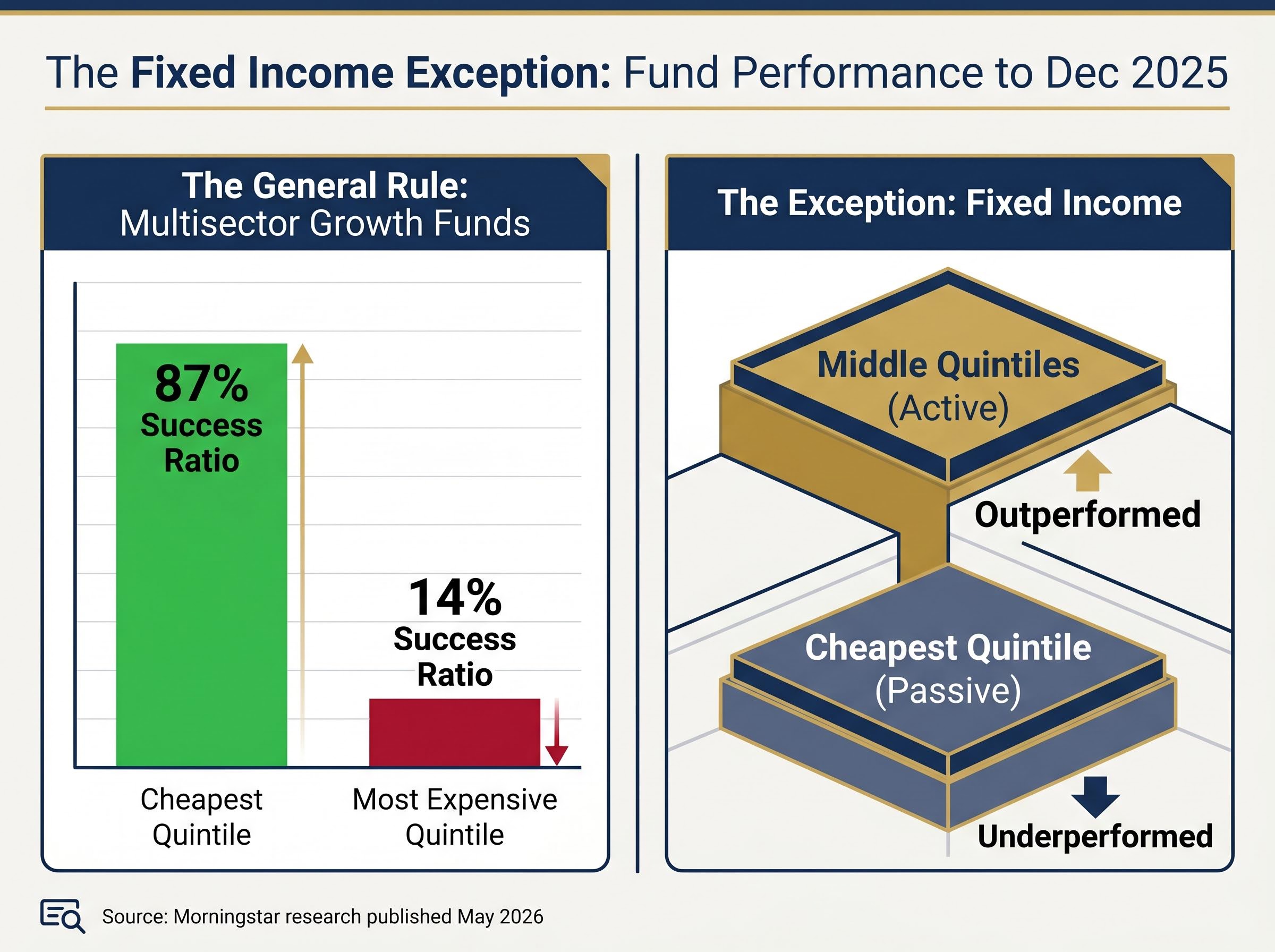

The most reliable rule in Australian funds research is that lower fees produce better outcomes. Across nearly every major category, cheaper funds deliver higher success ratios and stronger average returns. Except, it turns out, in bonds. Morningstar research published in May 2026, covering Australian fund performance to December 2025, found that the three middle cost quintiles in fixed income, dominated by competitively priced active strategies, outperformed the cheapest quintile, which is dominated by passive ETFs. This happened during one of the most difficult stretches for bond markets in a generation. What follows is an examination of what the data actually shows, the mechanical explanation for the outperformance, the market conditions that produced it, and what it means for how Australian investors should think about active bond funds when constructing a fixed income allocation.

