How the US Government Became Intel’s Investor and Deal Broker

1 hr ago

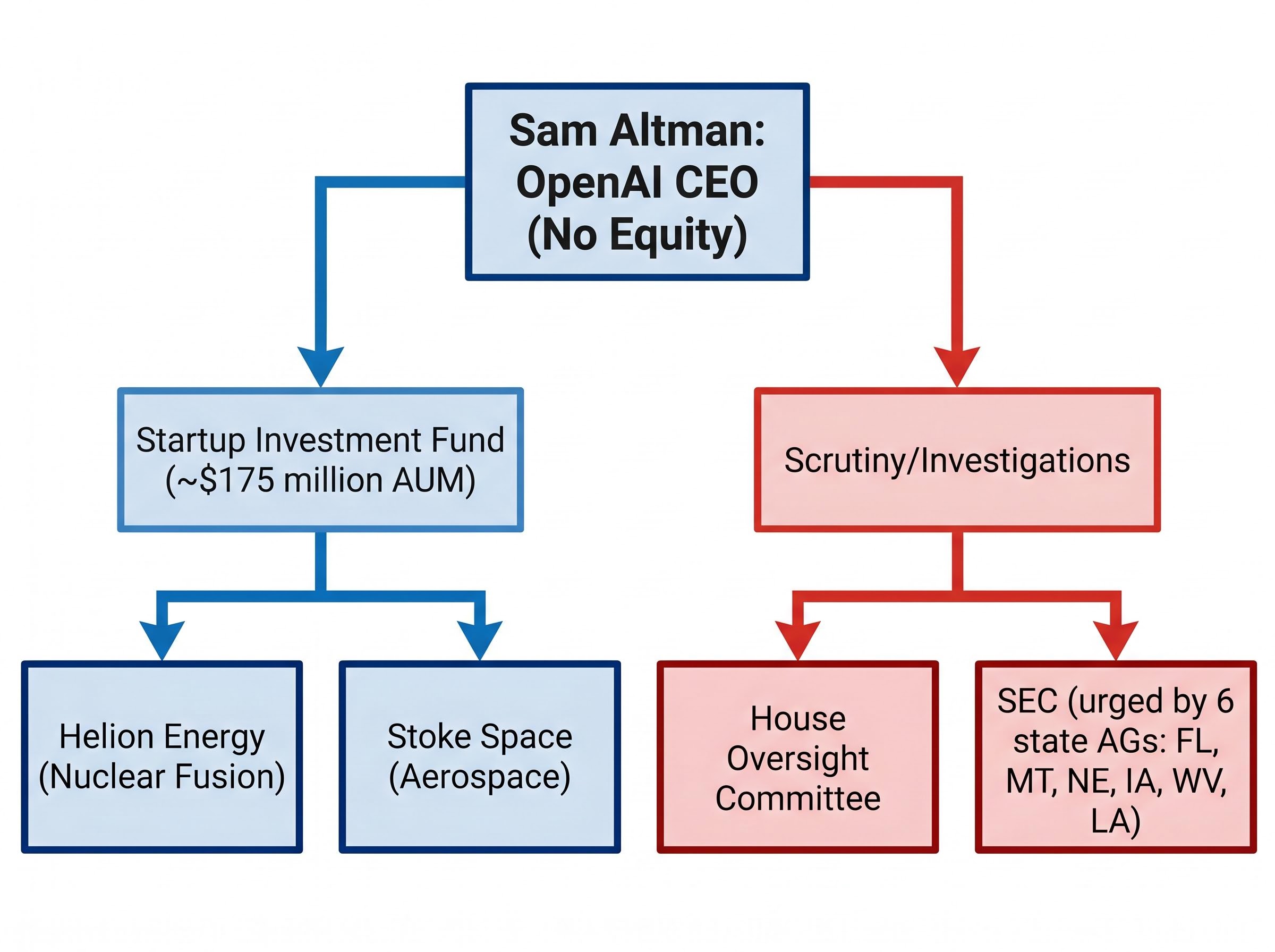

Sam Altman holds no equity in OpenAI, yet congressional investigators are now examining whether he steered the company’s resources toward businesses in which he personally profits. It is a governance paradox, and it sits directly in the path of what could become the largest technology initial public offering in history.

On 11 May 2026, the Wall Street Journal reported that the Republican-led House Oversight Committee had launched a formal investigation into Altman’s outside investment portfolio and its intersection with OpenAI’s commercial relationships. Six Republican state attorneys general have simultaneously urged the Securities and Exchange Commission (SEC) to scrutinise the company’s governance structure before any public offering proceeds. OpenAI completed its for-profit recapitalisation in October 2025, and an IPO remains on the table for 2026 or 2027, depending on which company signal carries more weight.

