How AI Stock Trading Actually Works, and Where It Fails

13 hrs ago

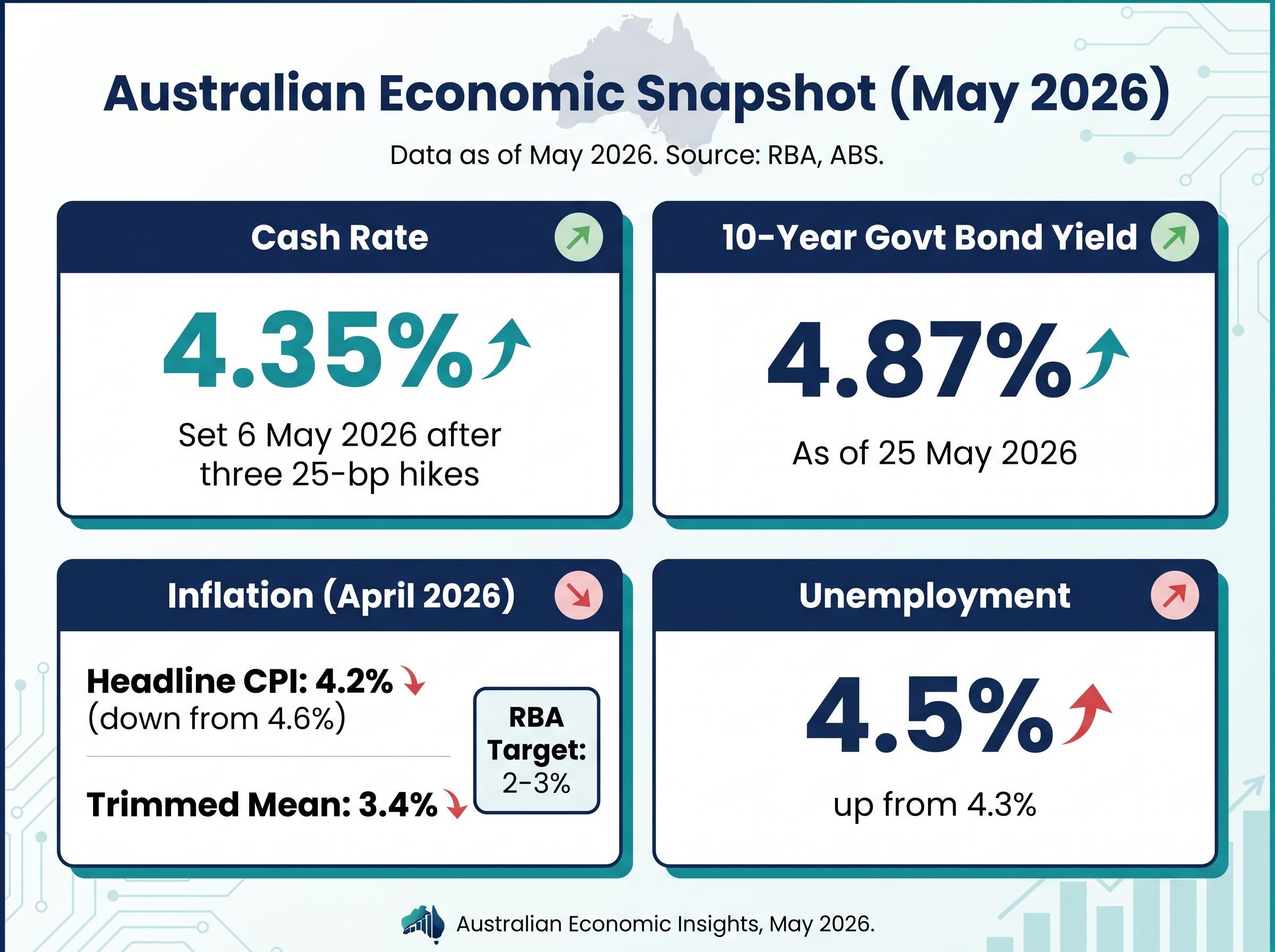

Australian 10-year government bond yields are sitting near 4.87%, a level that would have seemed implausible four years ago when fixed income investors were accepting returns barely above zero. The Reserve Bank of Australia (RBA) has delivered three consecutive 25-basis-point rate hikes in February, March, and May 2026, lifting the cash rate to 4.35%, and a trimmed mean inflation reading of 3.4% in April 2026 signals the Board’s tightening bias has not yet run its course. For investors who spent years treating bonds as a portfolio afterthought, the yield environment has changed in ways that demand active reassessment. This guide covers why current yield levels present a compelling entry point, how duration and instrument type shape the risk-return trade-off in a high-rate environment, and which categories of ASX-listed fixed income ETFs suit different views on the rate cycle ahead.

