In July 2024, the Australian Securities and Investments Commission (ASIC) published a finding that should matter to every investor placing capital into ASX-listed equities: Australian markets rank among the cleanest in the world. The claim appeared in Report 787 (REP 787), which assessed more than five and a half years of trading data across ASX-listed securities, covering the period from 1 November 2018 to 30 April 2024. Published on 24 July 2024, the report offered a confident verdict on the integrity of the exchange where most Australian retail portfolios live. Yet the rating rests on a specific measurement methodology that most investors have never encountered, and the headline finding carries boundaries that the headline itself does not disclose. What follows explains exactly what “market cleanliness” means in regulatory terms, how ASIC measured it, what REP 787 found, and where the rating’s limits sit for everyday investors.

What “market cleanliness” actually means for investors

The instinct is to read “clean” as “no cheating.” The regulatory definition is more precise and more narrow. Market cleanliness, as ASIC uses the term, refers to the absence of detectable informed trading ahead of price-sensitive corporate announcements. REP 787 assessed whether announcements, specifically takeover announcements and profit or earnings surprise announcements, were preceded by statistically unusual price movements during the review period of 1 November 2018 to 30 April 2024.

Pre-announcement price behaviour is the chosen lens because it is observable, quantifiable, and directly linked to whether certain parties accessed material information before the rest of the market. It is not a blanket assessment of fairness across all dimensions of market conduct.

The distinction matters. Market cleanliness does not cover:

- Market manipulation, such as wash trading or spoofing, which distorts prices through artificial activity rather than information asymmetry.

- Conflicted research, where brokerage analysts may issue biased ratings influenced by commercial relationships.

- Poor disclosure quality, where listed companies fail to communicate material information clearly or promptly.

“Australians can be confident in the integrity of our equity markets.” ASIC media release 24-162MR, 24 July 2024

Investors who understand this precise definition can calibrate their trust in the ASX more accurately, rather than treating the headline as a guarantee that every aspect of market fairness has been audited and passed.

