Why 30% Recession Odds Are Harder to Trade Than 60%

13 mins ago

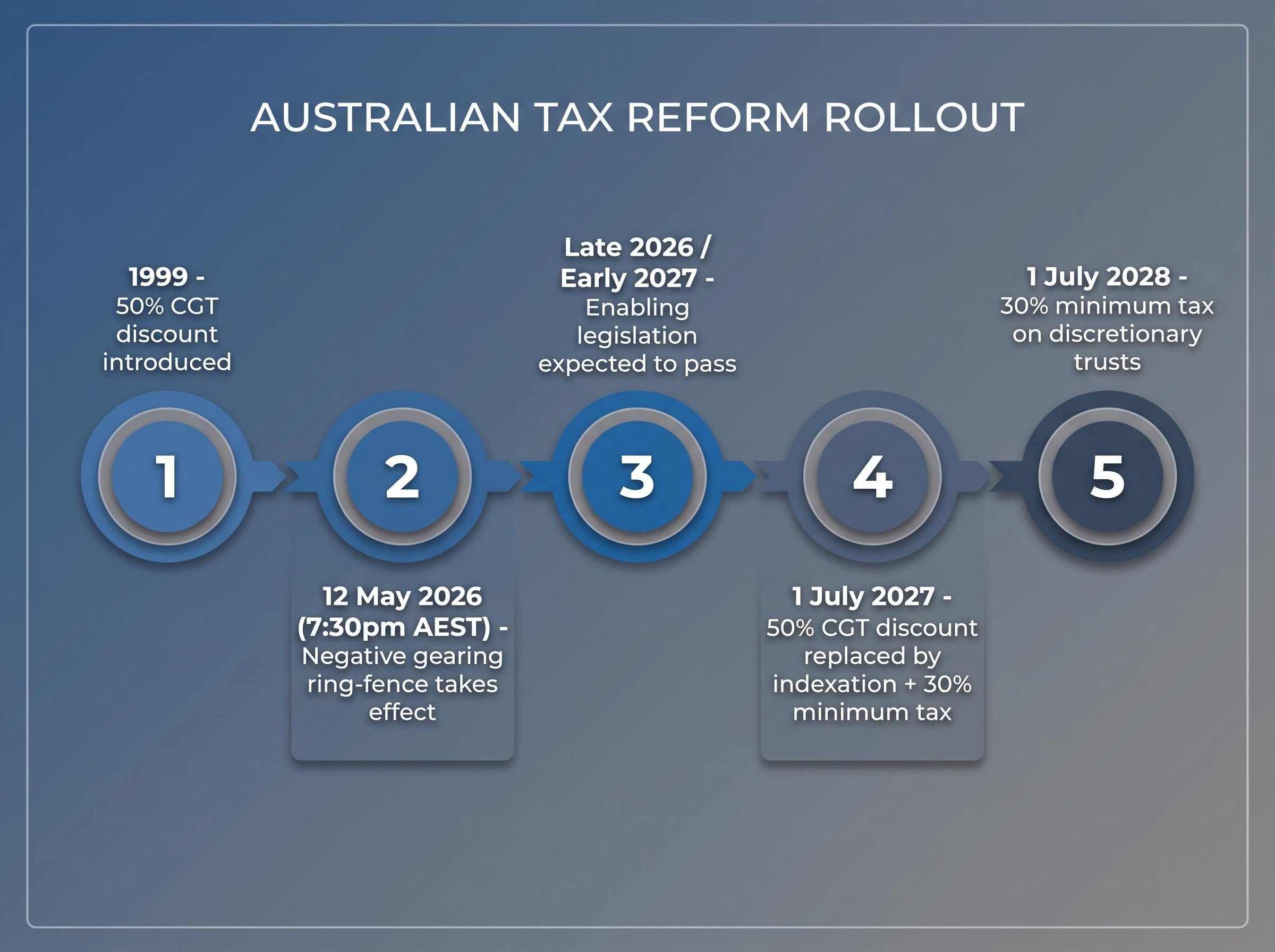

At 7:30pm AEST on 12 May 2026, the Federal Budget locked in the acquisition timestamp that now divides Australian property investors into two distinct tax regimes. Those who settled on established residential dwellings before that moment retain negative gearing concessions. Those who did not face a fundamentally different set of rules for the life of their assets. The negative gearing ring-fence is only the first of three reform pillars. A replacement of the 50% capital gains tax discount with cost base indexation and a 30% minimum tax takes effect from 1 July 2027, and a 30% minimum tax on discretionary trusts follows in July 2028. Together, the measures represent the most consequential restructuring of Australian investment taxation since the CGT discount was introduced in 1999. None of the three pillars are yet law, but the direction of travel is clear. This analysis explains what each reform does, who it affects and when, how property markets and ASX-listed equities are expected to respond, and what investors can do before the most significant change takes effect.

