Soft Payrolls, Sticky Wages: the Fed’s Dilemma in 2026

46 mins ago

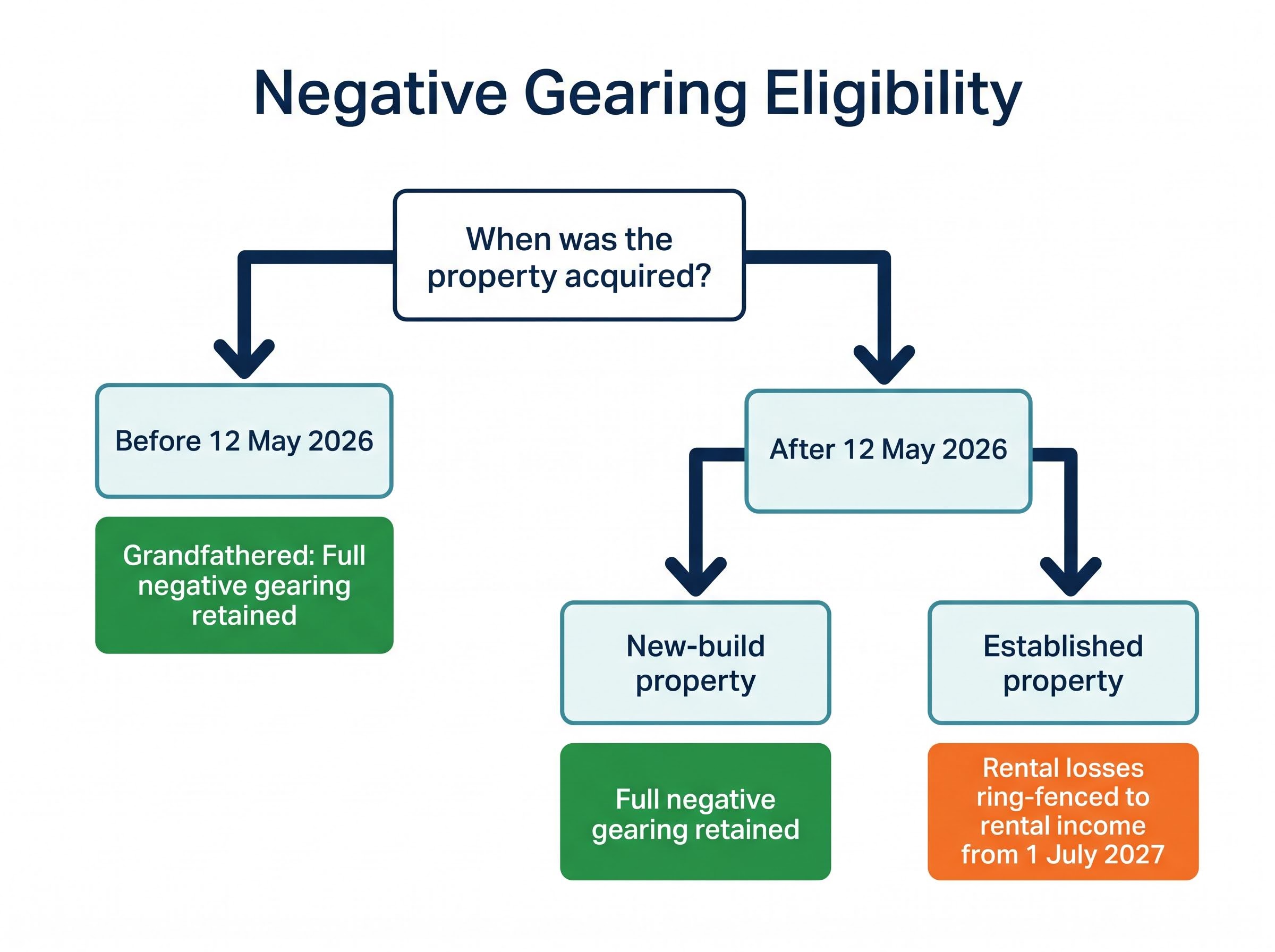

Australians hold more than two million negatively geared investment properties. The budget delivered on 12 May 2026 just changed the rules for every single one acquired after that date.

Treasurer Jim Chalmers has announced the most significant structural overhaul of property investment taxation in a generation. Negative gearing will be restricted to new builds, and the long-standing 50% capital gains tax discount will be replaced by a cost-base indexation model. Both changes take effect from 1 July 2027. Properties held before budget night remain protected under grandfathering provisions, but the implications for anyone who buys, sells, or restructures from this point forward are substantial.

What follows sets out exactly what has changed to negative gearing and the capital gains tax regime, what is protected under grandfathering, how the new CGT model works in practice, what trust holders need to act on, what the new worker tax offsets mean for everyday taxpayers, and what early market signals suggest about prices, rents, and construction.

Negative gearing is the mechanism by which rental property losses, where expenses such as mortgage interest, maintenance, and depreciation exceed rental income, are deducted against an investor’s other taxable income, including wages or salary. A teacher earning $95,000 who also owns a rental property generating a $10,000 annual loss could reduce their taxable income to $85,000, lowering the tax they owe across the board.