When big ASX news breaks, our subscribers know first

How ASIC measured cleanliness: the event-study method explained

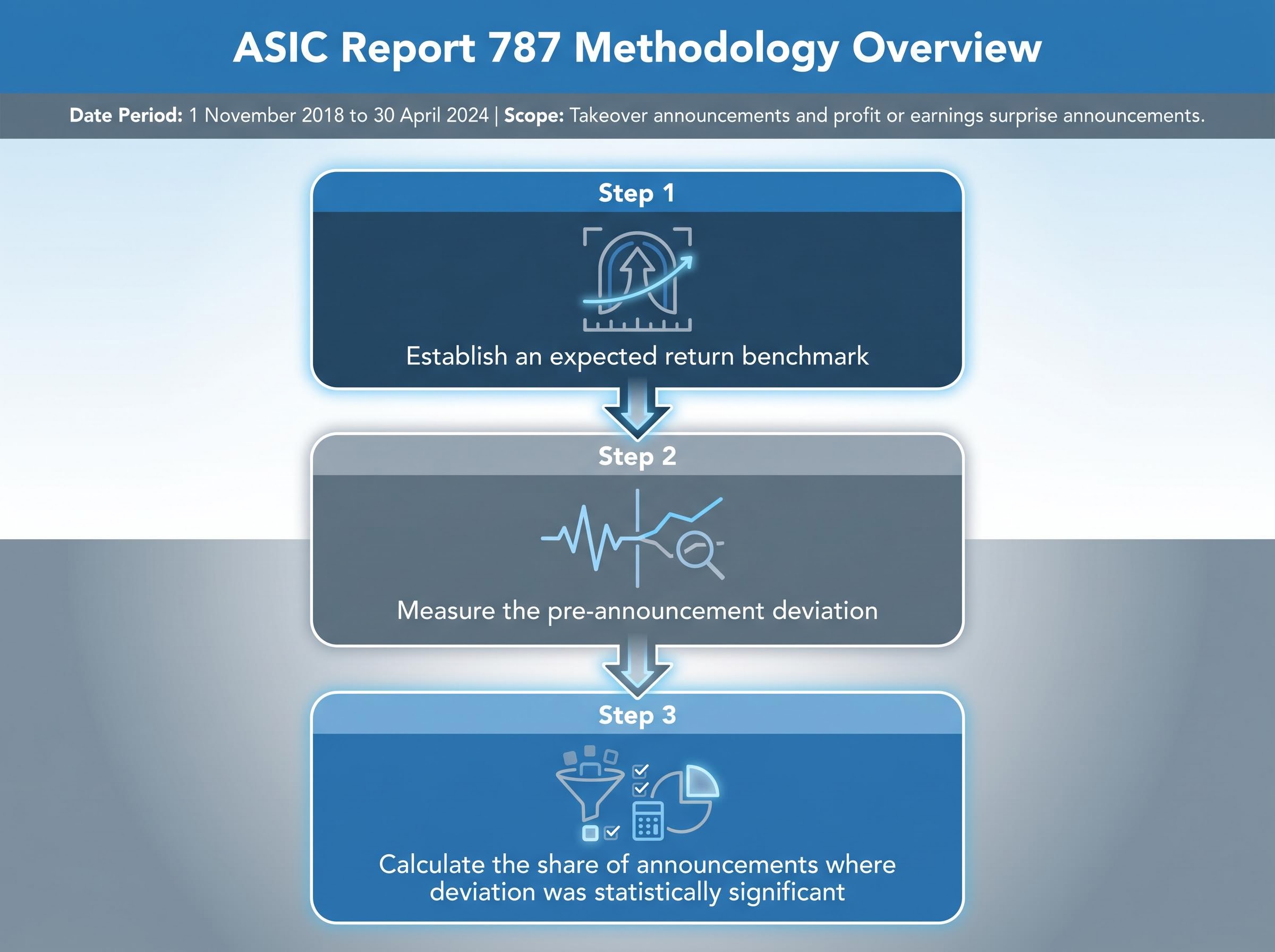

The methodology behind the cleanliness rating works like a detection process. It starts with an observation, tests it against a statistical expectation, and produces a rate.

The approach, described in REP 787 as an event-study style abnormal return analysis, follows a three-step logic:

The event-study method works precisely because price discovery mechanics on a modern exchange are transparent and time-stamped; every order, fill, and cancellation leaves a data trail that statistical analysis can interrogate against an expected baseline.

- Establish an expected return benchmark. For each announcement, ASIC constructed a model of what “normal” trading activity would look like, drawing on historical price and volume data adjusted against index-level benchmarks.

- Measure the pre-announcement deviation. If a stock moved significantly more than the benchmark predicted in the days before a price-sensitive announcement, that deviation was flagged as potentially abnormal.

- Calculate the share of announcements where deviation was statistically significant. The output is a rate: the proportion of announcements preceded by unusual price activity, not a count of proven insider-trading cases.

The data sources feeding this analysis included ASX-listed equity announcement data, price and volume data, and ASIC’s own surveillance and data analytics systems. The two inputs examined most closely were pre-announcement price movements and volume spikes relative to the benchmark expectation.

Understanding this is worth the effort. The cleanliness score is a statistical signal, not a verdict. A low rate of abnormal pre-announcement trading does not mean insider trading did not occur; it means the methodology did not detect a statistically significant footprint. That distinction shapes how much weight any investor should assign the rating.

Which announcements were included in the analysis

The analysis covered two categories of corporate announcements: takeover announcements and profit or earnings surprise announcements. These were selected because they represent high-materiality events where information asymmetry, and therefore the incentive for informed trading, is greatest. A leaked takeover bid or an early tip about an earnings miss creates the clearest window for someone with non-public information to profit, making these announcement types the sharpest test of pre-announcement integrity.

What REP 787 actually found, and how Australia compares globally

ASIC’s core finding was direct: Australian equity markets rank among the cleanest globally based on the event-study assessment published on 24 July 2024. The report covered trading activity across ASX-listed equities from 1 November 2018 to 30 April 2024, and the rate of detected abnormal pre-announcement price movements was low enough for ASIC to position Australia favourably against peer markets.

ASIC Report 787 covers more than five and a half years of trading data across ASX-listed securities, applying an event-study abnormal return analysis to assess whether corporate announcements were preceded by statistically unusual price movements during the review period from 1 November 2018 to 30 April 2024.