Three separate reform measures were announced on Budget night. Each operates on its own timeline, applies to different asset classes, and carries its own grandfathering logic. Conflating them produces incorrect planning conclusions.

| Reform Pillar | Effective Date | What Changes | Grandfathering / Exceptions |

|---|---|---|---|

| Negative gearing ring-fence | 12 May 2026 (7:30pm AEST) | Rental losses on established residential properties acquired after the timestamp cannot be offset against wage and salary income | Existing holdings acquired before timestamp retain full concessions; new residential builds remain fully eligible |

| CGT discount replacement | 1 July 2027 | 50% CGT discount abolished for gains accruing after this date; replaced by cost base indexation plus a 30% minimum tax on real gains | Gains apportioned: pre-2027 portion retains 50% discount eligibility; post-2027 portion subject to new regime |

| Discretionary trust minimum tax | 1 July 2028 | 30% minimum tax on discretionary trust distributions | Scope of exclusions (small business, testamentary trusts) subject to legislative drafting |

Enabling legislation for all three measures is expected to pass Parliament in late 2026 or early 2027. Until that occurs, a residual layer of uncertainty surrounds the precise mechanics, particularly around the CGT apportionment methodology and pre-CGT asset treatment.

The 2026-27 Budget speech delivered by the Treasurer confirmed all three reform pillars simultaneously: the negative gearing ring-fence taking effect at 7:30pm AEST on 12 May 2026, the replacement of the 50% CGT discount with cost base indexation and a 30% minimum tax from 1 July 2027, and the 30% minimum tax on discretionary trust distributions from July 2028.

The limitation is specific. Losses on established residential properties acquired after 7:30pm AEST 12 May 2026 cannot be claimed against salary income. The losses are ring-fenced, deductible only against future rental income or capital gains from the same property.

New residential builds acquired after the same date retain full negative gearing concessions. The distinction is deliberate: the policy channels investor capital toward new housing supply rather than existing stock.

The negative gearing ring-fence operates with a precision that surprises many investors: only established residential dwellings acquired after the 7:30pm timestamp are caught, while new builds acquired on the same night or any night thereafter retain full deductibility against all income sources, including salary.

The 50% CGT discount is replaced, for gains accruing after 1 July 2027, by a system that adjusts the cost base for inflation and then applies a 30% minimum tax on the resulting real gain. For long-held assets sold after this date, the gain will be apportioned between the pre-2027 period (which retains discount eligibility) and the post-2027 period (subject to the new regime).

The apportionment mechanism is the most technically complex element. The ATO has not yet issued a Law Companion Ruling on the acceptable valuation methodology for the 1 July 2027 boundary, and guidance is expected closer to the reform date.

The negative gearing ring-fence attracts the most attention. The CGT overhaul carries the greater financial consequence.

The reason is structural. Existing property investors are grandfathered under the negative gearing changes. An investor who held an established dwelling before 12 May 2026 retains the full ability to offset rental losses against their salary. The ring-fence only affects future acquisitions of established stock. For the existing investor base, the near-term impact is marginal.

No equivalent grandfathering exists for capital gains accruing after 1 July 2027. Every investor holding every asset class, not only residential property, faces a different after-tax outcome on gains accumulated from that date forward.

