Since 2009, 46 individuals in Australia have been criminally convicted of insider trading as a result of investigations led by the Australian Securities and Investments Commission (ASIC). That figure includes company chairs, chief executives, and a former investment analyst who received a three-year correction order as recently as 2020. With ASIC designating insider trading as an enforcement focus for 2026 and operating a dedicated specialist unit within its enforcement division, the regulator’s posture toward market misconduct appears more structured than at any previous point. At the same time, the most recently concluded enforcement action in this space ended not with a conviction but with a hung jury and discontinued charges, a reminder that prosecuting inside information cases remains genuinely difficult. This article explains what insider trading means under Australian law, how ASIC detects and prosecutes it, what a multi-year enforcement sweep reveals about the regulator’s methods, and why the 2026 enforcement environment matters to retail investors who want to understand the integrity standards governing Australian markets.

What insider trading actually means under Australian law

Most people assume insider trading means knowing something about a company and acting on it. The legal definition is both more precise and more expansive than that intuition suggests.

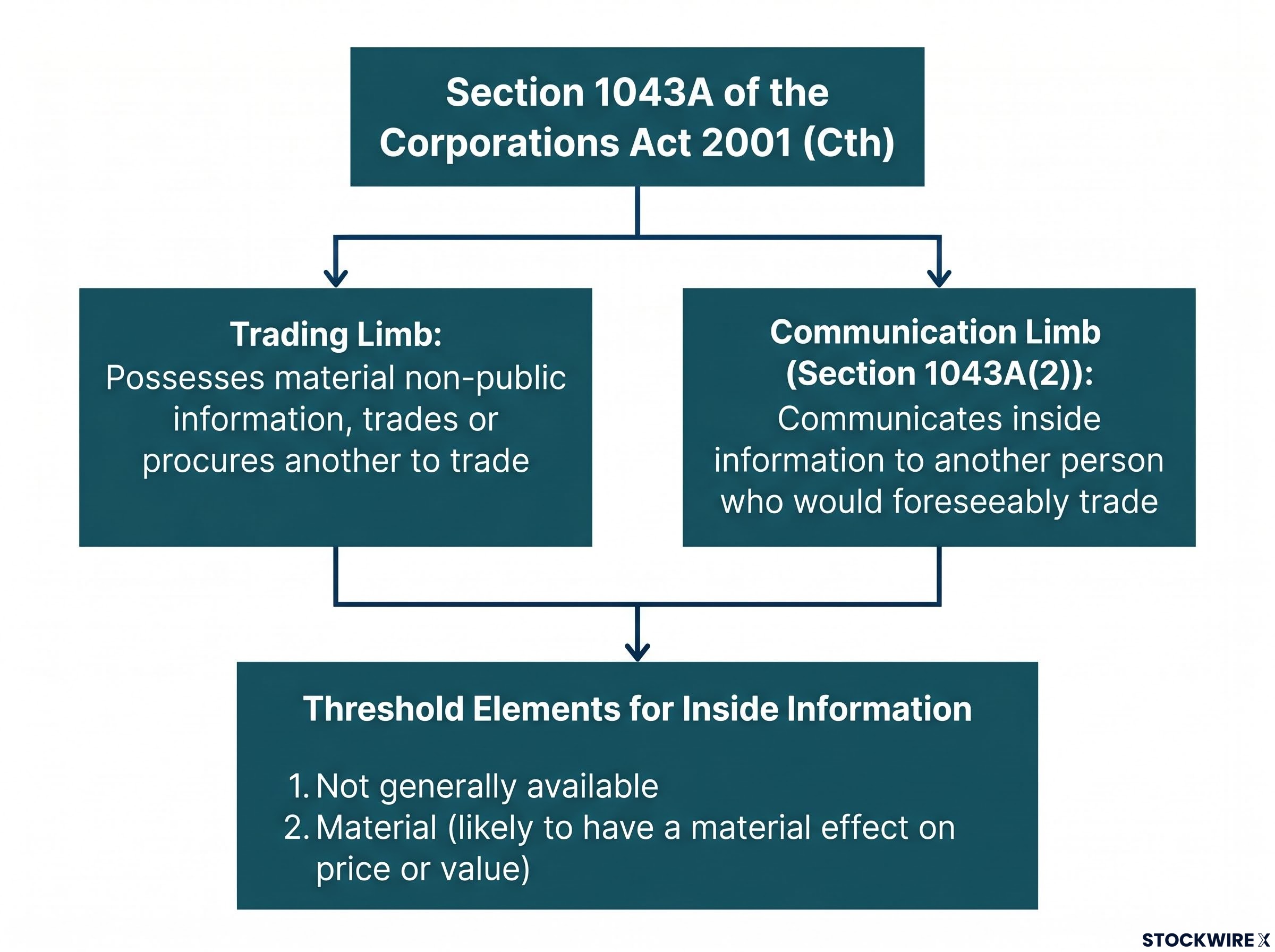

The offence is codified under section 1043A of the Corporations Act 2001 (Cth), and it operates through two distinct limbs:

- The trading limb: A person who possesses material non-public information about a financial product trades in that product, or procures another person to trade.

- The communication limb (section 1043A(2)): A person communicates inside information to another person who would foreseeably trade on it, even if the communicator never trades themselves.

The second limb is where the offence extends well beyond the boardroom. A company director who shares confidential earnings data with a friend over dinner can be guilty even if the director never buys or sells a single share. The friend, depending on what they knew and what they did with the information, may also be caught.

Two threshold elements define what qualifies as “inside information.” The information must be not generally available, and it must be material.

Information is material if it “would, or would be likely to, have a material effect on the price or value” of the financial product.

The offence applies to anyone in possession of material non-public information, not just company insiders by title. A contractor, an analyst, or a retail investor who receives a tip from someone with access to unreleased results can all fall within the statutory scope.

Insider trading sits within a broader category of market misconduct that also includes pump-and-dump schemes, wash trading, and spoofing; retail investors who can identify market manipulation warning signs are better positioned to distinguish between a security moving on genuine information and one being artificially inflated.

When big ASX news breaks, our subscribers know first

How the criminal penalty regime for insider trading is structured and scaled

The penalties attached to insider trading have not remained static. Parliament has escalated them deliberately, and the trajectory tells its own story about how seriously the offence is treated.

