Why Your ETF Portfolio May Be Less Diversified Than You Think

56 mins ago

Australia’s capital gains tax framework is being restructured for the first time in decades. On 15 May 2026, Treasurer Jim Chalmers announced reforms that will take effect in 2027, replacing the 50% holding-period discount with inflation indexation of the cost base and introducing a 30% minimum CGT rate floor. While housing commentary has dominated early coverage, these changes apply to all CGT assets, including listed equities and managed funds. For finance-literate investors holding Australian shares, the question forming in real time is whether to sell before the new regime begins. This article explains the mechanical shift from discount to indexation, assesses who actually faces a higher tax burden under the new rules, and draws on international evidence to evaluate whether pre-emptive selling or portfolio restructuring is warranted.

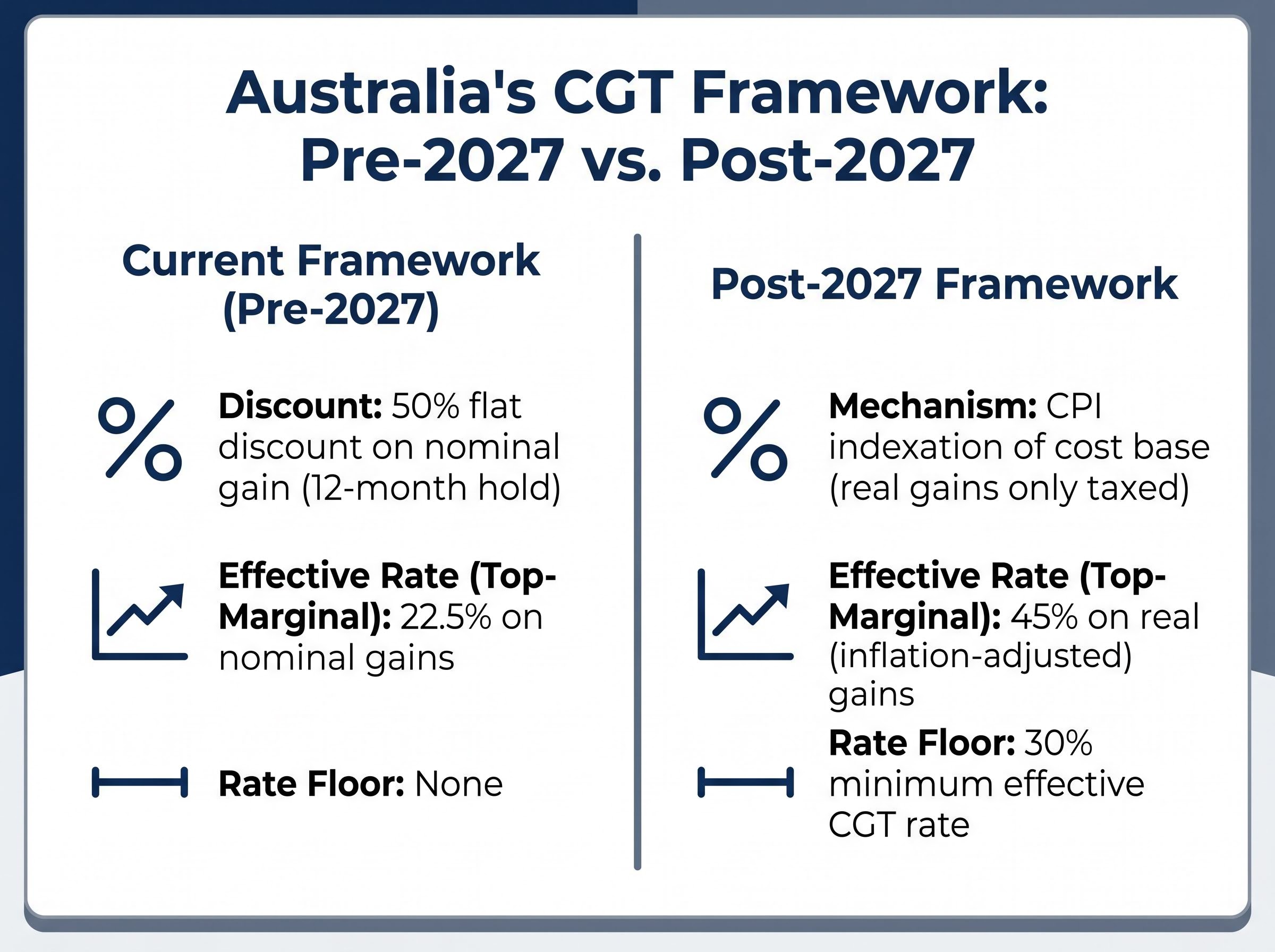

The current CGT framework taxes capital gains at the taxpayer’s marginal income tax rate, with a 50% discount applied to assets held for longer than 12 months. For a taxpayer on the top marginal rate of 45%, that discount produces an effective CGT rate of 22.5% on nominal gains. The system is simple: hold for a year, halve the gain, pay tax on the rest.

