Google’s U.S. search query volume in the short-query segment fell 12% year-over-year, according to a February 2026 DOJ exhibit. Yet Alphabet just reported 19% Search revenue growth in Q1 2026. That contradiction sits at the centre of the stock’s investment debate and demands resolution. Two federal antitrust rulings have gone against Google since August 2024. The remedies order on search distribution was finalised in December 2025, and the ad-tech divestiture fight is live in 2026. At the same time, AI-native tools are capturing query share in the segments most vulnerable to substitution. Alphabet’s thesis now hinges on whether management’s claim, that AI is accelerating search rather than cannibalising it, holds under scrutiny, and whether the antitrust remedies bite as hard as bears fear. This analysis separates the two antitrust tracks, evaluates the AI disruption signal from the noise, and translates the most credible risk scenarios into what they mean for Alphabet’s revenue moat and forward valuation.

The search distribution ruling and what the remedies actually require

The legal question is settled. On 5 August 2024, Judge Amit Mehta ruled that Google maintained an illegal monopoly in general search services through exclusive default agreements with partners including Apple and Samsung. That ruling is not a pending risk; it is a finding of fact.

What followed matters more for investors than the headline.

From liability to remedy: the specific mechanisms investors need to understand

The remedies order was finalised on 5 December 2025. No full structural breakup of the search business was ordered, and no data-sharing mandates were imposed. What was ordered carries a sharper financial edge than many investors have priced:

- A ban on all exclusive default search agreements, ending the arrangements that guaranteed Google’s placement on Apple and Android devices

- Mandatory choice screens on Android devices, requiring users to select their preferred search engine during setup

- An annual auction mechanism replacing pre-installed defaults, beginning Q1 2027, where Google can still bid for default placement but must compete at a market-clearing price

The auction mechanism is the detail that deserves the closest attention. Google retains the ability to win default placement, but exclusivity, the structural barrier that prevented rivals from competing, is gone. The margin compression follows directly.

The Apple default deal trajectory: Google’s payments to Apple grew from approximately $20 billion in 2022 to an estimated $28 billion in 2025, a roughly 30% increase over three years. Analyst estimates project the effective annual equivalent declining toward $12-14 billion under the auction mechanism, a reduction of approximately 50% from the 2025 estimated level.

Google’s appeal is ongoing, with proceedings expected to continue through late 2026 into 2027. The appeals timeline is the bull case’s primary shield against near-term financial impact. Whether it holds is a separate question.

When big ASX news breaks, our subscribers know first

Why the ad-tech case is the higher-stakes structural threat

The search distribution case gets the headlines. The ad-tech case, heard by a different judge in a separate courtroom, carries a structurally deeper threat to Alphabet’s margin quality.

The United States v. Google DOJ antitrust proceedings encompass two distinct cases before two separate judges, each with its own liability findings, remedies timeline, and potential financial impact on Alphabet’s core business segments.

On 17 April 2025, Judge Leonie Brinkema ruled that Google monopolised the ad-tech market through its Open Bidding and publisher tools. This is a distinct proceeding from the search case, with its own remedies timeline and a judge who has signalled openness to structural divestitures, rejecting Google’s arguments against a breakup.

The DOJ’s remedy demands target the core of Google’s advertising plumbing:

- Divestiture of DoubleClick for Publishers (DFP), Google’s dominant ad server

- Divestiture of Authorized Buyers/Open Bidding, Google’s ad exchange

- Forced interoperability and data sharing with rival platforms, with The Trade Desk specifically named as an intended beneficiary

The ad-tech segment operates at approximately 25% margins within Alphabet’s advertising operations. Goldman Sachs and Bank of America have modelled material EPS and revenue dilution in divestiture scenarios, with the direction of impact consistent across the analyst community even where specific figures carry attribution uncertainty. Behavioural remedies remain a fallback if structural relief is denied, but Judge Brinkema’s posture has tilted the probability distribution toward a more aggressive outcome than the search case delivered.

| Dimension | Search Distribution Case | Ad-Tech Case |

|---|---|---|

| Judge | Amit Mehta | Leonie Brinkema |

| Liability Ruling | August 2024 | April 2025 |

| Remedy Demanded | Default ban, choice screens, auction | DFP and ad exchange divestiture |

| Current Status | Remedies finalised; appeal ongoing | Remedies phase active in 2026 |

| Margin Exposure | Distribution cost compression | High-margin ad-stack component |

A DFP and ad exchange divestiture would not merely reduce a revenue line. It would remove the integration advantage that allows Google to price and optimise across the buy and sell side of the ad ecosystem simultaneously. That structural edge is a core component of the advertising moat.