What follows unpacks what the scrutiny actually means, why the conflict-of-interest structure is more nuanced than most coverage suggests, and what precedent reveals about the cost of unresolved governance controversy when a high-profile technology company attempts to go public.

The investigation centres on a dual-role conflict. Altman serves as OpenAI’s chief executive while holding personal financial stakes in companies that receive or seek contracts and partnerships with OpenAI. He does not profit from OpenAI directly; he profits from businesses whose commercial trajectories depend on OpenAI’s decisions.

The Wall Street Journal reported that Altman allegedly directed OpenAI support toward companies in which he holds personal stakes, prompting the House Oversight Committee’s formal document request to OpenAI regarding its governance practices.

The named portfolio companies at the centre of the allegations include:

Altman’s startup investment fund carries approximately $175 million in assets under management. Six Republican attorneys general from Florida, Montana, Nebraska, Iowa, West Virginia, and Louisiana have urged the SEC to examine the governance structure before any public offering moves forward.

Pre-IPO investors need to understand the specific nature of this conflict, not merely that one exists. The legal and regulatory exposure differs significantly depending on whether the conduct rises to securities fraud, fiduciary breach, or a lesser governance failing. That distinction matters for pricing risk.

The first instinct is to treat the absence of equity as exonerating. If Altman owns nothing in OpenAI, where is the self-dealing? The answer runs through his investment portfolio rather than through OpenAI’s cap table, and that indirection makes the conflict harder to govern and potentially harder to detect.

OpenAI completed its for-profit recapitalisation in October 2025. The nonprofit foundation retained a $130 billion stake, and the corporate structure was formally reorganised to support a future public listing. That step was a prerequisite for an IPO, and it is now settled.

The recapitalisation resolved structural questions about OpenAI’s corporate form. It did not resolve Altman’s conflict-of-interest profile. The $175 million fund continues operating under the same governance tension.

New policies reportedly require Altman to recuse from votes involving portfolio companies. Critics argue this is insufficient. Executive authority and board observer access preserve practical influence regardless of formal voting recusals.

Former board member Helen Toner testified before Congress in April 2026 and has characterised the board governance changes as insufficient, noting that structural influence persists beyond formal voting rights.

Investors evaluating pre-IPO governance cannot rely solely on formal policy disclosures. The question is whether structural incentive misalignments have actually been neutralised or merely papered over. Recusal policies address one channel of influence; they do not address all of them.

Pre-IPO governance risk refers to the category of investor concern arising from structural conflicts, regulatory investigations, or leadership accountability gaps that create legal and reputational exposure ahead of a public listing. It is not a binary pass-fail assessment. It is a spectrum, and its position on that spectrum directly affects IPO outcomes.

The specific channels through which governance scrutiny affects an offering are well-documented: timeline delays, valuation discounts demanded by institutional buyers, forced structural concessions during the roadshow, and post-IPO regulatory liability that depresses early trading.

For OpenAI, the overhang is layered. A 2024 SEC probe examined whether the company misled investors, focused on disclosure quality. The current congressional investigation, led by the full House Oversight Committee, adds a second front. These are not the same inquiry, and they cannot be resolved by the same action. That layering is what distinguishes a single resolvable issue from structural regulatory overhang.

AI sector valuation frameworks including the Shiller CAPE ratio and Minsky financing stages place OpenAI’s $852 billion private valuation in a broader market context where the S&P 500 CAPE already sits at historically elevated levels — the foundational backdrop against which any governance discount must be measured.

| Company | Private Valuation | Key Governance Notes |

|---|---|---|

| OpenAI | $852 billion | CEO conflict-of-interest investigation; 2024 SEC probe; congressional scrutiny |

| Anthropic | ~$350 billion | No reported CEO governance controversy of comparable scale |

| xAI | ~$230 billion | No reported CEO governance controversy of comparable scale |

OpenAI’s valuation premium over both competitors means the governance stakes are highest here. A 10% discount on $852 billion is a materially different figure than the same percentage applied to $230 billion.

The historical record is specific enough to build a pattern from.