This treatment made property investment one of the most widely used tax minimisation strategies in Australia. More than two million investment properties have been negatively geared under these rules.

The three-reform tax package carries a combined revenue impact of approximately $77 billion over the decade, spanning capital gains tax, negative gearing, and discretionary trust distributions, with trustees also receiving a rollover relief window from 1 July 2027 to restructure without triggering immediate CGT events.

The budget draws a hard line. Properties acquired after budget night (12 May 2026) are subject to new rules commencing 1 July 2027. For established (non-new) properties purchased after that date, rental losses will be ring-fenced: they can only be offset against rental income, not wages or salary. Unused losses can be carried forward to offset future rental income, but the cross-subsidy against employment income is gone.

New builds remain fully eligible for negative gearing under the incoming rules. The distinction between the two regimes is sharp:

For the millions of Australians who have built or are planning investment property portfolios, this is the single most consequential shift in decades. Whether an existing tax strategy remains valid or needs to be revisited depends entirely on which side of that line a property falls.

The grandfathering provisions are the first thing most existing investors want confirmed, and the clear cases are genuinely clear. All investment properties held at budget night (12 May 2026) retain access to negative gearing under the previous rules. Treasury’s FAQ documentation, released on budget night, specified that grandfathering applies to “existing interests,” with no sunset date.

The operative phrase: Treasury’s FAQ confirms grandfathering applies to “existing interests” held at budget night. This is the language investors and their advisers are now scrutinising for scope and limitation.

The uncertain cases are where caution is warranted. Treasury’s FAQ has not fully resolved several edge-case scenarios, and the ATO helpline experienced heavy demand immediately after the announcement as investors sought clarity. Specific questions remain around properties purchased before 1 July 2027 but not tenanted until after that date, and whether significant renovations or additions to grandfathered properties alter their status.

Three scenarios illustrate the spectrum:

Investors mid-purchase or planning imminent acquisitions need to understand that timing alone does not guarantee protection. ATO guidance on edge cases remains pending, and relying on forum speculation rather than official channels carries real risk.

The budget.gov.au tax reform documentation confirms the 1 July 2027 commencement date, the grandfathering provisions for properties held before 7:30 PM AEST on 12 May 2026, and the full scope of the cost-base indexation model replacing the 50% CGT discount.

Under the new regime, a property investor’s tax return will look materially different. The 50% CGT discount for individuals holding assets for more than 12 months, the mechanism that halved the taxable portion of a capital gain, is being replaced for new property acquisitions by a cost-base indexation model.

Indexation adjusts the original purchase price for inflation before the taxable gain is calculated. If a property was purchased for $500,000 and inflation over the holding period totalled 20%, the indexed cost base becomes $600,000. A sale at $750,000 would produce a taxable gain of $150,000 rather than $250,000. The gain that remains after indexation is the “real gain,” and it is taxed at a minimum rate of 30%, applying to individuals, trusts, and partnerships.

| Dimension | Outgoing 50% discount | Incoming indexation model |

|---|---|---|

| How the gain is calculated | Nominal gain halved (50% excluded) | Purchase price adjusted for inflation; gain measured as difference between sale price and indexed cost base |

| Effective tax treatment | 50% of nominal gain taxed at marginal rate | Real gain taxed at minimum 30% |

| Who it applies to | Individuals holding 12+ months | Individuals, trusts, and partnerships |

| Eligible properties | Grandfathered properties held before budget night | New acquisitions from 1 July 2027 |

Gains accrued before 1 July 2027 on properties held through the transition remain eligible for the existing 50% discount. The new regime applies only to gains accruing from that date on new acquisitions. Investors in new residential builds may elect between the existing and incoming CGT regimes, offering flexibility for those who act before the transition.

Several categories are explicitly excluded from the changes:

For long-term holders, indexation may produce comparable or even superior outcomes in high-inflation environments. The 30% minimum tax floor, however, adds a layer of complexity that makes individual modelling a requirement before any disposal decision.

For investors with large unrealised gains who need to understand the dollar cost of the change before acting, our full explainer on Australia’s CGT cost modelling works through scenarios showing a business founder selling a $1 million company could lose more than $225,000 in after-tax proceeds, and examines how the lock-in effect may discourage portfolio reallocation even where a sale would otherwise be rational.

A 30% minimum tax on trust distributions related to property investment income is being introduced from 1 July 2027. For the significant number of Australian investors who hold rental properties through family trusts, this changes the calculus that made those structures attractive in the first place.

Under existing arrangements, a family trust can distribute property income (including capital gains) to beneficiaries on lower marginal tax rates, reducing the overall tax paid. The incoming 30% floor means that regardless of the beneficiary’s marginal rate, property-related distributions will be taxed at no less than 30%. Many existing distribution strategies will become less effective as tax minimisation tools.

CPA Australia and the Tax Institute of Australia have both flagged these budget changes as priority items for client advisory work in 2026-27. The professional consensus is clear: conduct a thorough audit of trust structures and investment portfolios before the 1 July 2027 commencement, model individual disposal scenarios, and avoid panic-selling without proper analysis.

