Citi Puts Memory Supply Above Chip Design in AI Stock Rankings

36 mins ago

A business founder selling a $1 million company today could lose more than $225,000 in after-tax proceeds compared to the regime that existed yesterday. That is the scale of what the 2026 Federal Budget, delivered on 12 May 2026, has set in motion. The Albanese Government replaced Australia’s 50% capital gains tax (CGT) discount with inflation indexation and imposed a 30% minimum effective tax rate on capital gains from 1 July 2027, the most consequential change to investment taxation since the Howard Government introduced the flat discount in 1999. What follows unpacks exactly how the new mechanics work, what the transitional rules mean for assets already held, and how much wealth different investor types stand to lose under the revised system.

Under the old system, an investor who held an asset for more than 12 months simply halved the nominal gain before adding it to taxable income. The replacement method adjusts the asset’s cost base upward by the inflation rate before calculating the taxable gain, so only the real, inflation-adjusted gain is taxed.

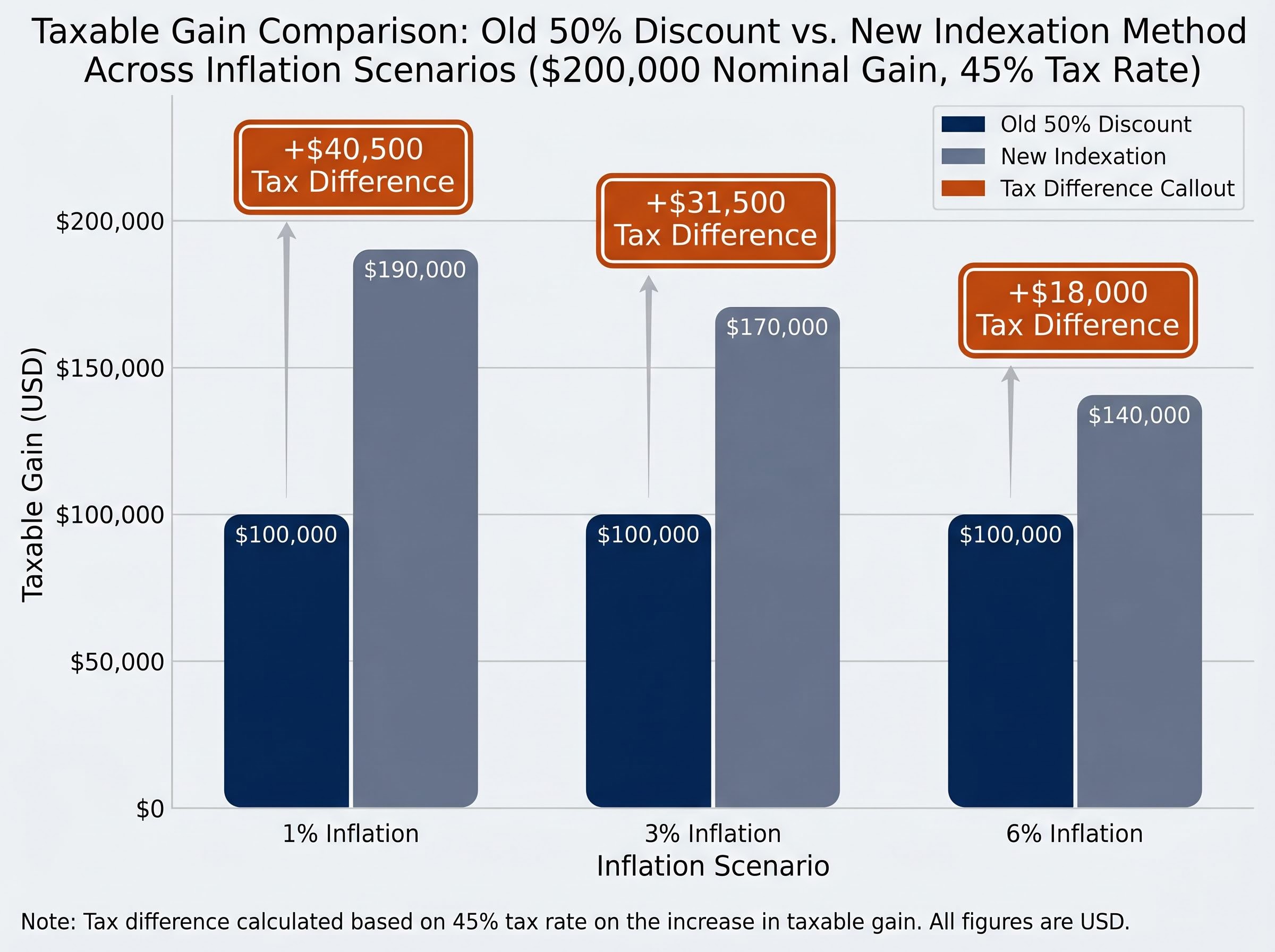

Consider a $500,000 asset purchased two years ago that sells for $700,000, producing a $200,000 nominal gain. Under the old 50% discount, the taxable gain was $100,000. Under inflation indexation at 2% annual inflation, the cost base rises to approximately $520,000, producing a taxable gain of roughly $180,000. The two methods converge at moderate inflation but diverge sharply at the extremes.

The indexation method’s real-world impact depends entirely on the Australian inflation environment: at the RBA’s current cash rate of 4.10% and headline CPI of 4.6% in the March 2026 quarter, the cost base adjustment under the new regime will be materially larger than the 1-2% scenarios modelled at Budget time.

The table below illustrates the divergence across three inflation scenarios for the same $200,000 nominal gain, taxed at the top 45% marginal rate.

| Inflation Rate (Annual) | Taxable Gain (Old 50% Discount) | Taxable Gain (New Indexation) | Tax Difference at 45% Rate |

|---|---|---|---|

| 1% | $100,000 | $190,000 | +$40,500 (investor pays more) |

| 3% | $100,000 | $170,000 | +$31,500 (investor pays more) |

| 6% | $100,000 | $140,000 | +$18,000 (investor pays more) |

A separate constraint operates alongside the indexation method: the 30% minimum effective tax rate on capital gains, effective from 1 July 2027. Whichever calculation produces the higher tax liability governs. For investors on lower marginal rates who previously benefited from the discount bringing their effective CGT rate well below 30%, this floor changes the equation regardless of the inflation environment.

