A Barclays analyst has warned investors that the AI-driven equity rally is building fragility into the very market conditions sustaining it, and that conventional hedging tools may not offer adequate protection if a correction arrives. In an investor note published on 2 June 2026, Barclays analyst Stefano Pascale identified a convergence of overextended positioning, rebounding euphoria, and rising interest rate sensitivity across equity markets. The warning stands out not for its bearishness (Pascale remains constructive on the medium-to-long-term outlook) but for its specificity: the note names lookback put options and equity-rate hybrid hedging structures as preferable alternatives to standard puts in the current environment. What follows breaks down what Barclays said, why the identified conditions matter, and what these less familiar hedging instruments actually do.

Barclays says the AI rally’s momentum is becoming its own risk

The rally has been convincing. Corporate earnings have held up. AI enthusiasm has broadened from a narrow cohort of mega-caps into a wider set of beneficiaries. Capital that sat on the sidelines has started chasing performance. Options markets have amplified the upside.

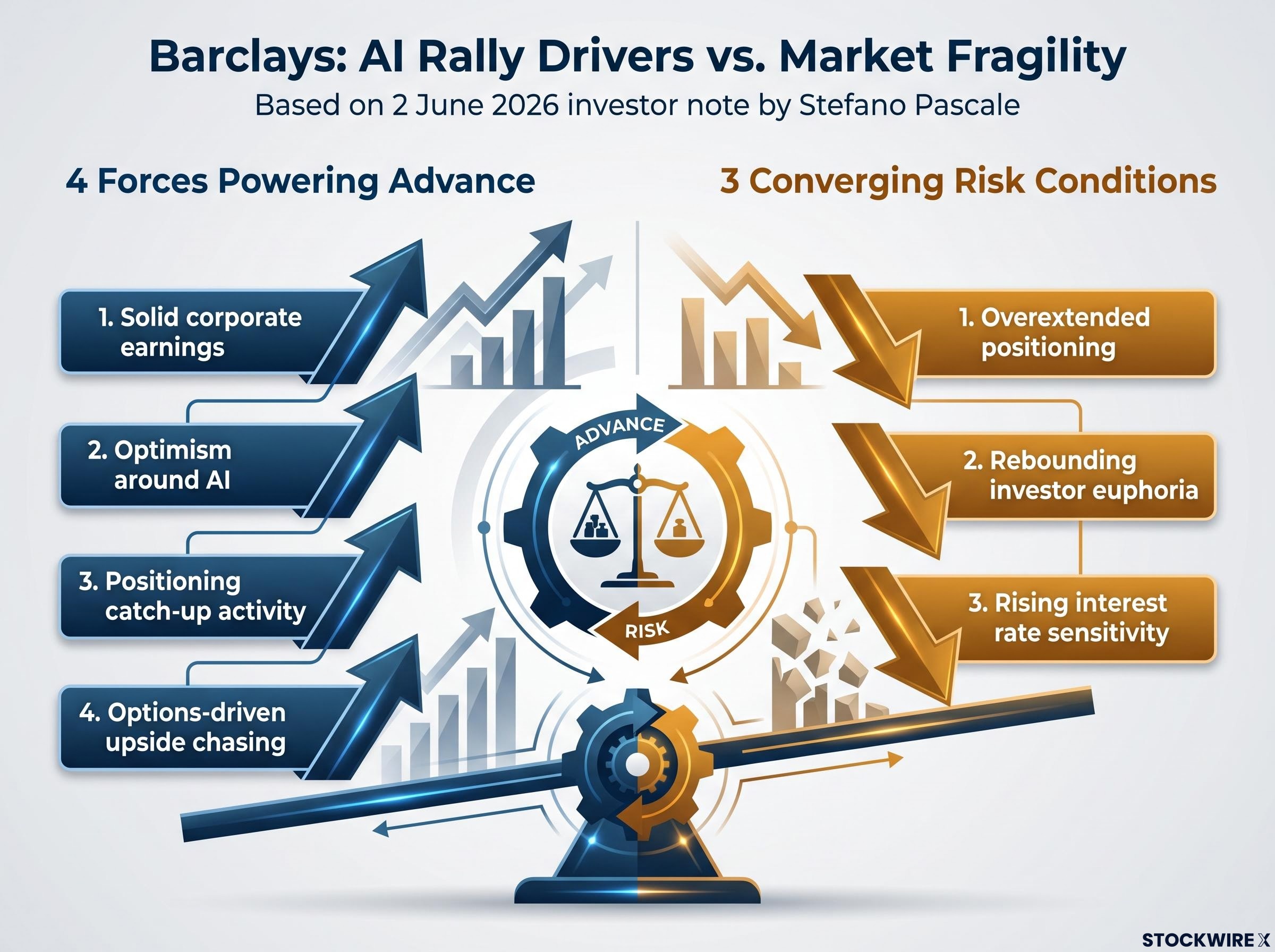

According to Pascale, these four forces powered the advance:

- Solid corporate earnings

- Optimism around AI

- Positioning catch-up activity

- Options-driven upside chasing

Each of those drivers, taken individually, supports the case for higher prices. Taken together, and at their current intensity, Pascale argues they have created a market that is constructive on a multi-month horizon but increasingly exposed to a sharp near-term pullback.

The fragility Barclays identifies sits on top of a valuation foundation that is already historically unusual: AI rally valuations, measured by the S&P 500 Shiller CAPE at 40-41, represent the second-highest reading in 155 years of market data, exceeded only by the dot-com peak of 44.2.

The distinction matters. This is not a bear call. Pascale’s note does not recommend exiting equities. It recommends recognising that the same mechanics propelling the rally, the momentum chasing, the systematic inflows, the euphoria rebound, are precisely the conditions that make a reversal, when it comes, faster and harder to hedge against with conventional tools.