The numbers tell the story without embellishment. The Australian 10-year government bond yield stood at 4.87% on 25 May 2026, according to Trading Economics, with data from the RBA and FRED confirming levels in the 4.87-4.96% range across late May. That figure sits 0.48 percentage points higher than a year earlier, and worlds apart from the sub-1% levels that prevailed during the pandemic era.

Australian 10-year government bond yield: 4.87% (25 May 2026). This represents one of the most compelling income entry points for Australian fixed income investors in over a decade.

The increase is not the product of a single surprise decision. Three consecutive RBA hikes have repriced the entire yield curve, and the move reflects a structural shift rather than a transient spike. Investors can now access positive real yields, meaning returns that exceed inflation expectations, after years in which holding bonds effectively guaranteed a loss of purchasing power.

Framing this environment as yield normalisation rather than a crisis shifts the analytical lens considerably: the decade of near-zero yields was the historical anomaly, and current levels near 4.87% are broadly consistent with the pre-quantitative-easing era when bonds still served as the portfolio’s income engine.

Three factors underpin the renewed case for fixed income allocation:

For Australian income investors who have relied primarily on dividends or property for yield, these conditions represent a genuine shift. Fixed income is once again a legitimate income source worth active portfolio consideration.

The RBA’s 6 May 2026 decision brought the cash rate to 4.35%, the third 25-basis-point increase in four months. The Board has now entered what amounts to an observation phase, assessing whether the cumulative tightening is sufficient to bring inflation back within the 2-3% target band.

The RBA’s May 2026 decision was not unanimous: eight of nine Board members voted for the hike, with the single dissent signalling that the threshold between hiking and holding is narrower than the headline margin implies, a detail that matters for investors trying to assess how much further the tightening cycle can run.

The data so far offers mixed signals. Trimmed mean inflation held at 3.4% year-on-year in April 2026, still firmly above target. At the same time, unemployment rose to 4.5% from 4.3%, suggesting early softening in the labour market. Neither data point, on its own, justifies an immediate further move. The next meeting is not expected to bring a policy change.

Australian fixed income investors face two plausible paths from here, and each calls for a different positioning.

Commonwealth Bank economists’ base case holds that the cash rate remains at 4.35% for the remainder of 2026. Market pricing, however, leaves a door open: a potential additional hike in September or October 2026 is priced as possible, though far from certain.

The uncertainty itself is the strategic argument. Rather than committing entirely to one view, investors may benefit from holding both floating rate and longer-duration instruments, a point the ETF category discussion that follows will address directly.

| Factor | Hold / eventual cut scenario | One more hike scenario |

|---|---|---|

| Bond prices | Rise as yields fall, favouring longer-duration holders | Further near-term pressure on longer-duration bonds |

| Income stability | Locked-in yields on longer bonds become increasingly attractive | Floating rate income rises with the additional hike |

| ETF type that benefits | Longer-duration government bond ETFs | Floating rate ETFs |

