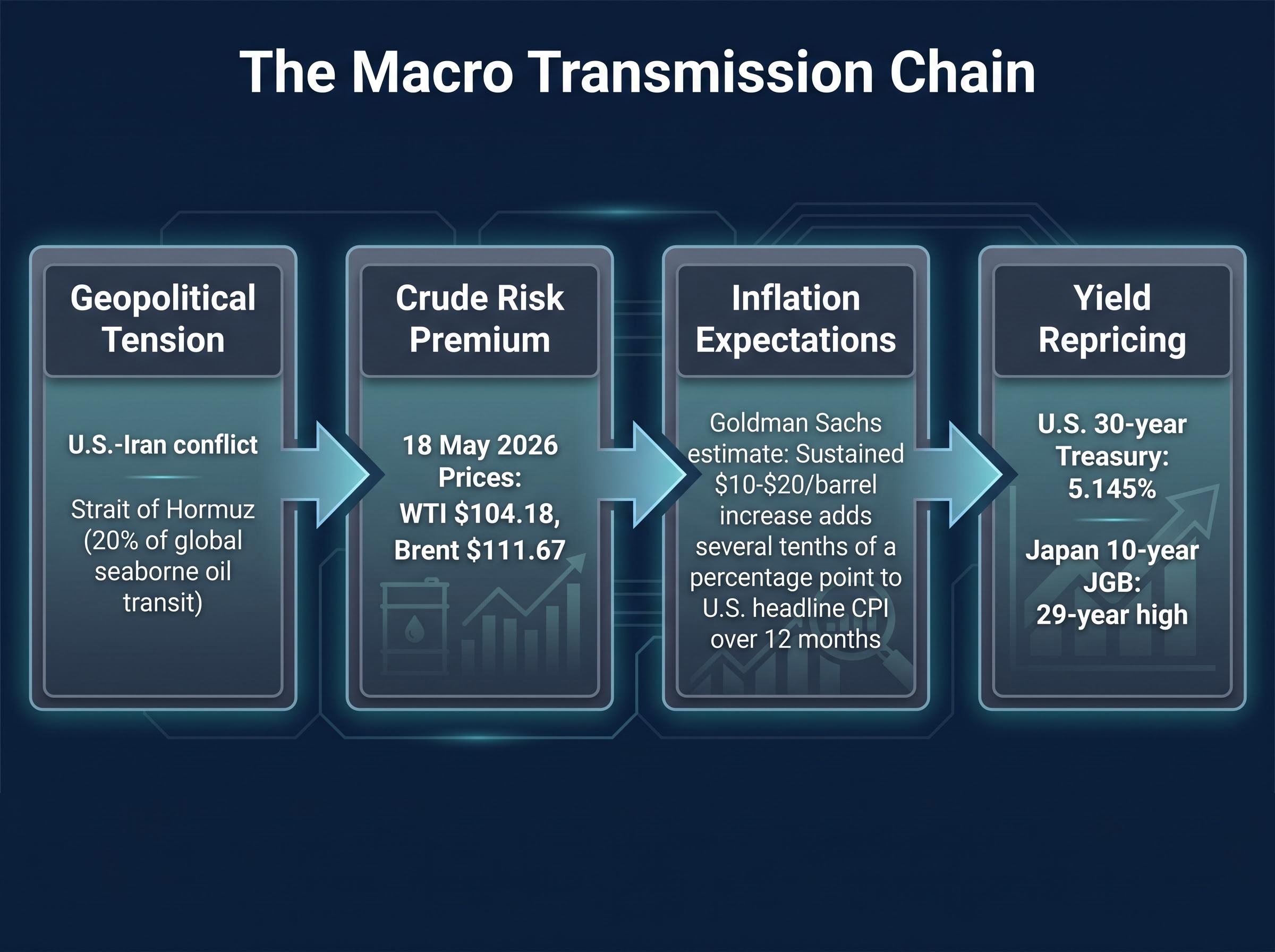

WTI crude topped $104 a barrel on 18 May 2026, Japanese government bond yields hit their highest level in 29 years, and U.S. 30-year Treasury yields sat at 5.145%. Three markets, three continents, one transmission mechanism. The U.S.-Iran conflict has crossed from geopolitical headline into market-moving macro event. Stalled diplomacy, credible military escalation signals from both Washington and Jerusalem, and a Strait of Hormuz that handles roughly 20% of global seaborne oil transit have combined to inject a durable risk premium into energy prices. That premium is now travelling upstream into inflation expectations and central bank rate path calculations in ways that matter for every duration-sensitive portfolio. What follows maps the exact transmission chain from Middle East military tension to crude oil, from crude to inflation expectations, and from inflation expectations to bond yields in the U.S. and Japan. Investors who understand each link can identify which signals to watch for escalation versus de-escalation and position accordingly.