When big ASX news breaks, our subscribers know first

Three converging conditions that worry Barclays right now

The first layer is positioning. Barclays characterises investor exposure as overextended, driven by capital inflows and what the note describes as unstable systematic exposure levels. When positioning is stretched, even a modest change in sentiment can trigger forced selling as systematic strategies unwind simultaneously.

The second layer is sentiment. Barclays noted that market indicators reflect a “strong rebound in investor euphoria.” Euphoria is not inherently dangerous, but it narrows the distance between current positioning and the point at which disappointment triggers a reversal. The margin for error shrinks.

Why rate sensitivity changes the hedging calculus

The third layer, and the one Barclays spends the most time on, is rate sensitivity. Equity markets have grown increasingly reactive to interest rate movements as investors recalibrate toward a more persistent inflation environment and a higher neutral rate scenario.

Rate sensitivity across equity markets has become structurally more pronounced as investors reprice for a higher neutral rate environment, with the IMF estimating that a 100 basis point increase in global long-term real rates lowers equilibrium price-to-earnings ratios on advanced-economy indices by 10-15%, holding earnings constant.

This matters for hedging because it disrupts a long-standing assumption. In a typical environment, bonds rise when equities fall, giving balanced portfolios a natural offset. In a persistent inflation scenario, equities and bonds can decline simultaneously. When both legs of a portfolio move in the same direction, conventional hedging logic breaks down.

Research on inflation expectations and equity-bond correlation shows that persistent inflationary environments compress equity valuations and push bond yields higher simultaneously, producing the correlated drawdown scenario that conventional balanced portfolio construction is structurally unable to offset.

Barclays also noted that volatility has declined and options-market pricing has made purchasing downside protection comparatively more attractive. The conditions, in other words, are favourable for hedging on price; the question is which instruments actually work.