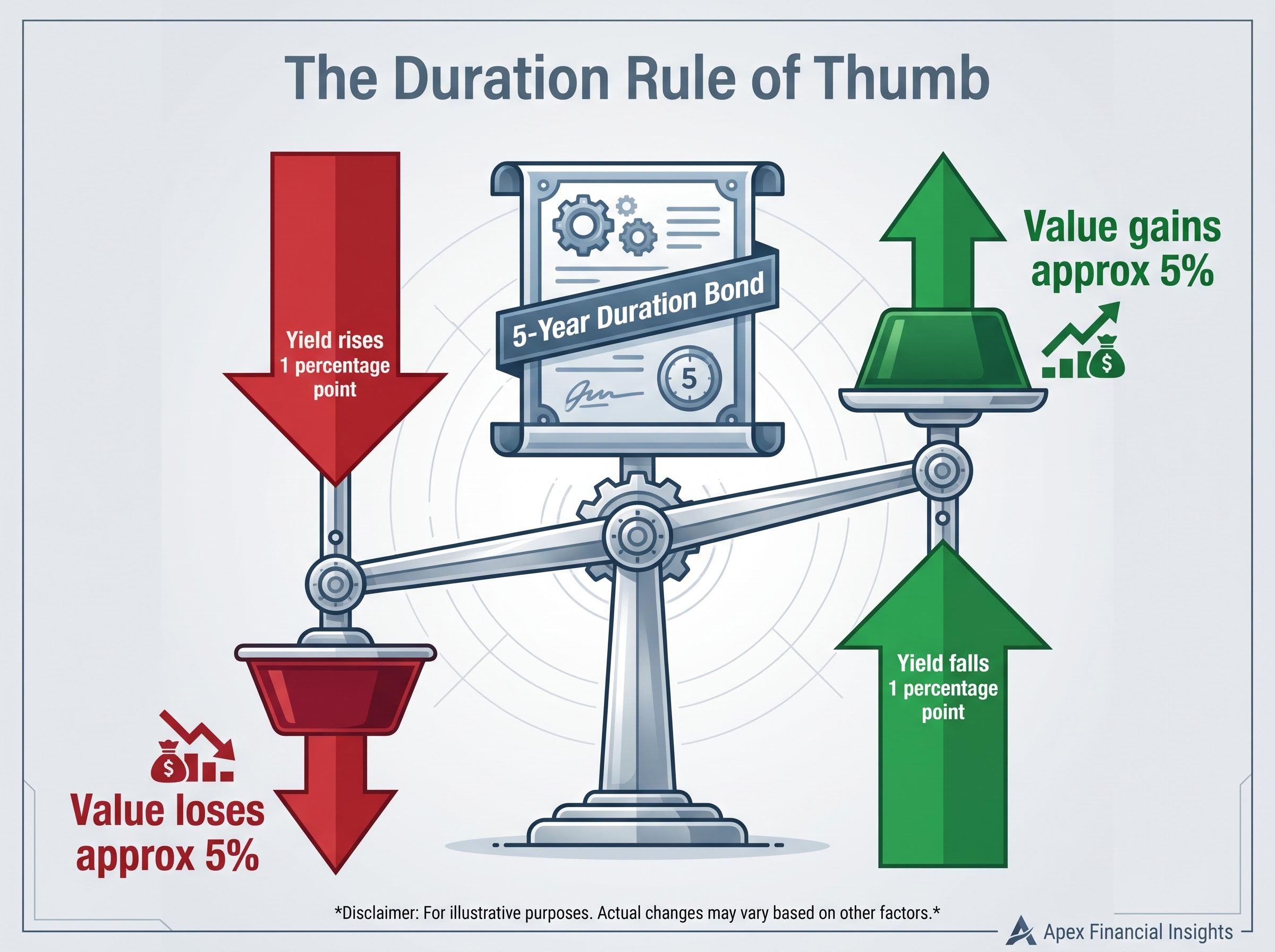

Duration is the single concept that determines how a fixed income holding responds to interest rate changes. In plain terms, it measures a bond’s price sensitivity to yield movements. A rough rule of thumb makes it concrete.

The duration rule of thumb: A bond with five years of duration will lose approximately 5% in value for each one percentage point rise in yields, and gain approximately 5% for each one percentage point fall.

The trade-off follows directly. Shorter-duration instruments protect capital if rates rise further, but they offer less income lock-in and limited capital gain potential if rates eventually fall. Longer-duration instruments carry more price sensitivity in both directions: greater risk if yields rise, greater reward if yields decline.

Four instrument types are relevant for Australian investors evaluating the current environment:

Investors who grasp duration and instrument type can evaluate any fixed income product independently, not just the ETFs discussed in this guide.

The ASX-listed fixed income ETF market spans products from iShares, Vanguard, BetaShares, VanEck, and Global X. Rather than leading with ticker codes, the more useful frame is matching each ETF category to the investor situation it serves.

| ETF category | Suits this investor | Key risk | Key benefit |

|---|---|---|---|

| Floating rate | Believes the cash rate stays elevated; prioritises capital preservation | Income drops quickly once the RBA cuts | Income resets with prevailing rates; minimal duration risk |

| Inflation-linked bonds | Concerned that trimmed mean inflation (currently 3.4%) remains sticky | Underperforms if inflation falls faster than expected | Capital value adjusts with CPI; direct inflation hedge |

| Longer-duration government bonds | Willing to accept near-term price volatility; wants to lock in current yields | Further yield rises erode capital value | Locks in elevated yields; capital gain potential if yields fall |

| Global ESG-screened (AUD-hedged) | Seeks international diversification with sustainability criteria | Foreign credit exposure; hedging cost | Geographic diversification; currency risk removed for AUD investors |

One point warrants emphasis. Specific post-January 2025 distribution yield, management expense ratio, and duration figures for named ETF tickers are not confirmed in current publicly available research. Investors should verify these details directly from fund provider product disclosure statements (PDS) or the ASX Investment Products Monthly Report before making allocation decisions.

