Minerals gained 3.1%, Regis Resources rose 2.8%, and Ramelius Resources advanced 2.5%, reflecting the sector-wide bid. But the standout move belonged to a single name.

Activist pressure fuels Northern Star rally

Northern Star Resources (NST) surged 13.6% to $21.03, providing the gold sector’s largest individual contribution. The scale of the move dwarfed the underlying gold price gain, illustrating how corporate governance events can detach a stock from its sector baseline.

Activist investor Elliott Management has built a significant stake in the gold miner and is pressuring the board on two fronts. Elliott has argued that extended interim leadership is value-destructive and has pushed for an external chief executive search focused on global gold leadership and mergers and acquisitions experience.

Elliott Management’s reported demands include: a global CEO search with a clear appointment deadline within the 2026 calendar year, and a formal strategic review focused on portfolio optimisation, which could include partial divestment of non-core operations or a whole-of-company sale to large North American or South African producers.

The company’s official position, outlined in an ASX filing on 30 May 2026, acknowledged constructive engagement with activist investors and confirmed a global search for a permanent CEO. However, Northern Star explicitly stated it was not currently in discussions regarding a change of control transaction, emphasising ongoing portfolio optimisation instead.

The gap between Elliott’s reported ambitions and the company’s public stance creates uncertainty, and markets are pricing in optionality. For investors, the Northern Star situation illustrates a broader principle: individual stock performance can detach sharply from sector-wide movements when targeted by institutional activist capital. Corporate governance and strategic direction carry pricing power independent of the underlying commodity.

Reassessing domestic portfolios for the new macro environment

The 2 June 2026 session delivered three distinct but simultaneous signals: a technology sector catching up to global peers, a base metals complex capitalising on structural supply shortages, and a gold sector energised by geopolitical fear and corporate activism. All three share a common thread. They are globally exposed, and the capital fuelling them is leaving domestically anchored positions.

The era of passive reliance on Australian bank yields faces headwinds that extend beyond a single session. Stretched valuations, a plateauing interest rate environment, and a softening domestic macro outlook are eroding the risk-adjusted case for overweight positions in rate-sensitive defensives.

Heading into the second half of 2026, the framework that emerges is one where globally exposed ASX equities, whether technology names with US dollar revenues, copper producers positioned against structural deficits, or gold miners offering geopolitical and activist optionality, command a growing share of institutional capital. The headline index may not always reflect it. The flows beneath the surface will.

For investors who recognise the rotation signals described in this article and want to act on them, our comprehensive walkthrough of portfolio rebalancing strategy covers how to identify drift in existing domestic defensive positions, when to trigger a rebalance, and how to execute tax-efficiently through superannuation and SMSF structures using private credit and fixed income as capital destinations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.