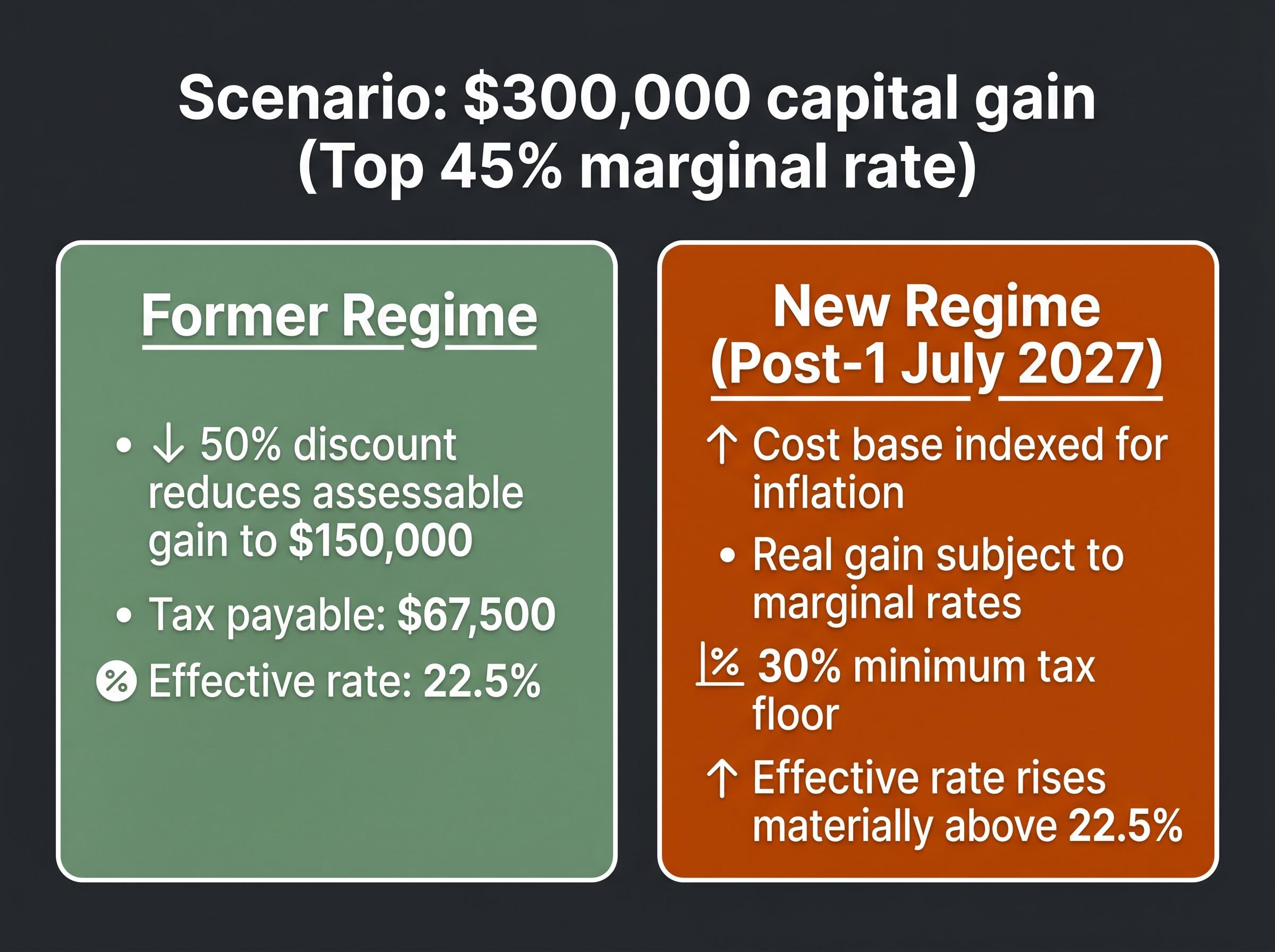

The arithmetic makes the difference concrete. Consider a $300,000 capital gain realised by a taxpayer on the top 45% marginal rate:

In a low-inflation environment returning toward the RBA’s 2-3% target band, the CPI indexation uplift on any given year’s cost base will be modest, meaning the 30% minimum tax floor is more likely to activate than the headline framing of the reform suggests, particularly for assets held for shorter post-2027 periods.

The 50% CGT discount has underpinned retail investment strategy since its introduction in 1999. Its removal resets the after-tax calculus for every long-term asset holder in the country.

Major bank economists at NAB, CBA, ANZ, and Westpac are broadly aligned: the CGT discount removal, not the negative gearing ring-fence, is the primary behavioural driver for investors over the medium term.

Understanding why these reforms constitute a structural shift, rather than a routine tax adjustment, requires understanding what the mechanisms were worth in combination.

Negative gearing allows a property investor to deduct rental losses (where mortgage interest and expenses exceed rental income) against all other income, including salary. There is no formal cap on the deduction. An investor earning $200,000 in salary and generating a $30,000 rental loss could reduce assessable income to $170,000, saving tax at their marginal rate every year the property ran at a loss.

The 50% CGT discount, introduced in 1999 under the Ralph Review of business taxation, replaced the prior cost base indexation system. It meant that when the investor eventually sold the property at a gain, only half that gain was assessable. The effective tax rate on the sale, even for a top-rate taxpayer, was 22.5%.

The combined effect created a dual subsidy:

This architecture made residential property a uniquely tax-efficient asset class. Property investors now make up approximately one-third of new mortgage demand nationally, according to ABS data to Q1 2026. The reforms dismantle both sides of this dual subsidy simultaneously.

The behavioural sequence is already partially visible. In the weeks before Budget night, agents and mortgage brokers reported a surge in investor enquiries and last-minute contracts for established properties, brought forward before the 7:30pm 12 May timestamp.

The expected timeline runs in four phases:

No quantitative post-announcement investor behaviour data is yet available. May-June 2026 ABS housing finance releases represent the first data milestone.