How digital advertising actually works, and why Google’s stack is so hard to replicate

Understanding why the ad-tech divestiture threat matters requires understanding the plumbing. The programmatic advertising ecosystem operates across three layers, each performing a distinct function:

- Demand-side platform (DSP): The tool advertisers use to set budgets, define target audiences, and place bids on ad inventory across the internet

- Ad exchange: The auction marketplace where bids from advertisers are matched against available ad slots from publishers in real time, typically within milliseconds

- Supply-side platform and ad server (SSP/ad server): The tool publishers use to manage their available ad inventory, set pricing floors, and serve the winning ad to the user

Google operates across all three layers. Most competitors operate on one side or two.

The integration advantage and why it matters for revenue quality

Vertical integration across the full stack creates a closed-loop optimisation advantage. Google can see both the bid (what the advertiser is willing to pay) and the inventory (what the publisher is offering) simultaneously. This allows real-time pricing and quality signal arbitrage unavailable to competitors operating on only one side of the market.

The Google Network sub-segment contributed roughly $7 billion in Q1 2026 revenue. The DOJ built its antitrust case on the conflict-of-interest inherent in one company operating both sides of the marketplace: serving publishers who supply inventory while simultaneously serving advertisers who buy it.

Rivals such as The Trade Desk, specifically named in the DOJ’s interoperability proposals, must rely on less complete data, structurally limiting their ability to match Google’s return on ad spend for advertisers. Forced interoperability or divestiture of DFP would degrade this advantage even if Google retains the advertising revenue line on paper, because the premium Google charges rests on signal completeness that a fragmented stack cannot replicate.

AI tools are taking short queries, but the revenue signal is still pointing up

The bearish data point is real.

Internal Google data submitted as a DOJ exhibit in February 2026 showed a 12% year-over-year drop in U.S. search queries under 10 words, the short-query segment most susceptible to AI assistant substitution.

ChatGPT, Perplexity, and Claude have collectively grown their share of U.S. query activity, with ChatGPT holding an estimated 17% of AI-assisted search interactions. Apple has been observed testing AI search prompts in Safari beta builds, and Wall Street Journal reports from May 2026 suggest Apple has explored a potential partnership with Perplexity as an alternative search provider, though no formal agreement has been announced.

The financial data complicates the narrative. Alphabet’s Q1 2026 total revenue grew 22% year-over-year to $109.9 billion, with Search and other revenue specifically growing approximately 19%. Advertiser spending has not migrated at scale.

| Metric | 2024 Value | Q1/April 2026 Value | Directional Signal |

|---|---|---|---|

| Google Global Search Share | ~91.5% | ~90.02% (April 2026) | Modest erosion |

| Alphabet Total Revenue Growth | N/A | +22% YoY | Accelerating |

| Search and Other Revenue Growth | N/A | ~+19% YoY | Resilient |

| Short Query Volume (U.S.) | N/A | -12% YoY | Structural decline |

| Marketers Testing AI Alternatives | N/A | ~15% (Kantar, April 2026) | Early-stage migration |

Both data points can be true simultaneously. If AI tools are capturing low-monetisation informational queries while Google retains high-intent commercial queries carrying premium cost-per-click rates, the revenue impact is muted in the near term. Kantar survey data from April 2026 indicates approximately 15% of U.S. marketers were testing AI search alternatives, citing lower cost-per-click as a primary motivation. The risk scenario to monitor is not immediate revenue collapse but a gradual quality-mix shift that compresses average CPC over time as AI tools improve answer quality in commercial-intent categories.

Google Cloud and the balance sheet as structural offsets to antitrust risk

The antitrust cases dominate the risk discussion. The Cloud business is building an entirely separate growth engine that may eventually dwarf the threatened advertising segments.

