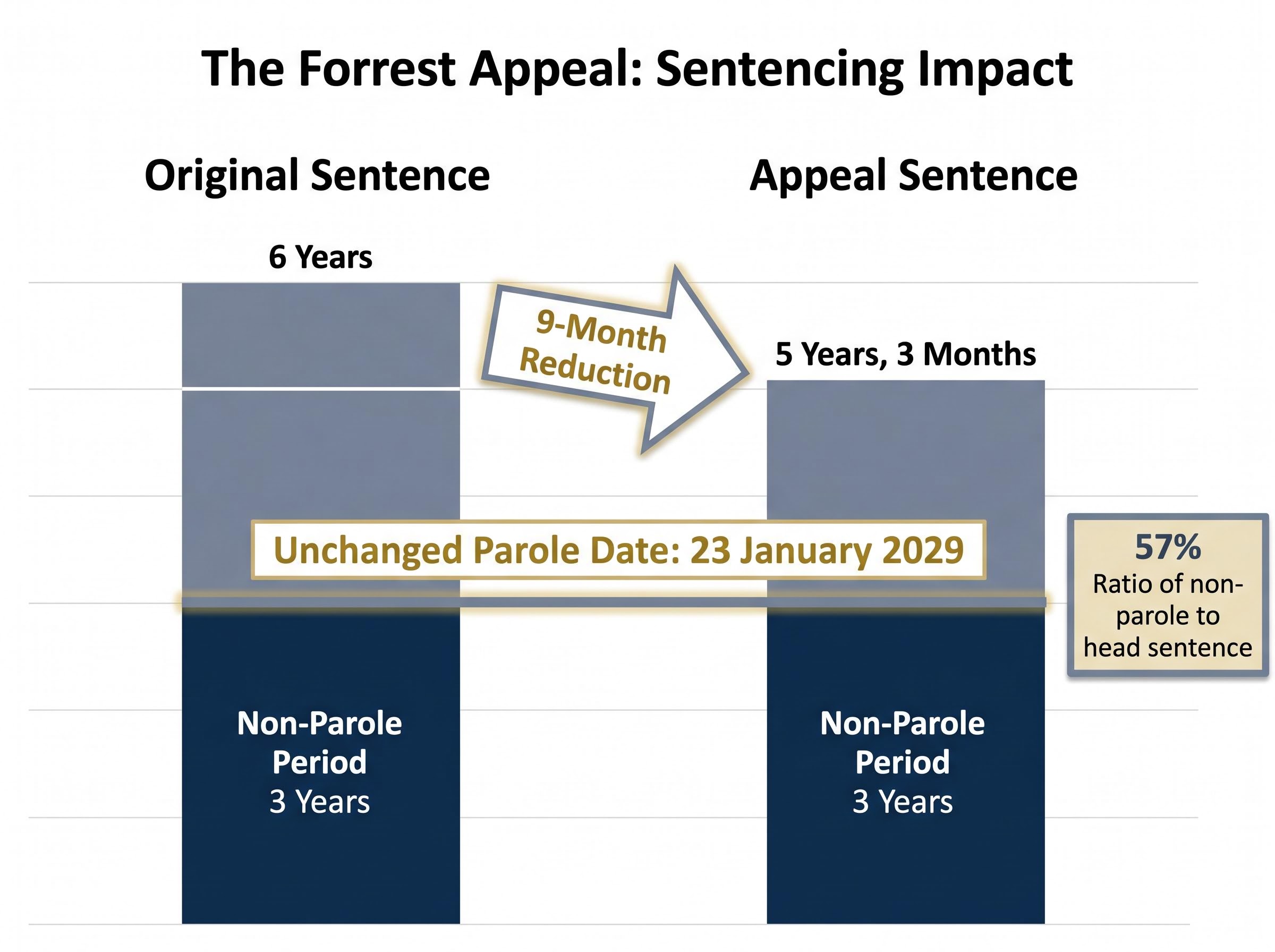

A nine-month sentence reduction sounds like a win for the defence. The Full Federal Court, however, made clear that the conduct was premeditated, executed with sophisticated planning, and involved a significant breach of trust. Rodney Forrest’s revised sentence of five years and three months is a reduction in form, not a reprieve in substance.

The Full Federal Court’s decision to re-sentence Forrest following his January 2026 conviction for insider trading involving Platinum Asset Management shares is the most significant recent appellate ruling in Australian market misconduct law. It clarifies a technically important but practically consequential question: what factors belong in the assessment of objective seriousness, and what factors belong elsewhere in the sentencing calculus. For anyone tracking insider trading penalties in Australia, this distinction carries weight well beyond the Forrest matter itself.

