The Memo That Halved Meta’s AI Infrastructure Cost Estimate

7 hrs ago

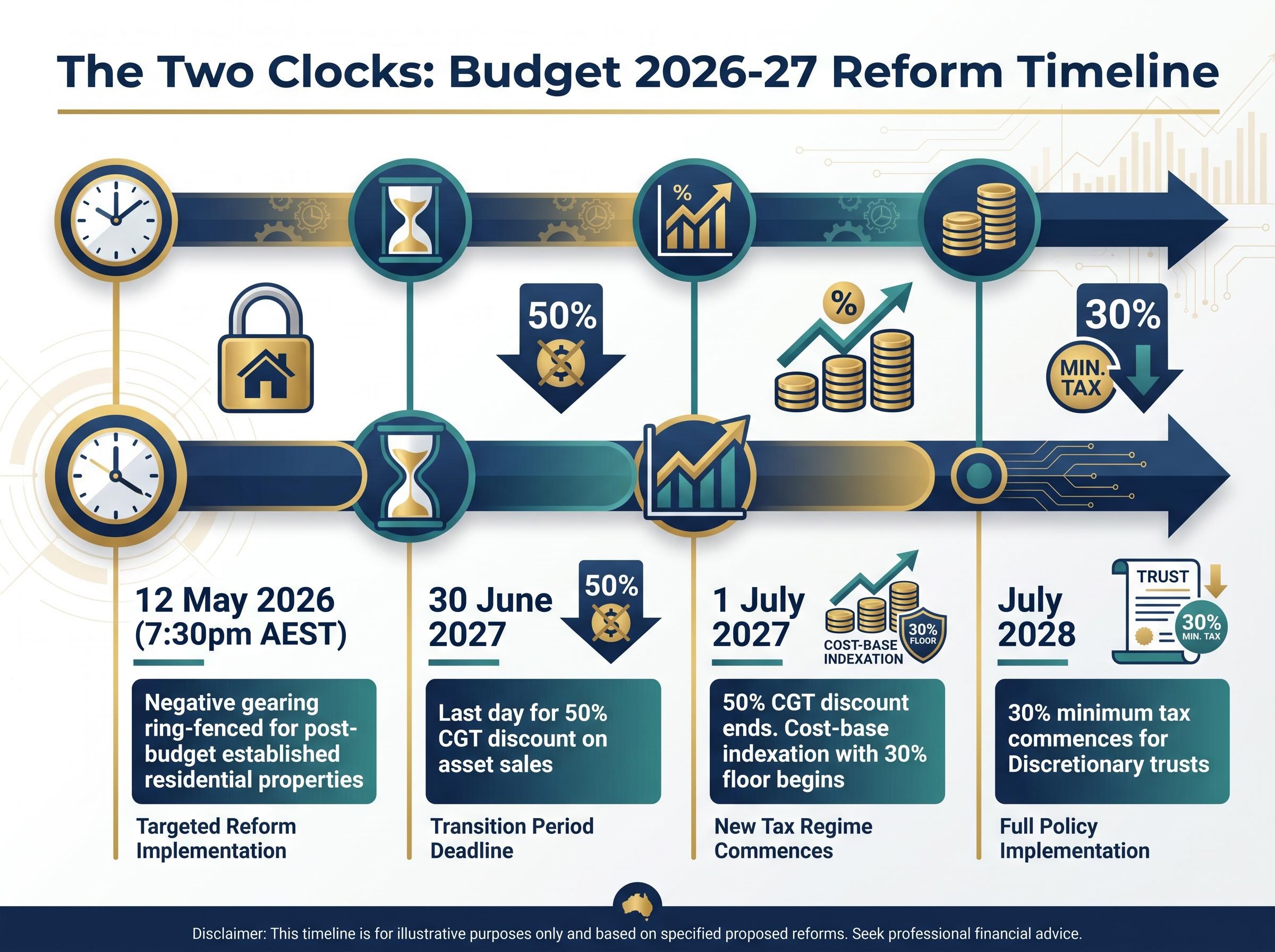

A single Budget night rewrote the rules that Australian property investors had relied on for 27 years. On 12 May 2026, the Federal Government announced the removal of the 50% capital gains tax (CGT) discount, the introduction of cost-base indexation with a 30% minimum tax floor, and the immediate ring-fencing of negative gearing to new builds only. These are not variations on one theme. They are three separate mechanisms, operating on two different timelines, that together dismantle the after-tax return architecture underpinning Australian residential property investment since 1999. What follows is an analysis of what each measure changes, who faces immediate consequences versus those with a planning window through to 1 July 2027, how different ownership structures interact with the new rules, and where capital is likely to flow once the transition is complete.

The reforms announced in Budget Paper No. 1, 2026-27 contain three distinct policy mechanisms. Each operates on its own timeline and affects a different dimension of the investment decision:

The Budget Paper No. 1, 2026-27 tax reform measures confirm all three mechanisms in a single policy document, establishing the legislative basis for the negative gearing ring-fencing, the 50% CGT discount removal, and the cost-base indexation regime with the 30% minimum floor.

The table below maps each measure against its effective date, the assets it targets, and whether grandfathering applies.

| Measure | What changes | Effective date | Assets affected | Grandfathering |

|---|---|---|---|---|

| Negative gearing ring-fencing | Losses on established residential property no longer deductible against other income | 12 May 2026 (7:30pm AEST) | Established residential (post-Budget purchases) | Yes, properties held before Budget night |

| 50% CGT discount removal | Discount abolished for disposals after commencement date | 1 July 2027 | All CGT-eligible assets disposed post-date | No, applies to all disposals after 1 July 2027 |

| Cost-base indexation with 30% floor | Cost base adjusted for inflation; 30% minimum tax on net capital gains | 1 July 2027 | All CGT-eligible assets disposed post-date | No |