That positioning, however, is comparative and relative. No single global ranking table exists. The International Organization of Securities Commissions (IOSCO) does not publish a universal cleanliness score, and no post-2024 public report has ranked multiple exchanges side-by-side using equivalent methodology. ASIC’s self-assessed comparative positioning against other well-supervised exchanges remains the primary reference point.

The Australian Financial Review’s July 2024 coverage noted that “cleanliness” is a proxy measure, a framing that matters when reading the headline finding. A low rate of detected abnormal trading reflects well on Australia’s market integrity, but it is not the same as a zero incidence of misconduct.

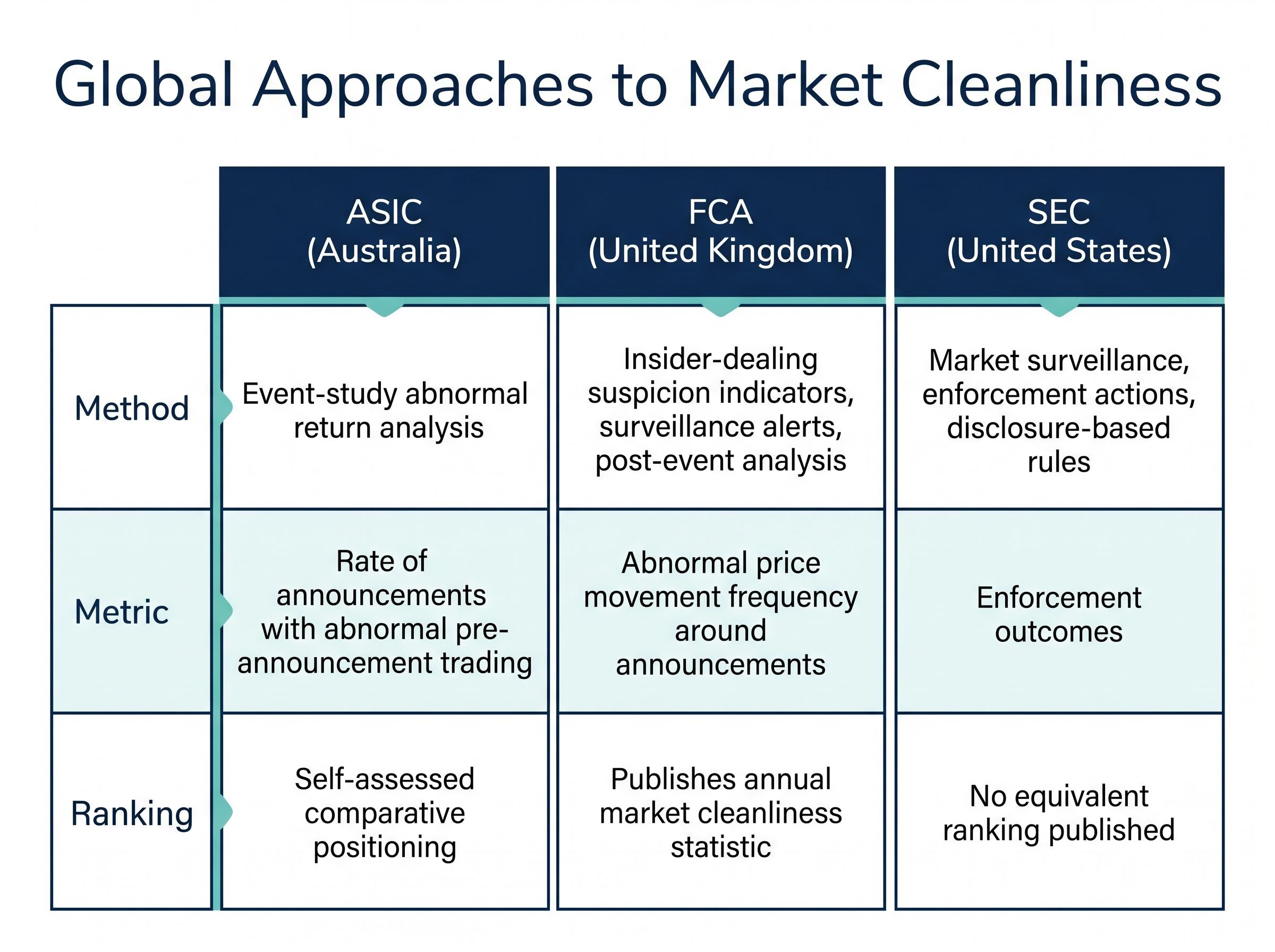

The table below outlines how major regulators approach market cleanliness measurement:

The FCA market cleanliness statistics provide an annual measure of abnormal trading volume and abnormal price movements ahead of corporate announcements on UK exchanges, offering the closest published equivalent to ASIC’s event-study approach and the primary basis for any comparative assessment between the two jurisdictions.

| Regulator | Jurisdiction | Primary Measurement Method | Key Output Metric | Publishes Ranking? |

|---|---|---|---|---|

| ASIC | Australia | Event-study abnormal return analysis | Rate of announcements with abnormal pre-announcement trading | Self-assessed comparative positioning |

| FCA | United Kingdom | Insider-dealing suspicion indicators, surveillance alerts, post-event analysis | Abnormal price movement frequency around announcements | Publishes annual market cleanliness statistic |

| SEC | United States | Market surveillance, enforcement actions, disclosure-based rules | Enforcement outcomes (cases brought, penalties imposed) | No equivalent ranking published |

“Australians can be confident in the integrity of our equity markets.” ASIC media release 24-162MR

The international context reinforces that Australia’s rating reflects genuine comparative strengths in surveillance and disclosure, not simply a favourable methodology choice. But the absence of a standardised global benchmark means the comparison is indicative rather than definitive.

Why Australia’s market structure supports a cleaner result

The data in REP 787 reflects outcomes. The question behind the outcomes is structural: what features of Australia’s market environment make low rates of abnormal pre-announcement trading more likely?

Four identifiable factors contribute:

High continuous disclosure obligations sit at the centre of Australia’s structural advantage: continuous disclosure obligations under ASX Listing Rule 3.1 require listed companies to release price-sensitive information immediately upon awareness, compressing the window during which material non-public information can circulate before reaching ordinary investors.

- High continuous disclosure standards. ASX listing rules impose immediate disclosure obligations for price-sensitive information, reducing the window during which material non-public information can circulate before reaching the market.

- Concentrated institutional ownership. A smaller number of large institutional holders means fewer parties with access to material information at any given time, narrowing the pool of potential informed traders.

- Strong surveillance infrastructure. ASIC’s data analytics systems and the ASX’s own market surveillance capabilities provide overlapping layers of detection.

- Smaller market size. The ASX is significantly smaller than US or UK exchanges. Commentary from Livewire Markets and the Australian Financial Review in July 2024 noted that this reduces the opportunity window for prolonged informed trading, as abnormal activity in a thinner market is more detectable than the same behaviour in a deeper, more liquid exchange.

These factors are not static. If institutional concentration shifts, if disclosure standards weaken, or if surveillance budgets contract, the structural conditions that support the clean rating would change. Investors who understand which factors are doing the work can monitor whether those conditions persist.

The governance question the clean rating does not resolve

One structural feature of Australia’s market sits in a different category. The ASX operates as both market operator and a participant in surveillance activity. This dual role aids detection efficiency; the operator has direct visibility over its own order book. It also raises governance questions about the independence of oversight.

This debate is separate from the REP 787 findings. The cleanliness rating measures pre-announcement trading patterns, not the governance structure of the entity monitoring them. But for investors thinking about systemic risk and the long-term durability of market integrity, the concentration of operational and surveillance functions within a single entity is worth tracking.

Separately, the CHESS (Clearing House Electronic Subregister System) infrastructure replacement programme remains ongoing through 2026. CHESS modernisation is relevant to market resilience and settlement efficiency, but it is a distinct operational issue from market cleanliness in the insider-trading sense.

The limits of the cleanliness score: what it cannot tell you

A rigorous measurement framework always comes with defined boundaries, and ASIC’s methodology is no exception. REP 787 itself acknowledged several limitations that investors should understand before treating the cleanliness rating as comprehensive assurance.

The four specific limitations of the event-study proxy methodology are:

- Sensitivity to announcement window choice. The size of the pre-announcement window examined affects the results. A narrower window may miss slower-building informed trading; a wider one may capture noise unrelated to information leakage.

- Statistical threshold sensitivity. The level at which a price movement is deemed “statistically unusual” is a methodological choice. Adjusting the threshold up or down changes the detected rate.