Premature disposals carry their own risk. Selling established properties before the transition purely to restructure may trigger CGT liabilities before investors have confirmed their reinvestment path. The window to restructure is already narrowing, but acting without analysis is as dangerous as doing nothing.

Investors holding property through trust structures should be putting these questions to their accountants:

The interaction between the new minimum tax and existing trust distribution strategies means that doing nothing may be as costly as acting hastily. Individual modelling is not optional.

The budget also delivers two measures aimed directly at wage earners, offering a moment of relative simplicity amid the investment tax complexity.

The first is the Working Australians Tax Offset (WATO): a permanent $250 per year offset taking effect from 1 July 2027. It will not appear in tax returns until July 2028, as it applies from the 2027-28 income year onward. The estimated cost is $6.4 billion over three years.

The second is an instant $1,000 tax deduction available without receipts, effective from the 2026-27 income year. Approximately 6.2 million workers are expected to benefit, generating an average saving of around $205 per worker.

| Measure | Amount | Eligibility | Available from | First in tax returns |

|---|---|---|---|---|

| Working Australians Tax Offset (WATO) | $250 per year (permanent) | Australian workers | 1 July 2027 | July 2028 |

| Instant tax deduction | $1,000 (no receipts required) | Approx. 6.2 million workers | 2026-27 income year | July 2027 |

For the majority of Australians who are not property investors, these measures represent the most tangible budget benefit: a modest but permanent reduction in the tax burden on ordinary workers.

The tax rules are only half the picture. The market environment in which they will play out is already generating competing forecasts, and the divergence is itself informative.

The three forecast areas that matter most:

Construction sector stress is already acute, with 2025 insolvencies setting an all-time national record and construction collapses accounting for 21% of all failures, a backdrop that raises legitimate questions about whether the industry has the capacity to deliver the new dwelling uplift HIA and Master Builders Australia are projecting from 2028.

The tension between industry warnings and economist support is genuine. The Property Council and REIA see the reforms as a direct threat to rental supply. Reform supporters see a short-term adjustment that new supply will correct.

AMP Chief Economist Shane Oliver has argued that short-term rental vacancy drops are a transitional consequence expected to be offset by new supply, characterising the reforms as a positive step toward reducing speculative investment in established housing.

The broader fiscal context adds another variable. The budget projects a $28.3 billion deficit for 2026-27 (approximately 1% of GDP). GDP growth has been revised down to 1.75% from 2.25%, and Treasury anticipates inflation will peak at approximately 5% around mid-year, attributed to the Iran energy shock. Whether the construction uplift materialises depends heavily on whether state-level planning reforms arrive alongside the federal tax changes, a coordination challenge that neither the budget papers nor the industry modelling can resolve on their own.

The tax rules governing investment property will look materially different from 1 July 2027, and the decisions made between now and then will lock in outcomes that could persist for decades.

The actionable threads are clear. Confirm whether existing properties are grandfathered. Model CGT outcomes under both regimes before selling anything. Have trust structures assessed by a qualified adviser who has modelled the 30% minimum tax against current distribution strategies. Consider whether any new acquisition plans should be redirected toward new builds to preserve negative gearing eligibility.

A new-build acquisition strategy now sits at the intersection of two policy settings pulling in the same direction: the budget’s negative gearing carve-out for new builds and the federal 5% Deposit Scheme, updated from October 2025 with no income caps or place limits, together reducing both the tax cost and the entry barrier for first-time property investors willing to commit to newly constructed dwellings.

Treasury and the ATO are expected to release further guidance on edge cases. Investors should monitor official channels at budget.gov.au and ato.gov.au rather than relying on forum speculation. The window is open. It will not stay open indefinitely.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Tax positions described are subject to further ATO guidance and legislative passage.

From 1 July 2027, negative gearing will be restricted to new builds only for properties acquired after 12 May 2026. Rental losses on established properties purchased after that date will be ring-fenced and can only offset rental income, not wages or salary.

Yes, properties held before 12 May 2026 are grandfathered and retain full negative gearing under the previous rules with no sunset date specified. However, properties purchased after budget night but before 1 July 2027 are not grandfathered and will be subject to the new rules from the commencement date.

Instead of halving the taxable capital gain, the new model adjusts the original purchase price for inflation before calculating the gain, and taxes the remaining real gain at a minimum rate of 30%. For example, a property bought for $500,000 with 20% inflation over the holding period would have an indexed cost base of $600,000, reducing the taxable gain on a $750,000 sale from $250,000 to $150,000.

Investors with property in family trust structures should urgently review their distribution strategies with a qualified adviser, as a new 30% minimum tax on trust distributions related to property investment income will apply from 1 July 2027. Both CPA Australia and the Tax Institute of Australia have flagged this as a priority advisory item for 2026-27.

Analyst modelling points to modest national property price softening of around 3-5%, with declines of up to 7% possible in Sydney suburbs with high investor concentrations. Industry groups including the REIA and Property Council of Australia have warned of upward rental pressure and tightening vacancy rates, though reform supporters argue new construction supply will offset this over time.