Why Your ETF Portfolio May Be Less Diversified Than You Think

53 mins ago

A retail investor who bought an ASX ETF in 2018 and sells it in 2028 will have their capital gain split across two entirely different tax regimes. The gain will be calculated against two different cost bases, under rules that did not exist until 12 May 2026. That is the practical reality of Australia’s most significant capital gains tax overhaul since the 50% discount replaced indexation in 1999.

The 2026-27 Federal Budget, handed down on 12 May 2026, announced the replacement of the flat 50% CGT discount with a CPI-based indexation model and a 30% minimum tax on real gains, both taking effect from 1 July 2027. The reform applies to individuals, trusts, and partnerships across all CGT asset classes. Legislation has not yet passed parliament, but the policy mechanics are publicly detailed in Treasury’s Budget factsheet published on 14 May 2026.

What follows is a step-by-step explanation of how the new system works: the indexation formula, the minimum tax structure, the split-calculation rule for assets already held, what remains unchanged, and what the transition window means for investors who act before 1 July 2027.

When the 50% CGT discount replaced the original CPI indexation method in 1999, it was pitched as a simplification. Rather than tracking quarterly inflation figures across the life of every asset, investors would simply halve their nominal gain. It was a blunt instrument, but it was easy to apply.

Over 26 years, that blunt instrument created a specific distortion. The flat 50% discount shelters both genuine real gains and the portion of a gain attributable purely to inflation, treating them identically. An asset that doubled in real value received the same discount as one that merely kept pace with the consumer price index. The government’s position, outlined in the Treasury factsheet, is that this has systematically under-taxed investment income relative to wages.

Treasury has cited three motivations for the reform:

The reform applies to all CGT assets, not only residential property. Understanding why the government framed the change this way helps investors assess whether further amendments are likely as the legislation passes through parliament.

The new system replaces the flat discount with a formula. The cost base of an asset is adjusted upward using the Consumer Price Index, so that only the gain above inflation is taxable.

The core calculation involves three steps:

Indexation Formula

Indexation Factor = CPI (sale quarter) / CPI (purchase quarter)

Adjusted Cost Base = Original Cost Base x Indexation Factor

Taxable Gain = Sale Price – Adjusted Cost Base

The CPI figures are drawn from the Australian Bureau of Statistics quarterly CPI series. The ABS released the March quarter 2026 CPI on 24 April 2026, providing the most recent reference data point. The ATO has committed to publishing guidance and calculation tools before the 1 July 2027 commencement date, according to the Treasury factsheet.

Low-inflation indexation scenarios complicate the picture further: when CPI growth tracks the RBA’s 2-3% target band, the annual indexation uplift is modest enough that the 30% minimum tax activates on most equity positions, meaning the floor rather than the formula becomes the operative constraint for the majority of long-term investors.

The ABS quarterly CPI series is the official data source for all indexation factor calculations under the new regime, with each quarter’s headline CPI figure determining the inflation adjustment applied to the cost base of assets sold in that period.