The category framework above provides the strategic filter. The next step is matching it to a specific rate view, which is where the guide’s final sections focus.

Investors who want to move directly from category logic to specific fund options will find our dedicated guide to ASX ETFs for Australia’s inflation environment useful; it assesses six ASX-listed funds across income, diversification, and liquidity categories with distribution yields and AUM figures, providing a concrete starting point for comparing products within the categories this article introduces.

The temptation in a high-rate environment is to park capital in floating rate products and high-interest savings accounts, collecting elevated income with minimal risk. That approach works until the cycle turns, and when it does, the repricing is swift.

Waiting for the rate cycle to visibly reverse often means the best entry yields have already passed. Longer-duration bonds begin appreciating in price before the first cut is announced, as markets price the shift in advance.

This asymmetry is the core positioning argument. Floating rate instruments will reprice downward as soon as the RBA signals easing. Longer-duration bonds, by contrast, lock in current yields and gain in capital value as yields fall. The investor who waits for certainty typically captures neither the yield nor the gain.

April 2026 headline CPI came in at 4.2%, down from a prior reading of 4.6%, offering some encouragement that inflation is moderating. The trimmed mean at 3.4%, however, remains outside the 2-3% RBA target band. Commonwealth Bank’s base case holds the cash rate steady for the remainder of 2026, with market pricing pointing to September or October 2026 as the earliest plausible timing for any further adjustment before an eventual easing cycle.

The ABS monthly CPI indicator for April 2026 recorded headline inflation at 4.2% and trimmed mean inflation at 3.4% in the twelve months to April, confirming that underlying price pressures remain above the RBA’s 2-3% target band despite the moderation in the headline figure.

That timeline gives investors room to build positions at current yields rather than rushing a single allocation decision. A practical approach:

These statements are speculative and subject to change based on market developments and RBA policy decisions. Past performance does not guarantee future results.

The combination of 10-year yields near 4.87%, a cash rate at or near its peak, and headline inflation moderating from 4.6% to 4.2% creates conditions where fixing income exposure carries a strong strategic rationale. The window may not remain open indefinitely. Once the RBA signals a shift toward easing, longer-duration yields will compress and the entry point will have passed.

The next steps for investors considering ASX fixed income ETFs are straightforward:

For investors who want the full institutional framework before committing to an allocation, our comprehensive walkthrough of bond portfolio management as rates normalise covers how BlackRock, PIMCO, Vanguard, and J.P. Morgan Asset Management are positioning duration exposure in 2026, with worked comparisons across short, intermediate, and long segments of the yield curve.

The ASX Investment Products Monthly Report publishes fund flow, listing, and asset class data across all exchange-traded products, giving investors a current picture of fixed income ETF market activity and category trends that complements the strategic framework outlined here.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

ASX fixed income ETFs are exchange-traded funds listed on the Australian Securities Exchange that hold bonds or other debt instruments, allowing investors to access diversified bond exposure through a single trade, with income distributed regularly based on the underlying holdings.

Duration measures a bond ETF's price sensitivity to rate movements; as a rule of thumb, a fund with five years of duration will lose approximately 5% in value for each one percentage point rise in yields and gain approximately 5% for each one percentage point fall, making longer-duration ETFs riskier when rates are rising but more rewarding when rates fall.

As of 25 May 2026, the Australian 10-year government bond yield stood at approximately 4.87%, according to Trading Economics, representing one of the highest levels in over a decade and a significant rise from the sub-1% levels seen during the pandemic era.

Investors who believe the RBA is near or at its peak cash rate of 4.35% are better served by longer-duration government bond ETFs, which lock in current elevated yields and appreciate in capital value as yields fall once the easing cycle begins.

A practical approach involves assessing your rate view, choosing duration accordingly, and staggering allocations across floating rate, longer-duration, and inflation-linked ETF categories to hedge against the timing uncertainty that no forecaster can resolve with confidence.