Investors cannot plan their response without first identifying which rule applies to each asset in their portfolio, and when. The two-clock structure, one already ticking since Budget night, the other commencing 1 July 2027, means the sequencing of decisions matters as much as the decisions themselves.

The Budget night announcement represents the biggest tax overhaul since 1999, when the Howard government introduced the 50% CGT discount that these reforms now dismantle, compressing nearly three decades of investor behaviour into a single policy reversal.

Under the existing regime, an investor who holds an asset for more than 12 months and sells at a gain simply halves the gain and pays tax at their marginal rate on the reduced amount. The calculation is predictable: regardless of how long the asset is held or how much of the gain reflects inflation, the discount is always 50%.

Cost-base indexation works differently. Instead of halving the gain, the system adjusts the original purchase price upward in line with inflation (using the Consumer Price Index). The investor then pays tax on the difference between the sale price and the indexed cost base, meaning only the real gain above inflation is taxed.

For a property purchased at $500,000 and sold at $900,000 after significant holding, the outcomes diverge:

The variable outcome under indexation, determined by how long the asset is held and what inflation does over that period, means there is no single answer to whether the new system is better or worse for a given investor. It depends on the specific numbers.

A related but distinct consequence of the 1 July 2027 commencement date is the end of the pre-1985 CGT exemption: assets held since before that year, which have historically been fully exempt from capital gains tax, will from that date have their gains measured against a deemed cost base equal to market value at 1 July 2027, creating significant valuation risk for holders of long-held family properties and rural assets.

These figures are simplified for illustration and do not constitute financial advice. Individual outcomes depend on holding period, inflation, and marginal tax rate.

The 30% minimum tax floor is where the mechanics shift from variable to constrained. Even where cost-base indexation would produce an effective tax rate below 30% on net capital gains, the floor overrides the calculation. The investor pays the higher of their indexed tax liability or 30% of the net gain.