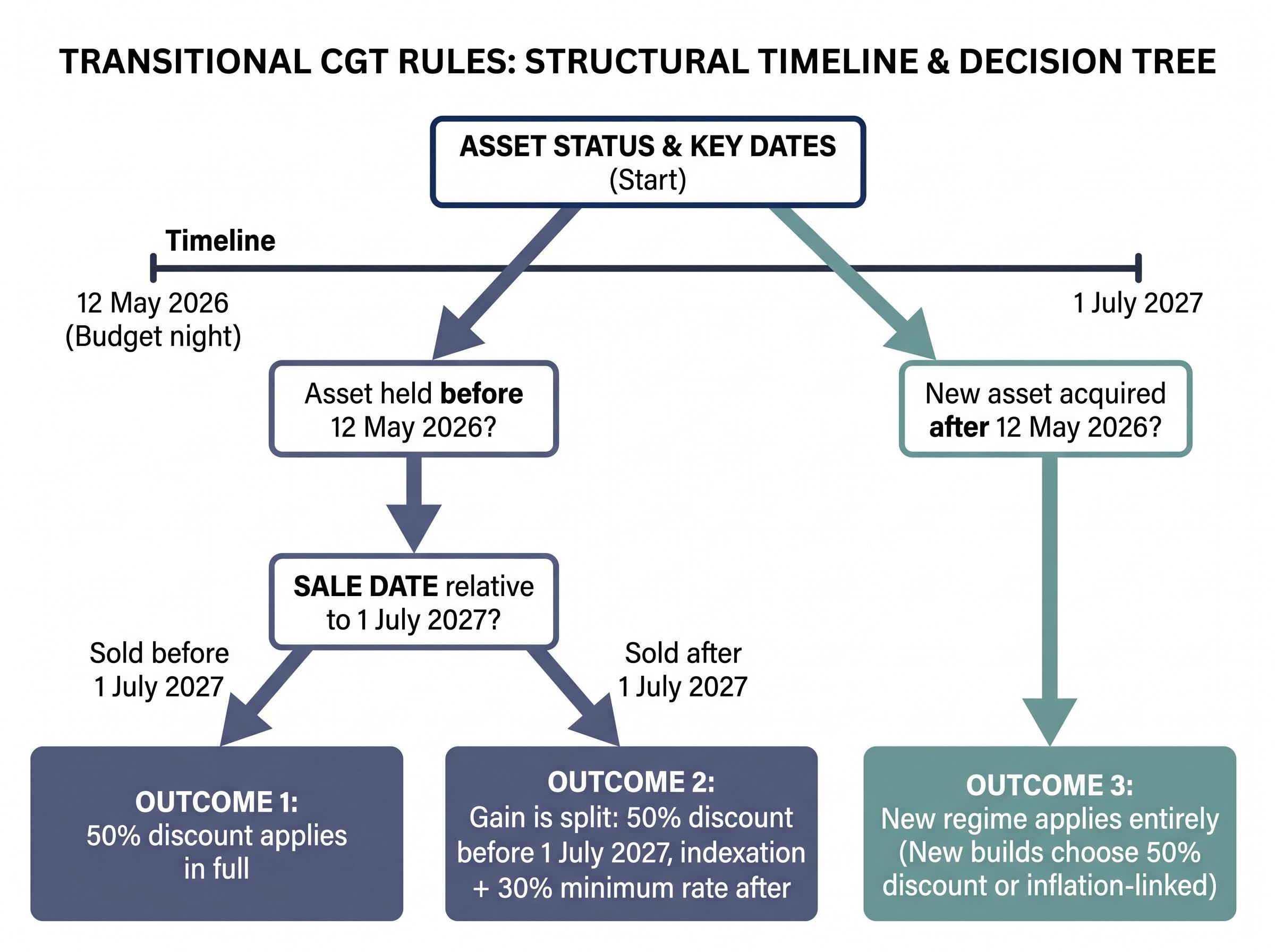

The immediate reassurance: assets held before Budget night (12 May 2026) are grandfathered. Gains accrued up to 1 July 2027 retain the 50% CGT discount. Only gains accruing after that date fall under the new indexed regime.

Three scenarios define the transition:

No valuation snapshot is required at the transition date. Instead, two methods are available to split the gain. The first is a formal valuation as of 1 July 2027, establishing a market value that separates pre-transition and post-transition gains. The second is the ATO time-apportionment formula, which divides the total gain proportionally based on how long the asset was held in each period.

A formal valuation tends to produce a more favourable outcome where an asset appreciated sharply in its early years and plateaued afterward, because the time-based formula assumes linear growth. ATO administrative guidance on the mechanics of either method has not yet been released as of Budget day; investors should monitor ATO.gov.au for details as they emerge.

The abstract percentages obscure what the reform actually costs in after-tax wealth. Analysis by Stockspot founder Chris Brycki, using the firm’s CGT calculator, models the impact across three investor types over a 10-year horizon, and the numbers escalate with the scale of the gain.

An ETF investor with a $100,000 portfolio faces an estimated $26,000 reduction in after-tax wealth. The driver is not a single tax event but the compounding effect of tax drag: higher annual tax on distributed gains reduces the capital available to compound in subsequent years.