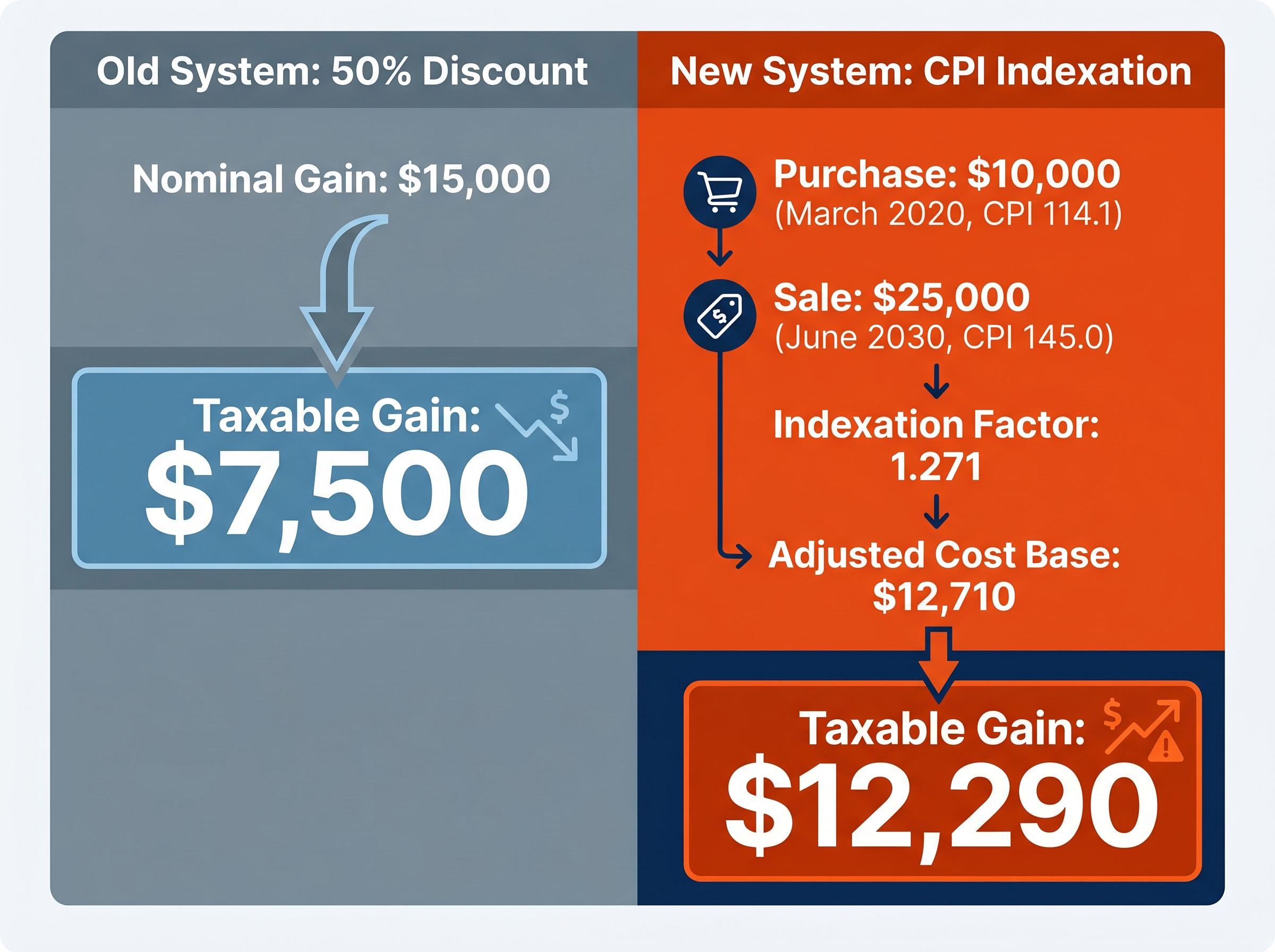

Consider shares purchased for $10,000 in the March 2020 quarter, when the ABS CPI stood at 114.1. The investor sells in a hypothetical June 2030 quarter, when the CPI has risen to 145.0, for $25,000.

The indexation factor is 145.0 / 114.1 = 1.271. The adjusted cost base becomes $10,000 x 1.271 = $12,710. The nominal gain is $15,000 ($25,000 minus $10,000), but the taxable gain under the new system is $12,290 ($25,000 minus $12,710).

Under the old 50% discount, the taxable gain on the same transaction would have been $7,500 (half of the $15,000 nominal gain). The new system produces a higher taxable amount when real returns are strong, because the inflation adjustment is smaller than the flat 50% haircut for assets that have genuinely outperformed CPI.

The second component of the reform may carry broader behavioural implications than the indexation formula itself. From 1 July 2027, a minimum 30% tax applies to the real (inflation-adjusted) capital gain, regardless of the investor’s marginal tax rate in the year of sale.

Under the previous system, a retired investor on a low marginal rate could pay as little as 16.5% effective tax on a capital gain by timing the sale to a low-income year. That strategy, widely used by long-term investors approaching or in retirement, is largely neutralised by the 30% floor.

| Investor Type | Old System Outcome | New System Outcome | Key Difference |

|---|---|---|---|

| High-income earner (45% marginal rate) | 50% discount; effective rate ~22.5% on nominal gain | Marginal rate on real gain (likely above 30% floor) | May pay less if large inflationary component |

| Retiree on low income (16.5% marginal rate) | 50% discount; effective rate ~8.25% on nominal gain | 30% minimum on real gain | Substantially higher effective rate |

| Superannuation fund (including SMSF) | Existing super CGT rules | No change; existing super CGT rules preserved | Not affected by the reform |

Assets held inside superannuation funds, including self-managed super funds (SMSFs), are explicitly excluded from the new framework. Existing super CGT rules remain in place.

Treasury Example: Ben

An investor whose gain is entirely attributable to inflation, with no real return above CPI, pays zero CGT under the new indexation system. Under the old 50% discount, the same investor would have faced a taxable capital gain of $70,021. The new system shields purely inflationary gains entirely.

For investors who planned to defer large asset sales until retirement to exploit a lower marginal rate, the minimum tax makes that strategy largely ineffective after 1 July 2027.

Treasury’s Budget factsheet, published on 14 May 2026, sets out the full mechanics of both the CPI indexation model and the 30% minimum tax, including the transitional split-calculation rule and the treatment of assets held before the commencement date.

These statements reflect announced policy and are subject to change during the parliamentary process. Legislation has not yet received Royal Assent.

