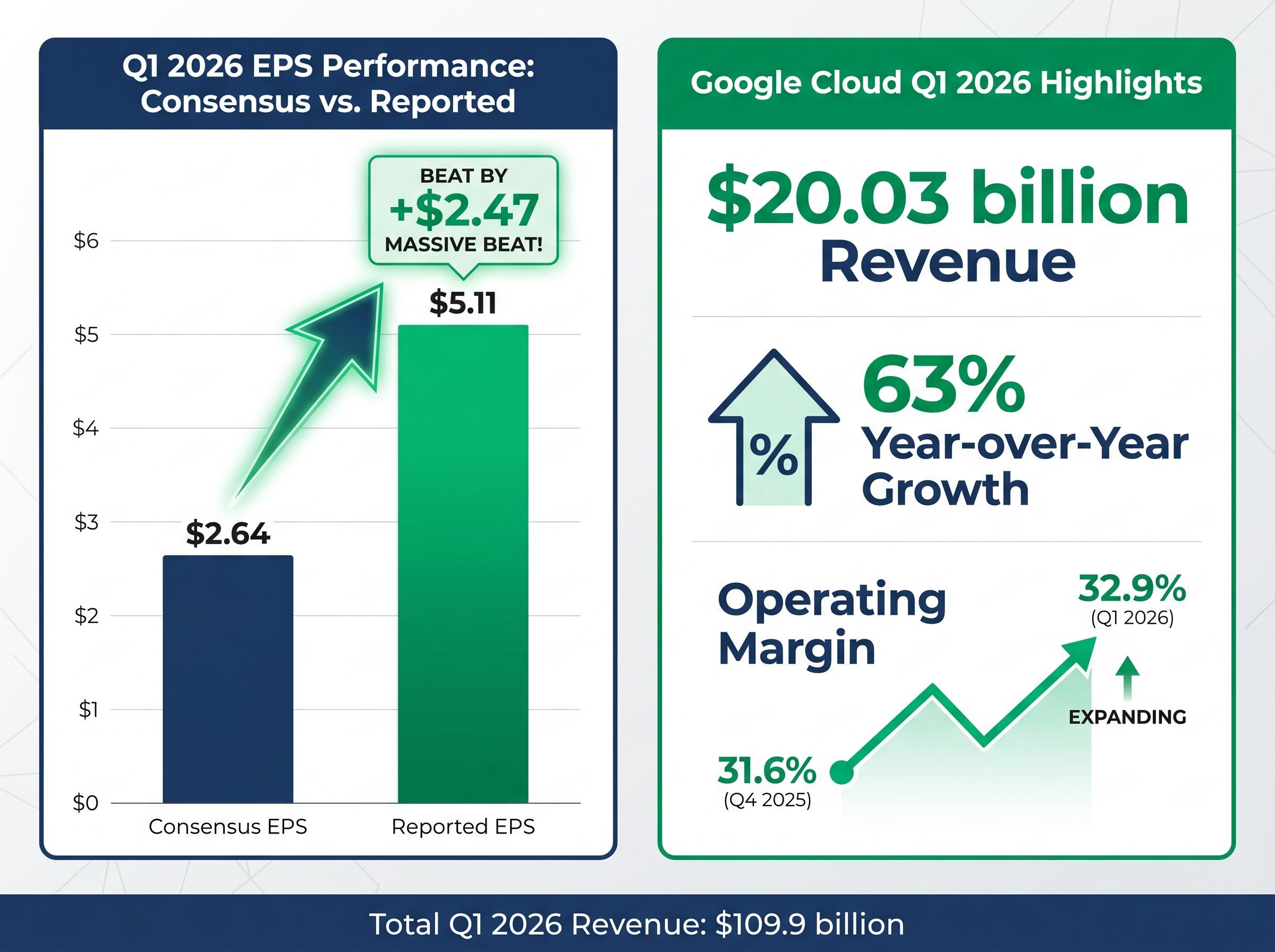

Alphabet’s engineers authored the research paper that made ChatGPT possible, yet Alphabet itself is rarely the first name investors reach for when building an AI portfolio. That gap between foundational contribution and market perception is worth examining. Following Q1 2026 earnings that delivered reported EPS of $5.11 against a consensus estimate of $2.64, Alphabet enters mid-2026 with Google Cloud growing at 63% year over year, Waymo surpassing 100,000 paid rides per week, and a quantum computing early-access programme now open to researchers and enterprise partners. The stock occupies a different position in the AI landscape than pure-play chip names, and that distinction carries direct implications for portfolio construction. This analysis walks through what makes Alphabet a structurally different AI investment, how each major segment contributes to or complicates that thesis, and what risks warrant attention before committing capital.

The company that invented the modern AI era

In 2017, a team at Google Brain (now merged into Google DeepMind) published “Attention Is All You Need,” the paper that introduced the Transformer architecture. Every large language model shipped since, from OpenAI’s GPT series to Meta’s Llama, is built on that foundation. For investors who associate Alphabet primarily with search advertising, this provenance tends to register as trivia. It is not.

The 2017 paper Attention Is All You Need, published by Vaswani et al. at Google Brain, introduced the Transformer architecture that underpins every major large language model in commercial deployment today, making Alphabet’s foundational role in the current AI economy a matter of academic record rather than corporate narrative.

The Transformer is the substrate of the current AI economy. Alphabet’s position at that foundational layer, upstream of the applications built on top of it, means its technical DNA is embedded across the entire industry. That lineage connects directly to present competitive standing.

Benchmark comparison: Alphabet’s Gemini 3.1 scores 94.3% on the GPQA benchmark, compared with 89.5% for OpenAI’s GPT-4o.

Gemini 3.1’s capabilities span several categories that reinforce this position:

- Multimodal performance: Leading scores across text, image, and reasoning benchmarks

- Ecosystem integration: “Personal Intelligence” agent capabilities across Gmail, Drive, Maps, and scheduling

- Search transformation: AI Overviews now appearing in approximately 47-50% of tracked U.S. Google Search queries

The result is a company whose AI investment case rests on originating the architecture, not merely adopting it.