The CGT drag on reactive trades compounds the problem beyond the single disposal event: every short-term realisation that forfeits the 12-month holding threshold, now combined with a higher effective rate under the new regime, adds a structural penalty that erodes the base available for subsequent compounding.

A property investor over the same horizon loses more than $50,000 in after-tax wealth. Property concentrates gains into fewer, larger disposal events, amplifying the impact of the higher effective rate at the point of sale.

The most exposed investor type is the business founder.

A business founder selling a $1 million company stands to lose in excess of $225,000 in after-tax proceeds under the new regime, according to Stockspot modelling. The 50% discount historically shielded a large nominal gain compressed into a single taxable event; its removal is felt most acutely where the gain is largest.

| Investor Type | Portfolio / Sale Value | Estimated After-Tax Wealth Loss | Key Driver of Loss |

|---|---|---|---|

| ETF investor | $100,000 | $26,000 | Compounding tax drag on annual distributions |

| Property investor | $100,000+ | $50,000+ | Concentrated gain at disposal |

| Business founder | $1,000,000 | $225,000+ | Large nominal gain in single taxable event |

The 50% discount entered the system in 1999 when the Howard Government replaced the original indexation method that had operated since CGT was introduced in 1985. Treasury’s argument for reverting is that the flat discount was structurally disconnected from actual economic gain.