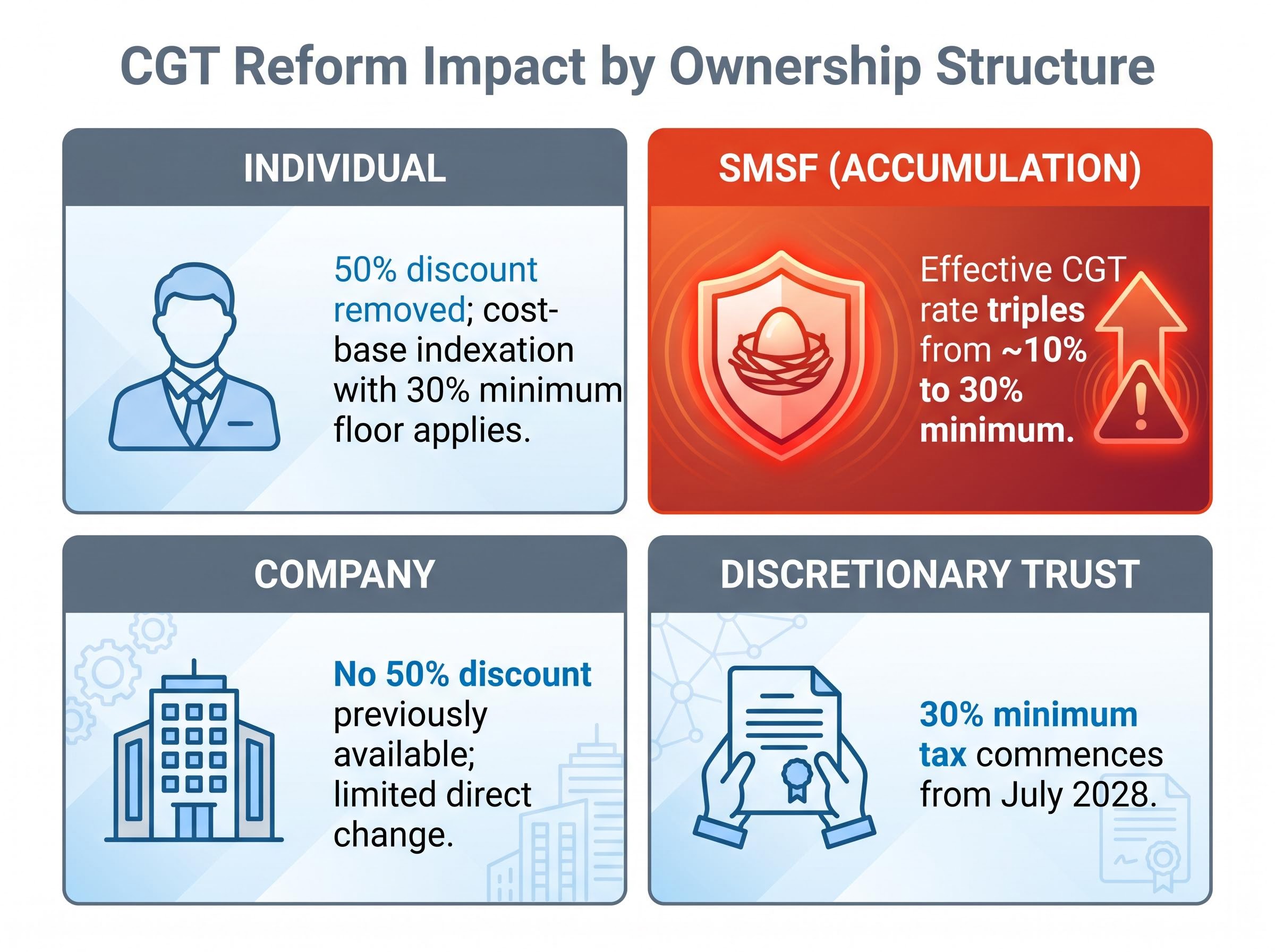

This floor has its most pronounced effect on entities that currently benefit from concessional tax rates. Companies do not use the 50% CGT discount under existing law, so the discount’s removal has limited direct impact on corporate structures. But for self-managed superannuation funds (SMSFs) in accumulation phase, the consequences are stark. Under the current system, a 15% tax rate combined with the 50% discount produces an effective CGT rate of approximately 10%. Under the 30% floor, that effective rate triples.

