How ASX’s CHESS Overhaul Became a $250M Governance Failure

23 hrs ago

An investor pulls up ANZ‘s share price, runs a price-to-earnings calculation, and checks the dividend yield. The numbers suggest the stock is cheap relative to its sector. The question that follows determines whether the analysis produces a disciplined investment decision or an expensive mistake.

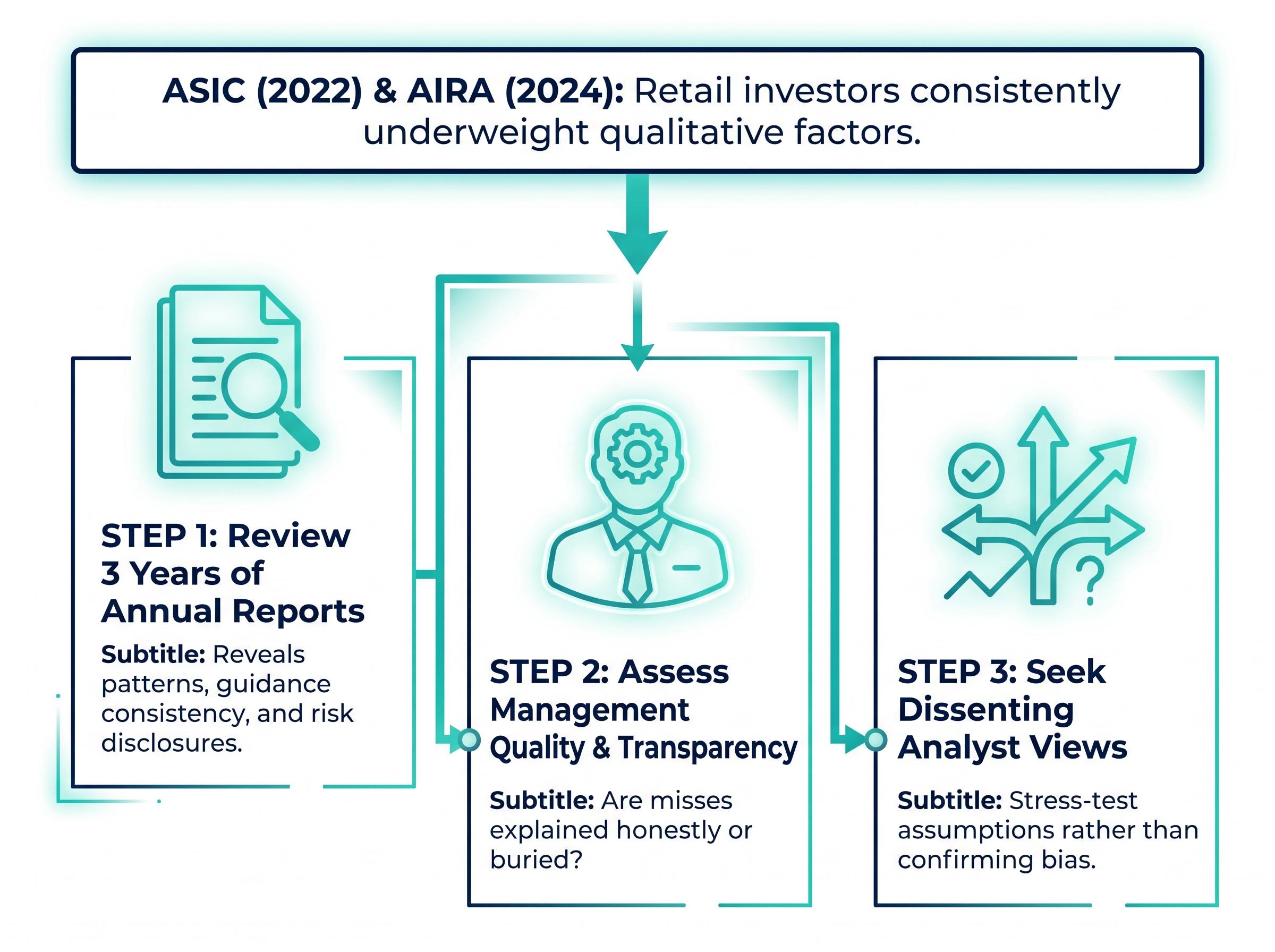

ASX bank stocks collectively account for roughly one-third of the domestic market by capitalisation and remain the most widely held equity category among Australian retail investors. Yet research from ASIC (REP 735, 2022) and the Australian Investors’ Relation Association (AIRA, 2024) consistently finds that retail investors underweight qualitative factors relative to their actual importance in driving outcomes. The numbers get the attention; the context behind them often does not.