From 2027, two changes replace that framework.

The 50% discount is removed entirely. In its place, the original cost base of a CGT asset is adjusted upward in line with the Consumer Price Index (CPI) before the gain is calculated. Only the portion of gain exceeding cumulative inflation over the holding period is subject to tax. In practical terms, the purchase price is inflated to reflect what it would be worth in today’s dollars, and only the real appreciation above that figure is taxable.

This is not a new concept. Inflation indexation was Australia’s original CGT treatment when the system was introduced in 1985. The Howard government replaced it with the 50% discount in 1999, primarily on simplicity grounds.

The second element is a 30% minimum CGT rate floor. This sets a statutory minimum for the effective CGT rate regardless of the taxpayer’s marginal income tax rate. In practice, this primarily affects lower-income taxpayers earning below approximately $45,000 annually, whose marginal rate would otherwise produce an effective CGT rate below 30%. High-income investors, who dominate equity-market commentary, already face effective rates well above this floor.

The following table compares the two frameworks across three dimensions.

| Feature | Current framework (pre-2027) | Post-2027 framework |

|---|---|---|

| Discount mechanism | 50% flat discount on nominal gain (12-month hold) | CPI indexation of cost base (real gains only taxed) |

| Effective rate (top-marginal taxpayer) | 22.5% on nominal gains | 45% on real (inflation-adjusted) gains |

| Rate floor | None | 30% minimum effective CGT rate |

The instinct to treat this as a uniform tax increase does not survive contact with specific taxpayer profiles. The distributional effects depend on three variables: marginal tax bracket, holding period, and the inflation environment during that holding period.

The inflation indexation mechanism may actually reduce CGT liability for assets held through high-inflation periods compared to the flat 50% discount. The reform replaces a crude tool with a precision instrument, and precision cuts both ways.

The 30% floor and indexation interaction is more nuanced than the headline rate suggests: as the RBA’s target band of 2–3% inflation becomes the new normal, annual CPI uplifts to the cost base will be modest, meaning the floor is more likely to activate for a broader range of investors than current market commentary implies.

The calculation itself is straightforward in principle. At disposal, an investor (or their accountant) needs to complete three steps:

The difficulty is not the formula. It is the record-keeping. An investor who has accumulated a portfolio over 15 years through regular contributions, dividend reinvestment plans (DRPs), and corporate actions holds dozens or hundreds of individual parcels. Each parcel has a different acquisition date and therefore a different CPI adjustment factor. Under the current 50% discount, every parcel receives identical treatment: halve the gain. Under indexation, every parcel requires its own calculation.

This was the pre-1999 CGT system, and the ATO has existing infrastructure and methodology for CPI-indexed cost base calculations. That operational precedent reduces the implementation risk argument. Modern portfolio tracking software and broker-issued tax statements are also substantially more capable than their 1999 equivalents.

The administrative dimension has been largely absent from market commentary so far. For active equity investors managing their own portfolios, the record-keeping implications may matter as much as the rate change itself.

