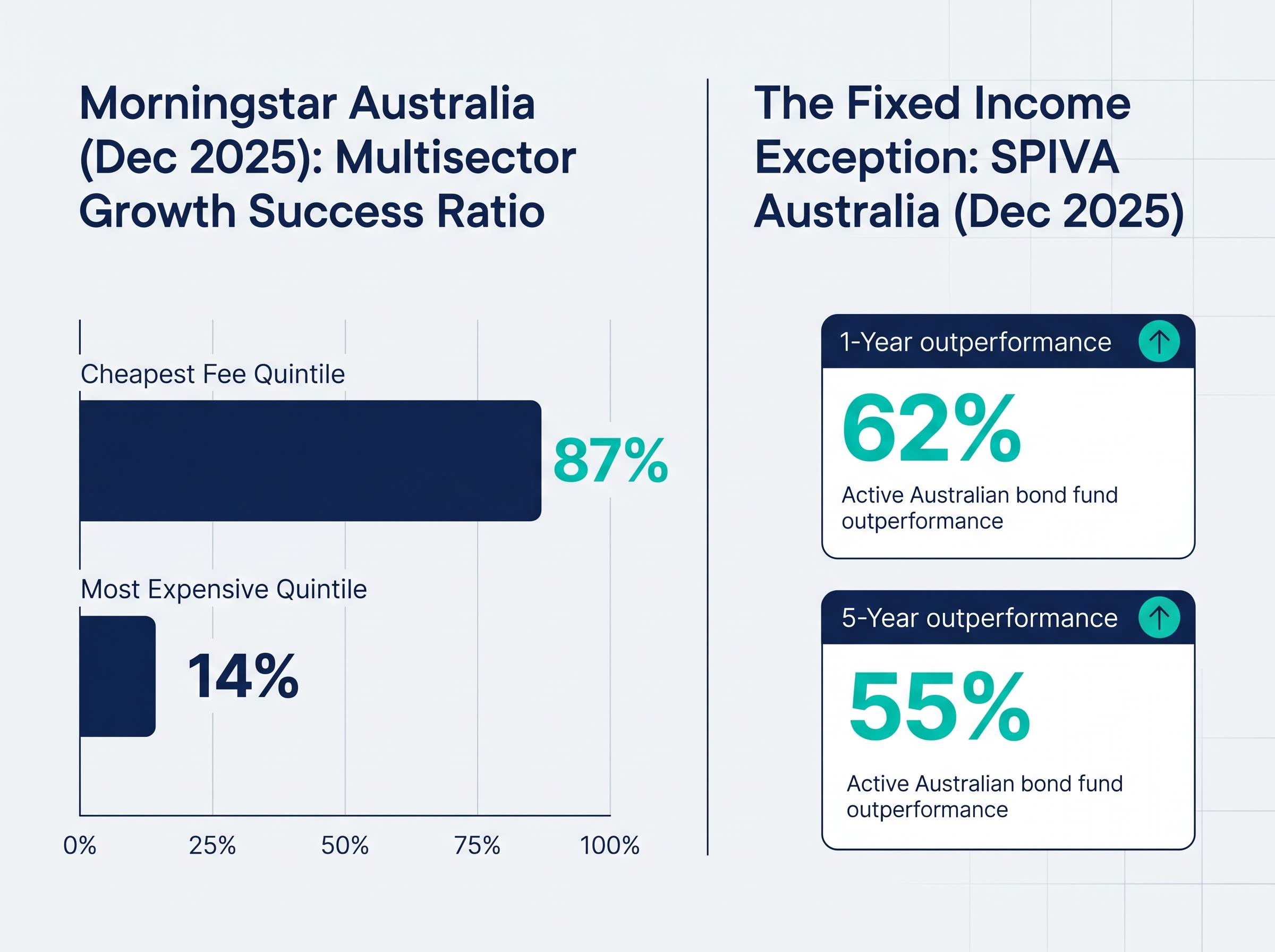

Across nearly every fund category, the cheapest option wins. Morningstar Australia’s fee study, using data through December 2025, found that funds in the lowest expense ratio quintile delivered an 87% success ratio in the multisector growth category, compared with just 14% for the most expensive quintile. The pattern held across equities, balanced funds, and most allocation categories. It is one of the most durable findings in fund research. Yet fixed income breaks the pattern. In the same study, three middle expense ratio quintiles, predominantly actively managed and competitively priced, outperformed the cheapest quintile in bond categories. For investors who apply a blanket “buy the cheapest” rule across their entire portfolio, the bond sleeve may be the one place that approach costs them money.

