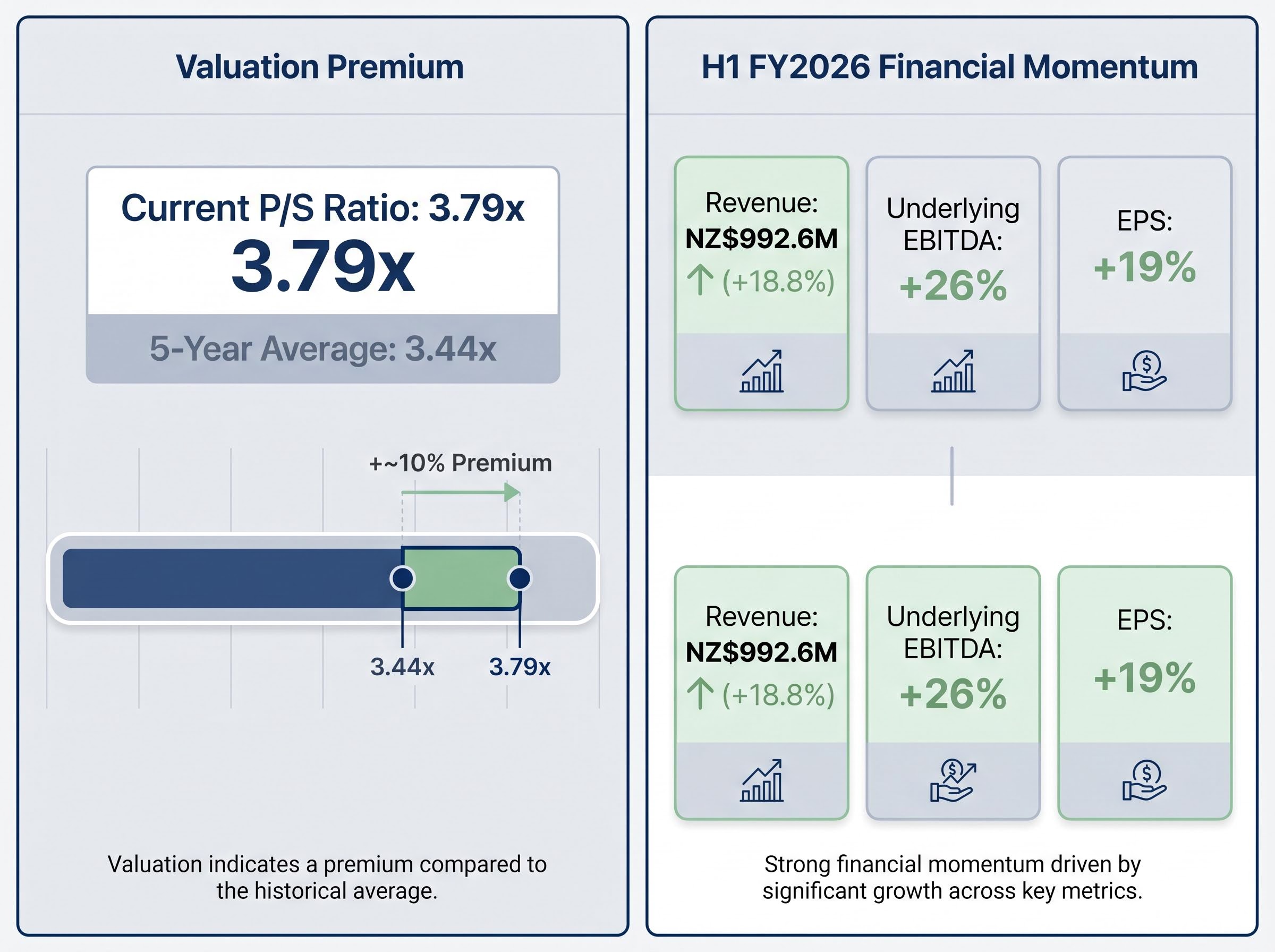

A2 Milk’s share price trades at a price-to-sales (P/S) ratio of 3.79x, roughly 10% above its five-year historical average of 3.44x. That premium might signal confidence in a company that delivered 18.8% revenue growth in the first half of FY2026. It might also signal a market that has not fully absorbed two developments: a guidance downgrade issued on 13 April 2026 citing supply chain challenges, and a voluntary US infant formula recall announced on 2 May 2026. The gap between what investors are paying for each dollar of A2M revenue and what the near-term outlook now supports is the central question for anyone evaluating the stock at current prices. What follows is a framework for reading that signal: why P/S is the appropriate valuation lens, what the financial trajectory looks like, where the risks sit, and what the above-average multiple does and does not tell investors about forward returns.