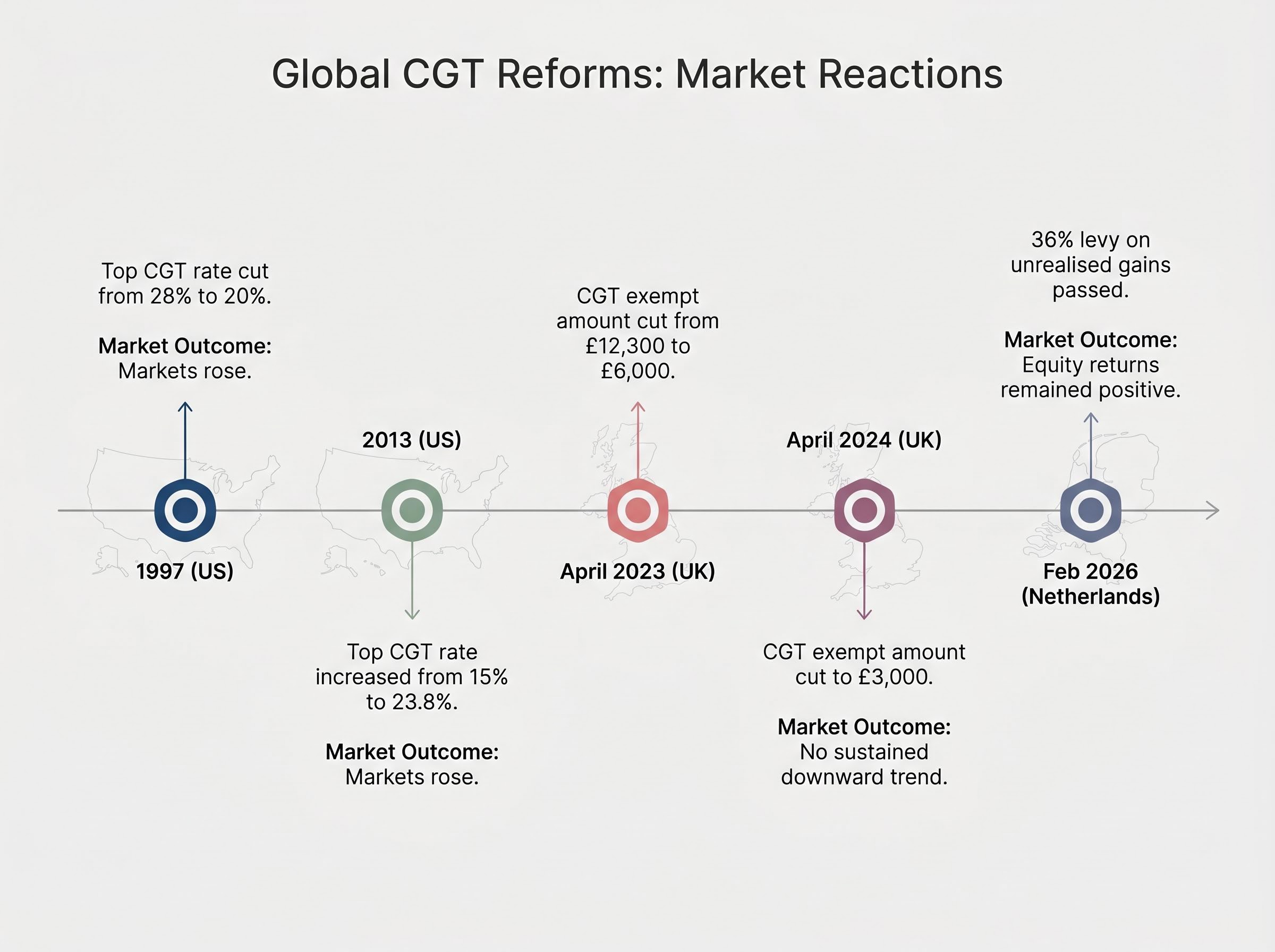

In 1997, the United States reduced its top CGT rate from 28% to 20%. Equity markets rose, but they were already rising before the change was announced. In 2013, the top US federal CGT rate increased from 15% to 23.8% (including the Net Investment Income Tax). Markets rose that year too. In neither case did the directional bet implied by pre-announcement commentary, that lower rates would boost equities and higher rates would suppress them, play out cleanly.

The United Kingdom has adjusted CGT rates and annual exempt amounts periodically. The most recent change, a reduction in the annual CGT exempt amount from £12,300 to £6,000 in April 2023 and then to £3,000 in April 2024, generated widespread pre-implementation selling predictions. UK equity indices did not produce the sustained downward trend the commentary anticipated.

The pattern across markets is consistent: CGT rate changes are absorbed as investors recalibrate expected after-tax returns. The adjustment is real, but it tends to be priced over the discussion period rather than at implementation.

CGT rate changes in the US and UK have not consistently produced the equity market outcomes investors anticipated before implementation. The announcement effect is typically the largest observable market signal; the actual implementation often generates less dramatic responses than feared.

Three factors reduce this reform’s capacity to generate market surprise in Australia:

The Netherlands offers a further reference point. A 36% levy on unrealised capital gains passed the Dutch lower house in February 2026, a structurally more aggressive reform than Australia’s indexed realised-gains approach. Dutch equity returns remained positive after passage.

Early coverage has conflated two separate budget measures, and the confusion is creating unnecessary anxiety among equity investors.

The budget includes a separate change to negative gearing rules targeting rental properties. Under the revised rules, losses on rental properties can only offset residential property income and capital gains. They can no longer be deducted against other income streams such as salary or business income. This narrows the prior broader offset capability.

This change does not affect negative gearing arrangements applied to leveraged equity investments. Investors using margin loans for share purchases, where interest expenses are deducted against dividend income and capital gains, are not touched by the negative gearing modification. The property-specific restriction has no bearing on the deductibility of interest on borrowings used to generate equity returns.

| Reform element | Property investors | Equity investors |

|---|---|---|

| CGT discount replaced by indexation | Applies (all CGT assets) | Applies (all CGT assets) |

| 30% CGT rate floor | Applies (all CGT assets) | Applies (all CGT assets) |

| Negative gearing restriction | Applies (rental property losses confined to property income) | Does not apply (leveraged equity interest deductions unchanged) |

For investors holding both property and equities, this distinction is directly actionable. The two reforms operate independently, and treating them as a single package overstates the impact on equity portfolios.