What follows is an examination of why active fixed income strategies have outperformed passive alternatives in Australia, what structural features of bond markets explain the exception, and how to think practically about where each approach fits within a fixed income allocation.

The rule that almost always works (and where it breaks down)

Morningstar Australia, December 2025: Funds in the cheapest fee quintile delivered an 87% success ratio in multisector growth, versus 14% for the most expensive quintile.

The fee-performance relationship is not received wisdom or a convenient generalisation. It is one of the most empirically supported findings in fund selection research. Morningstar’s cross-category analysis shows that lower fees predict stronger outcomes with remarkable consistency, across equities, balanced strategies, and most allocation categories.

The relationship holds because fees are a known drag on returns. In efficient markets where most managers struggle to generate alpha, that drag becomes the dominant differentiator over time.

Fixed income, however, sits outside this pattern:

- Where fees reliably predict outcomes: Equity categories (large-cap, small-cap, international), balanced funds, and most growth-oriented allocation categories.

- Where the relationship weakens: Some niche or concentrated categories where manager selection matters more.

- The explicit exception: Fixed income categories, where mid-priced active strategies outperformed the cheapest passive alternatives during the study period.

This is not a reason to abandon fee discipline. It is a reason to investigate what makes bond markets structurally different from the markets where the fee rule holds.

When big ASX news breaks, our subscribers know first

Why bond markets are built differently from equity markets

The active outperformance case in fixed income is not a temporary anomaly or a lucky streak. It follows logically from how bond markets actually function, in ways that differ sharply from equity markets.

Four structural features make bond markets less efficient:

- Over-the-counter trading: Most bonds trade through dealer networks rather than on centralised exchanges. This creates fragmented pricing, wider bid-offer spreads, and genuine scope for mispricing that skilled traders can exploit.

- Debt-weighted index construction: Bond indices allocate based on how much debt an issuer has outstanding, not on financial health or creditworthiness. The most indebted issuers receive the largest index weightings.

- Forced rebalancing mechanics: Passive funds tracking bond indices can become mechanically forced sellers when bonds are downgraded and forced buyers during index reconstitution, often at economically poor prices.

- Episodic liquidity: Bond market liquidity is uneven. In stressed periods, the cost of replicating an index rises sharply, creating tracking drag that does not appear in a fund’s stated fees.

Active managers can adjust duration, credit quality, sector allocation, and liquidity exposure far more quickly than index-tracking funds. That flexibility has limited value in efficient, continuously traded equity markets. In fragmented, OTC-traded bond markets, it becomes a genuine source of differentiation.

The index construction problem in bonds

Debt-weighted indexing rewards borrowing volume, not creditworthiness. An issuer that doubles its outstanding debt receives a proportionally larger index weighting, regardless of whether that borrowing signals strength or deteriorating financial health.

This creates systematic exposure to the most leveraged issuers at exactly the wrong point in a credit cycle. When credit conditions tighten and defaults rise, passive bond funds are mechanically overweight the names most likely to suffer downgrades or losses.

What the 2022-2026 rate cycle exposed

The structural weaknesses outlined above existed long before 2022. What the 2022-2026 rate cycle did was turn them into measurable performance gaps.

When the Reserve Bank of Australia and global central banks raised rates sharply from 2022 onward, duration risk became the dominant return driver in fixed income. Passive funds tracking broad bond indices could not reduce their exposure to long-dated bonds quickly. Active managers could and, in many cases, did shorten duration well before the worst of the sell-off.

Credit spread dispersion widened simultaneously. The gap between stronger and weaker issuers grew, meaning security selection became more important than broad market exposure. In Australia specifically, RBA rate volatility, concentrated bank issuance dynamics, and the behaviour of superannuation flows created an environment where local market knowledge and active positioning mattered more than in calmer periods.

SPIVA Australia Year-End 2025: 62% of active Australian bond funds outperformed their benchmarks over the one-year period ending December 2025, marking the third consecutive year of majority outperformance.

Over the five-year horizon, 55% of active Australian bond funds outperformed their benchmarks, according to SPIVA Australia. The contrast with equity categories in the same report is notable.

| Category | Active outperformance (1-year) | Active outperformance (5-year) |

|---|---|---|

| Australian bond funds | 62% | 55% |

| Australian equity funds | Active underperformance more prevalent | Active underperformance more prevalent |

Three consecutive years of majority active outperformance in bonds, at a time when equities showed the opposite pattern, is the clearest empirical support for the structural case. The rate cycle did not create the structural advantages. It amplified them enough to show up in the scorecards.