This guide covers how the main quantitative valuation tools work (PE, P/B, DDM, DCF), what makes them particularly relevant or limited for bank stocks, and what additional research steps are non-negotiable before acting on any number the models produce. The reader will leave with a practical framework, not a definition list.

The appeal of quantitative valuation metrics is real. A PE ratio can be calculated in seconds, compared across peers in a spreadsheet, and tracked over time with minimal effort. For an investor screening the Big Four, the speed and comparability of these tools are genuine advantages.

The problem is that those same properties make the numbers dangerous when used without context. Bank earnings are sensitive to net interest margins, credit cycles, remediation charges, and regulatory capital changes. A reported EPS figure can be temporarily flattering in a benign credit environment or temporarily depressed by a one-off legal provision. The number is real; its durability is not guaranteed.

Consider ANZ, trading at approximately $34.57 with FY24 EPS of $2.15. That produces a PE of 16.1x against a sector average of roughly 17x, implying a sector-adjusted fair value of approximately $37.18 per share. On paper, it looks cheap.

The experienced investor’s instinct, the one captured in the persistent community shorthand “ANZ looks cheap, but what’s the catch?”, is correct. A low PE or high dividend yield is a prompt for further investigation, not a conclusion.

The PE ratio, P/B, and return on equity that appear throughout any bank stock analysis are part of a broader toolkit; the fundamental analysis metrics that underpin each of these ratios carry specific interpretive rules that determine whether a high or low reading is meaningful in context.

The signals that look attractive and the questions they should trigger:

According to ASIC REP 735 (2022), retail investors routinely underweight qualitative factors relative to their importance in actual investment outcomes, relying instead on simplified heuristics such as headline yield and brand familiarity.

Each of the four core valuation methods does a different job, and understanding them in combination produces a richer picture than any single metric.

Price-to-Earnings (PE) compares share price to earnings per share. It is the fastest comparative tool for ASX banks, but earnings distortions from remediation charges, net interest margin shifts, or one-off legal costs can make a reported PE misleading in any given period.

Price-to-Book (P/B) compares market capitalisation to net asset value. For banks, where the balance sheet is the business, a P/B below 1 signals that the market has concerns about asset quality or capital adequacy rather than offering a simple bargain.