For investors holding both property and equities who want to understand the full scope of the property-side restriction, our full explainer on the negative gearing changes covers the ring-fence mechanics, the grandfathering cut-off of 12 May 2026, the trust distribution minimum tax, and the analyst forecasts for rental market and construction activity through 2028.

The question is not “should I sell before 2027?” It is whether the after-tax return calculation under the new framework changes the hold or sell decision that would have been made anyway.

The investor cohort for whom the change is most material is specific: high-income taxpayers on the top marginal rate, holding large equity positions with substantial nominal gains accumulated over long periods in a low-inflation environment. For this group, the 50% discount has provided significantly more relief than inflation indexation would have, because most of their gain is real appreciation rather than inflationary noise.

Investors in this position should model the indexed cost base versus the 50% discount for their specific holdings before treating the reform as a reason to realise gains early. The calculation is tractable: identify the acquisition date, apply the CPI index factor for the holding period, and compare the taxable gain under each method.

Reactive selling carries a countervailing risk. Crystallising a tax liability now under the current regime to avoid a potentially smaller, or not materially different, liability under the new regime is a calculable error rather than a prudent hedge. The current effective CGT rate of 22.5% for top-bracket taxpayers is the rate paid today if gains are realised today. Deferral keeps the option value of indexation intact.

The lock-in effect on portfolio reallocation is a second-order consequence the rate arithmetic alone does not capture: higher effective CGT rates discourage asset sales even where reallocation would otherwise be rational, creating portfolio drag that compounds over the years between now and a future disposal.

Investor profiles most likely to face a genuinely increased tax burden:

Investor profiles where the change may be neutral or favourable:

The CGT reform announced today is a genuine structural change with real distributional effects. It replaces a blunt instrument with a mechanically precise one, and some investors will pay more while others may pay less. That is the arithmetic reality.

Its impact on aggregate equity market returns is likely to be modest. The reform’s scope is confined to the discount mechanism and a rate floor that primarily affects lower-income taxpayers. It was discussed publicly for months before the announcement, reducing its surprise premium. Indexation provides a partial offset for some investor cohorts, particularly those holding assets through periods of elevated inflation.

Sectoral rotation toward franked dividend stocks is one of the more actionable structural implications of the reform: the removal of the CGT discount raises the relative after-tax value of fully franked income compared to capital appreciation, supporting a repricing in favour of banks, telcos, utilities, and infrastructure on the ASX.

Among comparable recent CGT reforms in developed economies, the 2027 Australian change sits at the moderate end of the spectrum. The Netherlands’ 36% levy on unrealised capital gains, passed in February 2026, represents a structurally more aggressive approach, yet Dutch equity returns remained positive after passage. The UK’s reduction of the annual CGT exempt amount to £3,000 in 2024 was narrower in mechanism but generated similarly disproportionate pre-implementation anxiety.

Among comparable recent CGT reforms in developed economies, the 2027 Australian change is at the moderate end of the spectrum. The primary investor task between now and implementation is portfolio-level modelling of the indexed cost base versus the current discount, not reactive reallocation.

The most common investor error in reform windows is reacting to headline framing rather than individual-position arithmetic. For equity investors with long-held Australian shares, the calculation is worth doing before 2027. The numbers, not the narrative, should drive the decision.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Tax outcomes depend on individual circumstances, and the legislative detail of the 2027 reforms may evolve before implementation.

From 2027, instead of halving a nominal capital gain after 12 months, investors will adjust the original cost base of an asset upward using the Consumer Price Index (CPI) for the holding period, so only the real inflation-adjusted gain is subject to tax at the full marginal rate.

High-income taxpayers on the top 45% marginal rate holding large equity positions with substantial nominal gains accumulated during low-inflation years (roughly 2012-2020) face the greatest risk of a higher tax burden, because the 50% flat discount historically provided more relief than modest CPI indexation would.

No. The budget's negative gearing restriction only confines rental property losses to property income and capital gains; it does not affect deductions for interest on margin loans or other borrowings used for leveraged equity investments.

The 30% minimum effective CGT rate primarily affects lower-income taxpayers earning below approximately $45,000 annually, whose marginal rate would otherwise produce an effective CGT rate below 30%; high-income investors already face effective rates well above this floor.

The article recommends modelling the indexed cost base against the current 50% discount for specific holdings before acting, because reactive selling crystallises a known liability today to avoid a potentially smaller or neutral liability under the new regime, which is a calculable error rather than a prudent hedge.