When big ASX news breaks, our subscribers know first

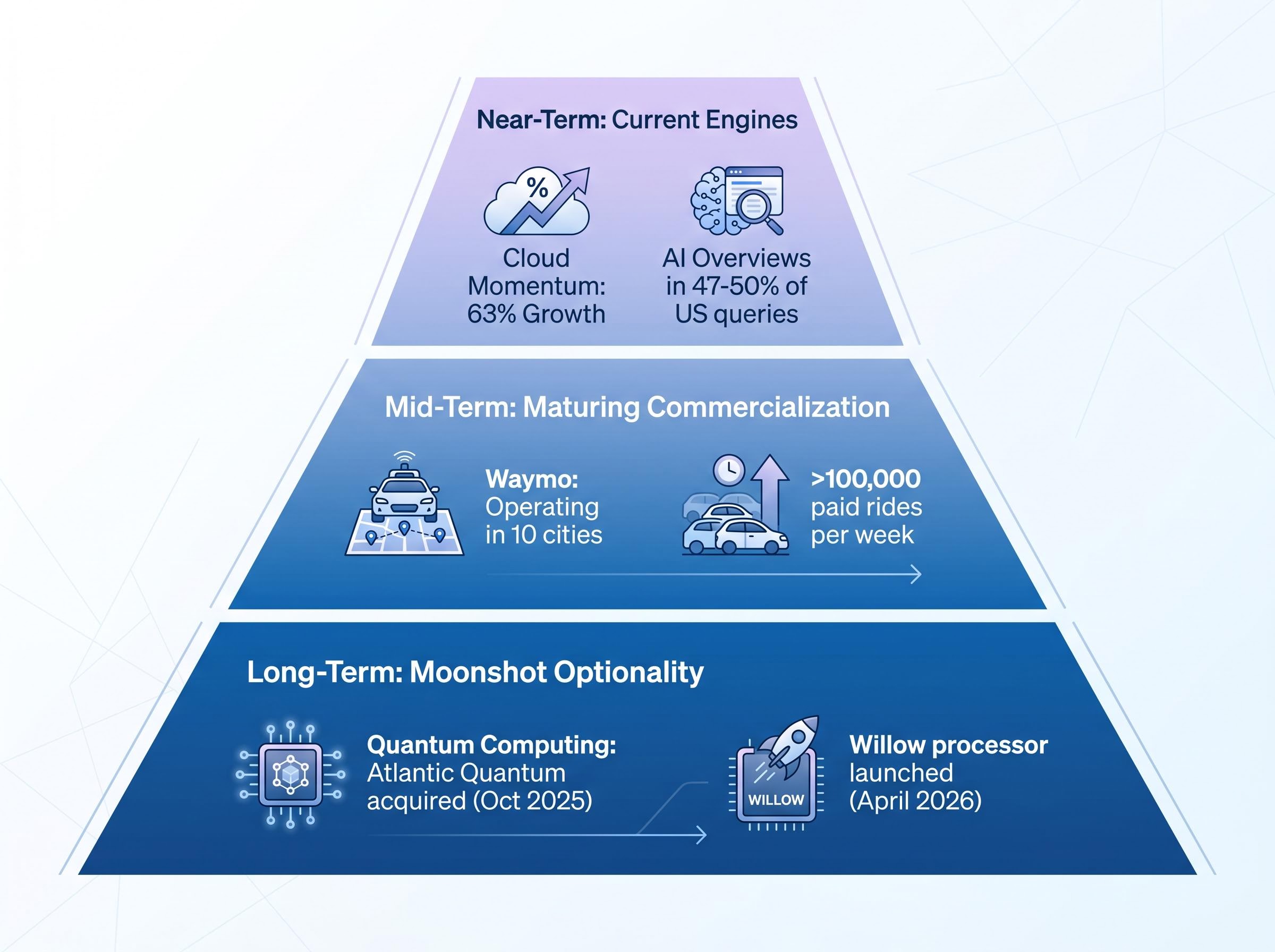

What 63% cloud growth actually means for the investment case

Google Cloud generated $20.03 billion in Q1 2026 revenue, a 63% increase year over year. Within Alphabet’s total Q1 revenue of $109.9 billion, Cloud now represents a segment large enough to move the consolidated earnings picture, which it did: the $5.11 EPS against $2.64 consensus reflected Cloud’s outperformance alongside Search strength.

The revenue headline, however, is only half the story. Operating margins expanded from approximately 31.6% in Q4 2025 to 32.9% in Q1 2026. Growth and profitability are moving in the same direction simultaneously, a combination that separates a scaling business from a capital-intensive land grab.

Global cloud infrastructure market growth reached 35% year over year in Q1 2026, with Amazon holding 28% share, Microsoft 21%, and Google 14%, according to Synergy Research Group data; that positioning places Google Cloud’s 63% segment growth well above the broader market expansion rate, indicating share gains rather than simple market tailwind.

| Metric | Q4 2025 | Q1 2026 |

|---|---|---|

| Revenue | — | $20.03 billion |

| Operating Margin | 31.6% | 32.9% |

| Year-over-Year Growth | — | 63% |

TPUs, Vertex AI, and the infrastructure edge

Underlying this margin expansion is a proprietary compute layer. Alphabet’s 7th-generation Ironwood TPUs reduce reliance on third-party chip supply and create a structural cost advantage in AI workloads. Vertex AI and Gemini integrations serve as the commercial delivery mechanism, converting infrastructure investment into enterprise Cloud revenue. Management has cited a multi-hundred-billion-dollar order backlog, suggesting the growth trajectory has runway beyond the current quarter.

What Waymo and quantum computing add to the portfolio that Wall Street is still pricing in

Waymo now operates across ten U.S. cities, delivering over 100,000 paid rides per week as of Q1 2026. Active integrations with Uber and expanded Lyft partnerships in newly launched markets, including Nashville, indicate commercial infrastructure maturing rather than stalling. The business is described as approaching profitability, though exact revenue figures and profitability timelines remain undisclosed in official filings.