Why price-to-sales is the right lens for valuing A2 Milk

A2M does not pay a meaningful dividend. Dividend yield, the default screening tool for many ASX-listed consumer staples, tells investors nothing useful here. Earnings multiples such as price-to-earnings (P/E) are distorted by a business model that reinvests aggressively into China e-commerce expansion and brand building rather than maximising near-term profit.

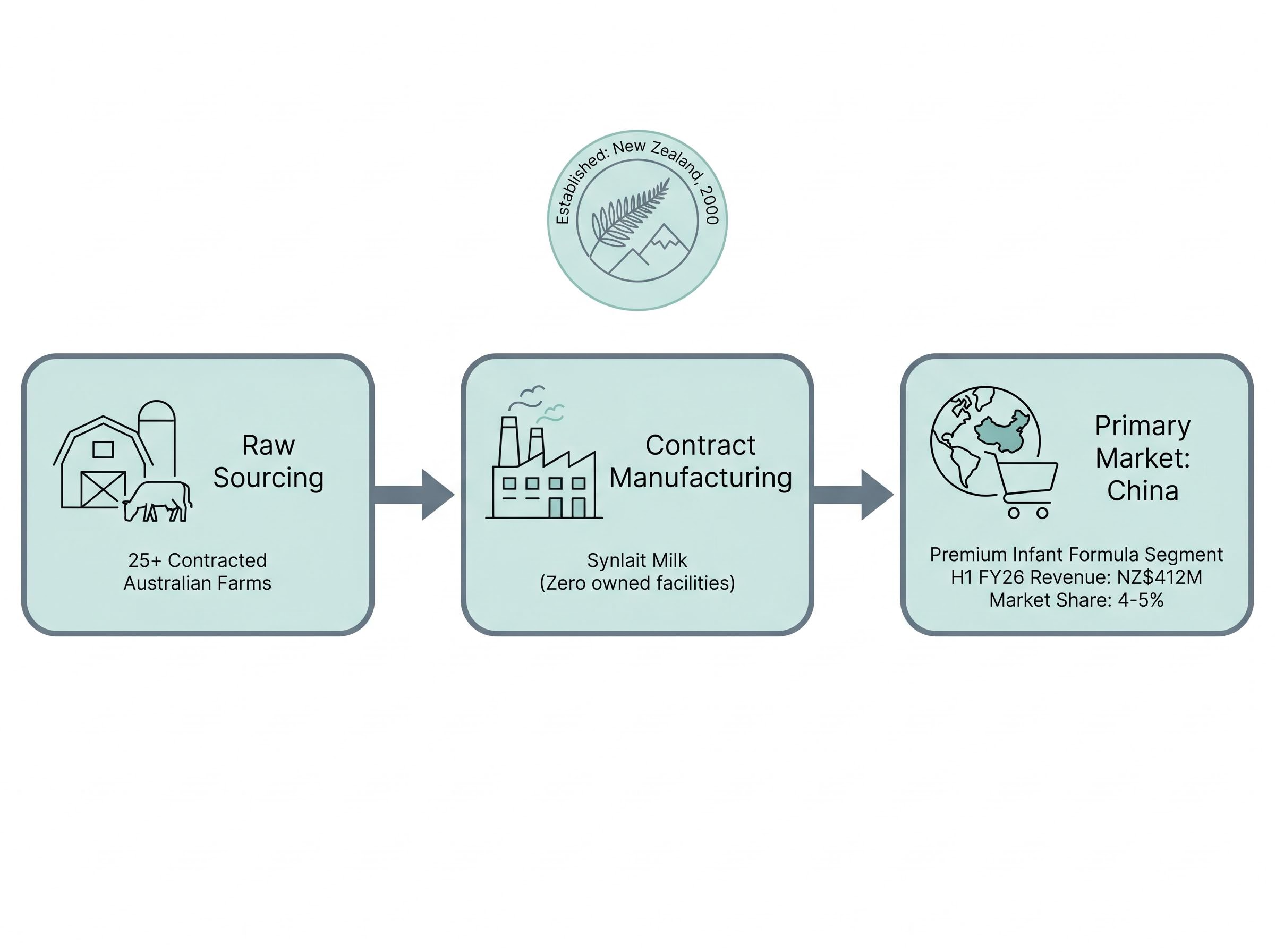

Price-to-sales measures what investors pay for each dollar of revenue. It suits asset-light, brand-driven companies where earnings fluctuate with reinvestment decisions but revenue reflects underlying demand. A2M operates via 25+ contracted Australian farms and manufactures through Synlait Milk, carrying no heavy capital base that would distort earnings multiples.