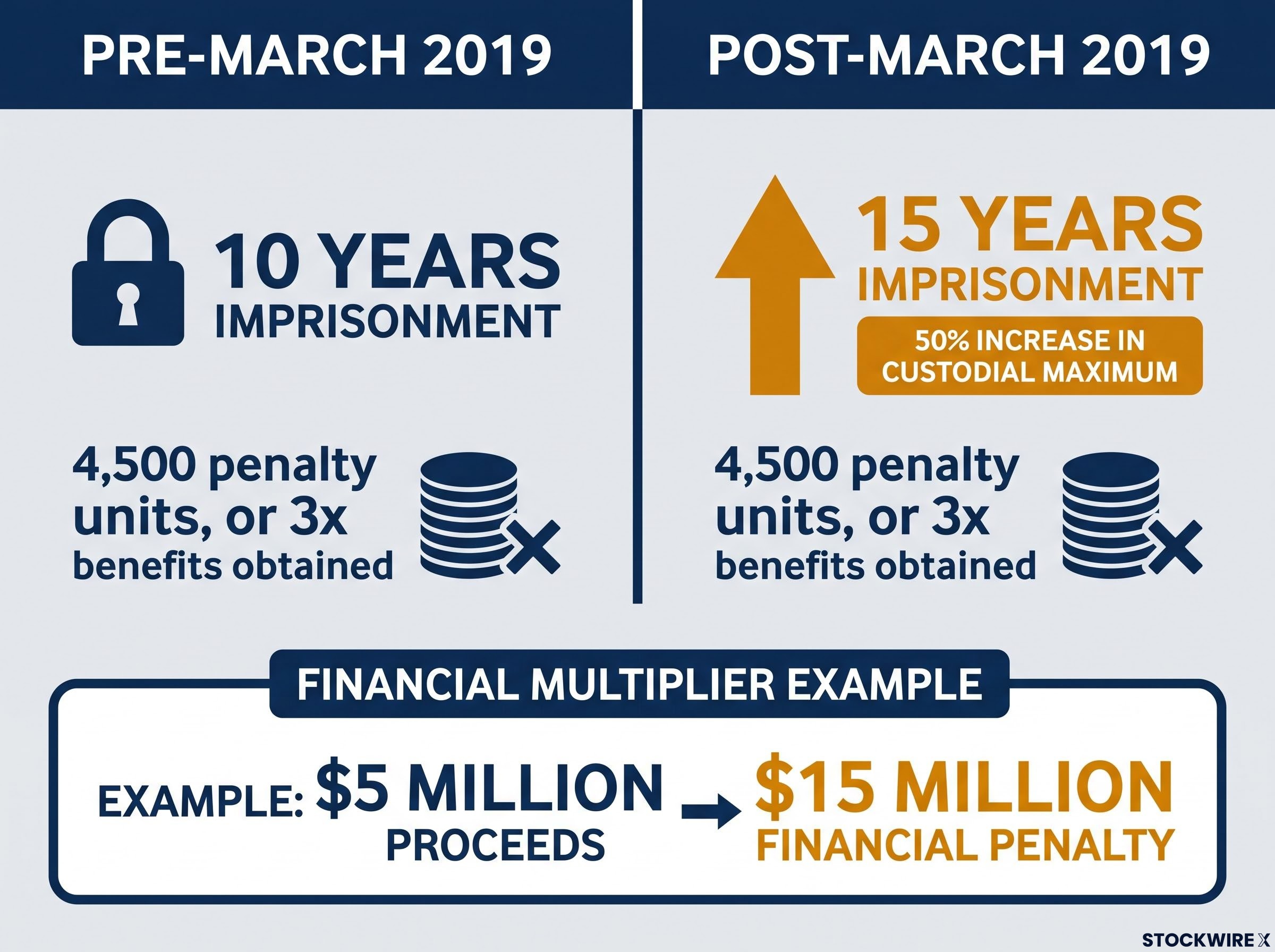

Prior to March 2019, the maximum penalty for insider trading offences was 10 years imprisonment and/or a fine equivalent to 4,500 penalty units, with an alternative financial penalty of three times the total value of benefits obtained from the offending conduct. Following a legislative amendment in March 2019, the maximum custodial sentence rose to 15 years imprisonment, while the financial penalty unit cap remained unchanged.

| Time Period | Maximum Custodial Penalty | Financial Penalty |

|---|---|---|

| Pre-March 2019 | 10 years imprisonment | 4,500 penalty units, or 3× benefits obtained |

| Post-March 2019 | 15 years imprisonment | 4,500 penalty units, or 3× benefits obtained |

The “three times benefits obtained” provision means the financial penalty scales with the profits generated by the offence.

Under this alternative pathway, if an individual is alleged to have generated $5 million in proceeds from insider trading, the court could impose a financial penalty of up to $15 million, regardless of the penalty unit calculation.

A 50% increase in the custodial maximum represents a deliberate legislative signal. This is not a technical compliance breach with a technical penalty; it is a financial crime carrying consequences comparable to serious fraud.

No further statutory changes to the insider trading penalty regime have been made since the March 2019 amendment through mid-2026. What has changed is how the sentencing range is actually applied. Michael Ming Jinn Ho, a former investment analyst convicted of insider trading offences between 2016 and 2018, received a three-year intensive correction order rather than full-time custody, illustrating the breadth of judicial discretion within the available range.

How ASIC detects insider trading before anyone is charged

The gap between committing insider trading and being charged with it is filled by surveillance infrastructure that most market participants never see operating.

ASIC relies on real-time market surveillance tools and cross-venue data feeds, maintained in cooperation with the ASX and other market operators, to monitor trading activity across Australian financial markets. These systems are designed to detect anomalous patterns: trades that cluster around material announcements, unusual volume spikes in otherwise thinly traded securities, and order flows that diverge from a security’s established trading behaviour.

Machine-learning-enhanced alerting has expanded what these systems can identify. A single trade placed before an earnings announcement might look innocuous. But when surveillance tools aggregate trades across multiple accounts, venues, and time intervals, the pattern can become unmistakable.