The ATO concessional CGT treatment for SMSFs in accumulation phase combines a 15% tax rate with a one-third discount for assets held beyond 12 months, producing the approximately 10% effective CGT rate that the 30% minimum floor directly overrides from 1 July 2027.

The window between Budget night and 30 June 2027 is not theoretical. It is a defined period in which investors holding appreciated established residential property can still dispose of assets under the existing 50% CGT discount regime. After that date, the discount disappears.

30 June 2027 is the last date on which an investor can sell an asset and have the 50% CGT discount applied. Disposals settling after this date fall under the new cost-base indexation regime with the 30% minimum tax floor.

Professional advisory firms including KPMG, Baker McKenzie, EY, Pitcher Partners, HLB Mann Judd, and RSM have all published post-Budget analyses recommending that investors engage with transitional planning now rather than deferring. Property data firms CoreLogic, Domain, and SQM Research have noted early signs of increased listings and investor activity in the post-Budget period, a potential early signal of the anticipated sell-down.

The practical steps for investors navigating this window are sequential, not simultaneous:

The investors most exposed are those who assume the 30 June 2027 deadline leaves ample time to decide later. Valuation queues, adviser capacity, and settlement periods all narrow the practical window faster than the date implies.

The city-by-city variation in CGT outcomes adds a further layer of complexity to the sell-versus-hold decision: PropTrack analysis suggests Melbourne investors are more likely to benefit from indexation relative to the old discount, while Brisbane investors face a higher probability of a larger tax bill under the new regime, reflecting differences in how real price growth tracked against inflation across each market.

The statement that “the new rules affect investors” obscures more than it reveals. The practical consequences of the 30% floor and the negative gearing ring-fencing vary materially depending on the structure through which the asset is held.

| Structure | CGT discount (old rules) | CGT treatment from 1 July 2027 | Negative gearing eligibility | Key planning implication |

|---|---|---|---|---|

| Individual | 50% discount available | Cost-base indexation; 30% minimum floor | Ring-fenced for established (post-Budget purchases) | Directly subject to both measures; assess sell-before vs. hold-through |

| SMSF (accumulation) | 50% discount; effective rate ~10% | 30% minimum floor; effective rate triples | Ring-fenced for established (post-Budget purchases) | Largest proportional impact; review superannuation-held property urgently |

| Company | No 50% discount available | 30% minimum floor; limited direct change | Ring-fenced for established (post-Budget purchases) | Discount removal has minimal direct impact; broader capital flow shifts are material |

| Discretionary trust | 50% discount available to beneficiaries | 30% minimum tax from July 2028 | Ring-fenced for established (post-Budget purchases) | Separate commencement date (July 2028); distinct planning timeline |

The SMSF accumulation phase stands out as the single largest impact point. An effective CGT rate rising from approximately 10% to 30% on property disposals represents a fundamental change to the after-tax return profile of superannuation-held property. Discretionary trusts face their own separate timeline, with the 30% minimum tax commencing from July 2028, according to Budget Paper No. 1. Investors holding property across multiple structures face the additional complexity of coordinating planning across different effective dates.

At the individual level, these reforms change tax bills. At the market level, they redirect capital.

The negative gearing ring-fencing removes a holding-cost subsidy for established residential property purchased from Budget night onward. The CGT discount removal, from July 2027, reduces the after-tax return on disposal. Together, these measures structurally reduce investor demand for established residential stock.

The redirection is by design. Negative gearing remains available for new builds, channelling investor demand toward new construction. Residential developers, including Stockland, Mirvac, and Lendlease, stand to benefit from increased demand for new product. Building materials suppliers such as Boral, CSR, and James Hardie are positioned to see flow-through demand if new build activity accelerates.

CoreLogic, Domain, and CommBank Economic Research have all published post-Budget commentary connecting early listing and activity signals to the reforms. ASX-listed REITs, including Dexus, Charter Hall, GPT, Goodman Group, and Scentre, are exposed at both the entity level and through unitholder tax position changes on capital distributions after 1 July 2027.

