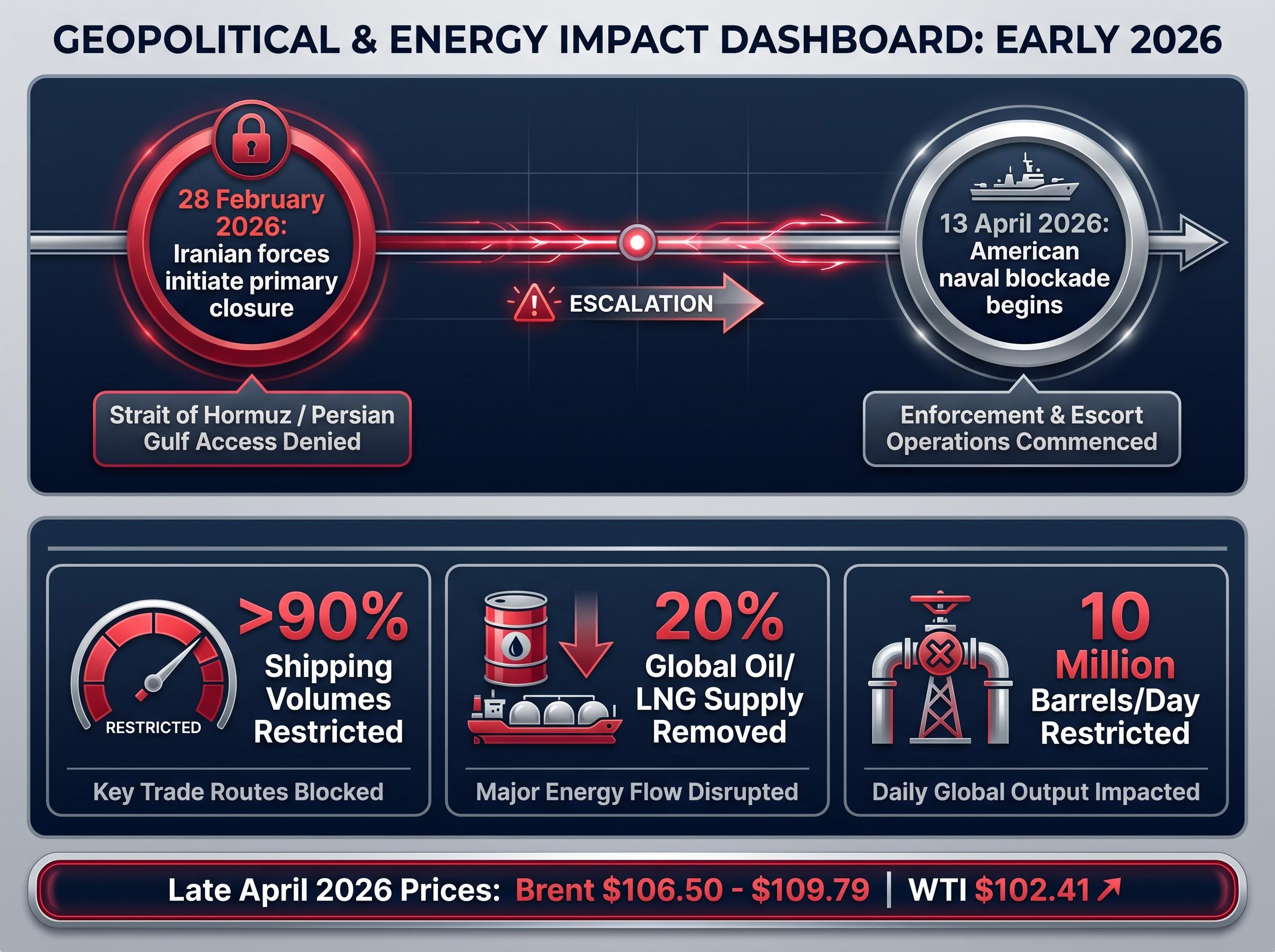

Over 10 million barrels of petroleum per day have vanished from global markets since late February 2026. This sudden supply contraction stems from a dual naval blockade of the Strait of Hormuz involving both Iranian and American military forces. The resulting global energy crisis has triggered cascading effects across international financial systems, disrupting historical market correlations and forcing a complete reassessment of macroeconomic risk.