The surveillance infrastructure described above underpins the Australian market cleanliness rating measured by ASIC Report 787, which ranked Australian equity markets among the world’s cleanest across a six-year period, though that rating captures only detectable pre-announcement trading patterns and does not address the full range of potential misconduct.

- ASIC market surveillance detects anomalous trading through cross-market data feeds and algorithmic alerting systems

- ASIC investigation and evidence gathering follows, involving document production, communications analysis, and witness examination

- Referral to the CDPP for criminal prosecution decision, where the Commonwealth Director of Public Prosecutions assesses whether the evidence meets the standard for criminal charges

Why prosecution is harder than detection

Detection identifies a suspicious pattern. Prosecution requires proving what a specific person knew, and when they knew it.

Establishing that an individual possessed specific inside information at a specific moment demands documentary evidence or testimony, not just trading pattern analysis. Emails, text messages, meeting records, and witness accounts must reconstruct the information chain from source to trade.

The Andrew Corner proceedings illustrate this gap concretely. ASIC alleged Corner directed two companies under his control to sell 1.7 million Big Un shares while holding material non-public information. Evidence was presented. A jury deliberated. On 30 March 2026, the jury concluded without reaching a unanimous verdict. The Commonwealth Director of Public Prosecutions (CDPP) subsequently discontinued charges in June 2026 (ASIC media release 26-108MR).

A hung jury is not an acquittal. But it demonstrates that even when surveillance identifies the pattern and investigators build the case, the evidentiary burden of proving possession remains the prosecution’s most formidable challenge.

The Big Un sweep: what one enforcement cluster reveals about ASIC’s methods

The Big Un enforcement matter is not a single prosecution. It is a multi-year, multi-defendant sweep that reached an investment analyst, a chief financial officer, and two auditors, and it remains the most fully reported insider trading enforcement cluster in recent Australian regulatory history.

Each individual in the sweep faced a different enforcement mechanism, and the outcomes map the range of tools ASIC deploys.

| Individual | Role | Alleged or Proven Conduct | Outcome |

|---|---|---|---|

| Michael Ming Jinn Ho | Investment analyst | 5 insider trading counts + 1 count communicating inside information (2016-2018) | Convicted; 3-year intensive correction order (ASIC 20-209MR) |

| Graham Rothesay Swan | External auditor | Failed to conduct 2017 Big Un audit to applicable standards | Criminally convicted (ASIC 22-198MR) |

| Jakin Leong Loke | Auditor | Involvement in non-compliant 2017 Big Un audit | Auditor registration suspended 12 months (ASIC 22-049MR) |

| Andrew Corner | Former CFO | Alleged sale of 1.7M shares through controlled companies while holding inside information | Hung jury 30 March 2026; charges discontinued June 2026 (ASIC 26-108MR) |

Corner is alleged to have facilitated the sale of 1.7 million Big Un shares through two privately held companies, generating proceeds exceeding $5 million, while allegedly in possession of inside information.

An additional related matter involving Evans (ASIC media release 26-069MR) forms part of the same enforcement cluster, though publicly available detail on that action is limited.

The sweep’s structure is what distinguishes it. ASIC did not pursue only the most obvious trading participant. The investigation extended to the professional advisers whose audit failures created or failed to prevent the information environment in which the trading occurred. When investors read a company’s audit and governance disclosures, those documents sit within a live enforcement context where the quality of the audit itself can become the subject of regulatory action.

What the public record reveals about ASIC’s enforcement direction in 2026

ASIC’s stated direction and the publicly accessible record do not tell the same story in the same level of detail. Both layers matter, and the gap between them is itself informative.

ASIC’s enforcement escalation since late 2024 reflects a deliberate institutional decision to compress the pipeline from surveillance to criminal referral, with the dedicated insider trading team established in September 2024 designed specifically to increase the volume and speed of prosecutions reaching the CDPP.

What ASIC has communicated:

ASIC’s published enforcement priorities explicitly list insider trading under the category of misconduct damaging market integrity, with strengthening the investigation and prosecution of insider trading conduct named as a specific commitment for 2026.