Why $104 oil is not just a supply story

The numbers landed on 18 May 2026 in a cluster:

- WTI futures at $104.18 per barrel, up 3.13% on the session

- Brent futures at $111.67 per barrel, up 2.21%

- Natural gas futures up 2.70% to $3.04

All three moved on the same catalyst: renewed U.S.-Iran escalation rhetoric and a shipping-risk reassessment in the Persian Gulf. But the price itself is not a supply-outage price. No confirmed barrels have been removed from the market. What the market is pricing is a probability, the risk premium layered on top of baseline demand-supply conditions reflecting the chance that barrels could be removed.

That distinction matters because it makes the price reversible.

Bank of America’s CIO team characterises current prices as “geopolitical-risk-driven” and explicitly identifies de-escalation in the Middle East as the mechanism that would pull prices back below recent highs.

If the premium is probability-based rather than loss-based, it can expand or collapse far faster than a fundamental supply rebalancing. The direction depends on diplomacy and military posture, not inventory draws.

When big ASX news breaks, our subscribers know first

The Strait of Hormuz and what physical disruption would actually mean

The Strait of Hormuz is the single largest volume oil transit chokepoint on the planet, according to the U.S. Energy Information Administration’s (EIA) World Oil Transit Chokepoints framework. Roughly 20% of global seaborne crude passes through it. No alternative route offers comparable capacity for Persian Gulf producers.

That concentration is what gives the current risk premium its size. Even without a confirmed blockade, the probability of shipping disruption or sanctions enforcement tightening is enough to keep forward prices elevated and volatility bid.

Iranian exports have been running above the lows seen during earlier, more strictly enforced sanction episodes. Variable enforcement and alternative export channels have allowed volumes to persist. The disruption risk in 2026 is therefore partly about enforcement tightening, not solely about kinetic conflict.