The sheer scale of this disruption extends far beyond localised geopolitical tension, permeating every layer of the international economy. Foreign exchange markets, fixed-income yields, and commodity pricing models are all recalibrating to reflect a prolonged structural deficit. Physical energy constraints are currently driving currency valuations, complicating central bank policy, and rewriting the fundamental rules of defensive investing.

The Mathematics of a Global Supply Shock

The geopolitical headlines capture the military tension, but the financial reality is dictated entirely by cold mathematics. The Strait of Hormuz functions as the primary maritime artery that establishes the baseline pricing for the entire global energy complex. When physical flow through this chokepoint stops, markets must instantly reprice the global cost of production, transport, and manufacturing.

The current dual blockade evolved in two distinct phases that severely shocked energy markets. Iranian forces initiated the primary closure on 28 February 2026, followed by an American naval blockade of Iranian ports beginning on 13 April 2026. This combined military action has restricted shipping volumes by more than 90%, effectively removing 20% of total global oil and liquefied natural gas supply from the market.

The EIA transit chokepoints data confirms that prior to the disruption, over 20.9 million barrels per day flowed through this specific maritime route, validating why the current restriction is impacting physical markets so severely.

This sudden contraction translates to approximately 10 million barrels per day of restricted physical output. A supply reduction of this magnitude alters the global inflation outlook by creating immediate, structural energy deficits that cannot be resolved through strategic reserves. As of late April 2026, Brent crude is trading between $106.50 and $109.79 per barrel, with West Texas Intermediate (WTI) crude holding at $102.41.

| Commodity | Pre-Crisis Status | Disruption Percentage | Current Price Level |

|---|---|---|---|

| Brent Crude | Normal baseline flow | 20% of global supply | $106.50 to $109.79 |

| WTI Crude | Normal baseline flow | Indirect correlation | $102.41 |

| Liquefied Natural Gas | Normal baseline flow | 20% of global supply | Elevated premiums |