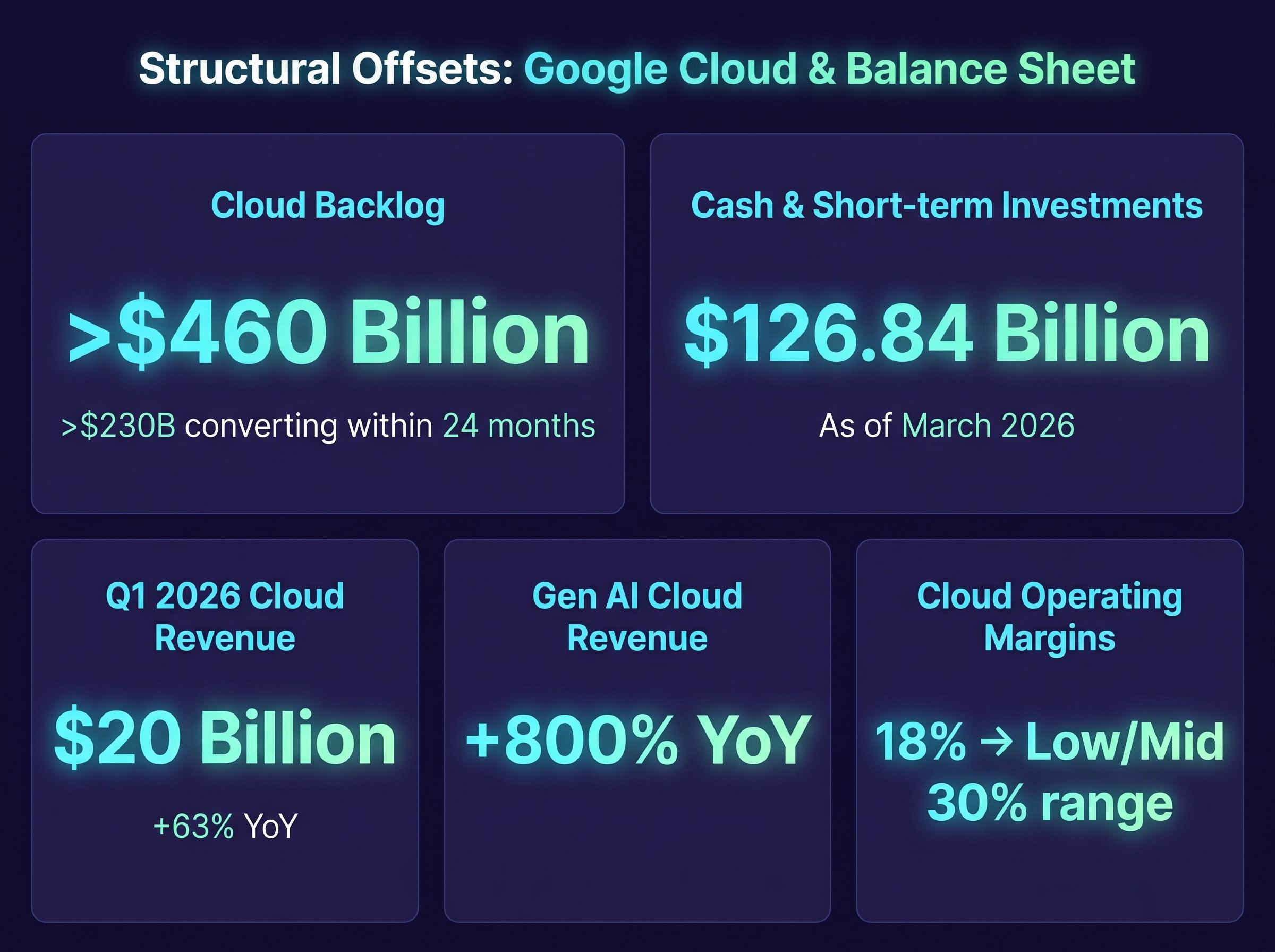

Google Cloud revenue grew 63% year-over-year to $20 billion in Q1 2026. Operating margins expanded to the low-to-mid 30% range from approximately 18% in the prior year’s first quarter. Generative AI product revenue within Cloud grew approximately 800% year-over-year.

The single most consequential number in Alphabet’s forward story is the backlog.

Cloud backlog nearly doubled to over $460 billion. Management has guided that more than half converts to recognised revenue within 24 months, implying over $230 billion in near-term contracted cloud revenue.

The balance sheet provides additional structural resilience:

- $126.84 billion in total cash and short-term investments as of March 2026

- Cloud backlog of $460 billion with 24-month conversion guidance on more than half

- Cloud operating margins expanding from 18% to the low-to-mid 30% range year-over-year

Capital expenditure approximately doubled year-over-year, and free cash flow declined roughly 50% as infrastructure spending intensified. The forward P/E sits at approximately 25-30x based on Q1 2026 EPS of $2.62. An investor who prices Alphabet purely as an advertising business with antitrust risk is missing the growth vector that bulls cite as the primary reason the stock commands a premium despite regulatory headwinds.