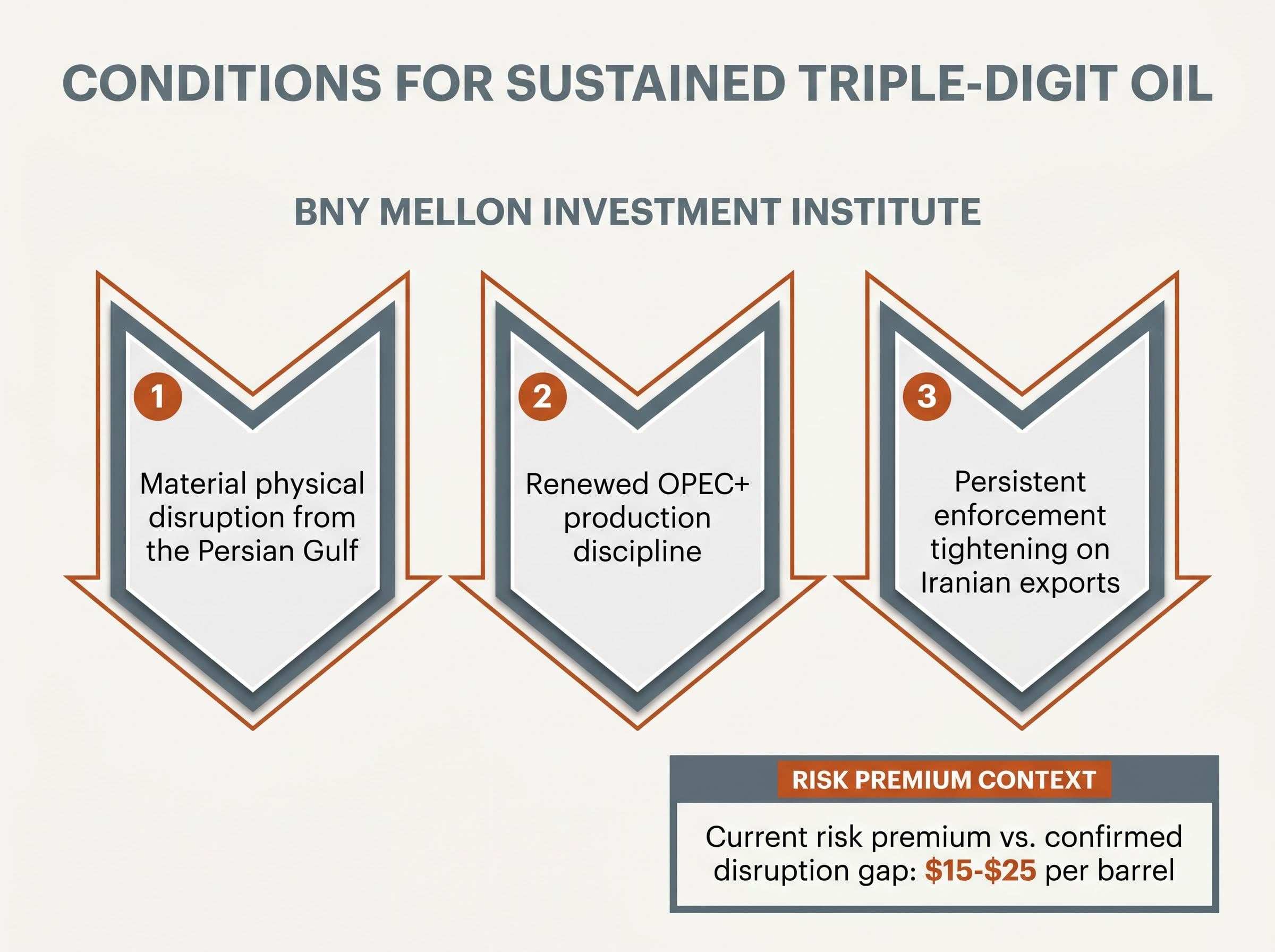

Current risk-premium environment versus a confirmed disruption

The gap between these two scenarios is potentially $15-$25 per barrel. Goldman Sachs treats $100+ crude as tactically plausible but not a durable equilibrium without confirmed export or transport outages, citing U.S. shale responsiveness and non-OPEC supply growth as moderating forces.

BNY Mellon’s Investment Institute identifies three conditions required for sustained triple-digit oil:

- Material physical disruption from the Persian Gulf

- Renewed OPEC+ production discipline

- Persistent enforcement tightening on Iranian exports

Without at least one of those conditions holding, the institute frames current prices as partly transitory. The market is pricing what could happen. A confirmed disruption would reprice what is happening.

How an oil spike becomes a U.S. inflation problem

The mechanical pass-through from crude to consumer prices runs through a well-documented channel. Goldman Sachs economists estimate that a sustained $10-$20 per barrel increase in crude adds several tenths of a percentage point to U.S. headline CPI over 12 months, with smaller effects on core inflation. Headline inflation, which includes food and energy, absorbs the hit directly. Core inflation, which strips those components out, feels it only if energy costs bleed into wages and services.

| Crude price move | Estimated CPI impact | Timeframe | Core vs headline |

|---|---|---|---|

| +$10/barrel sustained | Several tenths of a percentage point | 12 months | Headline primarily; modest core pass-through |

| +$20/barrel sustained | Larger headline effect; core dependent on wage dynamics | 12 months | Headline significant; core conditional on expectations |

BNY Mellon characterises energy-driven bumps as “temporary” to headline CPI while core disinflation continues. But the institute notes that consumer-facing gasoline prices can move inflation expectations in ways that complicate Federal Reserve messaging.

Corporate margin absorption is acting as a temporary buffer between upstream energy costs and consumer prices: companies including Procter and Gamble, Nike, and Hasbro are compressing gross margins by approximately 150 basis points rather than raising shelf prices, a dynamic that contains measured CPI but shifts the inflation risk from a broad goods breakout into a sector-specific earnings compression story for consumer discretionary equities.

That second-order effect is where the real policy risk sits. The CPI print matters; the expectations channel matters more.

The Federal Open Market Committee’s (FOMC) Summary of Economic Projections identifies “geopolitical events” and “potential increases in energy prices” as upside inflation risks, placing the oil-to-inflation channel squarely within the Fed’s stated risk framework.

The FOMC Summary of Economic Projections from March 2026 notes that potential effects of Middle East developments represent a salient upside inflation risk, with officials explicitly flagging the possibility that inflation could prove more persistent than baseline staff projections if energy costs re-accelerate.

What the Fed, ECB, and Bank of Japan are actually saying

Each of the three major central banks has addressed energy-driven inflation risk explicitly. Their language differs; their architecture does not.