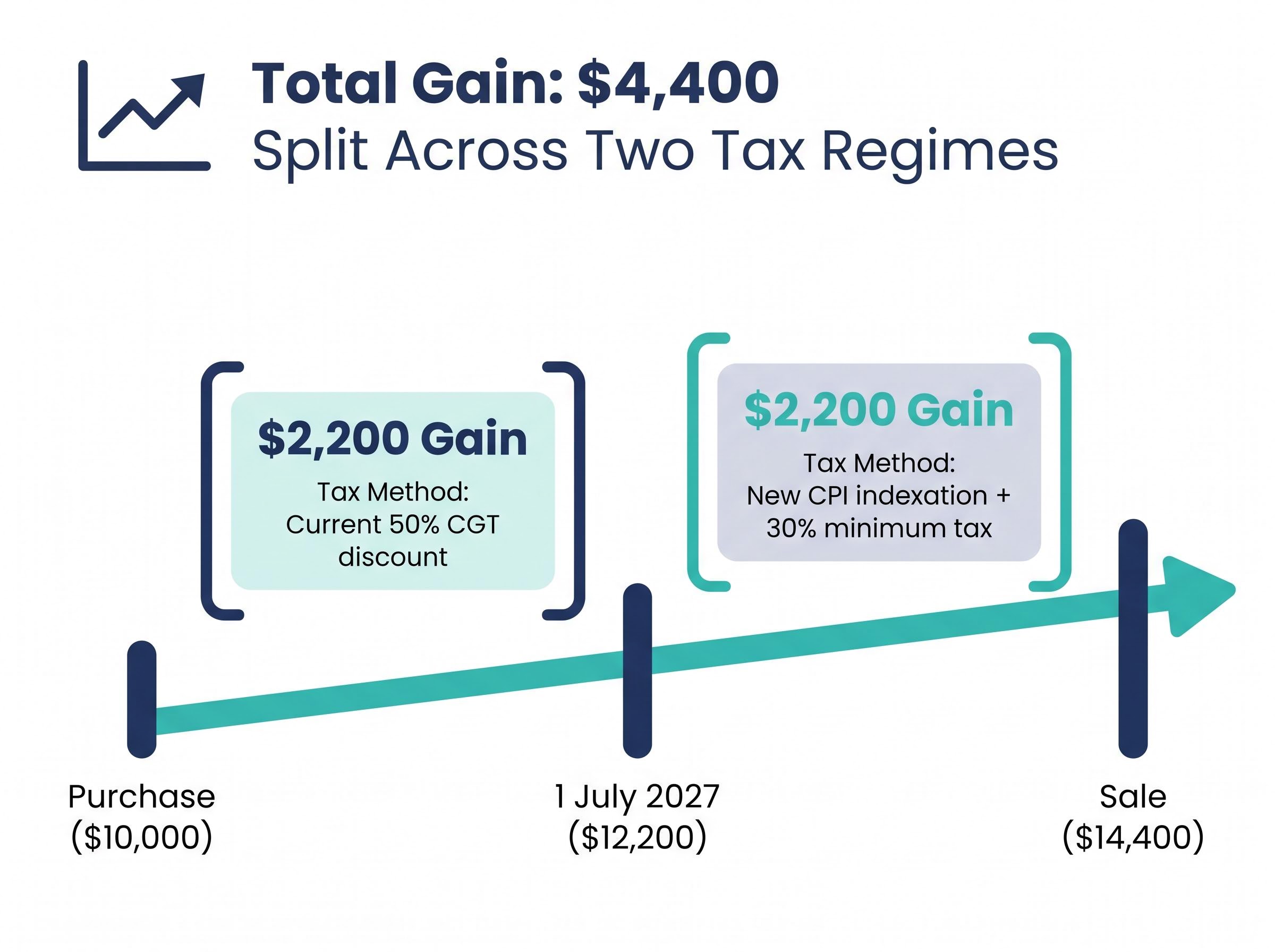

Every investor who currently holds a CGT asset purchased before 1 July 2027 will be subject to a split-calculation rule if they sell after that date. The gain is divided at the asset’s market value on 1 July 2027, with each portion taxed under different rules.

The Treasury factsheet states: “The 50 per cent CGT discount will apply to the difference between the asset’s cost base and its value at 1 July 2027.” Gains accruing after that date use the new CPI indexation system, with the 1 July 2027 value serving as the new cost base for the indexation calculation.

Consider an ASX-listed ETF purchased for $10,000. By 1 July 2027, it has grown to $12,200. The investor eventually sells for $14,400.

| Period | Cost Base Used | Gain Amount | Tax Method Applied |

|---|---|---|---|

| Purchase to 30 June 2027 | $10,000 (original cost base) | $2,200 | Current 50% CGT discount |

| 1 July 2027 to sale date | $12,200 (deemed cost base at transition) | $2,200 | New CPI indexation + 30% minimum tax |

The total gain of $4,400 is split across two regimes. The pre-transition portion benefits from the existing 50% discount. The post-transition portion is subject to indexation and the 30% minimum tax on the real component.

