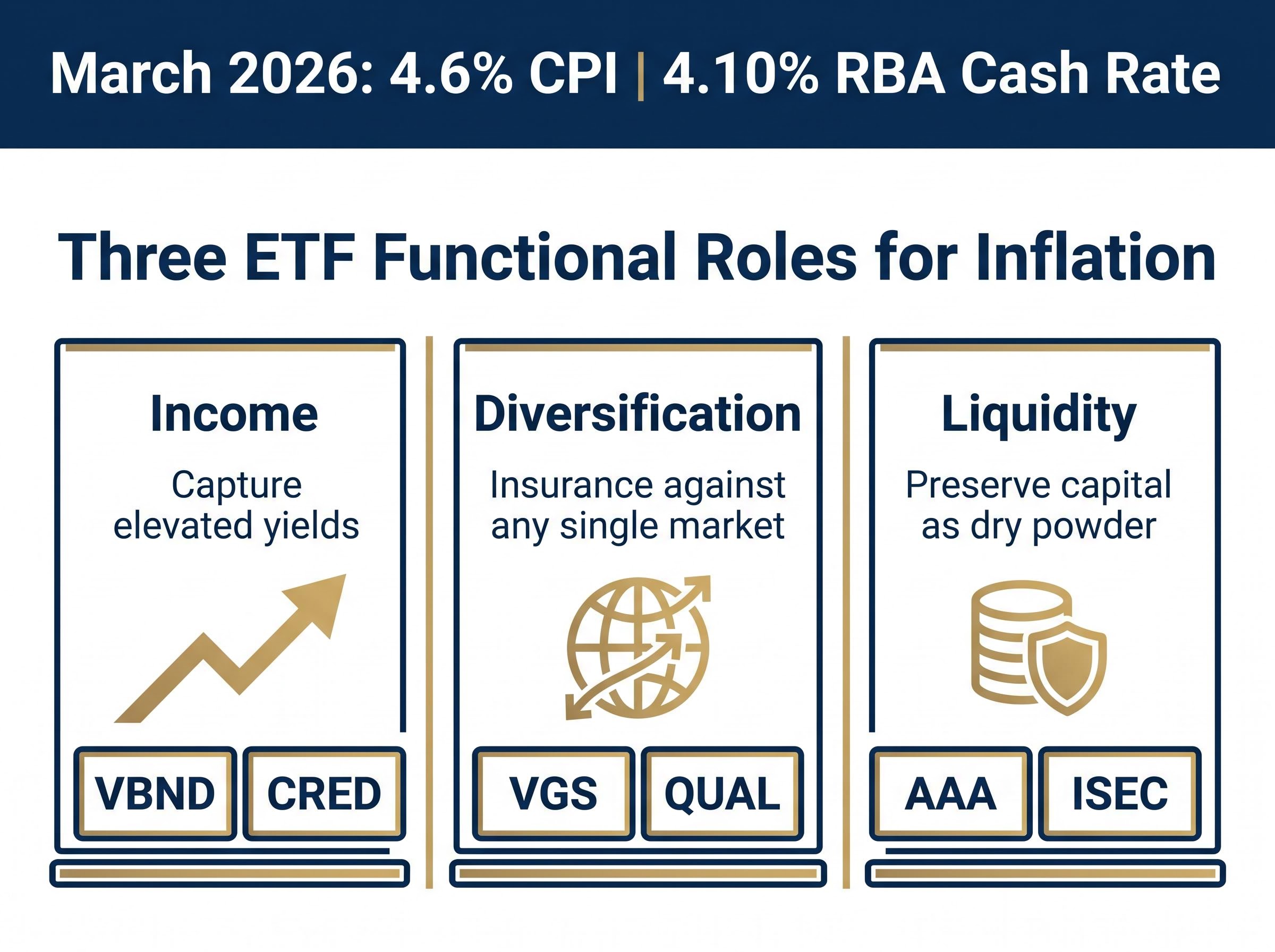

Annual inflation hit 4.6% in March 2026, driven largely by war-related fuel price spikes, and the RBA cash rate is sitting at 4.10%. For Australian retail investors, that combination is not just a headline. It is a live portfolio challenge. Elevated inflation erodes purchasing power, compresses real returns on cash, and creates volatility across equity and bond markets. Knowing which ETF structures tend to hold up, or even benefit, during inflationary periods gives investors a practical edge when selecting the best ETFs for inflation in Australia. This article profiles six ASX-listed ETFs across three categories: income, global diversification, and liquidity. Each fund is assessed for its role in an inflation-aware portfolio, what assets it holds, and why its specific structure matters right now. Readers will finish with a clear picture of six concrete starting points, the metrics for each, and an understanding of how each fits into a portfolio built for resilience when prices are running hot.

Prioritising Investment Themes in an Inflationary Climate

Income, diversification, and liquidity are not arbitrary buckets. They represent three distinct functional roles in a portfolio under inflationary pressure.

- Income ETFs capture elevated yields before rates potentially peak and reverse, locking in returns that may not be available once central banks shift course.

- Diversification ETFs act as insurance against any single market or currency absorbing the hardest hit, spreading exposure across geographies and factor profiles.

- Liquidity ETFs preserve capital and flexibility, holding purchasing power as dry powder for redeployment when better entry points emerge.

With the RBA cash rate at 4.10% and annual CPI at 4.6%, all three roles carry weight simultaneously. Supply-side oil shocks, the type currently driving Australian inflation, have historically produced only brief upward rate pressure before growth concerns shift central bank priorities.

RBA rate cycle timing matters considerably for each of these three categories: the window for locking in elevated bond yields is short if the cash rate peaks and reverses within six to twelve months, as supply-shock historical patterns suggest it may.

“Supply-side oil shocks have historically reversed rate pressure within six to twelve months as growth concerns take over.”

That pattern makes positioning across all three categories more resilient than concentrating in one. What follows is a fund-by-fund assessment across each.