The Morningstar finding that breaks the fee rule

The general finding from Morningstar Senior Manager Research Analyst Zunjar Sanzgiri is unambiguous across most categories. Cheaper funds win, and they win by wide margins.

In multisector growth funds, the cheapest quintile delivered an 87% success ratio compared with just 14% for the most expensive quintile.

The pattern holds in Australian equities, international equities, and multi-asset categories. The data is consistent enough to treat cost as a reliable predictor of outcomes in most portfolio decisions. The key messaging directives from the research are clear:

The broader evidence on fee compounding on long-term outcomes shows why the cost-first rule holds with such force across most categories: a 1% annual fee difference on a $100,000 portfolio earning 7% gross compounds into approximately $62,000 in lost wealth over 20 years, a drag that no alpha source in most asset classes can reliably offset.

- The cheapest quintile of funds outperformed in nearly every major Australian fund category studied.

- Success ratios declined consistently as fees increased, with the most expensive funds producing the worst outcomes.

- The relationship between lower fees and better performance held across both active and passive vehicles.

Then fixed income broke the pattern. The three middle expense ratio quintiles, where competitively priced active bond strategies sit, outperformed the lowest-cost quintile during the study period ending December 2025. The cheapest fixed income quintile is predominantly passive ETFs. This is not a classification quirk. It is a meaningful active-versus-passive divergence in the one asset class where the cost-first shortcut failed.

When big ASX news breaks, our subscribers know first

Why bond markets in 2022-2025 were unusually hostile to passive strategies

The 2022 rate shock was the defining event. The Reserve Bank of Australia and other major central banks delivered the sharpest and fastest rate-hiking cycle in decades. Broad-market bond ETFs, constructed to track cap-weighted indices, held long-duration exposure as rates rose. There was no mechanism within the passive structure to reduce that risk. The result was simultaneous drawdowns in equities and bonds, undermining the assumption that a passive bond allocation would hedge equity risk.

The RBA cash rate history shows the cash rate rising from 0.10% in April 2022 to 4.35% by November 2023, a tightening pace with no modern precedent in Australia, which translated directly into the duration losses that passive bond ETFs absorbed without any ability to reduce exposure.

Three compounding structural pressures explain why passive fixed income was exposed:

- Duration lock-in. Passive bond indices mechanically held long-duration positions through the entire rate-hiking cycle. Investors had no ability to shorten duration ahead of rate rises.

- Cap-weighting toward the most indebted issuers. Broad-market bond indices give greater weight to issuers that borrow more, creating a structural tilt toward leveraged entities regardless of credit quality trends.

- Loss of the equity-hedge function. The passive bond allocation that was assumed to stabilise portfolios during equity downturns instead fell alongside equities in 2022, removing the diversification benefit investors relied on.

When correlations break, the passive hedge fails

In 2022, bond-equity correlations turned positive. Passive bond ETFs declined at the same time as equity markets, a regime-specific failure rather than a permanent one, but one with lasting consequences for how advisers and institutional investors think about what “defensive” means in a fixed income context.

Australian adviser commentary from 2024 onward reflected a recalibration. The conversation shifted from whether passive bonds were the default to whether the structure itself was fit for purpose during active central bank cycles. The 2022-2024 period also featured elevated yield dispersion across sectors and issuers, which widened the gap between the best and worst bond positions well beyond what a stable, low-rate environment would produce.

The mechanics of active bond management in stressed markets

Active bond managers operated through the 2022-2024 cycle with a specific set of tools, each of which addressed a different dimension of the stress.

Duration management was the primary lever. Managers adjusted portfolio DV01 (the dollar value of a basis point, which measures how much a portfolio’s value changes when interest rates move by one basis point) relative to the benchmark. Commentary from PIMCO, Western Asset Management, and Fidelity International Australia described how managers shortened duration ahead of rate hikes and gradually re-extended as central banks approached terminal rates. Passive investors had no equivalent mechanism.