Assets purchased after Budget night (12 May 2026) are subject to the same transitional framework, with the 1 July 2027 date serving as the split point.

The split-calculation rule creates a practical obligation: investors will need a documented market value for each CGT asset as at 1 July 2027. The options available include:

Listed shares and ETFs have straightforward reference prices. Unlisted assets, including investment properties and private company holdings, will require a formal independent valuation. According to GPL Financial Group, summarising commentary from CFS, “asset values are going to need to be determined as at 1 July 2027, which will involve some additional work, including seeking a valuation.”

Accountants are warning of increased record-keeping complexity, particularly for investors with dividend reinvestment plan (DRP) shares, multiple purchase parcels, and properties with numerous improvement costs. Each asset will effectively need a split calculation with documentation supporting both the original cost base and the transition-date value.

One additional complication: assets acquired before 20 September 1985 were previously outside the CGT net entirely. This reform brings them in for the first time, requiring valuations to be established from scratch for many long-held family properties and generational assets.

After three sections of structural change, it is worth identifying what has not moved. Several elements of the existing CGT framework remain entirely unaffected:

One specific carve-out applies to newly constructed residential dwellings. Buyers of new-build properties can choose between the 50% discount or the new indexation method at the time of eventual sale. This exemption does not extend to existing dwellings, shares, or other CGT asset classes.

Knowing these boundaries prevents investors from restructuring parts of their portfolio that are not actually affected by the reform.

The period from now (May 2026) to 30 June 2027 is a genuine planning window. Gains realised before that date on existing holdings are fully subject to the current 50% discount, which may be more favourable for investors with large unrealised gains on a low original cost base.

The following actions, in priority order, address the most time-sensitive requirements:

Legislation status: The CGT reform has not yet received Royal Assent as at 14 May 2026. Final details may be amended during the parliamentary process. Investors should monitor ATO guidance releases as the 1 July 2027 commencement date approaches.

Advisory firms including GPL Financial Group and CFS have noted substantial planning activity is expected before the start date. The ATO has committed to releasing calculation tools and guidance before commencement, but these have not yet been published.

For investors whose primary holdings are exchange-traded funds, our dedicated guide to CGT changes and ETF portfolio structure examines how low-turnover passive funds compare with active managed funds on a post-reform after-tax basis, walks through buy-only rebalancing strategies that defer taxable events, and explains how the widened 20-percentage-point CGT gap between superannuation and personal ownership reshapes asset location decisions for growth-oriented ETF positions.

The reform is not uniformly more or less generous than the 50% discount. It is better for low-return, inflation-tracking assets (where the indexation adjustment may shield most or all of the gain) and worse for high-growth assets held over long periods (where the real gain is substantial and the 30% floor bites harder than a low marginal rate would have).

The minimum 30% tax on real gains is the structural change with the broadest behavioural implications. It removes the retirement-timing strategy that many long-term investors have relied on for decades.

The lock-in effect on portfolio reallocation is a secondary consequence the reform may not fully resolve: when effective CGT rates rise, investors rationally defer disposals, reducing market liquidity and potentially concentrating holdings in legacy positions that no longer reflect the investor’s strategic intent.

The period to 30 June 2027 is the last opportunity to realise gains under the current rules. The value of that window depends entirely on each investor’s specific cost base, holding period, and inflation expectations. Modelling individual positions against both regimes, consulting a registered tax agent or financial adviser for personalised advice, and monitoring ATO guidance releases are the three actions that convert this transition period from an abstract policy shift into a concrete planning opportunity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

From 1 July 2027, Australia will replace the flat 50% CGT discount with a CPI-based indexation model that adjusts the cost base of an asset for inflation, so only real gains above CPI growth are taxable, alongside a 30% minimum tax on those real gains.

If you sell an asset after 1 July 2027 that you purchased before that date, your total gain is divided at the asset's market value on 1 July 2027; the portion of the gain accrued before that date is taxed under the existing 50% discount, while any gain accrued after that date is subject to the new CPI indexation and 30% minimum tax.

No, assets held inside superannuation funds, including self-managed super funds (SMSFs), are explicitly excluded from the new CGT framework, and existing super CGT rules remain fully in place.

Divide the ABS CPI figure for the quarter you sell the asset by the ABS CPI figure for the quarter you purchased it to get the indexation factor, then multiply your original cost base by that factor; the taxable gain is the sale price minus this inflation-adjusted cost base.

Investors should model unrealised gains on existing positions under both the old and new regimes, collate cost-base records including dividend reinvestment plan shares and improvement costs, arrange documented valuations for unlisted assets as at 1 July 2027, and consult a registered tax agent before restructuring any holdings.