When big ASX news breaks, our subscribers know first

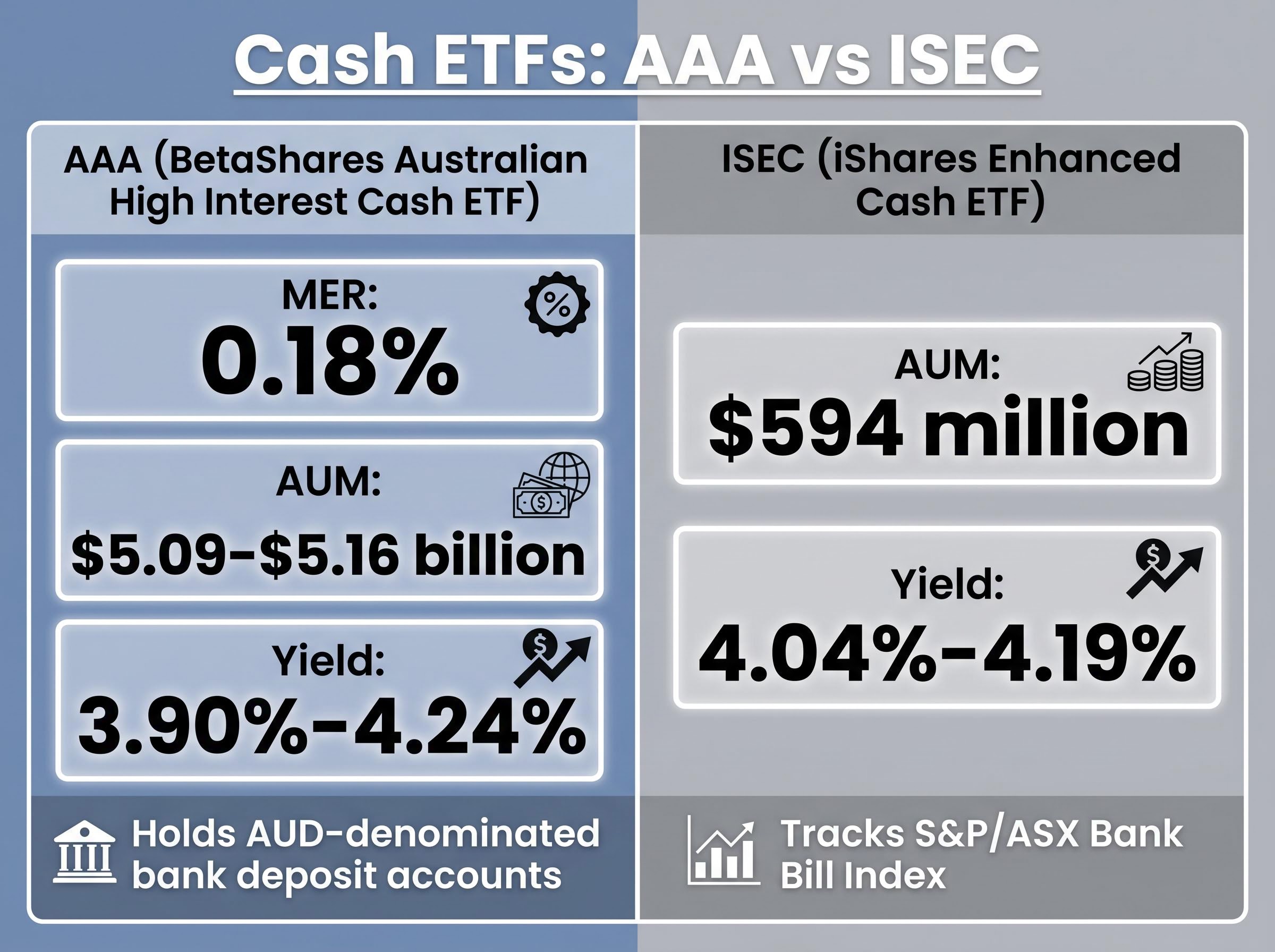

AAA and ISEC: keeping powder dry without surrendering yield

Two ASX-listed cash ETFs offer distinct paths to the same objective: earning a real return on capital held in reserve.

BetaShares Australian High Interest Cash ETF (ASX: AAA) is the simpler option. It invests in AUD-denominated bank deposit accounts and aims for regular income with capital preservation, making it the closest ASX-listed equivalent to a high-interest savings account. iShares Enhanced Cash ETF (ASX: ISEC) takes a step up in complexity. It holds short-duration money market instruments and investment-grade corporate bonds, tracking the S&P/ASX Bank Bill Index, and targets a marginally higher yield for that additional exposure.

The strategic case for both is the same. In an environment where rates may reverse within six to twelve months, a liquidity sleeve preserves capital and earns a return while the investor waits for better entry points in equities or bonds.

| Fund | ASX Code | MER | AUM (approx) | Yield (approx) |

|---|---|---|---|---|

| BetaShares Australian High Interest Cash ETF | AAA | 0.18% | $5.09-$5.16 billion | 3.90%-4.24% |

| iShares Enhanced Cash ETF | ISEC | Verify at blackrock.com/au | $594 million | 4.04%-4.19% |

Both funds allow investors to earn a yield materially above zero on reserves while retaining the ability to redeploy quickly. The distinction comes down to preference:

- AAA suits investors who want maximum simplicity and capital preservation with minimal credit exposure.

- ISEC suits investors comfortable with slightly more complexity in exchange for marginally higher yield potential from short-duration corporate and money market instruments.

