Earnout Structures Explained Using a Live ASX Deal

4 hrs ago

Since 1999, any Australian who sold an investment asset held for more than a year paid tax on only half the capital gain. From 1 July 2027, that rule is gone.

The 2026-27 Federal Budget announced the most significant overhaul of Australia’s capital gains tax framework in a quarter century. The 50% CGT discount for individuals, trusts, and partnerships is being replaced by a CPI-based indexation model and a 30% minimum tax on real gains. For property investors, accountants, and anyone holding shares or managed funds, the practical implications are immediate and layered with complexity.

This article explains how the new system works mechanically, which assets are affected and which are not, what the transitional rules mean for assets already held, and what remains unresolved in the legislation. Readers will finish with a clear framework for understanding what changes on 1 July 2027 and what questions to put to their tax adviser before then.

The break is clean. From 1 July 2027, the 50% CGT discount for individuals, trusts, and partnerships is abolished. In its place, two new rules apply together:

“Investors will only pay tax on their real capital gain.” — 2026-27 Federal Budget factsheet

The government’s stated rationale is that the existing discount taxes nominal gains, including the portion driven purely by inflation, while indexation strips that inflation component out. Pitcher Partners described the announcement as a “seismic shift in the CGT and broader income tax landscape.” K&L Gates characterised it as “a substantial change… likely significantly increasing CGT for most investors.”

This is the most significant CGT reform since the discount was introduced in 1999. As at mid-May 2026, it remains at the proposal and consultation stage; no exposure draft legislation has been released.

The CGT discount removal sits alongside two other structural changes from the same Budget: together the three 2026 Budget reform pillars, covering the negative gearing ring-fence, the CGT overhaul, and a 30% minimum tax on discretionary trust distributions from July 2028, collectively reshape the after-tax calculus for every investor holding property or managed fund assets in Australia.