Three criticisms shaped the policy case:

The Senate Select Committee on the CGT Discount, which reported in February 2026, is credited with shaping the grandfathered, non-retroactive design of the reform. Understanding this policy logic matters for durability: the reform is positioned as a structural correction rather than a revenue measure, which makes reversal politically harder for any future government to justify.

The new regime does not affect all assets equally. Some face materially higher tax drag; others gain a relative advantage.

| Assets Facing Higher Tax Drag | Assets With Relative Tax Advantage |

|---|---|

| Established investment property | Passive low-turnover ETFs |

| High-turnover active managed funds | Dividend-paying blue chips (franking credits) |

| Startups and venture investments | Superannuation contributions |

| Gold and cryptocurrency | Owner-occupied property (exempt) |

| Discretionary trust distributions (if confirmed) | Bonds and term deposits |

High-turnover active funds are particularly exposed because they distribute realised capital gains annually to unit holders regardless of whether the investor sold, amplifying tax drag under the new settings. Economists predict house price falls of up to 4% from the combined CGT and negative gearing reforms, according to the Australian Financial Review.

Superannuation retains concessional tax treatment but contributions are capped and capital remains largely inaccessible until preservation age. Pre-Budget CommBank modelling estimated the combined reforms at $25-30 billion in revenue over 10 years.

Superannuation’s concessional tax treatment is real, but CGT costs inside super funds are not always visible: pooled trust structures can transfer capital gains liabilities from exiting members to remaining members, creating drag that never appears in a headline fee figure and partially offsets the rate advantage the current article highlights.

Higher CGT creates an incentive to defer realising gains. Investors holding appreciated assets avoid selling to sidestep the tax event, concentrating portfolios and reducing reallocation to more productive uses. The policy contradiction is notable: the Government wants capital redirected toward new housing supply and productive business activity, yet higher effective CGT rates incentivise holding rather than selling and reinvesting.

Investors have just over 13 months before the new regime applies. Not every decision needs to be made today. The following framework sequences the priorities:

These reforms are announced but not yet law. Draft legislation and ATO guidance have not been published as of Budget day. Final details may change during parliamentary process. Investors should monitor Treasury.gov.au and ATO.gov.au for updates before making irreversible decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The central tension in the reform is unresolved. The Government argues it redirects capital toward productive uses and improves intergenerational equity. Critics counter that it reduces after-tax returns across equity investing, venture capital, and business formation, potentially reinforcing Australia’s structural productivity challenges. Both readings have evidence behind them, and neither will be settled by Budget night alone.

CommBank’s pre-Budget estimate pegged the combined CGT and negative gearing changes at $2 billion over four years and $25-30 billion over 10 years. The negative gearing restriction took effect from Budget night for new established property purchases. A trust distribution minimum 30% tax rate was announced, though its applicability to discretionary trusts remains unconfirmed in official Budget papers as of publication.

Three open legislative questions remain for investors to track:

The durable principle is straightforward: long-term, diversified, low-turnover investing in tax-advantaged structures becomes more important when the tax environment tightens around capital gains. The investors who understand the reform’s internal logic, and its open questions, are better positioned to adapt as the details are confirmed than those who react to headlines with irreversible portfolio changes.

Tax-efficient portfolio rebalancing becomes substantially more complex under the new settings: assets with embedded gains held before Budget night need to be evaluated against their post-transition gain trajectory before any reallocation decision is made, since selling prematurely to reset cost bases could trigger a larger taxable event than holding through the transition.

The 2026 Federal Budget replaces the existing 50% CGT discount for assets held more than 12 months with an inflation indexation method and imposes a 30% minimum effective tax rate on capital gains, both taking effect from 1 July 2027.

Assets held before Budget night on 12 May 2026 are grandfathered, meaning gains accrued up to 1 July 2027 still attract the 50% CGT discount; only gains accruing after that date fall under the new indexed regime.

Under inflation indexation, the asset's original cost base is adjusted upward by the annual inflation rate before the taxable gain is calculated, meaning only the real gain above inflation is taxed rather than simply halving the total nominal gain.

According to Stockspot modelling, an ETF investor with a $100,000 portfolio could lose around $26,000 in after-tax wealth, a property investor more than $50,000, and a business founder selling a $1 million company in excess of $225,000 in after-tax proceeds.

Investors should assess whether their existing assets are grandfathered, model the gain-split impact using the time-apportionment formula or a formal valuation, review superannuation contribution capacity, and wait for draft legislation before making structural changes to trusts or asset ownership.