Hyperscaler capital expenditure trends across Q1 2026 place Alphabet’s $180-190 billion annual infrastructure commitment in sharper relief: combined capex across the four largest cloud operators reached $130.65 billion in a single quarter, up 71% year-over-year, a competitive dynamic that shapes how quickly Cloud margin expansion can continue before infrastructure costs re-accelerate.

Alphabet’s broader AI investment case rests on segments that sit entirely outside the antitrust blast radius: Waymo’s autonomous ride network, Gemini’s consumer deployment scale, and a capital expenditure programme that management frames as the foundation for decade-long infrastructure returns.

What Wall Street is pricing in and where the analyst consensus could be wrong

The consensus view is constructive. As of 13 May 2026, GOOG closed at approximately $397.66, up approximately 15% year-to-date from roughly $345 at the start of 2026. The majority of the 38-54 covering analysts (depending on share class) maintain a Strong Buy or Buy rating, with average price targets ranging from approximately $362 to $408.

Morgan Stanley rates the stock Overweight, viewing regulatory risk as meaningful but manageable with the appeals process offering favourable odds. Barclays holds at Equal Weight, modelling EPS risk from an ad-tech breakup scenario. Piper Sandler maintains an Overweight rating, viewing AI erosion risk as limited over the near-to-medium term.

Across the analyst community, the regulatory valuation discount averages 7-12%. That discount assumes the appeals process runs long and remedies remain behavioural rather than structural.

Alphabet’s relative valuation, at approximately 29x earnings, sits at the lowest P/E multiple among the Magnificent Seven despite Cloud growth outpacing Azure and AWS by the widest margin in recent memory, a gap that the analyst community has increasingly cited as a structural mispricing rather than a justified regulatory discount.

Three scenarios where the current regulatory discount is not enough

The consensus could prove inadequate under three specific conditions:

- An adverse appellate ruling accelerates implementation of the default ban before the market has priced it, compressing Apple distribution revenue by approximately 50% earlier than modelled

- A structural ad-tech divestiture order removes the closed-loop margin premium, degrading advertising margin quality beyond current analyst scenarios

- AI-native query migration crosses from informational queries into commercial-intent searches, compressing average CPC as AI tools improve answer quality where advertiser dollars concentrate

These are monitoring conditions, not forecasts. Management’s counterclaim, that AI integration is accelerating search usage rather than cannibalising it, remains a testable hypothesis investors should track through quarterly Search revenue growth rates and average CPC trends.

Antitrust remedies are a tax on dominance, not a death sentence for the franchise

Two antitrust rulings have gone against Google. The search distribution auction mechanism will compress what Google pays for default placement. A potential ad-tech divestiture could remove the integration advantage at the heart of the advertising margin stack. AI tools are taking short-query share at a measurable rate. Each pressure is real and quantifiable.

The structural advantages remain substantial. Search revenue grew 19% in Q1 2026. Cloud revenue grew 63% with a $460 billion backlog. The balance sheet holds $126.84 billion in cash and short-term investments. YouTube advertising revenue reached approximately $10 billion in Q1 2026, up approximately 11% year-over-year, with U.S. viewers watching 200 million hours per day on living room screens. Total FY 2025 revenue reached $402.8 billion.

The forward monitoring framework for investors rests on three evidence markers:

- Search revenue growth rate trend as the primary gauge of AI displacement velocity

- Appellate ruling timeline as the antitrust catalyst that determines when remedies begin compressing distribution economics

- Cloud backlog conversion progress as the valuation support anchor independent of advertising outcomes

The investment question is not survival. It is degree of impairment. The current 7-12% regulatory discount embedded in analyst valuations assumes a specific legal timeline and a specific severity of remedies. An investor who agrees with those assumptions is underwriting manageable compression of a dominant franchise. An investor who disagrees should be applying a materially larger discount, and tracking the three evidence markers above to know when the consensus view requires revision.

For investors weighing how much of an AI allocation to concentrate in Alphabet given the antitrust headwinds described above, our full explainer on Alphabet versus Nvidia as AI investments examines how Alphabet’s diversified stack across Cloud, Gemini, and Waymo compares with a pure-play semiconductor bet across risk, growth rate, and valuation metrics.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Forward-looking statements regarding legal proceedings, revenue impacts, and market share trends are subject to change based on judicial outcomes, market developments, and company performance.