Duration risk in Australian bond ETFs produced sharply divergent outcomes during the 2022-2024 cycle: a fund with 17 years of effective duration faced an implied capital loss of roughly 17% for each 1% rise in yields, while intermediate-duration alternatives with 8 years of duration absorbed the same rate moves with roughly half the drawdown.

Yield curve positioning allowed active managers to use steepeners, flatteners, and key-rate duration adjustments to hedge against non-parallel yield curve shifts, expressing views on the shape of the curve independently of the index’s duration profile.

Sector rotation between Commonwealth government bonds, semi-government securities, and corporate credit gave managers the ability to shift allocations as yield spreads and fundamental conditions changed, while passive ETFs held all sectors simultaneously in fixed proportions.

The index’s built-in flaw: rewarding the most indebted

Credit selection represents a structural advantage that is grounded in index construction logic. Cap-weighted bond indices mechanically increase exposure to issuers as they borrow more. An issuer that doubles its outstanding debt doubles its index weight, regardless of whether the additional borrowing reflects deteriorating fundamentals or increased leverage risk. Coolabah Capital Investments has framed this as the “borrow more, own more” problem in Australian fixed income.

Active managers can exit deteriorating credits before index rebalancing forces passive funds to continue holding them. They can also hold cash and liquid government bonds to buy when spreads blow out, acting as buyers when passive vehicles and risk-parity strategies become forced sellers. Western Asset Management’s 2024 white paper documented this dynamic using case studies from both the March 2020 COVID episode and the 2022 rate shock.

| Active Lever | What It Does | When It Adds Value | Passive Equivalent |

|---|---|---|---|

| Duration management | Adjusts interest rate sensitivity relative to benchmark | Active central bank hiking or cutting cycles | None; duration is fixed by index composition |

| Yield curve positioning | Expresses views on the shape of the yield curve | Non-parallel curve shifts (steepening or flattening) | None; index holds a static curve profile |

| Credit selection | Avoids deteriorating issuers, targets undervalued credits | Rising defaults, widening credit dispersion | Cap-weighted; overweights the most indebted issuers |

| Sector rotation | Shifts between sovereign, semi-government, and corporate debt | Spread compression or widening across sectors | Fixed proportional allocation to all sectors |

| Liquidity / opportunistic buying | Holds cash to buy during sell-offs and forced liquidations | Market stress episodes with forced sellers | Fully invested; must hold index at all times |

What “regime” means for the active-passive decision in fixed income

The Morningstar finding creates an apparent contradiction: passive usually wins, yet active won here. The resolution is regime-dependence.

The conditions favouring active fixed income are specific and identifiable:

- High yield dispersion across sectors and issuers, creating meaningful differences between the best and worst positions.

- Active central bank policy cycles, where duration and curve positioning decisions have a measurable impact on returns.

- Uncertain inflation, which rewards managers who can adjust quickly to shifting real rate expectations.

The conditions favouring passive fixed income are equally specific:

The regime-dependence of fixed income returns connects directly to a broader question about portfolio resilience beyond the 60/40 split: when the stock-bond negative correlation turns persistently positive during inflation shocks, the conventional defensive function of a bond allocation fails not because bonds are priced incorrectly but because the macroeconomic regime has changed.

- Stable rate environments where duration risk is low and predictable.

- Tight, uniform credit spreads where credit selection adds minimal incremental return.

- Low volatility where the cost of active management exceeds the alpha available.

Asset consultants have already embedded this regime sensitivity into their frameworks. JANA Investment Advisers concluded that core sovereign bond exposure can be passively managed, while recommending active management in credit and multi-sector fixed income. Frontier Advisors recommended increasing allocations to active absolute-return and unconstrained bond strategies following the 2022 drawdowns.

The Association of Superannuation Funds of Australia (ASFA) published survey data in late 2024 indicating that the majority of large Australian super funds intended to increase or maintain allocations to active credit and absolute-return bond strategies over 2025-2027, while core sovereign exposure was more likely to be indexed or managed with low tracking error.