- Insider trading has been designated as an enforcement priority for 2026

- A dedicated specialist insider trading team has been established to expedite investigations and increase the volume of criminal referrals to the CDPP

- Surveillance infrastructure includes machine-learning-enhanced alerting and cross-market data sharing arrangements with the ASX

What is not confirmed in publicly indexed documents as at early June 2026:

- No ASIC publication separately itemises insider trading as a named standalone priority distinct from broader market integrity themes

- No publicly available document discloses the structure, staffing, or case targets of any specialist insider trading unit

- No post-January 2024 new insider trading prosecution has been announced in publicly indexed ASIC media releases or major Australian business press beyond the Big Un matter

What the public record does and does not show

No ASIC or ASX document published since January 2024 provides a discrete insider trading alert count, investigation volume, or case-target metric. This is consistent with ASIC’s broader reporting pattern: aggregate enforcement outcomes are published, but insider-trading-specific metrics are not disaggregated from overall market misconduct categories.

The 46 convictions since 2009 remain the baseline against which any 2026 activity is measured. The absence of headline prosecutions in 2025-2026 does not necessarily indicate reduced enforcement activity. ASIC’s surveillance infrastructure is active and its capability has expanded. But the publicly accessible record does not currently support quantified claims about recent enforcement volume or direction. The opacity is a structural feature of how ASIC communicates, not a signal that should be read in either direction.

What 46 convictions and a specialist unit mean for investors watching Australian markets in 2026

The enforcement record is not theoretical. 46 criminal convictions since 2009, including convictions of company chairs and chief executives, represent sustained regulatory action over more than 15 years. The 15-year maximum custodial penalty enacted in March 2019 defines the seriousness of the offence at the statutory level. Ho’s intensive correction order demonstrates that courts apply meaningful consequences within the sentencing range, even where full-time custody is not imposed.

For retail investors, the practical implications are specific:

- The communication limb applies to tip recipients. Under section 1043A(2), receiving market-sensitive information from someone with access to non-public data is not a safe harbour. Depending on what the recipient knew and how they acted, the offence can reach them directly.

- Surveillance operates in real time. ASIC’s cross-market monitoring and machine-learning alerting systems are designed to detect patterns that individual participants cannot see from their own trading position. “No one will notice” is a poor risk assessment.

- A hung jury does not mean absence of risk. The Corner proceedings demonstrate ASIC’s willingness to prosecute difficult insider trading cases regardless of outcome certainty. A failure to convict is not the same as a determination that no offence occurred.

46 individuals have been criminally convicted of insider trading since 2009, including chief executives and company chairs, as a result of ASIC-led investigations.

The enforcement infrastructure that produced those convictions remains active. The surveillance systems have been upgraded. The penalties have been escalated. For investors operating in Australian markets, these are not background facts; they are the integrity standards within which every trade is placed.

For readers wanting to understand how Australian appellate courts assess objective seriousness in insider trading matters, our full explainer on insider trading sentencing mechanics examines the Forrest re-sentencing in detail, including how courts distinguish subjective factors from the objective gravity of the offence and why a reduced term can still signal a toughened enforcement environment.

The enforcement record is real, the gaps are real, and both matter

ASIC’s 46-conviction record and the escalating penalty regime that supports it represent genuine enforcement built over more than 15 years. The Big Un sweep demonstrated that enforcement reaches beyond individual traders to the auditors and advisers who shape a company’s information environment. These are not regulatory gestures; they are completed proceedings with real consequences for the individuals involved.

The gaps are equally real. The most high-profile prosecution in the Big Un cluster ended without conviction. The publicly accessible record for 2025-2026 does not contain new insider trading cases, and disaggregated enforcement data for this offence category is not published. The specialist unit and 2026 priority designation, whatever their precise public mandate, exist against an infrastructure that has already produced those 46 convictions, and retail investors can reasonably treat that record as evidence of ongoing regulatory vigilance.

Investors who want to track ASIC’s current enforcement posture directly can consult the regulator’s published enforcement priorities and media releases at asic.gov.au. Those who receive market-sensitive information through professional or personal networks should consider seeking independent legal advice before acting, given the reach of both limbs of section 1043A.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.