The Federal Reserve treats energy-driven inflation as a supply-side shock it would “look through” if inflation expectations remain anchored. FOMC statements and speeches from officials have stated that a renewed oil-price shock linked to Middle East tensions could slow disinflation and delay rate cuts, but only if it feeds into broader wage-price dynamics.

Fed rate-cut odds collapsed from 45% to 12% for the June meeting in the weeks following the Hormuz closure, with Barclays and JPMorgan both cutting their full-year 2026 cut forecasts to approximately 50 basis points from 100 basis points, a repricing that illustrates how an energy supply shock can mechanically alter the rate path without the central bank explicitly acknowledging it.

The European Central Bank (ECB) is more direct in its references. President Christine Lagarde has noted in multiple press conferences that “geopolitical tensions, particularly in the Middle East,” can generate renewed energy price volatility pushing headline inflation higher in the near term. The Governing Council’s risk assessment warns that “a further escalation of the conflict in the Middle East” could raise energy prices and slow the decline in inflation.

The Bank of Japan (BoJ) identifies “developments in international commodity prices, including crude oil, amid geopolitical risks” as an upside risk to Japan’s inflation outlook. With 10-year JGB yields at multi-decade highs, officials caution that a new surge in imported energy costs could temporarily lift CPI, but policy focus remains on whether those costs translate into wage-price dynamics.

| Central bank | Current posture on energy shocks | Condition for changing stance | Key communication reference |

|---|---|---|---|

| Federal Reserve | Look through transitory spike | De-anchoring of inflation expectations; wage-price spillover | FOMC Summary of Economic Projections; official speeches |

| ECB | Acknowledge near-term headline risk; hold easing path | Sustained energy shock slowing underlying disinflation | Lagarde press conferences; Governing Council accounts |

| Bank of Japan | Monitor imported cost pass-through | Energy costs feeding into wage-price dynamics | BoJ Outlook for Economic Activity and Prices |

The shared condition all three banks are watching

The common thread is conditional permissiveness. All three tolerate a transitory energy spike but shift stance if it feeds into wages, core inflation, or de-anchored longer-run expectations.

The asymmetry in this framework is worth noting. Escalation that breaks the condition triggers tightening signals across all three economies. De-escalation that removes the energy risk premium does not immediately trigger cuts, because the premium was “looked through” rather than priced into the rate path. The upside risk is priced; the downside relief is not symmetrically available.

Bond markets from Washington to Tokyo: reading the yield surge

The yield data from 17-18 May 2026 tells a story that extends beyond any single domestic driver.

| Market | Instrument | Yield level | Notable context |

|---|---|---|---|

| United States | 10-year Treasury | 4.626% | One-month peak |

| United States | 30-year Treasury | 5.145% | Reflecting fiscal and geopolitical term premium |

| United States | 5-year Treasury | 4.287% | Curve steepening signal |

| United States | 10-2 year spread | 31.32 bps | Widened 15.27% |

| Japan | 10-year JGB | 29-year high | BoJ normalisation plus global term premium |

The U.S. long end reflects both fiscal premium and the geopolitical-risk component of term premia. Goldman Sachs notes that an energy-driven inflation scare can push nominal long yields higher even if real yields are constrained by safe-haven demand.

Goldman Sachs highlights the asymmetry: if conflict escalates into a growth-negative shock, safe-haven flows could eventually dominate and pull long yields lower. But in the current phase, where conflict raises inflation without yet destroying growth, nominal yields move higher.

The JGB move to 29-year highs sits at the intersection of two reinforcing forces. The BoJ’s own policy normalisation is lifting domestic yields, while global term-premium repricing, transmitted through investor allocations and foreign exchange expectations, adds an external layer. JPMorgan’s mid-year 2026 outlook notes that global geopolitical uncertainty has elevated the term premium component across major bond markets, with Japan particularly sensitive because the domestic and global drivers are reinforcing rather than offsetting each other.

For investors with fixed income exposure, the simultaneous repricing in Washington and Tokyo signals that geopolitical risk is functioning as a global term-premium driver, not a localised one. Diversification assumptions built on uncorrelated duration exposure between U.S. and Japanese bonds deserve reassessment.

The signals that will tell you whether this is a regime shift or a spike

The difference between a reversible risk premium and a structural supply shock will be visible in three escalation signals, ordered by proximity to physical supply impact:

- Strait of Hormuz shipping data: Tanker transit volumes and insurance premium movements are the earliest indicator of whether disruption probability is increasing toward realisation.