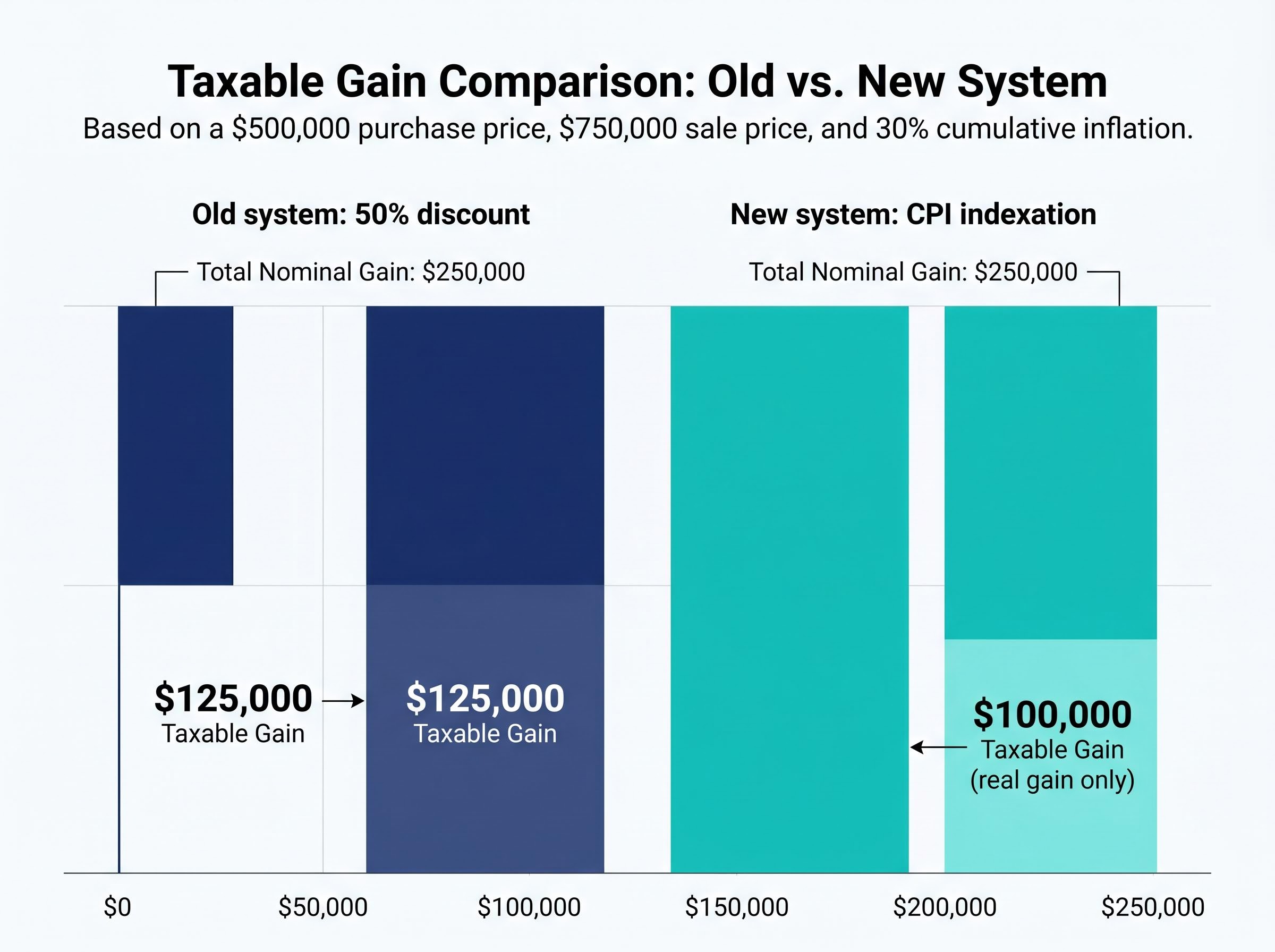

Under the new model, the original purchase price of an asset (the cost base) is adjusted upward using the Consumer Price Index (CPI) to reflect inflation over the holding period. The taxable gain is then the difference between this inflation-adjusted cost base and the sale price, not the difference between the original price and the sale price.

Consider an illustrative example. An investor buys an asset for $500,000 and sells it years later for $750,000, during which time cumulative inflation reached 30%.

| Component | Old system (50% discount) | New system (CPI indexation) |

|---|---|---|

| Purchase price | $500,000 | $500,000 |

| CPI-adjusted cost base | Not applicable | $650,000 (30% inflation factor) |

| Sale price | $750,000 | $750,000 |

| Nominal gain | $250,000 | $250,000 |

| Taxable gain | $125,000 (50% discount applied) | $100,000 (real gain only) |

In this scenario, indexation produces a lower taxable gain than the 50% discount. That outcome depends on the inflation rate relative to the asset’s price growth, a point explored in the next section.

The 30% minimum tax then applies to the real gain. Investors on a marginal rate above 30% pay their marginal rate as usual. Lower-income investors who would otherwise pay less than 30% pay the 30% floor instead. Income support and Age Pension recipients are exempt from the floor but remain subject to indexation.

Several mechanical details remain unresolved. Pitcher Partners noted that “precise details of the proposed indexation were not made available in the Government’s announcement.” Outstanding questions include:

Australia used cost base indexation before 1999, so the concept is not new. The difference is that the pre-1999 system had no 30% floor, making the proposed model a hybrid without a direct historical precedent.

Australia used cost base indexation before 1999, and the ATO cost base indexation guidance from that era establishes the foundational mechanics the new regime is adapting, including how the CPI factor is applied to the original purchase price to produce an inflation-adjusted cost base.

If a property rises from $500,000 to $750,000 over a decade, the nominal gain is $250,000. But if inflation accounts for $150,000 of that increase, the investor’s real gain, the actual increase in purchasing power, is only $100,000. Without indexation, tax is levied on the full $250,000, including the $150,000 that simply kept pace with rising prices.

The dynamic mirrors bracket creep in wage taxation. Just as a worker can be pushed into a higher tax bracket by inflation-driven pay rises that do not increase real purchasing power, an investor can face tax on gains that are purely inflationary. In both cases, the government collects additional revenue without the taxpayer being genuinely better off.