Three valuation metrics compared for A2M:

- Dividend yield: Not applicable; the company is in a growth reinvestment phase with no meaningful dividend

- P/E ratio: Distorted by variable reinvestment spend and margin expansion timing; useful as a secondary check, not a primary screen

- P/S ratio: Reflects demand-side momentum directly; most appropriate for brand-led, asset-light consumer businesses

A2M’s current P/S of 3.79x sits approximately 10% above its five-year historical average of 3.44x.

P/S is a screening tool, not a standalone verdict. It works best when compared against a company’s own historical range rather than cross-sector benchmarks.

P/S ratio is one of five core fundamental analysis metrics that investors in brand-driven consumer businesses should read together, because a premium multiple only carries meaning once revenue growth, margin trajectory, and return on equity have been assessed against sector peers.

When big ASX news breaks, our subscribers know first

What A2 Milk actually is and why the premium segment matters

A2 Milk Company, established in New Zealand in 2000, produces and markets dairy products sourced exclusively from cows that naturally produce only A2 beta-casein protein. Standard dairy contains a mixture of A1 and A2 proteins; A2-only products are marketed as being easier to digest for consumers sensitive to conventional dairy. This protein distinction is the foundation of the company’s brand premium.

The operating model is deliberately light on physical assets. A2M owns no farms and no manufacturing facilities. Revenue is generated by brand positioning, product formulation, and distribution, with Synlait Milk serving as the contract manufacturer for its infant formula range.

China’s premium infant formula segment is the financial centre of gravity. In H1 FY2026, China revenue reached NZ$412 million, up 15% year-on-year. The company holds an estimated 4-5% share of China’s premium infant formula market. Full-year FY2025 revenue was NZ$1.90 billion, up 14% year-on-year.

Three pillars underpin A2M’s competitive positioning:

- A2 protein differentiation: a science-backed product claim that supports premium pricing in a crowded market

- Asset-light model: no owned farms or manufacturing, reducing capital intensity and amplifying margin leverage on revenue growth

- China premium segment exposure: the largest and fastest-growing revenue stream, driven by consumer willingness to pay for imported infant formula brands

The financial momentum behind the current valuation

The H1 FY2026 results, published on 16 February 2026, represent the most recent confirmed earnings data point. Revenue reached NZ$992.6 million, up 18.8% year-on-year. Underlying EBITDA (earnings before interest, tax, depreciation, and amortisation, a measure of operating profitability before accounting adjustments) grew 26% year-on-year. Earnings per share rose 19%.

| Metric | FY2025 Full Year | H1 FY2026 | YoY Change |

|---|---|---|---|

| Revenue | NZ$1.90 billion | NZ$992.6 million | +18.8% (H1) |

| NPAT / Underlying EBITDA | NZ$202.9 million (NPAT) | Underlying EBITDA up 26% | +21% (FY25 NPAT) / +26% (H1 EBITDA) |

| EPS | Not separately disclosed | Up 19% | +19% (H1) |

The 52-week low of approximately A$4.88, reached in October 2025, and the subsequent recovery into early 2026 reflected genuine business improvement. China demand strengthened, H1 results beat expectations, and management reaffirmed FY26 guidance at the time of the February release.

Analyst consensus as of May 2026: Moderate Buy, average price target A$8.71, implying approximately 33% upside from current levels (range: A$6.75 to A$9.90).

That consensus, sourced from TipRanks, predates the full market absorption of the April guidance downgrade and the May recall. Whether it holds will depend on the developments outlined in the next section.

The risks that complicate the growth premium

The 13 April 2026 trading update was the most material near-term development. Management lowered FY26 full-year guidance, citing supply chain challenges. This was a concrete adverse event: guidance had been reaffirmed just two months earlier at the H1 results, and the revision signals that supply-side pressures became more severe than management anticipated.

The April guidance revision was driven by five converging supply constraints operating simultaneously, including Synlait manufacturing backlogs, enhanced cereulide testing requirements, freight capacity disruption linked to Middle East conflict, elevated demand from competitor recalls, and higher Chinese customs inspection rates, each of which management characterised as a timing issue rather than a structural demand problem.