For investors, the question is not whether Waymo works. It does. The question is how much of its potential revenue contribution, which analysts project could become meaningful by the end of the decade, is reflected in Alphabet’s current share price. Given the absence of standalone financial disclosure, the answer appears to be: not much.

Google Quantum AI has followed a separate but parallel trajectory of accelerating milestones:

- October 2025: Acquisition of Atlantic Quantum, expanding hardware capabilities

- November 2025: Publication of a five-stage roadmap toward practically useful quantum computing

- April 2026: Launch of an early-access programme for the Willow quantum processor

- April 2026: Announcement of expansion into neutral atom quantum systems, broadening beyond superconducting qubits

Analyst consensus: 89% of S&P Global-surveyed analysts (59 of 66) rate Alphabet a “buy” or “strong buy.”

BCA’s AI investment strategy, published on 1 May 2026, provides an institutional anchor for the analyst consensus picture: combined cloud remaining performance obligations for Alphabet, Microsoft, and Amazon tripled from $596 billion to $1.5 trillion year over year, the forward demand signal BCA cited when upgrading Communication Services to overweight and naming Alphabet as a preferred position.

That consensus reflects confidence in the known business. The optionality from Waymo and quantum, with payback timelines measured in years rather than quarters, represents a different kind of value: one that could materially reprice the stock over a 3-10 year horizon but requires patience.

How to read the risks before adding Alphabet to an AI portfolio

The capex trajectory demands honest attention. Alphabet’s updated 2026 guidance calls for $180-190 billion in capital expenditure, revised upward from prior guidance of $175-185 billion, with further increases signalled for 2027. At this scale, the question of whether AI infrastructure spending generates adequate returns shifts from theoretical to urgent.

The AI infrastructure investment cycle affecting Alphabet extends well beyond its own balance sheet: approximately 75% of projected hyperscaler capex is directed toward physical hardware and data centre construction, a concentration that has fuelled a semiconductor supercycle and introduced macroeconomic dependencies around power grid capacity that constrain all participants equally.

AI Overviews appearing in approximately 47-50% of U.S. search queries raises a separate concern. Some industry analyses cite click-through rate drops of approximately 61% for queries where AI-synthesised responses appear, though Alphabet-specific quantification remains unavailable. Whether AI Overviews cannibalise traditional Search ad revenue or create new “AI-native” ad formats that offset the shift is a legitimately open question, not a resolved one.

Competitive gaps exist as well. Gemini 3.1 Pro lags Meta’s Llama 3 in cost-efficiency for enterprise tasks and trails Anthropic’s Claude 3.5 on safety metrics. Regulatory risk around a potential ecosystem breakup continues as an overhang without near-term resolution.

| Risk Category | Key Data Point | Near-Term Impact | Resolved in Current Results |

|---|---|---|---|

| Capex Escalation | $180-190B (2026 guidance) | Margin pressure if returns lag | No; further increases signalled for 2027 |

| Search Cannibalisation | 47-50% of queries show AI Overviews | CTR compression on traditional ads | No; monetisation transition ongoing |

| Competitive Gaps | Lags Llama 3 (cost), Claude 3.5 (safety) | Enterprise share risk | Partially; Gemini leads on benchmarks |

| Regulatory Overhang | Potential ecosystem breakup pressures | Sentiment drag, legal costs | No; unresolved |

None of these risks are trivial. The Q1 results suggest the business can absorb them in the near term. Whether it can over a multi-year capex cycle is the harder question.