When big ASX news breaks, our subscribers know first

Evaluating Currency Strength Through Commodity Export Capacity

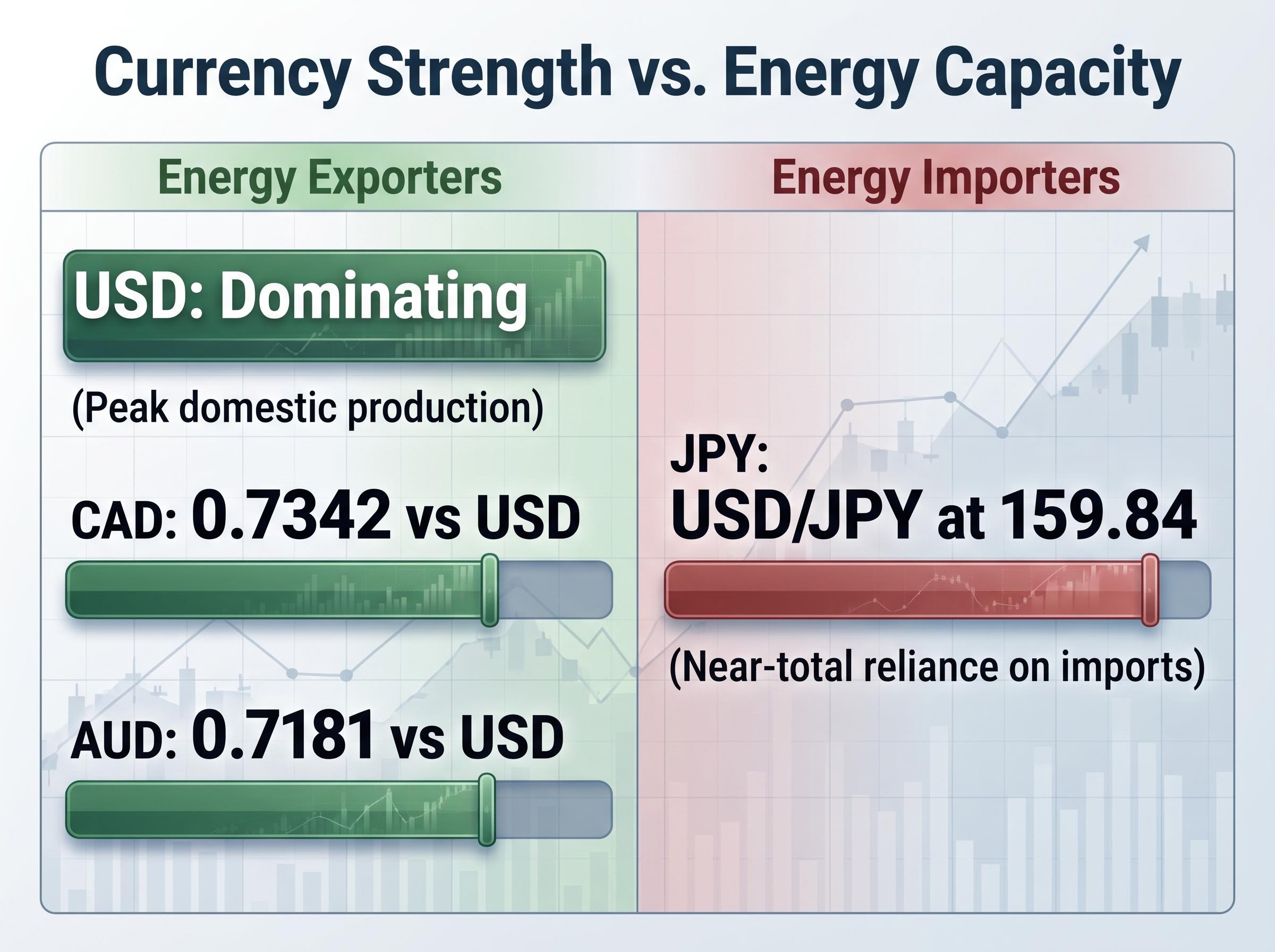

Foreign exchange markets have largely abandoned their traditional safe-haven assumptions in response to this structural supply shock. A new paradigm has emerged where a nation’s energy export capacity strictly dictates its monetary strength. Investors are currently evaluating currency resilience through the single lens of whether a country imports or exports its baseline petroleum requirements.

This shift is most evident in the historically weak performance of the Japanese yen during the current crisis. Japan relies heavily on imported energy, and the severe pressure on energy-reliant currencies has pushed the USD/JPY exchange rate toward 160, trading at approximately 159.84 as of late April 2026. Conversely, the US dollar has maintained significant strength due to substantial domestic energy production capabilities offsetting the broader geopolitical fear.

The BIS commodity price research explains that the transition of the United States into a net energy exporter fundamentally shifted its currency behaviour, allowing it to appreciate rather than depreciate during global energy supply disruptions.

Market data reveals that currencies backed by commodity export capacity are absorbing the shock far more effectively.

- United States Dollar (USD): Dominating foreign exchange markets due to peak domestic energy production combined with structurally high interest rates.

- Canadian Dollar (CAD): Demonstrating distinct resilience as a primary energy exporter, trading steadily at 0.7342 against the USD despite broader market volatility.

- Australian Dollar (AUD): Maintaining stability through significant liquefied natural gas and resource exports, holding at 0.7181 against the USD.

- Japanese Yen (JPY): Suffering severe depreciation due to near-total reliance on imported petroleum and natural gas to fuel its industrial base.

There are isolated exceptions to this commodity-driven hierarchy that require careful analysis. The Hungarian forint emerged as the strongest currency during the mid-April market shock, an anomaly driven entirely by local political developments following recent elections rather than structural macro factors.

Monetary Policy Constraints Amid Persistent Inflation

Global policymakers find themselves trapped between the inflationary force of surging petroleum prices and the reality of rapidly slowing economic growth. The petroleum supply shock complicates monetary policy by directly feeding into core inflation metrics, effectively eliminating the possibility of previously anticipated rate cuts. Central banks are telegraphing a clear necessity to prioritise inflation control over economic expansion, despite the restrictive impact on global growth trajectories.