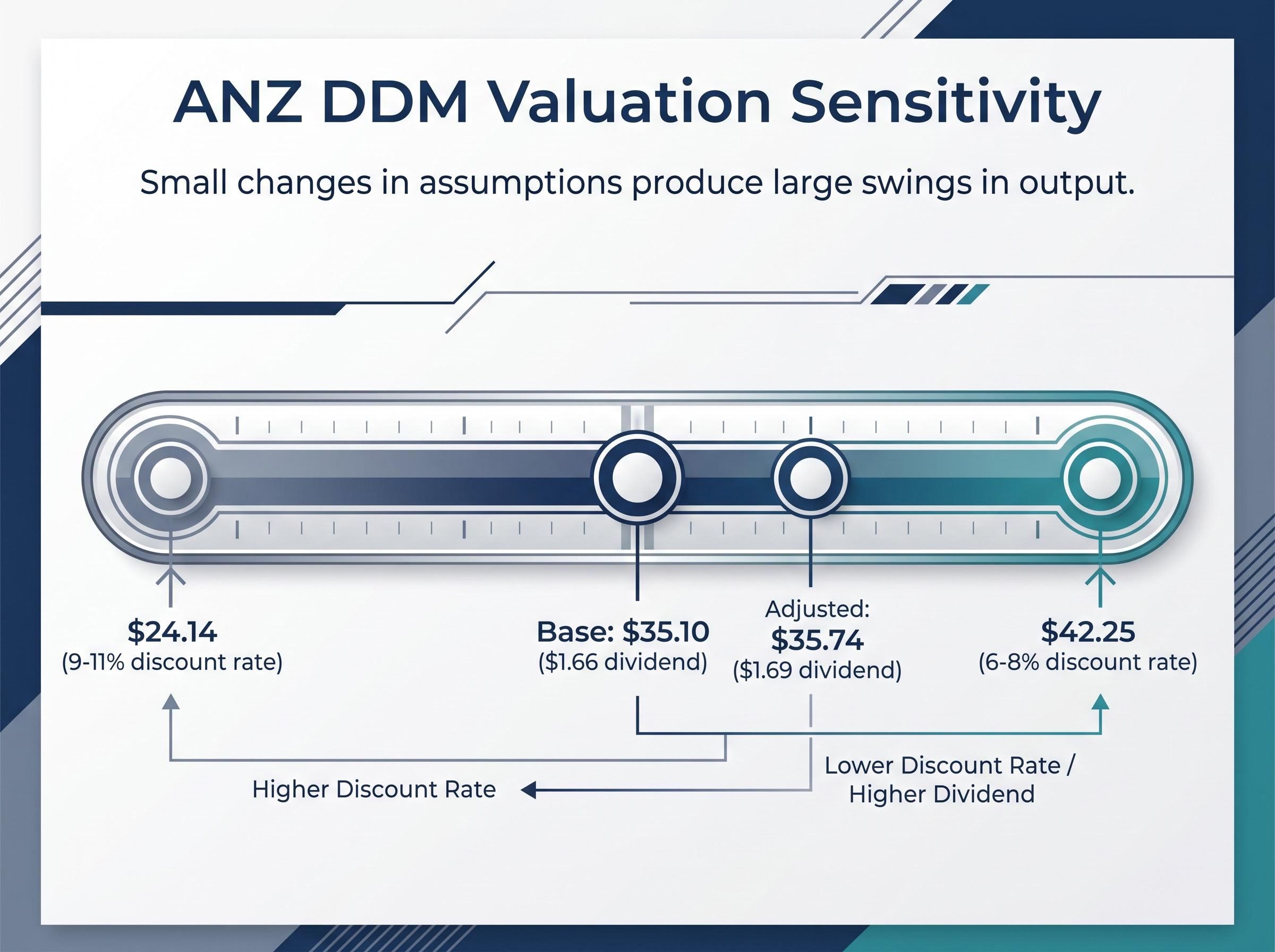

Dividend Discount Model (DDM) values a stock as the present value of its future dividends. Given the high payout ratios of Australian banks, DDM is especially relevant for this sector. ANZ‘s DDM outputs illustrate the sensitivity: a base valuation of $35.10 using a $1.66 dividend, an adjusted valuation of $35.74 using $1.69, and a matrix range spanning from $24.14 (at a 9-11% discount rate) to $42.25 (at a 6-8% discount rate). Small changes in assumptions produce large swings in the output.

The sensitivity of DDM outputs to small changes in discount rate assumptions is not unique to ANZ; DDM application to ASX income stocks more broadly shows that the valuation range produced by shifting the discount rate even two percentage points often exceeds the current share price itself, which is why the model functions best as a boundary-setter rather than a precise target.

Discounted Cash Flow (DCF) estimates intrinsic value by discounting future cash flows. For banks, it is more complex than for industrial companies because the balance sheet is the business; free cash flow calculations must be adapted to equity cash flows or dividends rather than free cash flow to the firm.

Method selection is itself a judgement call. EV/EBITDA is less applicable to banks but standard for mining stocks like BHP (ASX: BHP), where commodity cycles dominate. Forward PE is preferred for growth sectors, as with WiseTech Global (ASX: WTC), where expected earnings growth matters more than trailing figures.

| Method | Best Suited To | Key Limitation for Banks |

|---|---|---|

| PE | Quick peer comparison | Earnings distorted by credit cycles and one-off charges |

| P/B | Asset-heavy businesses | Book value may not reflect true loan quality |

| DDM | High-payout dividend stocks | Fragile when dividends are not genuinely sustainable |

| DCF | Intrinsic value estimation | Cash flow definition is complex for financial institutions |

A practical step-by-step process ties these tools together:

These two factors form the specifically Australian layer that makes a direct comparison to international bank valuations misleading. They are not optional fine print; they are material inputs to the numbers themselves.

Dividend imputation, the franking credit system, means that fully franked dividends carry a tax credit representing company tax already paid. For superannuation funds and low-income investors, those credits can be refunded in full, making the effective yield meaningfully higher than the headline cash yield.

When running a DDM on an ASX bank stock, gross yield (including the franking credit) should be the input for eligible investors, not the cash yield alone. The ATO provides guidance on how imputation credits are calculated and claimed, and the difference between gross and cash yield can be material enough to shift the valuation output.

Running a franking credit calculation using the standard 30/70 formula, where the credit equals the cash dividend multiplied by 30 and divided by 70, can shift the effective yield input for a DDM by enough to move the valuation output by several dollars per share for pension-phase investors.

APRA‘s “unquestionably strong” capital benchmarks, introduced following the Royal Commission, raised the minimum capital base Australian banks must hold. Higher capital requirements directly constrain return on equity: more capital held against the same asset base means lower returns per dollar of equity.

APRA’s unquestionably strong capital framework sets out the specific capital benchmarks Australian authorised deposit-taking institutions must meet, establishing the structural constraint on ROE that makes direct comparisons between Australian and international bank P/B multiples systematically misleading.

This has a direct effect on DDM and P/B analysis. A bank required to hold more capital may structurally earn lower ROE, which in turn justifies a lower P/B multiple. A lower P/B for an Australian bank relative to an international peer may partially reflect genuine regulatory constraint rather than mispricing.