A higher effective CGT rate on exit also produces a lock-in effect: investors facing a materially larger tax bill on sale have a financial incentive to hold assets longer than they otherwise would, which can reduce portfolio liquidity and suppress the transaction volumes that the property market relies on for price discovery.

Competing views persist. PIPA and the REIA warn that ring-fencing losses for established dwellings will reduce rental supply in middle-ring suburbs and push vacancy rates lower. The HIA describes the restriction as correcting a distortion that favoured buying existing stock over financing construction. Underlying population growth and supply constraints will partially offset demand withdrawal, particularly outside Sydney and Melbourne.

Analyst commentary flags ASX-listed residential developers, including Stockland, Mirvac, Lendlease, Peet, Cedar Woods, and AVJennings, as potential beneficiaries of investor demand being redirected toward new supply. CFOs and CEOs have described the measures as “supportive of new supply” in media interviews, while emphasising that construction costs and planning constraints remain binding factors.

Broker research also references building materials producers (Boral, CSR, Brickworks) as potential medium-term volume beneficiaries if new dwelling approvals accelerate.

No ASX-listed company has revised earnings guidance to quantify these effects as at mid-May 2026. The equity market discussion remains at the broker and analyst level, not yet reflected in board-level, ASX-filed guidance revisions.

The window between now and 1 July 2027 is the most consequential planning period for Australian investment taxation in a quarter-century. Four actions, in priority order, define the framework:

Investors exploring how to reposition portfolios across property, equities, REITs, and superannuation will find our dedicated guide to which asset classes win under the new tax settings, which models after-tax wealth outcomes across a 10-year horizon and identifies passive ETFs and accumulation-phase super as the structurally advantaged positions under the 2026 regime.

Tax advisers are recommending clients wait for draft legislation and ATO guidance before executing complex cost-base reset strategies. “Wash sale” approaches (selling then rapidly repurchasing the same asset to reset cost base) carry a known Part IVA anti-avoidance risk, and most firms are counselling caution until the legislative detail is finalised.

The three reform pillars, taken together, dismantle the incentive architecture that made buy-and-hold residential property the default Australian wealth-building strategy. The near-term loss deduction advantage is ring-fenced. The long-term capital gain concession is being replaced. The trust distribution efficiency is being taxed at a 30% floor.

Genuine uncertainty remains. The measures are not yet law. The Federal Opposition has signalled intent to oppose or reverse the CGT discount removal and the discretionary trust minimum tax, though no formal reversal policy has been articulated.

The political centre of gravity may not favour full restoration of pre-2026 settings. The Greens and several crossbenchers are pushing for even stronger measures on investor taxation, suggesting the final legislative form may soften at the edges but not reverse direction.

The combined legislative timeline runs through July 2028, meaning investors face at least two years of structural uncertainty before the full regime is in place. Key technical details, including the CGT apportionment methodology, pre-CGT asset treatment, and super fund interactions, remain unresolved.

Yet the direction is clear. Investor portfolios built around the dual subsidy of negative gearing and the 50% CGT discount need reassessment regardless of how the margins resolve. Those who wait for complete certainty before engaging professional advice may find the most valuable planning options have already closed.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These measures are announced but not yet legislated; final legislative form may differ from current Budget announcements. Financial projections and behavioural expectations discussed in this analysis are subject to change based on market developments, legislative amendments, and regulatory guidance.

The negative gearing ring-fence means that rental losses on established residential properties acquired after 7:30pm AEST on 12 May 2026 can no longer be offset against wage or salary income. Instead, those losses are deductible only against future rental income or capital gains from the same property. New residential builds acquired after that date retain full negative gearing concessions.

From 1 July 2027, the 50% capital gains tax discount is abolished for gains accruing after that date and replaced by a system that adjusts the cost base for inflation, then applies a 30% minimum tax on the resulting real gain. Gains on assets held across the boundary will be apportioned, with the pre-2027 portion retaining the 50% discount and the post-2027 portion subject to the new regime.

Investors who settled on established residential dwellings before 7:30pm AEST on 12 May 2026 retain full negative gearing concessions for the life of those assets. Only established residential properties acquired after that precise timestamp are caught by the ring-fence.

Advisers including Ashurst, KPMG, and DLA Piper recommend four actions: segmenting portfolios by likely disposal timeline, obtaining formal market valuations on long-held assets to establish the apportionment boundary, assessing whether to dispose of highly appreciated assets before the CGT regime changes, and reviewing discretionary trust structures ahead of the 30% minimum tax arriving in July 2028.

From 1 July 2028, a 30% minimum tax will apply to distributions from discretionary trusts, reducing the tax efficiency of using family trusts to hold property or investment assets. The precise scope of exclusions, such as for small business or testamentary trusts, is still subject to legislative drafting, and advisers are actively modelling whether companies or fixed trusts may be more efficient structures under the new regime.