VBND: global bond exposure with the currency risk removed

Currency hedging is not a technicality; it is a structural feature that determines whether an Australian investor’s bond returns reflect credit and rate movements or get swamped by foreign exchange volatility. Vanguard Global Aggregate Bond Index (Hedged) ETF (ASX: VBND) removes that distortion. AUD hedging means investors receive the return profile of a globally diversified bond portfolio without the unpredictable drag or windfall of currency movements.

The fund holds a broad mix of investment-grade government and corporate debt from across global developed markets. That breadth makes it a diversified income vehicle rather than a concentrated single-market bet on Australian rates alone.

The timing dimension matters too. When interest rates approach a peak and subsequently fall, bond prices rise. For investors who believe the current rate cycle is near its high, an entry into a fund like VBND positions the portfolio to benefit from that reversal across multiple sovereign and corporate credit markets simultaneously.

| Fund | ASX Code | Category |

|---|---|---|

| Vanguard Global Aggregate Bond Index (Hedged) ETF | VBND | Income |

Current MER, AUM, and yield figures should be verified directly at vanguard.com.au or the ASX product page before making any investment decision, as these were not confirmed in research at the time of publication.

CRED: monthly income from Australian blue-chip borrowers

A 5.2% distribution yield, paid monthly. For income-focused investors, that figure is where the conversation starts.

BetaShares Australian Investment Grade Corporate Bond ETF (ASX: CRED) holds senior fixed-rate bonds issued by high-quality Australian companies. “Investment grade” means these borrowers have been assessed by credit ratings agencies as carrying sufficiently low default risk to warrant the designation, reducing the chance of missed payments compared with higher-yielding but riskier alternatives.

Distribution yield: approximately 5.2% over the trailing twelve months, paid on a monthly basis.

Monthly distributions make CRED practically useful for investors managing regular cash flow needs, whether self-funded retirees drawing living expenses or portfolio builders reinvesting income on a consistent schedule. The positioning becomes particularly relevant when rates are at or near a peak: senior fixed-rate bonds lock in current yields, and if rates subsequently fall, the capital value of those bonds tends to rise.

| Fund | ASX Code | MER | AUM (approx) | Category |

|---|---|---|---|---|

| BetaShares Australian Investment Grade Corporate Bond ETF | CRED | 0.25% | $1.79 billion | Income |

At $1.79 billion in assets under management, CRED represents one of the more accessible fixed-income income streams available on the ASX.

VGS: a single ticket to more than 1,000 global companies

Geographic diversification is not a luxury during inflationary periods. It is structural protection against the specific risk that Australian inflation and rate dynamics diverge from the rest of the developed world.

Vanguard MSCI Index International Shares ETF (ASX: VGS) provides exposure to more than 1,000 large-cap companies across developed markets outside Australia, tracking the MSCI World ex-Australia Index. Different economies move through their rate cycles at different speeds. Holding only Australian assets concentrates the investor in one policy environment; VGS spreads that exposure across North America, Europe, and Asia-Pacific developed markets in a single transaction.

Early 2026 performance has been mixed. The S&P 500 returned approximately 16.4% in 2025 before US technology sector volatility weighed on international equity returns in the opening months of this year. Investors should consider VGS as a long-term core holding rather than a short-term tactical trade.

Index concentration risk is a material consideration for VGS investors: the Magnificent Seven accounted for nearly 33.7% of the S&P 500 by April 2026, meaning a broad international equity fund tracking developed markets carries a de facto large technology sector overweight that broad diversification figures do not immediately reveal.

| Fund | ASX Code | MER | Benchmark | Category |

|---|---|---|---|---|

| Vanguard MSCI Index International Shares ETF | VGS | 0.18% | MSCI World ex-Australia Index | Diversification |

At 0.18% MER, VGS is one of the lower-cost routes to broad international equities on the ASX, making it a practical diversification tool for investors who do not want home-country bias to dominate their inflation-era positioning. Current AUM should be verified at vanguard.com.au.