Most retail investors can access a PE ratio in two seconds. The competitive advantage for any investor willing to do more sits in the qualitative layer. The question is what “doing more” actually looks like in practice.

According to the AIRA (2024) report on retail investor participation and engagement, a significant proportion of retail investors buy based on familiarity or a “defensive” perception rather than thorough due diligence, a pattern that qualitative analysis is specifically designed to interrogate.

The ASX Australian Investor Study (2023) reinforced this finding, showing that retail investors tend to treat large, familiar companies as inherently safe without conducting deeper analysis.

The ASX Australian Investor Study reinforces the ASIC findings at scale, showing that a substantial share of retail investors treat large, recognisable companies as inherently lower risk without conducting the deeper balance sheet and governance analysis that would justify that assumption.

Three steps turn qualitative research from an abstract concept into a concrete weekend task:

Resources such as ASIC MoneySmart and the ASX Education Centre provide accessible starting points for investors new to fundamental research.

The four major Australian banks trade on broadly similar quantitative metrics, yet they carry meaningfully different qualitative profiles. Each illustrates a distinct lesson.

ANZ screens well on valuation metrics but carries execution risk that the market prices in as a discount. Analysts have consistently focused on capital allocation discipline, strategic communication consistency, and whether operational improvement is sustained rather than promised. The lesson: a low multiple may be accurate rather than an opportunity.

NAB occupies a middle ground. Commentary tends to focus on whether the business banking franchise generates consistent returns and whether strategic direction is producing durable advantages. “Adequate but not compelling” is itself a qualitative finding, and the market prices it accordingly.

CBA trades on a higher multiple than peers, and analysts frequently justify that premium through franchise strength, technology investment, execution consistency, and management communication quality. The qualification matters: a premium multiple means the margin for error is smaller. Franchise quality is not an automatic buy signal when that quality is already priced in.

Westpac remains one of the most instructive cases in Australian banking. A long governance and compliance shadow, stemming from the AUSTRAC matter and Royal Commission exposure, continues to create valuation drag. The stock often appears statistically cheap, yet the market continues to question whether cultural change is genuine and whether earnings improvement is durable. Headline cheapness that reflects unresolved business quality concerns is not mispricing.

Research from AIRA and the ASX Investor Study shows that retail investors treat the Big Four as safe by default. That assumption is precisely the pattern qualitative analysis is designed to challenge.

| Bank | Key Qualitative Concern | Market Implication |

|---|---|---|

| ANZ | Execution risk and strategic communication consistency | Discount may reflect risk, not opportunity |

| CBA | Premium valuation leaves minimal margin for error | Quality priced in; disappointment punished harshly |

| NAB | Strategic direction adequate but not yet compelling | Valuation gap with CBA persists on quality grounds |

| WBC | Governance and compliance history; cultural change questioned | Apparent cheapness may reflect structural concerns |

Quantitative methods provide the map coordinates. Qualitative research determines whether the map is accurate for the terrain the investor is actually navigating.

Before acting on any valuation output for an ASX bank stock, an investor should be able to answer questions across six categories:

The valuation cross-check, the final step, only becomes meaningful after these qualitative questions have been addressed. Investors who consistently achieve strong outcomes with bank stocks in Australia are not those with better spreadsheets. They are those who ask better qualitative questions before the numbers are run.

For investors wanting to see these qualitative overlays applied to a complete worked valuation, our dedicated guide to valuation models for ASX bank shares runs PE and DDM analysis on ANZ against live May 2026 data and then stress-tests both outputs against credit cycle signals, RBA rate assumptions, and APRA capital changes that standard model inputs do not automatically capture.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The four core methods are Price-to-Earnings (PE), Price-to-Book (P/B), Dividend Discount Model (DDM), and Discounted Cash Flow (DCF). Each measures a different aspect of value, and using them in combination produces a more reliable picture than relying on any single metric.

Bank earnings can be temporarily distorted by credit cycle conditions, one-off legal provisions, or remediation charges, making a low PE appear attractive when the underlying earnings quality is not durable. A low multiple is a prompt for further investigation, not a conclusion.

Franking credits represent company tax already paid and can be refunded in full to eligible investors such as superannuation funds. When running a DDM on an ASX bank, gross yield including the franking credit should be used as the input rather than the cash yield alone, which can shift the valuation output by several dollars per share.

APRA's unquestionably strong capital benchmarks require Australian banks to hold higher capital bases, which structurally constrains return on equity. This means a lower P/B multiple for an Australian bank relative to an international peer may partially reflect regulatory constraint rather than genuine mispricing.

Investors should review at least three years of annual reports to identify whether management guidance has been consistently met, assess the quality and transparency of executive communication, and deliberately seek out bearish analyst views to stress-test their assumptions before drawing any conclusion from the numbers.