What follows is a walkthrough of the case facts, the specific legal error that succeeded on appeal, and the sentencing principles (general deterrence, breach of trust, and remorse) that Australian courts apply when measuring the gravity of insider trading offences. The analysis concludes with a clear framework for interpreting how courts weigh these cases, grounded in the specific facts of the Forrest decision.

The Forrest case in brief: what happened and how it ended up on appeal

Rodney Forrest worked as an investment manager, a position that gave him access to material non-public information about Platinum Asset Management. He used that access to trade in Platinum shares and to procure others to do the same, with the total value of trades exceeding $3 million.

The procedural sequence moved with unusual speed:

- ASIC conducted an investigation lasting approximately six months before referring the matter to the Commonwealth Director of Public Prosecutions (CDPP)

- Forrest entered a guilty plea at first mention at the Downing Centre Local Court in August 2025

- He was sentenced in January 2026 to six years’ imprisonment, with a three-year non-parole period and parole eligibility set for 23 January 2029

- Forrest appealed the sentence to the Full Federal Court

- The Full Court reduced the head sentence to five years and three months, a reduction of nine months, but left the non-parole period and parole eligibility date unchanged

The Full Court characterised the conduct as “premeditated, planned, involving a considerable breach of trust, and executed with a high degree of sophistication.”

That characterisation was not disturbed on appeal. What the Full Court corrected was narrower, and more technically precise, than the headline reduction might suggest.

When big ASX news breaks, our subscribers know first

How Australian courts sentence insider traders: the framework that makes this case legible