On 2 May 2026, A2M announced a voluntary recall of approximately 16,000 units of a2 Platinum USA-label infant formula across three batches, due to possible cereulide toxin risk. The recalled product was from a discontinued line. No confirmed illnesses were reported, and the US Food and Drug Administration (FDA) published a formal recall notice. The recall was isolated to the US market with no China regulatory impact.

The FDA recall notice for A2 Platinum infant formula confirms that the affected batches were limited to a discontinued USA-label product line, with no confirmed illnesses reported and no regulatory action extending to A2M’s China or Australian market products.

Competition in China continues to intensify. Domestic brands Feihe and Yili have gained an estimated 2-3% market share in the premium infant formula segment through localisation strategies and Tmall investment. Dairy tariff-related supply shortages have also created input cost headwinds.

Four risk categories investors should weigh:

- FY26 guidance revision: full-year outlook lowered in April 2026, citing supply chain challenges

- US recall: voluntary, isolated to a discontinued product line, but sentiment-damaging and subject to ongoing FDA scrutiny

- China competitive pressure: Feihe and Yili gaining share in the premium segment via localisation and e-commerce

- Synlait supply chain uncertainty: merger talks between Synlait and Synergy (initiated approximately October 2025) could consolidate manufacturing supply but carry execution risk

Perpetual commentary (approximately 3 May 2026): “Asset-light model intact, but monitor Synlait/Synergy talks.”

The next major ASX story will hit our subscribers first

What trading above a historical average P/S actually means in practice

A P/S ratio above a long-term average can mean two different things. It can reflect a genuine growth premium, where the market is pricing in an acceleration in revenue growth that justifies paying more per dollar of current sales. Or it can reflect a valuation stretch, where the market has moved ahead of fundamentals.

The distinction depends on the direction of revenue growth. For A2M, revenue growth was 14% in FY2025, accelerating to 18.8% in H1 FY2026. That acceleration supported the premium. The April guidance downgrade now introduces genuine uncertainty about whether the acceleration continues through the second half.

The expectations gap concept is central to reading A2M’s April guidance cut correctly: the share price reaction was not driven by the absolute level of revised earnings but by the distance between what management had signalled in February and what the trading update revealed two months later.

The analyst price target range of A$6.75 to A$9.90 reflects that disagreement directly. The gap between the lowest and highest target is nearly 47%, an unusually wide spread that signals genuine analytical divergence about the forward trajectory.

How to apply the P/S signal in context

- Compare to own history: A2M’s 3.79x sits 10% above its 3.44x five-year average, a moderate rather than extreme premium

- Assess whether revenue growth justifies the premium: H1 FY2026 growth of 18.8% supported it; the April guidance cut calls it into question

- Cross-check with a forward-looking method: discounted cash flow analysis or scenario-based revenue modelling provides the structural view that a single ratio cannot

No single ratio provides a buy or sell verdict. P/S is most valuable as a starting diagnostic, not a conclusion.

A2 Milk’s premium multiple reflects real growth, but the margin for error has narrowed

A2M’s P/S premium over its historical average is supported by genuine revenue growth acceleration in H1 FY2026. The 18.8% top-line growth and 26% EBITDA expansion were real, confirmed by ASX filings. The analyst consensus of Moderate Buy with an average target of A$8.71 reflects a market that, as recently as February, saw the trajectory continuing.

The April guidance cut and supply chain pressures changed the equation. Investors are now paying an above-average multiple at precisely the moment forward visibility has declined. The US recall, while isolated, added a layer of sentiment risk that had not been present when the share price was recovering from its October 2025 low.

Three forward indicators will determine whether the current premium proves justified:

- FY2026 full-year results (expected approximately August 2026): whether the guidance downgrade proves conservative or accurate

- Updated analyst consensus post-guidance downgrade and post-recall, particularly from UBS and Macquarie

- Synlait-Synergy merger status: resolution or escalation of supply chain consolidation risk

A stock trading above its historical average P/S is a signal worth investigating, not a verdict in itself. For A2M, the investigation points to a company where the growth case remains structurally intact but the near-term execution risk has increased. Investors considering the stock at current levels would benefit from waiting for the FY2026 full-year data before forming a firmer view.

Investors wanting broader market context for why guidance cuts are landing harder in 2026 than in prior years will find our full explainer on the ASX earnings downgrade cycle useful; it maps the 25 ASX 200 companies still flagged as downgrade risks alongside the macro pressures, including 4.6% CPI and RBA rate trajectory, that are compressing multiples across consumer staples.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.