Where passive still makes sense in a bond portfolio

None of this amounts to a blanket case against passive fixed income. The honest answer is more specific than “active always wins in bonds,” and that specificity is what makes the distinction genuinely useful.

| Where passive is more rational | Where active adds clearest value |

|---|---|

| Highly liquid government bond exposure | Investment-grade credit strategies |

| Short-duration, cash-like sleeves | Unconstrained or core-plus bond funds |

| Situations where implementation simplicity and cost minimisation dominate | Multi-sector fixed income allocations |

| Plain-vanilla sovereign exposure where tracking error is low | Volatile or stressed market environments |

Large Australian superannuation funds generally reflect this distinction in practice. Many use passive strategies for efficient, liquid sovereign exposures and active managers for less efficient or more specialised fixed income segments, particularly credit-heavy or opportunistic mandates. The approach is blended rather than ideological, matching the tool to the segment.

Australian advisers tend to operate on a similar basis. Passive where costs and simplicity are the priority. Active where the track record in credit selection, duration management, and downside protection is genuinely differentiated.

How Morningstar’s updated rating framework now prices this in

Morningstar formalised this nuance in April 2026 with an update to its Medalist Rating methodology. The update introduced a new Price Score that makes visible whether a fund’s fee level is a competitive advantage or a drag on its overall rating.

The updated framework assesses funds across three components:

- Price Score: Lower-cost funds receive a rating boost; higher-cost funds receive a discount. This formalises fee discipline within the rating.

- Team and process quality: The investment team’s depth, stability, and the rigour of the investment process.

- Parent organisation: The quality and alignment of the fund’s parent company with investors’ interests.

The methodology change is not a departure from fee discipline. It is a recognition that fees must be assessed alongside what the investor is actually purchasing.

What the Price Score means for bond fund selection

Under the updated framework, a mid-priced active bond fund with strong qualitative ratings for team, process, and parent can score well, even if it does not sit in the cheapest quintile. The Price Score penalises expensive funds, but it does not automatically reward the cheapest option if the qualitative inputs are weak.

This reinforces the article’s central observation. In fixed income, a competitively priced active fund with genuine skill in credit selection and duration management may represent better value than the cheapest passive alternative. The updated Medalist Rating now formally accounts for that distinction.

What bond investors should actually do with this information

The practical application starts with a segment-by-segment audit of the bond sleeve, rather than a blanket decision for or against active management.

- Identify the segment type. Separate the bond allocation into its components: broad sovereign exposure, credit-heavy strategies, unconstrained or multi-sector funds, and short-duration or cash-equivalent holdings.

- Assess active versus passive track record for each segment. Use SPIVA Australia data, which is publicly available and updated regularly, to evaluate whether active managers in that specific category have outperformed their benchmarks over meaningful time horizons.

- Evaluate the fee-to-quality ratio. Apply the Morningstar Medalist Rating framework (updated April 2026) to assess whether an active fund’s fees are justified by its process, team, and track record, rather than simply comparing expense ratios in isolation.

APRA’s prudential framework encourages superannuation trustees to justify investment choices against members’ best financial interests, supporting a case-by-case approach rather than ideological blanket positions. Individual investors benefit from the same discipline.

“In fixed income, the question is not whether you are paying the least. It is whether what you are paying for is genuinely worth it.”

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The fee rule still matters, just not everywhere equally

Fee discipline remains one of the most reliable guides to fund selection across most asset classes. Across nearly all non-fixed-income categories, Morningstar Australia’s data through December 2025 confirmed the cheapest funds outperformed. That finding is not in dispute.

What the fixed income evidence adds is a refinement. Bond markets are structurally less efficient than equity markets. Passive replication has specific design flaws in fixed income, from debt-weighted indexing to forced rebalancing at poor prices. The 2022-2026 rate cycle amplified both weaknesses, and SPIVA Australia documented the result: three consecutive years of majority active outperformance in Australian bonds.

Morningstar’s April 2026 methodology update formalises the same distinction, assessing fee discipline alongside quality rather than treating cost as the sole predictor.

The portable principle: apply fee-first thinking to equities and highly efficient markets. Apply fee-plus-quality thinking to bonds and less efficient segments where skill, structure, and flexibility have a measurable edge.