As property’s after-tax return profile deteriorates, capital is projected to shift toward equities. The reallocation thesis centres on investors applying stricter criteria favouring dividend yield and franking credits, the attributes that most directly replace the tax efficiency property previously offered.

High-yield mature businesses, particularly the major banks and established miners with fully franked dividends, are positioned as likely beneficiaries. Conversely, long-duration growth sectors such as technology, biotech, and early-stage resources may see reduced demand from investors who previously used tax-advantaged property holdings to offset the risk profile of growth equity positions.

Investors exploring how to position equity portfolios around the capital reallocation thesis will find our deep-dive into ASX sectoral rotation under the new CGT regime covers the relative after-tax return advantage of fully franked dividend income, the expected flow toward banks, telcos, utilities, infrastructure, and A-REITs, and the structural headwinds facing pure-growth equity strategies once the 30% floor closes the low-income-year timing strategy.

The negative gearing ring-fencing has been in force since 7:30pm AEST on 12 May 2026. Any established residential property purchased since that moment operates under the new rules. The CGT changes give investors approximately 13 months from Budget night to dispose of assets under the existing 50% discount regime, with 30 June 2027 as the hard deadline.

Professional advisory firms including KPMG, Baker McKenzie, EY, Pitcher Partners, HLB Mann Judd, and RSM have identified formal asset valuation before 1 July 2027 as the single most time-sensitive preparatory action, regardless of whether the investor ultimately sells or holds.

The formal valuation anchors the cost base for any future disposal under the new regime. Without it, investors risk contested or unfavourable cost-base determinations years after the transition.

Three steps warrant immediate attention:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The 50% CGT discount was introduced in 1999. For 27 years, it shaped how Australians accumulated wealth, how they structured property holdings, and how they weighed property against equities in portfolio construction. On 30 June 2027, that policy architecture ends.

The abolition of the 50% CGT discount marks the end of a 27-year policy framework that defined the after-tax return profile of Australian property investment. What replaces it is not a modified version of the old system but a structurally different regime.

The reforms are confirmed across Budget Paper No. 1 and ATO guidance, and the breadth of professional firm commentary from KPMG, Baker McKenzie, EY, Pitcher Partners, HLB Mann Judd, and RSM confirms they are being treated as a generational shift, not a marginal adjustment.

Three analytical threads converge: the mechanics of what changed, the transitional window in which investors can still act under the old rules, and the structural reallocation of capital that follows once the new regime is fully in force. Investors who engage with these changes now, obtaining formal valuations, reassessing ownership structures, and modelling the post-2027 environment, position themselves to navigate the transition on their own terms. Those who default to prior assumptions face material tax outcomes they did not plan for, in a market that has already begun to move.

The 2026-27 Budget introduced three reforms: the removal of the 50% capital gains tax discount for disposals after 1 July 2027, replacement with cost-base indexation subject to a 30% minimum tax floor, and the immediate ring-fencing of negative gearing so that losses on established residential properties purchased after 12 May 2026 can no longer be offset against other income.

Cost-base indexation adjusts the original purchase price of an asset upward in line with inflation using the Consumer Price Index, so only the real gain above inflation is taxed, rather than simply halving the nominal gain as the 50% discount did. A 30% minimum tax floor applies regardless, meaning investors pay the higher of their indexed tax liability or 30% of the net capital gain.

30 June 2027 is the last date on which an investor can dispose of an asset and have the 50% CGT discount applied; any disposal settling after this date falls under the new cost-base indexation regime with the 30% minimum tax floor.

SMSFs in accumulation phase are among the most severely affected structures because the current combination of a 15% tax rate and the 50% CGT discount produces an effective CGT rate of approximately 10%, which the 30% minimum tax floor will triple from 1 July 2027.

Advisers from firms including KPMG, EY, and Baker McKenzie recommend three immediate actions: classifying every property by purchase date and type to identify which rules apply, obtaining formal asset valuations before 1 July 2027 to anchor the cost base for any future disposal, and engaging a tax adviser to model the sell-before versus hold-through decision based on individual structure, holding period, and marginal tax rate.