- Iranian export volume tracking: A sustained decline in Iranian crude exports below recent averages would confirm enforcement tightening or physical obstruction, moving the market from probability pricing to disruption pricing.

- Formal central bank language upgrades: If the FOMC, ECB, or BoJ shifts from “acknowledge the risk” to “incorporating energy shock into baseline projections,” the rate path repricing accelerates.

De-escalation indicators and the path back below $100

The reversal mechanism runs through a parallel set of signals:

- Confirmed diplomatic progress between the U.S. and Iran, visible in formal readouts rather than background reporting, would compress the risk premium directly.

- Reduction in U.S. or Israeli military posture signals, such as force repositioning or public de-escalation language from senior officials, would lower the probability weighting on disruption scenarios.

- Oil returning below $95 on volume would confirm that the market is repricing the premium rather than simply experiencing a short-covering rally.

Goldman Sachs notes that even with de-escalation, non-recessionary growth and persistent demand support a non-trivial baseline oil price. The floor is not pre-conflict lows. BNY Mellon’s three conditions for sustained triple-digit oil provide the framework: remove the conditions, and the premium fades; the underlying demand environment does not.

A Wolfe Research yield decomposition of the 40-basis-point surge in the 10-year Treasury since the conflict began attributes only 19 basis points to the geopolitical shock itself, with the remaining 21 basis points driven by growth repricing and structural fiscal factors that will not reverse under a peace agreement, setting a hard ceiling on how far yields can fall even in the most optimistic diplomatic scenario.

A conflict priced in but not resolved: what this means for U.S. portfolios now

The current environment presents an asymmetric setup. Geopolitical risk is priced into energy, inflation expectations, and bond yields, but the underlying condition generating that premium remains active and unresolved.

Escalation triggers further repricing across all three channels. De-escalation removes the premium but does not immediately open the door to Fed cuts, because the “look through” posture means cuts were never explicitly linked to the premium in the first place. The relief trade is real; the policy easing trade is conditional on separate variables.

The gold market corroborates this reading. Spot gold fell 1.3% to $4,483.67 per ounce on 17 May, with futures down 1.7% to $4,484.82 and silver futures declining 4.18% to $74.305 on 18 May. Higher yields are compressing the opportunity cost of holding non-yielding assets, and the traditional safe-haven bid is being suppressed by the yield channel rather than replaced by risk appetite.

Currency market repricing adds a fourth transmission channel that the bond and energy markets do not fully capture: the energy shock has restructured how foreign exchange markets value national currencies, with exporters strengthening relative to importers as energy trade flows displace conventional macro drivers of exchange rate determination.

The FDIC’s 2025 Risk Review documents that rising longer-term rates are generating mark-to-market losses on bank securities portfolios, illustrating how the yield repricing transmits from sovereign bond markets into the real economy.

The FDIC 2026 Risk Review documents how changes in longer-term interest rates generate mark-to-market losses on bank securities portfolios, quantifying the channel through which sovereign yield repricing flows directly into the balance sheets of deposit-taking institutions and into broader credit conditions.

The portfolio-level implications reduce to three variables:

- Duration is the most exposed asset class characteristic; simultaneous global yield repricing means long-dated fixed income carries both domestic and geopolitical term-premium risk.

- Energy exposure remains a hedge against further escalation, with the premium reversible but the underlying demand case intact.

- Gold faces opportunity cost compression in a higher-yield environment, reducing its effectiveness as a portfolio hedge until either yields retreat or conflict escalates sharply enough to overwhelm the yield disadvantage.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding energy prices, inflation, and central bank policy are speculative and subject to change based on market developments and geopolitical conditions.

The transmission chain is clear. The endpoint is not.

Regional military tension to crude risk premium to inflation expectations to bond yield repricing: all four links in that chain are active simultaneously as of mid-May 2026. No formal supply disruption has materialised. Diplomatic channels are stalled but not closed. All three central banks are holding conditional “look through” postures that could shift if the condition breaks.

The uncertainty is genuine, but it is not formless. The indicators that will resolve it are specific and watchable: Strait of Hormuz shipping data, Iranian export volumes, and central bank language upgrades on energy risk. Those three signals will determine whether this conflict transitions from a priced risk to a realised macro shock. Until they move, the premium persists, and portfolios built on pre-conflict assumptions carry exposure they may not have measured.