The analytical finding becomes usable once investors understand when each approach is structurally advantaged. The Morningstar data reflects a specific regime, not a permanent reversal of the cost rule.

How fund ratings are evolving to incorporate fees

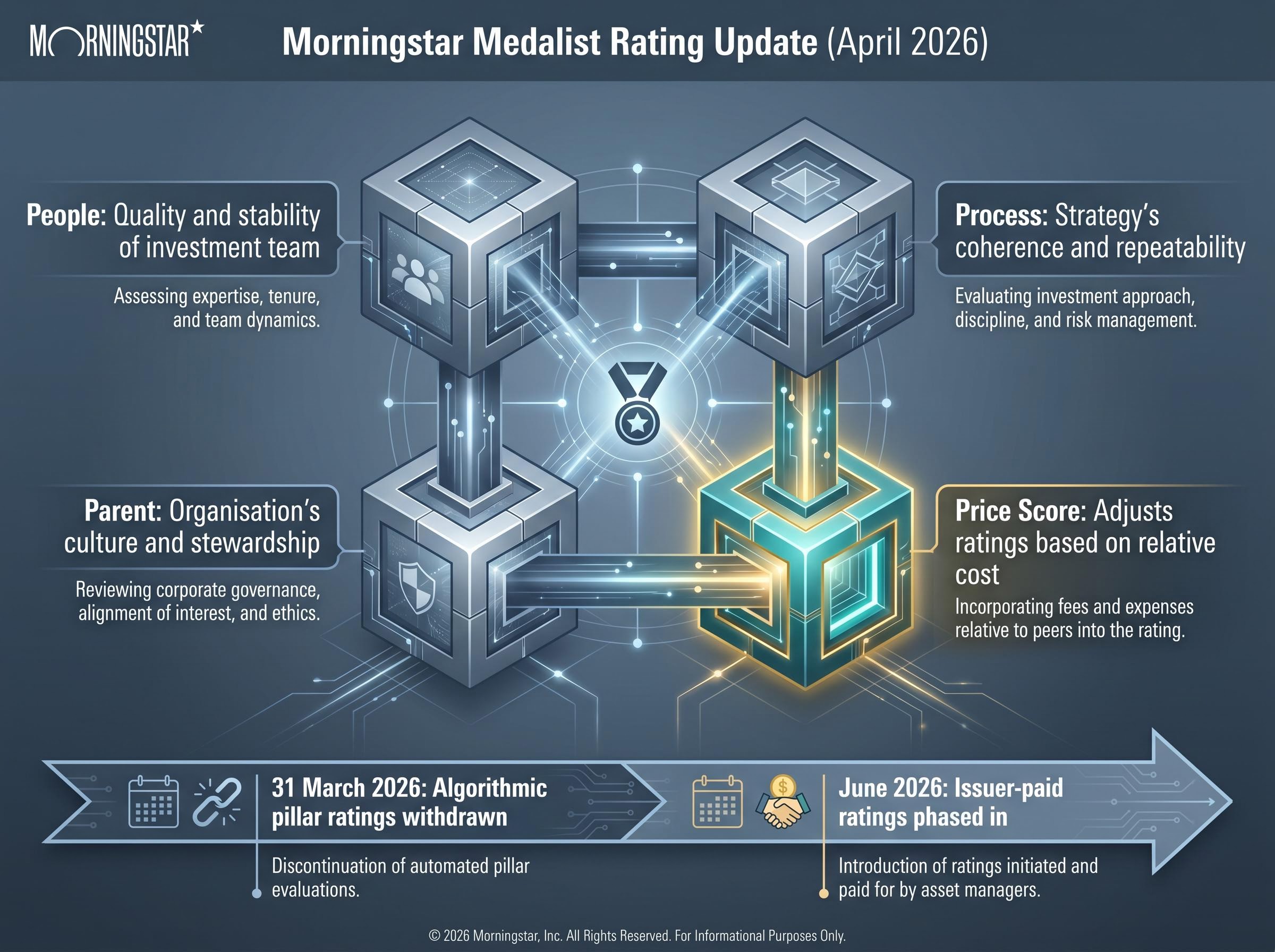

Morningstar implemented an update to its Medalist Rating methodology in April 2026, introducing a pricing score alongside the existing assessment framework. The four components now contributing to a Medalist Rating are:

- People: Assessment of the quality and stability of the investment team.