Economists broadly support the principle of taxing only real gains. Critics of the current reform, however, argue that the 30% minimum floor partially undermines the equity argument. An investor on a marginal rate of 19% would, under indexation alone, pay 19% on their real gain. The floor forces them to pay 30%, a rate that exceeds their actual marginal rate on real income.

The answer depends on inflation, asset price growth, and location. PropTrack analysis found that over the past decade, approximately 27% of properties that generated a capital gain would have faced a smaller taxable gain under indexation than under the 50% discount. That share peaked at 39% in Q4 2023, roughly 12 months after Australia’s headline inflation reached its cyclical high, the minimum qualifying period for a CGT discount.

Even in the low-inflation period before the pandemic, approximately 26% of investor gains would have attracted a lower taxable amount under indexation.

City-level variation is notable. Melbourne has seen a growing share of sales where indexation would have produced a lower taxable gain, reflecting more moderate price growth against sustained inflation. Brisbane has moved the other way, with strong capital growth widening the advantage of the 50% discount. Sydney’s advantage from the discount has diminished in recent years as price growth moderated.

The implication is straightforward: indexation favours investors in high-inflation, modest-growth environments; the 50% discount favours investors in strong capital growth, low-inflation periods. The relative benefit depends heavily on when the asset was purchased, where it is located, and what inflation was doing over the holding period.

The new indexation and 30% floor apply broadly to assets held by individuals, partnerships, and trusts for 12 or more months. The following table summarises asset scope and key conditions.

| Asset type | In scope from 1 July 2027 | Key condition or exception |

|---|---|---|

| Existing investment property | Yes | 12-month hold requirement |

| New residential build | Yes | Can elect 50% discount on first disposal |

| Shares and managed funds | Yes | 12-month hold requirement |

| Pre-CGT assets (acquired before 19 September 1985) | Yes, from 1 July 2027 | Deemed cost base at market value on 1 July 2027 |

| Principal place of residence | No | Main residence exemption unchanged |

| Corporate entities | Largely unaffected | Already taxed at or above 30% |

The new-build exception is the one significant carve-out. Investors in newly built residential properties can elect to use either the existing 50% CGT discount on first disposal or the new indexation plus 30% minimum tax. This functions as a deliberate incentive to support new housing supply and aligns with the government’s broader affordability agenda.

Pre-CGT assets, those acquired before 19 September 1985 and previously fully exempt, will become taxable from 1 July 2027, but only on gains arising after that date. A deemed cost base equal to market value at 1 July 2027 will apply, preserving the exemption for prior gains. Pitcher Partners stressed that “the market value adopted at 1 July 2027 will directly determine the amount of any future taxable gain” and warned that valuation disputes will be a focal point, particularly for illiquid or unique assets.

Several grey areas remain unresolved:

The transitional framework creates three distinct time bands, each producing a different tax outcome:

This bifurcation creates live planning questions. Accounting firms are already advising clients with large embedded gains to review whether accelerating disposal before July 2027 would lock in more favourable treatment under the 50% discount. Some advisers are also recommending deferring loss realisation to offset future real gains under the new system, though loss treatment rules have not yet been confirmed.

Property investors evaluating whether to sell before 1 July 2027 must also account for the negative gearing ring-fence that took effect from 12 May 2026 for newly acquired established properties, a separate policy change that compounds the after-tax return shift for leveraged residential investors.

“Complex transitional measures to come.” — K&L Gates, May 2026

For complex situations, including start-up equity, private business exits, and trust structures, the prevailing recommendation is to wait. With no exposure draft legislation or ATO guidance released as at mid-May 2026, the detail that would inform restructuring decisions simply does not yet exist.