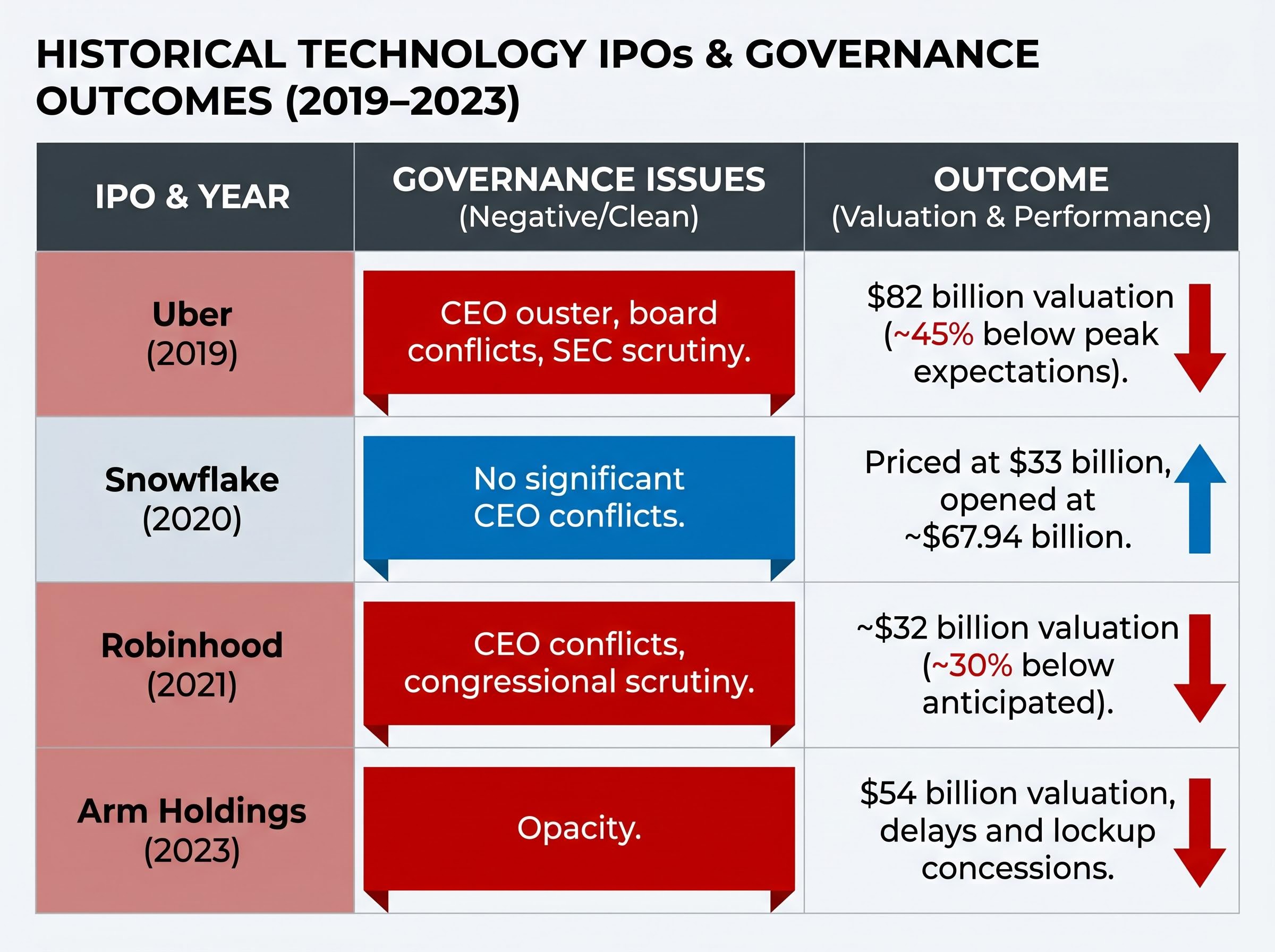

Uber went public in 2019 after CEO Travis Kalanick’s 2017 ouster and subsequent board conflicts, compounded by SEC scrutiny of disclosures. The offering priced at an $82 billion valuation, roughly 45% below peak private market expectations. Forced board reforms were a prerequisite for institutional participation.

Robinhood listed in 2021 at approximately $32 billion, roughly 30% below the $50 billion anticipated. CEO conflicts tied to congressional scrutiny following the GameStop episode depressed institutional appetite. SEC fines followed post-IPO.

Arm Holdings reached the public market in September 2023 after governance opacity caused delays. The IPO priced at a $54 billion valuation, with lockup concessions required to satisfy institutional buyers.