- Process: Evaluation of the investment strategy’s coherence and repeatability.

- Parent: Assessment of the fund management organisation’s culture and stewardship.

- Price Score: A new component that adjusts ratings based on a fund’s cost relative to peers in its category.

Strategies with higher costs face greater difficulty achieving Gold, Silver, or Bronze ratings. The pricing score is calibrated by category rather than applied as a universal fee threshold, an acknowledgment that fee predictiveness varies by asset class. Some active bond funds have retained positive Medalist assessments despite higher fees than passive ETFs, where the historical evidence supports the value-add.

Australian adviser commentary has noted that while equity and multi-asset managers with above-median fees face the greatest rating risk, fixed income ratings reflect a more mixed balance between fee efficiency and demonstrated risk management.

The Australian timeline: a different transition path

Australian and New Zealand non-superannuation funds followed a distinct transition pathway. Algorithmic pillar ratings were withdrawn from 31 March 2026, with issuer-paid ratings phased in from June 2026. During this transition window, Morningstar ratings for Australian-domiciled funds should be read with awareness of which methodology was in effect at the time the rating was issued.

Building a fixed income allocation that reflects the actual evidence

The practical resolution of the active-passive debate in Australian fixed income is the core-satellite framework that major super funds already employ. AustralianSuper uses predominantly active fixed income in its diversified options. UniSuper runs a passive core complemented by specialist active credit and absolute-return bond strategies. Cbus Super has expressed a preference for active management particularly in credit and emerging markets debt.

The Morningstar finding provides a specific anchor: it was the mid-priced active tier (quintiles 2, 3, and 4) that outperformed, not simply any active strategy regardless of cost. Investors should apply fee scrutiny within the active universe rather than treating “active” as permission for high fees.

| Fixed Income Segment | Recommended Approach | Rationale |

|---|---|---|

| High-quality sovereign bonds | Passive or low-tracking-error core | Efficiently priced; information advantages are minimal; fees matter most |

| Investment-grade credit | Competitively priced active | Credit selection and sector rotation add value; cap-weighting flaws are most pronounced |

| Multi-sector / absolute-return bonds | Active with duration flexibility | Duration management and liquidity levers activate during stress; passive cannot replicate |

| Emerging market debt | Active with specialist mandate | Higher dispersion, lower liquidity, and greater credit risk reward active selection |

Three verification steps are necessary before implementing any allocation decision:

For investors ready to move from the allocation framework to actual fund selection, our comprehensive walkthrough of managed fund due diligence covers the specific PDS sections that carry the most decision weight, how to verify AFS licence status on ASIC Connect, and a structured red-flag screening process applicable to any active fixed income mandate.

- Check current management expense ratios via product disclosure statements, as published fees change and the Morningstar study period ended December 2025.

- Confirm active ETF availability for retail access, noting that the landscape of ASX-listed active bond ETFs is evolving and requires direct verification.

- Source current performance data directly from fund managers’ official publications, as the specific quantitative performance claims in this research require independent verification.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

The cost rule still stands, but it needs a fixed income footnote

The Morningstar research confirms that cost discipline remains one of the most reliable indicators of fund performance outcomes across almost every Australian fund category. That principle does not disappear for fixed income. It becomes conditional.

The relevant cost question in fixed income is not “passive or active?” but rather which tier of active management, and whether the fee reflects a genuine, verifiable source of value-add in the specific market conditions being navigated. The mid-priced active tier outperformed. The most expensive tier did not.

The 2022-2025 rate cycle has reshaped how institutional investors, asset consultants, and now Morningstar’s own methodology think about active fixed income management in Australia. Advisers and self-directed investors constructing or reviewing a fixed income allocation should consult current product disclosure statements, consider the regime context for any active-versus-passive decision, and use the Morningstar Medalist Rating (with awareness of the April 2026 methodology update) as one input in a broader assessment. The cost rule holds. It simply requires a fixed income footnote.