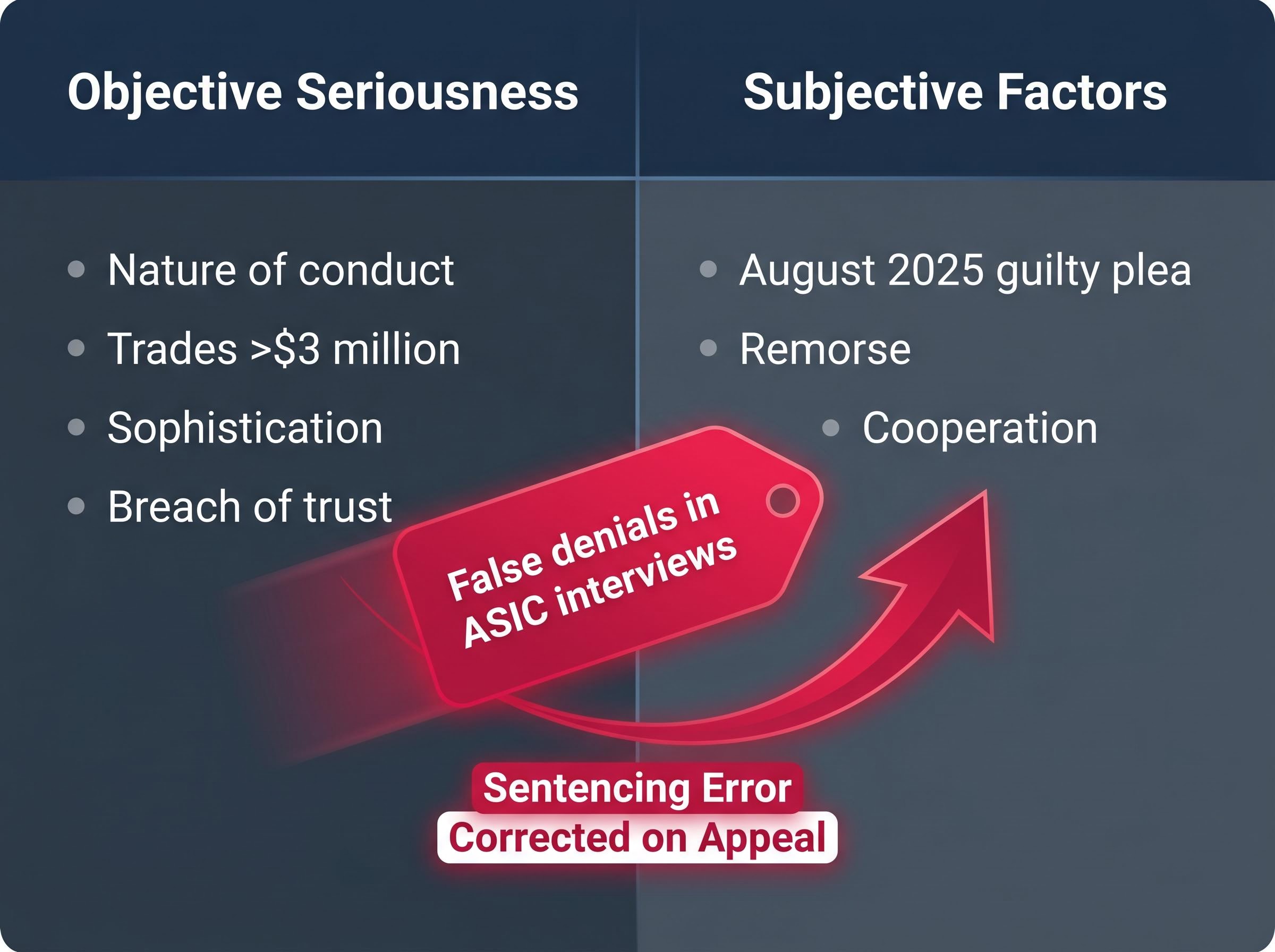

Australian insider trading sentencing rests on two analytically separate assessments. The first is objective seriousness: the gravity of the conduct itself, assessed independently of who committed it. This includes the nature of the offending, the scale of the trades, the degree of planning, and whether a breach of trust was involved. The second is subjective factors: the offender’s personal circumstances, including remorse, cooperation with authorities, the timing and value of a guilty plea, and prior character.

These two categories are not interchangeable. Objective seriousness sets the baseline. Subjective factors then adjust the sentence up or down from that baseline. Understanding this distinction is what makes the Forrest appeal outcome legible rather than arbitrary.

Subjective factors courts commonly consider include:

- Remorse (whether genuine contrition has been demonstrated)

- Guilty plea (its timing and the utilitarian value of avoiding a trial)

- Cooperation with investigators

- Prior character and criminal history

Why general deterrence carries particular weight in insider trading cases

The Full Court identified general deterrence as a primary sentencing consideration in the Forrest re-sentencing. Courts have repeatedly emphasised this factor in market misconduct cases for two reasons.

First, insider trading is a covert offence. It is difficult to detect without sophisticated market surveillance and data analysis, which means courts cannot rely on the certainty of detection alone to discourage potential offenders. The severity of consequences must do the work that visibility cannot.

Courts and commentators disagree on whether financial penalties achieve deterrence beyond the headline dollar amount when the defendant is a large institutional firm; the Macquarie short sale case exposed this tension directly, with critics noting the $35 million civil penalty was financially immaterial to the firm while proponents pointed to mandatory independent expert reviews and public declarations as the genuine deterrence mechanism.

Second, the harm is diffuse. Unlike fraud targeting a single identifiable victim, insider trading corrodes the confidence and position of all market participants. Courts give explicit weight to this systemic harm. ASIC Report 787 (REP 787), published in July 2024, assessed Australian equity markets as among the world’s cleanest over the period November 2018 to April 2024. That is the market integrity standard courts are protecting when they impose sentences designed to deter.

The Australian market cleanliness rating produced by ASIC REP 787 is a statistical proxy based on detectable informed trading ahead of price-sensitive announcements, not a direct count of insider trading incidents, which means a low score reflects the absence of a measurable footprint rather than a confirmed zero rate of misconduct.

The legal error that opened the door to appeal

The original sentencing judge incorporated Forrest’s false denials during his initial ASIC interviews into the assessment of objective seriousness. The Full Court ruled this was an error.

False denials in interview are post-offence conduct. They speak to the offender’s character, his willingness to cooperate, and the weight that should be given to his eventual guilty plea. They are, in legal terms, a subjective factor. They do not describe the offence itself.

Objective seriousness, properly assessed, contains the nature of the trading, the scale of the transactions, the degree of premeditation and sophistication, and the breach of trust inherent in misusing a professional position. None of these elements includes what the offender said to investigators after the conduct was complete.

| Objective Seriousness Factors | Subjective / Personal Factors |

|---|---|

| Nature and type of insider trading conduct | False denials in ASIC interviews |

| Total value of trades (in excess of $3 million) | Timing and value of guilty plea (August 2025) |

| Degree of planning and sophistication | Evidence of remorse or contrition |

| Breach of trust (professional position) | Cooperation with authorities |

| Procuring others to trade | Prior character and criminal history |

This is not a matter of judicial preference. Misclassifying a subjective factor as an objective one inflates the starting point for the sentence before mitigating factors are applied. The result is a longer term than the law permits. The Full Court corrected the error and reduced the head sentence by nine months.