Why Alphabet is a different kind of AI stock than Nvidia or Broadcom

Nvidia sells the infrastructure. Broadcom designs the custom silicon. Alphabet builds the products that sit on top of both. The distinction matters for portfolio construction: buying Nvidia is a bet on AI compute demand; buying Alphabet is a bet on AI reaching consumers and enterprises through search, cloud services, autonomous vehicles, and quantum computing simultaneously.

| Metric | Alphabet | Nvidia | Broadcom |

|---|---|---|---|

| Market Cap | ~$4.6 trillion | ~$4.8 trillion | ~$2.0 trillion |

| Analyst Buy Rate | 89% (59/66) | 95% (56/59) | 94% (44/47) |

| 12-Month Price Target | ~$421.70 ($311-$515) | — | — |

| Gross Margin | 60.43% | — | — |

| AI Revenue Driver | Search, Cloud, Waymo, Quantum | GPU/Software Infrastructure | Custom ASIC Accelerators |

Alphabet’s 89% buy-rate sits below Nvidia’s 95%, but the difference reflects a distinct risk-return profile rather than weaker fundamentals. Alphabet also pays a dividend of $0.22 per share, raised in Q1 2026, and trades within a 52-week range of $147.84 to $387.38.

Portfolio positioning: infrastructure layer vs. ecosystem layer

The distinction between infrastructure-layer AI investments (chips, custom silicon) and ecosystem-layer AI investments (search monetisation, cloud services, autonomous vehicles, quantum) is practical, not academic. Investors seeking concentrated exposure to AI compute demand may prefer Nvidia or Broadcom. Investors seeking broad AI exposure with a revenue-generating core, where multiple segments could reprice independently, may find Alphabet better suited to that objective.

Semiconductor concentration risk compounds the portfolio construction question: semiconductor companies accounted for a record 13% of US equity market capitalisation in April 2026, surpassing dot-com era concentration levels, which means investors buying Nvidia as a pure AI infrastructure play are simultaneously absorbing index-level concentration exposure that interacts with any Alphabet position in the same portfolio.

What Alphabet’s Q1 2026 results signal about the rest of 2026

EPS beat: Alphabet reported $5.11 per share against analyst consensus of $2.64, nearly doubling expectations.

That magnitude of earnings surprise suggests AI monetisation across Search and Cloud is accelerating faster than analyst models assumed, not simply tracking a known trajectory. Post-earnings upgrades from Goldman Sachs, JPMorgan, and Citi reflect institutional re-rating of the AI monetisation timeline, providing near-term price support beyond the headline beat.

The Q1 2026 earnings reaction across the hyperscaler group illustrated how differently the market is now pricing each company’s spending-to-revenue conversion: Alphabet surged to an all-time high on the same session that Meta fell more than 9%, despite both companies reporting record capital expenditure commitments.

Three forward indicators are worth monitoring through the second half of 2026:

- Cloud margin trajectory: Whether operating margins sustain above 32% will signal whether scale economics are durable or quarter-specific

- AI Overviews CTR evolution: As AI-synthesised responses expand across more query types, the click-through rate impact on traditional Search ad revenue will become measurable

- Waymo city-expansion pace: The rate at which Waymo enters new U.S. markets provides a real-time gauge of commercialisation momentum

The primary counterweight remains capex. With guidance at $180-190 billion for 2026 and further increases expected in 2027, investors will need evidence that infrastructure spending is converting into revenue at rates sufficient to justify the outlay.

Alphabet is not a search company with AI ambitions; it is an AI company with a search cash flow engine

Search remains the cash flow engine. It funds a portfolio of AI businesses operating on different growth timelines and carrying different risk profiles. The investment case organises into three tiers:

- Near-term: Cloud momentum at 63% growth with expanding margins; Search AI monetisation through AI Overviews and AI-native ad formats

- Mid-term: Waymo commercialisation across ten cities, approaching profitability with extended but measurable payback

- Long-term: Quantum computing optionality, with four milestones delivered between October 2025 and April 2026 and commercial applications still years away

Alphabet suits investors seeking diversified AI exposure underpinned by current revenue generation, not a high-beta wager on any single AI segment. The Q1 2026 results strengthen that thesis. The capex trajectory, competitive gaps, and regulatory overhang complicate it. Both of those realities can coexist in the same stock.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.