Why conventional puts fall short in current market conditions

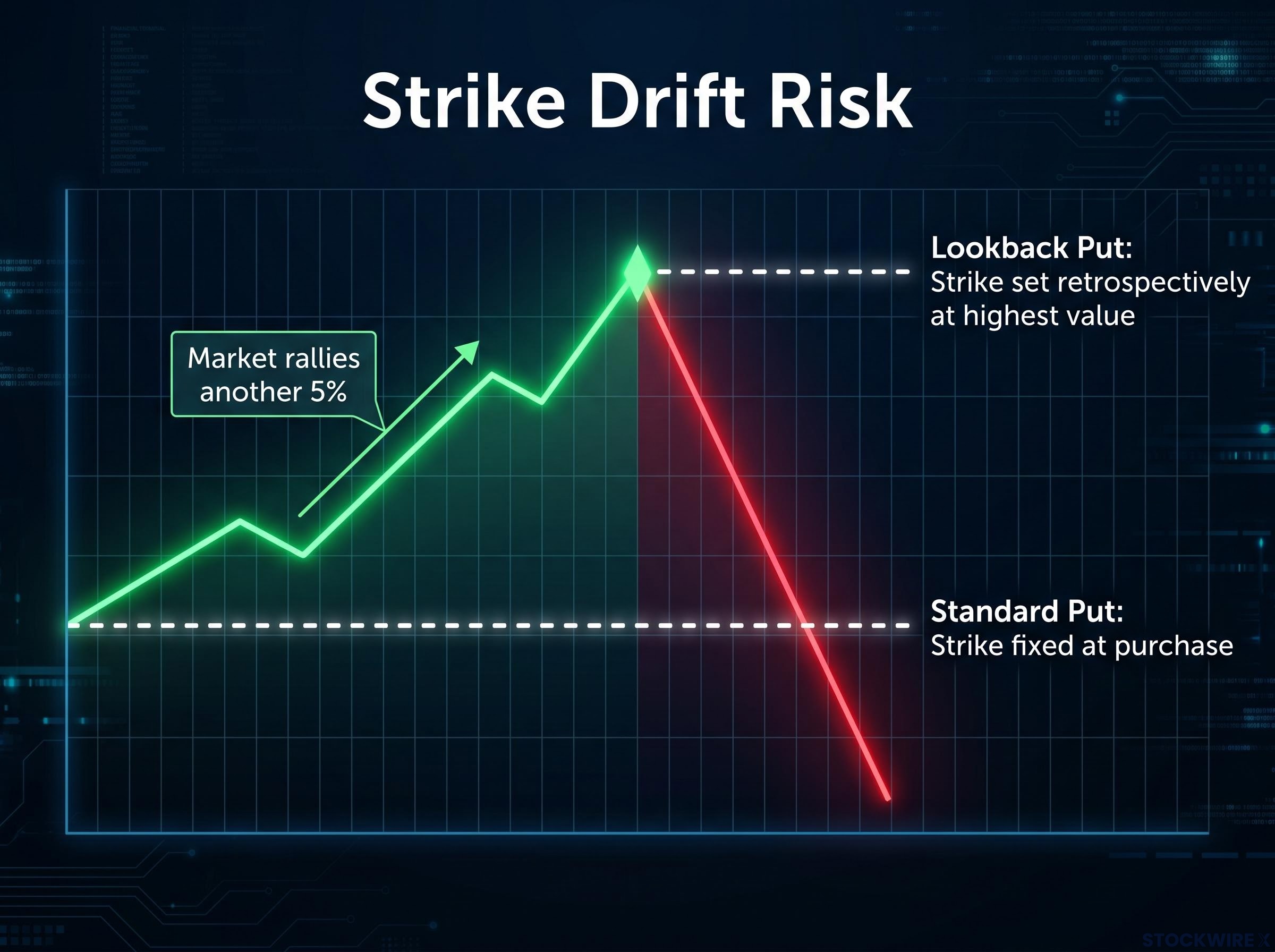

Barclays introduced the concept of “strike drift” to describe a specific problem facing investors who buy standard put options in the current environment.

A standard put option requires the buyer to commit to a strike price at the time of purchase. If the market continues rising before the correction arrives, that strike drifts further away from relevance. The put expires worthless, or delivers far less protection than intended, even though the investor was correct about the eventual direction.

Strike drift risk: In Barclays’ framing, the absence of an identifiable correction trigger means the timing of any pullback is highly uncertain, making it structurally difficult to select the right strike price for a standard put.