The Full Court confirmed that, notwithstanding the identified error, the offending remained serious and warranted substantial imprisonment.

The correction was precise. It did not recharacterise the conduct or soften the court’s view of its gravity.

What the unchanged non-parole period signals about courts’ appetite for leniency

A nine-month reduction to the head sentence invites a natural reading: the appeal succeeded, and the outcome was more favourable. That reading is incomplete.

The three-year non-parole period was not altered. The earliest date Forrest can seek release on parole remains 23 January 2029, identical to the original sentence. The floor of the sentence, the minimum period actually served before parole eligibility, was treated as appropriate by the Full Court.

The logical sequence is worth tracing:

- The head sentence was corrected from six years to five years and three months to remove the effect of the identified legal error

- The non-parole period of three years was retained without adjustment

- The practical release date of 23 January 2029 is unchanged

- Future appeals in similar cases should not assume that a successful challenge to the head sentence will produce a corresponding reduction to the non-parole period

A three-year non-parole period against a five-year-three-month head sentence represents a ratio of approximately 57%. The Full Court’s correction was targeted and narrow. It removed a specific legal error without extending broader mercy, and the minimum time Forrest will actually serve before he is eligible for release reflects the court’s continued emphasis on actual imprisonment as a deterrent signal.

ASIC’s enforcement posture and what this case tells market participants

The Forrest prosecution did not emerge from a vacuum. It fits within a deliberate escalation of ASIC’s insider trading enforcement posture. A specialist insider trading team was established in late September 2024 to accelerate investigations and increase the volume of criminal briefs referred to the CDPP. Insider trading enforcement has been designated a priority area for both 2025 and 2026.

Three markers define the changed enforcement environment:

- A dedicated insider trading enforcement team with concentrated investigative resources

- A faster referral pipeline from ASIC investigation to CDPP criminal prosecution

- An increased volume of criminal briefs being prepared and referred

The Forrest matter illustrates what this structure produces. A six-month investigation led to referral, and a guilty plea was entered at first mention. Concentrated investigative resources, applied to a well-defined offence type, produced an early resolution that reduced trial burden and accelerated the deterrence outcome.

ASIC has identified insider trading as a priority enforcement area for 2026, reinforcing its commitment to market integrity through criminal prosecution of market misconduct.

ASIC Report 787 (REP 787, July 2024) assessed Australian equity markets as among the world’s cleanest over a multi-year measurement period. That assessment is the baseline ASIC is working to protect. The enforcement investment in specialist teams, faster pipelines, and criminal referrals reflects a structural commitment to maintaining that standard.

ASIC Report 787, published in July 2024, assessed Australian equity markets across a multi-year measurement period covering November 2018 to April 2024, concluding that Australia’s markets operate with a high degree of integrity, a standard that informs the severity with which courts approach insider trading offences designed to corrode that integrity.

For investment professionals with access to material non-public information, the risk calculus has materially changed. The enforcement environment is more structured, more rapid, and more likely to result in criminal prosecution than it was five years ago.

Criminal prosecution of finance professionals has accelerated across multiple domains beyond insider trading, with ASIC pursuing directors of failed AFSL holders under section 1041G of the Corporations Act in cases where client funds were misused, a pattern that confirms the regulator’s structural shift toward personal criminal liability rather than firm-level civil remedies.

The shift toward personal liability for disclosure failures is not limited to insider trading prosecutions; ASIC is simultaneously pursuing executives for continuous disclosure breaches under sections 180 and 674 of the Corporations Act, making the individual accountability theme a defining feature of the regulator’s 2025-2026 enforcement strategy.

A precise correction, not a lenient outcome: the Forrest appeal in proper perspective

The Full Federal Court’s decision clarified an important sentencing principle. Objective seriousness must be assessed on the nature of the conduct alone. Post-offence behaviour, including false denials in regulatory interviews, belongs in the subjective analysis. Correcting a technical sentencing error does not require a wholesale re-evaluation of sentence severity.

What the appeal did not change is at least as significant as what it did. The characterisation of the conduct as premeditated, sophisticated, and involving a considerable breach of trust was not disturbed. The non-parole period was retained. The parole eligibility date of 23 January 2029 was unchanged. General deterrence was explicitly endorsed as the dominant sentencing consideration.

The net result: a nine-month reduction to the head sentence and zero change to the minimum time served before parole eligibility.

Australian courts will correct legal errors when they exist. The Forrest decision confirms that. It also confirms that appellate correction in market misconduct cases is a precise instrument, not an invitation to reconsider whether the sentence was broadly too harsh. The floor held.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.