- Inability to distinguish insider trading from legitimate market anticipation. As ASIC acknowledged, the metric cannot separate genuine insider trading from sector-specific trading patterns, informed speculation based on public signals, or routine pre-announcement positioning by sophisticated investors.

- Exclusion of other fairness concerns. A low rate of abnormal pre-announcement trading says nothing about conflicted research, poor disclosure quality, or broader retail fairness issues.

The metric cannot distinguish insider trading from legitimate information leakage, market anticipation, or sector-specific trading patterns.

Post-report commentary from retail investor advocates, while welcoming the cleaner-market findings, cautioned that detected pre-announcement patterns do not address all retail fairness concerns. Livewire Markets noted in July 2024 that results are sensitive to both the chosen announcement window and the statistical threshold applied.

The cleanliness score functions best as one input among several. Investors assessing the structural integrity of their investment environment benefit from combining it with attention to disclosure quality, enforcement activity, and the governance structures discussed above.

How ASIC is strengthening enforcement beyond the cleanliness score

The REP 787 finding is a snapshot. The enforcement picture behind it is dynamic, and ASIC’s actions since publication indicate the regulator treats market integrity as an ongoing project rather than a completed assessment.

In 2025, ASIC established a specialist insider trading team, with its first reported outcomes appearing in 2026 media releases including 26-007MR. The team’s mandate covers intensified surveillance, intelligence gathering, and an increased focus on criminal referrals to the Commonwealth Director of Public Prosecutions (CDPP).

The enforcement pipeline in action is visible through the Rodney Forrest case. ASIC conducted a six-month investigation into Forrest’s trading in Platinum Asset Management shares before referring the matter to the CDPP. Forrest was convicted of insider trading involving more than $3 million in transactions. Following a re-sentencing, Forrest received a revised sentence of five years and three months, with a non-parole period of three years and parole eligibility from 23 January 2029.

The enforcement deterrence debate is not unique to insider trading: the $35 million penalty imposed on Macquarie Securities in March 2026 for systematic short sale misreporting prompted the same question, with critics arguing the figure was financially immaterial to a firm of that scale and others contending that court declarations and mandatory expert reviews deliver consequences beyond the headline number.

The enforcement sequence illustrates the pipeline’s full arc:

- ASIC surveillance and intelligence identifies suspicious trading patterns.

- Investigation and referral to the CDPP follows, with ASIC building the evidentiary case.

- Prosecution is conducted by the CDPP.

- Sentencing and deterrence signalling completes the enforcement loop, with outcomes publicised to reinforce consequences.

Insider trading has been listed as a designated enforcement priority in ASIC’s 2026 priorities announcement (25-273MR, November 2025).

The combination of a specialist team, active prosecution outcomes, and designated priority status confirms that the clean rating reflects active deterrence and enforcement, not just favourable market conditions. For investors, this means the regulatory infrastructure backing the ASX’s cleanliness rating is functioning, with resources directed specifically at sustaining it.

For investors wanting to understand how insider trading enforcement fits within ASIC’s broader surveillance priorities, our dedicated guide to ASIC’s FY2026-27 financial reporting focus areas covers the regulator’s designated scrutiny domains for revenue recognition, asset impairment, and audit quality, providing a fuller picture of where ASIC is directing its oversight resources across listed company disclosures.

A clean market is not a perfect market, but Australia’s foundations are solid

Australia’s equity markets carry a well-evidenced claim to global cleanliness. That claim is grounded in a rigorous (if proxy-based) methodology, structural conditions that reduce the opportunity for informed trading, and an enforcement apparatus that is demonstrably active.

The reader who has followed this article now understands three things they likely did not before: the precise, narrow definition of market cleanliness as regulators use it; the event-study methodology that produces the rating; and the specific limits of what the score can and cannot guarantee about market fairness.

The combination of REP 787’s findings, the specialist insider trading team established in 2025, and insider trading’s designation as an enforcement priority for 2026 gives Australian investors a credible institutional basis for confidence. That confidence should be informed, not complacent. The cleanliness score is one lens among several when assessing the structural integrity of an investment environment.

Investors seeking primary source detail can access ASIC Report 787 directly, alongside ASIC’s current enforcement priorities page for the latest enforcement positioning.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.