The problem is not that puts are bad instruments. The problem is that puts demand timing precision in an environment Barclays explicitly characterises as lacking a visible catalyst. Corrections in these conditions tend to be sudden and sentiment-driven, arriving without the advance signals that give hedgers time to position. Standard puts purchased too early, or at a strike that no longer reflects the market’s level, can underperform precisely when protection is needed most.

Lookback puts and hybrid hedges explained in plain terms

Lookback put options solve the timing problem by removing it. Instead of requiring the investor to choose a strike price upfront, the strike is set retrospectively based on the highest value the underlying asset reaches during the option’s life. If the market rallies another 5% before correcting, the lookback put captures that peak. The investor does not need to predict when the top occurs.

Barclays cited historical analysis supporting a superior risk-reward profile for lookback structures compared with conventional puts, though specific quantitative figures were not provided in the note.

Barclays is not the only voice signalling caution through derivatives positioning: institutional put exposure against AI stocks reached notable scale in Q1 2026, with former OpenAI researcher Leopold Aschenbrenner disclosing approximately $8.46 billion in notional put exposure against ten semiconductor names and ETFs through a 13F filing, a scale of hedging activity that reflects growing structural scepticism among sophisticated market participants.

Equity-rate hybrid hedges address the second risk Barclays flagged: the scenario where equities fall and bond yields rise at the same time. These instruments are designed to generate returns specifically when both conditions occur simultaneously, providing protection in the correlated-risk environment that traditional balanced portfolios cannot offset.

| Feature | Standard put | Lookback put |

|---|---|---|

| Strike determination | Fixed at time of purchase | Set retrospectively at highest value during option life |

| Timing risk | High: requires accurate entry timing | Low: adjusts to peak automatically |

| Best suited for | Corrections with identifiable catalysts | Environments lacking visible correction triggers |

| Barclays’ preference | Less favoured in current conditions | Preferred for current risk environment |

Neither instrument is widely used by retail investors. Understanding them conceptually, however, equips readers to assess the logic of Barclays’ recommendation and to ask more informed questions of their financial advisers.

The broader picture: what the Barclays note means for portfolio positioning

Pascale’s note is not a sell signal. It is a statement that the risk-reward of holding unhedged long exposure has deteriorated in the near term, even as the medium-to-long-term case for equities remains intact.

Pascale maintains a constructive medium-to-long-term market outlook, framing the hedging recommendation as a tactical risk management adjustment rather than a directional call against equities.

The “no identifiable trigger” observation deserves particular attention. The absence of a visible catalyst does not reduce the probability of a correction; it increases the likelihood that any correction will be abrupt and sentiment-driven rather than gradual and data-driven. That distinction is what makes conventional put structures, which reward precise timing, less effective.

One transparency note: Barclays is the sole verified source for the claims in this article. No comparable commentary from peer institutions was independently verified at time of publication, and specific quantitative targets, VIX levels, and positioning data cited in the note could not be independently confirmed.

A well-timed caution, not a market call to panic

Pascale’s note sits in a specific analytical register: it identifies observable conditions (stretched positioning, rebounding euphoria, rising rate sensitivity), connects them to a practical problem (strike drift in conventional hedges), and recommends instruments designed to address that problem (lookback puts and equity-rate hybrids).

It is not a forecast of a crash. It is not a call to exit the AI trade. It is a risk management signal grounded in positioning data and market structure analysis.

The institutional hedging divergence visible in Barclays’ note reflects a broader pattern that was already observable in late April 2026, when institutional investors were reducing fixed income duration and increasing cash allocations while retail sentiment remained optimistic against a backdrop of elevated valuations and geopolitical risk.

The conditions Barclays identified are dynamic. Readers with unhedged equity exposure may wish to monitor volatility pricing, positioning data, and rate expectations in the weeks ahead as indicators of whether the risk window Barclays described is widening or narrowing.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements referenced in this article are sourced from Barclays’ analyst commentary and are subject to change based on market developments.