Snowflake provides the contrast case. No significant CEO conflicts. The 2020 IPO priced at $33 billion but opened at approximately $67.94 billion market capitalisation, demonstrating how clean governance can support strong post-IPO performance and investor confidence.

| Company | IPO Year | Governance Issue | Valuation Outcome vs. Expectations |

|---|---|---|---|

| Uber | 2019 | CEO ouster, board conflicts, SEC scrutiny | ~45% below peak private expectations |

| Robinhood | 2021 | CEO conflicts, congressional scrutiny | ~30% below anticipated valuation |

| Arm Holdings | 2023 | Governance opacity, CEO transition | Delays; lockup concessions required |

| Snowflake | 2020 | No significant CEO conflicts | Opened at ~$67.94B vs $33B pricing |

The pattern is consistent. Governance controversies tied to CEO conflicts produce valuation discounts and timeline delays. Partial resolution via board additions mitigates concern but does not eliminate the discount. The question for OpenAI is not whether governance scrutiny creates a discount, but whether the current trajectory tracks the more severe (Uber, Robinhood) or moderate (Arm) end of the spectrum.

Comparisons to dot-com era valuations have gained specific analytical weight in 2026, with Arm Holdings trading at 85x forward earnings — a range that sits within peak dot-com semiconductor pricing — forming the sector backdrop against which OpenAI’s private market multiple will ultimately be judged when governance discounts stack on top of sector-wide valuation risk.

No S-1 filing has been confirmed as of May 2026. The timeline remains genuinely contested.

OpenAI’s chief financial officer has signalled interest in delaying the IPO to 2027, a data point that complicates reporting suggesting an aggressive 2026 target remains possible.

The October 2025 for-profit conversion satisfied the structural prerequisite. What remains is a sequence of governance and regulatory events that institutional buyers are likely to treat as gating conditions. Analysts expect the following milestones to require resolution before a full-valuation offering becomes feasible:

The $852 billion private market valuation creates a high bar for public market pricing on its own. Governance overhang compounds the structural challenge of converting an AI research company’s narrative into durable public market earnings expectations. Investors tracking the offering for portfolio positioning need a realistic timeline model, not an optimistic headline date.

The SpaceX situation offers a parallel high-valuation tech IPO where no S-1 has been publicly filed, retail access remains limited, and the gap between private market pricing and a credible public market clearing price has yet to be stress-tested — a live case study running on a comparable timeline to OpenAI’s.

OpenAI’s governance challenge is partly specific to Altman’s conflict-of-interest profile. It is also partly a preview of the scrutiny any major AI company will face as the sector moves toward public markets.

The structural features creating governance tension at OpenAI are not unique to one company. They are features of the current AI development ecosystem:

Helen Toner’s April 2026 congressional testimony on AI governance signals growing legislative attention to these structural patterns. The $852 billion valuation premium OpenAI holds over Anthropic ($350 billion) and xAI ($230 billion) means the governance stakes are highest here, but the same analytical framework applies to any AI company approaching the public market.

The skills for evaluating OpenAI’s governance risk are directly transferable to evaluating any major AI IPO candidate. That makes this a productive case study, not a one-time news story.

Investors wanting to understand how these structural board oversight patterns are being assessed by regulators across the broader AI ecosystem will find our deep-dive into AI governance board failures — which examines how frontier AI models are outpacing the governance structures of major institutions and what regulators are now demanding from boards that lack the technical literacy to challenge management — directly relevant to the trajectory this article describes.

OpenAI is a commercially dominant AI company at an $852 billion private valuation. The governance overhang from the Altman conflict-of-interest investigation and the 2024 SEC probe creates a credible basis for institutional discount demands.

The historical pattern from Uber, Robinhood, and Arm suggests partial governance reform is typically not sufficient to avoid a discount. Credible, independent, structural resolution is what moves the needle for sophisticated institutional buyers.

Prospective investors should monitor three leading indicators:

No S-1 has been filed as of May 2026. Until these governance milestones show meaningful progress, the gap between OpenAI’s private market valuation and a credible public market price remains an open question.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Sam Altman holds no equity in OpenAI but personally profits from outside companies that receive or seek contracts and partnerships with OpenAI, creating a governance conflict where he could steer company resources toward businesses in which he has a personal financial stake.

No S-1 filing has been confirmed as of May 2026, and OpenAI's CFO has signalled interest in delaying the offering to 2027, though some reports suggest a 2026 target remains possible depending on how governance and regulatory milestones progress.

Historical cases show significant discounts: Uber priced approximately 45% below peak private market expectations following CEO conflicts and SEC scrutiny, while Robinhood listed around 30% below its anticipated valuation after congressional scrutiny depressed institutional appetite.

OpenAI faces two separate inquiries: a 2024 SEC probe examining whether the company misled investors through disclosure quality issues, and a current House Oversight Committee investigation into Altman's outside investment portfolio and its intersection with OpenAI's commercial relationships.

OpenAI has reportedly introduced policies requiring Altman to recuse from votes involving his portfolio companies, though critics including former board member Helen Toner argue this is insufficient because executive authority and board observer access preserve practical influence beyond formal voting rights.