Market expectations have firmly recalibrated to this prolonged restrictive environment across all major economies.

The Federal Reserve is widely expected to hold interest rates steady at 3.5% to 3.75% during its late April policy meetings, prioritising inflation containment. The European Central Bank is maintaining its unchanged rate stance, an outcome markets are pricing with a 99% probability given ongoing energy vulnerabilities. The Bank of Japan is keeping baseline rates constant despite severe currency depreciation pressures, trapped by slow domestic growth. The Bank of England has paused all monetary easing discussions while assessing the secondary inflation impacts of the global supply shock.

For readers wanting to understand how long these restrictive central bank policies might last, our full explainer on projected Fed interest rate timelines examines the specific inflation metrics and geopolitical triggers that are expected to keep borrowing costs elevated into 2027.

The Yield Curve and Government Debt Pressures

This prolonged central bank gridlock places immense pressure on fixed-income markets globally. Short-term government debt yields are increasing as traders anticipate hawkish monetary policy persisting well into the third quarter of the year. The 10-year US Treasury yield currently stands at 4.36%, reflecting this recalibrated expectation for higher baseline borrowing costs across the economy.

Simultaneously, long-term debt instruments are suffering notable valuation declines as risk models are rewritten. Investors demand greater compensation for the heightened risk of extended government borrowing in a structurally inflationary environment. This dynamic forces a fundamental repricing of fixed-income portfolios across international markets, eliminating traditional bond market protections.

Dismantling the Precious Metals Myth

Historical market paradigms suggest that gold should surge during a severe geopolitical conflict, yet current trading data dismantles this conventional expectation. Bullion is failing to act as a definitive safe-haven asset, reacting instead as a standard industrial commodity under severe macroeconomic pressure. Understanding this anomaly requires looking beyond the geopolitical headlines to the underlying structural forces driving the current bullion sell-off.

The overwhelming strength of the US dollar and elevated central bank interest rates make zero-yield assets fundamentally unappealing to institutional investors. When government debt offers risk-free yields above 4%, the opportunity cost of holding physical gold becomes increasingly difficult to justify in sophisticated institutional portfolios. This structural headwind is compounding the effect of broad market margin calls, which compel leveraged investors to liquidate their bullion holdings to cover equity shortfalls.

However, sovereign wealth funds and monetary authorities are taking a distinctly different approach, and record central bank gold accumulation continues to establish a formidable pricing floor as nations systemically repatriate physical bullion to hedge against western financial sanctions.

Market Dynamics Commentary The combination of sustained high interest rates and absolute US dollar dominance is currently overriding all traditional geopolitical fear premiums in the bullion market.

These compounding macroeconomic pressures have forced gold prices down from earlier highs of $4,706 to a spot price of $4,599.80 per ounce by late April 2026. This sharp decline must be contextualised against the substantial valuation increase bullion experienced during the prior two years of trading. Investors who allocate capital based on outdated assumptions about wartime gold behaviour risk significant misallocation in this high-yield environment.

Managing Volatility and Positioning for Market Resolution

The macroeconomic complexity of this dual blockade requires investors to synthesise the impacts of physical energy shortages, fundamental currency shifts, and central bank gridlock. A prolonged restriction of 20% of global energy supply demands a portfolio approach that prioritises capital preservation over aggressive growth mandates. Maintaining adequate liquidity while systematically acquiring diversified, cash-generative assets offers a mathematical advantage while weathering the duration of the Hormuz blockade.

Strategic portfolio managers are implementing targeted consumer sector rotation strategies, moving capital away from fuel-intensive businesses that face immediate profitability threats and into discount retail chains that historically capture market share when household budgets tighten.

Historical comparisons to the 1970s oil embargoes and the 2022 market shocks provide critical context for eventual market recovery patterns. Financial markets frequently show a pronounced capacity to recover once conflict resolution appears even remotely possible, often rallying significantly before official treaties are ever signed. Investors who position themselves defensively now will be best equipped to capture value during that eventual normalisation phase.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to rapidly changing geopolitical conditions and market risk factors.