QUAL: quality-factor equities built to pass cost increases on

Diversification by breadth, the kind VGS provides, is one layer. Diversification by characteristic is another, and in inflationary environments it may be the more targeted one.

VanEck MSCI International Quality ETF (ASX: QUAL) screens for highly profitable global businesses with strong balance sheets, low debt, and demonstrated pricing power. It applies three specific quality-factor filters:

- High profitability (return on equity)

- Low financial leverage (debt-to-equity)

- Stable earnings growth

The pricing power mechanism is concrete. When input costs rise, companies that can pass those increases to customers without losing significant sales volume protect their profit margins. Commodity-exposed or highly indebted businesses typically cannot do this as effectively. The quality factor has historically outperformed in late-cycle environments where credit conditions tighten and weaker companies feel the most pressure.

MSCI research on quality factor performance confirms that quality indexes have historically outperformed the broad market during periods of slower growth and monetary easing, driven by the robust balance sheets and stable earnings that insulate these companies when credit conditions tighten.

| Fund | ASX Code | MER | AUM (approx) | Category |

|---|---|---|---|---|

| VanEck MSCI International Quality ETF | QUAL | 0.40% | $8.04 billion | Diversification |

With $8.04 billion in AUM as of 31 March 2026, QUAL is one of the largest ETFs in the Australian market. Canstar data shows the international quality ETF category delivered approximately 15.48% in one-year returns, reflecting strong investor conviction in the quality factor as a long-term holding during periods when cheap-money growth stories become vulnerable.

What investors need to consider before buying any of these six

Inflation-resilient ETFs do not eliminate risk. Each category carries its own:

- Duration risk (bonds): if rates rise further rather than peaking, bond prices fall, and VBND and CRED would face capital losses.

- Market risk (equities): VGS and QUAL remain fully exposed to global equity drawdowns regardless of their diversification or quality characteristics.

- Reinvestment risk (cash ETFs): if rates fall faster than expected, AAA and ISEC will see their yields compress, reducing forward income.

The three-category framework (income, diversification, liquidity) is a portfolio construction principle, not a recommendation to hold all six simultaneously. The right mix depends on time horizon, risk tolerance, and existing holdings.

Conventional safe haven assets including long-dated government bonds, gold, and the Japanese yen have not performed their traditional defensive role during the 2026 oil shock, because supply-driven stagflation tends to push bonds and equities lower simultaneously rather than inverting their usual correlation.

Dollar cost averaging, regular scheduled purchases aligned with a pay cycle, can reduce the timing risk of entering any of these positions during a volatile environment. Selfwealth by Syfe’s Auto-Invest feature, for instance, supports weekly, fortnightly, or monthly scheduled purchases for any ASX-listed ETF, which aligns with this approach.

“Dollar cost averaging through volatility reduces timing risk and captures more upside when markets eventually recover.”

Actionable ETF Strategies for Inflation

The framework is straightforward. Income ETFs (VBND, CRED) capture elevated yields before rates peak. Diversification ETFs (VGS, QUAL) reduce concentration in any single market or policy environment. Liquidity ETFs (AAA, ISEC) preserve capital and flexibility for redeployment.

Australia’s current inflation environment, 4.6% CPI and a 4.10% cash rate, makes all three roles relevant simultaneously rather than favouring one category over another. If rate pressure follows the historical supply-shock pattern and begins to reverse within six to twelve months, investors who have already positioned across these categories will be better placed to benefit from falling yields boosting bond prices and markets recovering.

An inflation portfolio allocation framework that incorporates alternatives alongside the income, diversification, and liquidity categories covered here, specifically a 20% allocation to physical gold and commodities, addresses a gap the six-ETF structure does not fill: protection against geopolitical tail risks and AUD depreciation that bond and equity positions cannot hedge independently.

Before investing, readers should verify current fund metrics at the issuer websites: vanguard.com.au, betashares.com.au, vaneck.com.au, and blackrock.com/au, as well as the ASX product pages. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.