The direction of the reform is set. The detail that determines individual tax outcomes is still being written. The following table summarises the key unresolved issues, why they matter, and their expected resolution path.

| Unresolved issue | Why it matters | Expected resolution path |

|---|---|---|

| CPI indexation method | Quarterly vs annual calculation affects gain size | Exposure draft legislation |

| Capital loss treatment (nominal vs real) | Determines offset value of realised losses | Exposure draft legislation |

| Trust and managed fund streaming | Affects whether 30% floor applies at trust or beneficiary level | Exposure draft legislation and ATO guidance |

| Pre-CGT asset valuation methodology | Determines the deemed cost base for assets entering the CGT net | ATO ruling or safe-harbour rules |

| Small business CGT concession interaction | Affects eligibility for 15-year exemption and active asset reduction | Exposure draft legislation |

| Start-up and founder concessions | Founders cannot index sweat equity; lose 50% discount without carve-out | Government consultation (promised, not scheduled) |

The start-up concern is particularly pointed. K&L Gates warned that the change “is a major concern for start-ups (including founders and those given equity in start-ups as compensation for less-than-market wages (or none at all)).” Indexation rewards those who contribute capital; founders and employees who contribute labour, time, and ideas cannot index a non-cash cost base. Without a targeted carve-out, they lose the 50% discount with no offsetting benefit.

On property markets, PropTrack analysis suggests the policy alone is not expected to materially shift property prices or rental levels in isolation. Supply-demand fundamentals remain unchanged. The anticipated near-term effect is a modest softening in established property demand and marginal growth in new-build investment activity, consistent with the government’s stated housing supply objectives.

Higher effective CGT rates also create a lock-in effect on portfolio reallocation, discouraging investors from selling appreciated assets even when better opportunities exist elsewhere, which may partially undermine the government’s stated goal of redirecting capital toward productive uses including new housing supply.

Both Pitcher Partners and K&L Gates explicitly recommend waiting for exposure draft legislation before making major restructuring decisions, particularly for trust structures and business exits.

The 50% CGT discount is being replaced by CPI indexation plus a 30% minimum tax from 1 July 2027. That policy direction is locked in, even though the legislation has not yet been released.

Investors holding appreciated assets, particularly those with pre-CGT holdings, large unrealised gains in established property, or equity in start-ups, have a window before July 2027 that warrants a portfolio review conversation with a qualified tax adviser. The transitional rules create genuine timing considerations that differ by asset class and holding period.

Exposure draft legislation and ATO guidance, when released, will resolve the mechanical questions: CPI calculation method, loss treatment, trust rules, and founder concessions. Monitoring these as they emerge will be the difference between informed planning and reactive decision-making.

For investors who want to understand how the broader market is repricing in response to these changes, our deep-dive into ASX sectoral rotation under the new CGT regime covers the expected shift toward fully franked income stocks including banks, telcos, infrastructure, and A-REITs, and examines the specific strategies advisers are prioritising across the 14-month window before 1 July 2027.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These policy settings are subject to change as legislation is drafted and finalised.

Readers should consult a registered tax adviser before making any disposal or restructuring decisions based on the announced changes.

From 1 July 2027, the 50% CGT discount for individuals, trusts, and partnerships is abolished and replaced with CPI-based cost base indexation plus a 30% minimum tax on real capital gains, meaning investors pay their marginal rate or 30%, whichever is higher.

Under CPI indexation, the original purchase price of an asset is adjusted upward by the Consumer Price Index over the holding period, so taxable gains are calculated only on the real increase in value above inflation rather than on the full nominal gain.

Shares, managed funds, existing investment properties, and most other assets held by individuals, partnerships, and trusts for 12 or more months are in scope, while the principal place of residence retains its full main residence exemption and newly built residential properties can elect the old 50% discount on first disposal.

Gains on assets purchased before 1 July 2027 but sold after that date are bifurcated, with the portion of the gain attributable to the pre-2027 holding period taxed under the old 50% discount rules and the portion attributable to the post-2027 period taxed under the new indexation and 30% minimum tax regime.

Accounting firms are already advising clients with large embedded gains to review whether accelerating a disposal before July 2027 would produce a more favourable tax outcome, but leading advisers including Pitcher Partners and K&L Gates recommend waiting for exposure draft legislation before making major restructuring decisions, as key mechanical details remain unresolved.