The ASX 200 has now fallen for six consecutive sessions and turned negative for calendar year 2026, as a widening wave of corporate guidance cuts strips away the earnings assumptions that had underpinned Australian equities heading into May. This is not a single company stumbling. Across retail, healthcare, financials, industrials, and consumer staples, ASX-listed businesses are simultaneously revising their FY26 profit expectations downward.

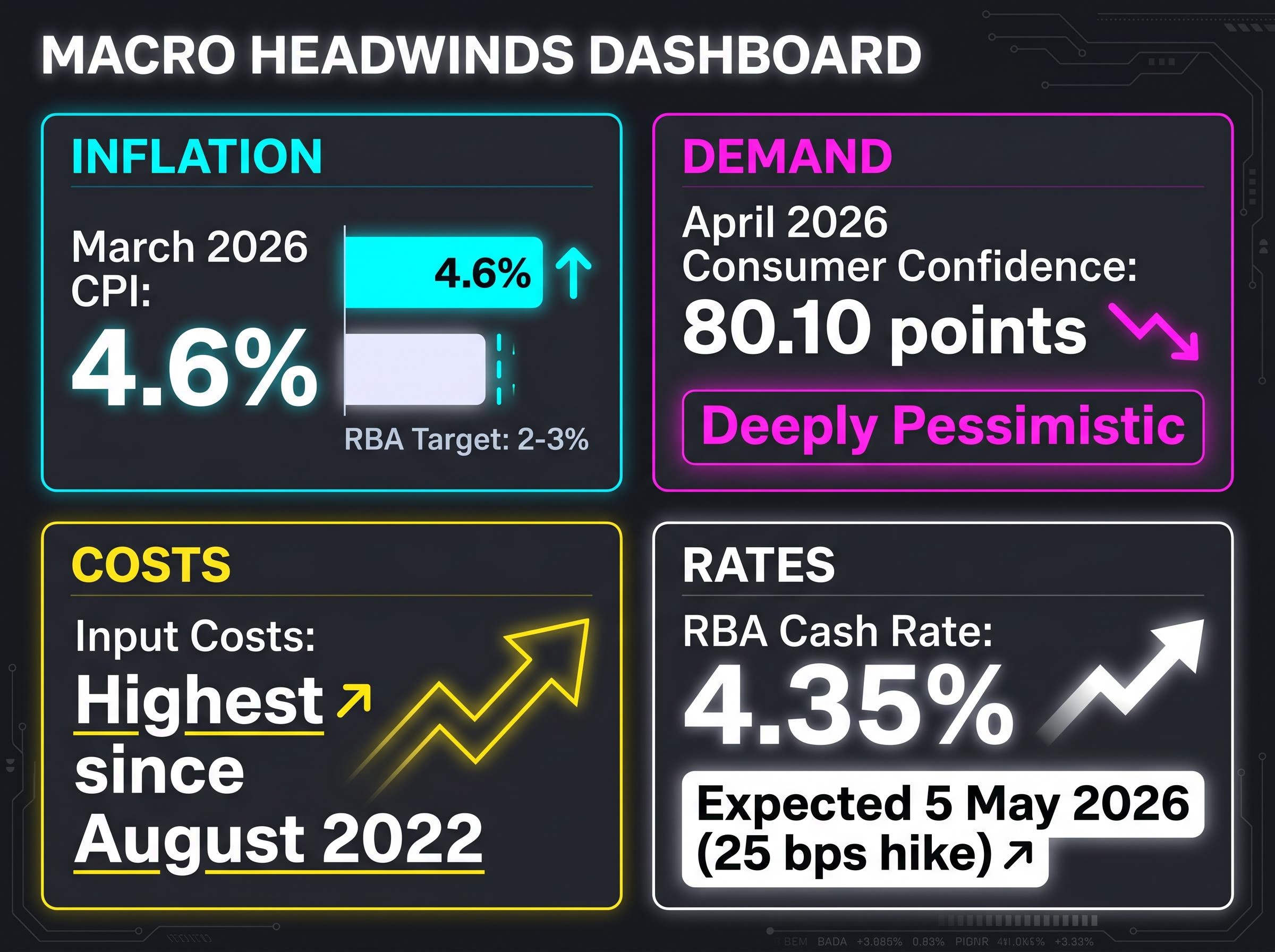

The drivers are overlapping and self-reinforcing: input cost inflation at its highest since August 2022, Middle East-linked disruption to freight and fuel, an RBA expected to hike rates for the third consecutive meeting, and consumer confidence sitting at a deeply pessimistic 80.10 points. What follows maps which companies have cut guidance, which sectors are most exposed, what macro forces are doing the damage, and what the aggregate earnings picture looks like for investors navigating Australian equities right now.

A market in retreat: what the ASX 200’s six-day losing streak is telling investors

Six consecutive days of losses have pushed the ASX 200 into negative territory for the calendar year, and the decline has a clear fundamental fingerprint. The sectors dragging the index lower are precisely those where guidance cuts have been most concentrated: retail, healthcare, and industrials.

ASX market breadth tells a sharper story than the headline index move: in the week ending 1 May 2026, 22 ASX 200 constituents hit fresh 52-week lows even as the weekly loss registered just 0.65%, with Consumer Discretionary contributing 7 new annual lows and Healthcare contributing 5, including Cochlear and CSL, confirming the downgrade pressure is concentrated in precisely the sectors flagged in this cycle.

- Index close on 5 May 2026: 8,626 points, down 0.82% on the session

- Weekly decline: approximately 2.5% in the first week of May

- Consecutive losing sessions: six

- Year-to-date status: negative for calendar year 2026

Historical context sharpens the signal. Since 1980, the ASX 200 has averaged a May gain of just 0.17%; over the past decade that figure improves only to 0.51%. The May-to-October half of the year produces average returns of 0.37%, compared with 5.78% for November-to-April. Even in a good year, May offers little tailwind. In a downgrade cycle, it offers none.

UBS equity strategists have stated explicitly that it is “too early to buy the ASX 200 dip,” warning that the downgrade cycle has further to run.

When big ASX news breaks, our subscribers know first

The companies that have already cut: a sector-by-sector breakdown

The pattern emerges company by company. In retail, Accent Group downgraded guidance on 4 May citing softer trading conditions. Adairs received a broker downgrade from Bell Potter the same day on margin pressure. Endeavour Group reported half-to-date FY26 retail sales growth of just 0.7%, down from 1.3% at the February half-year, while its Hotels division moderated to 3.7% growth from 4.5%. EVT flagged emerging softness in consumer demand.

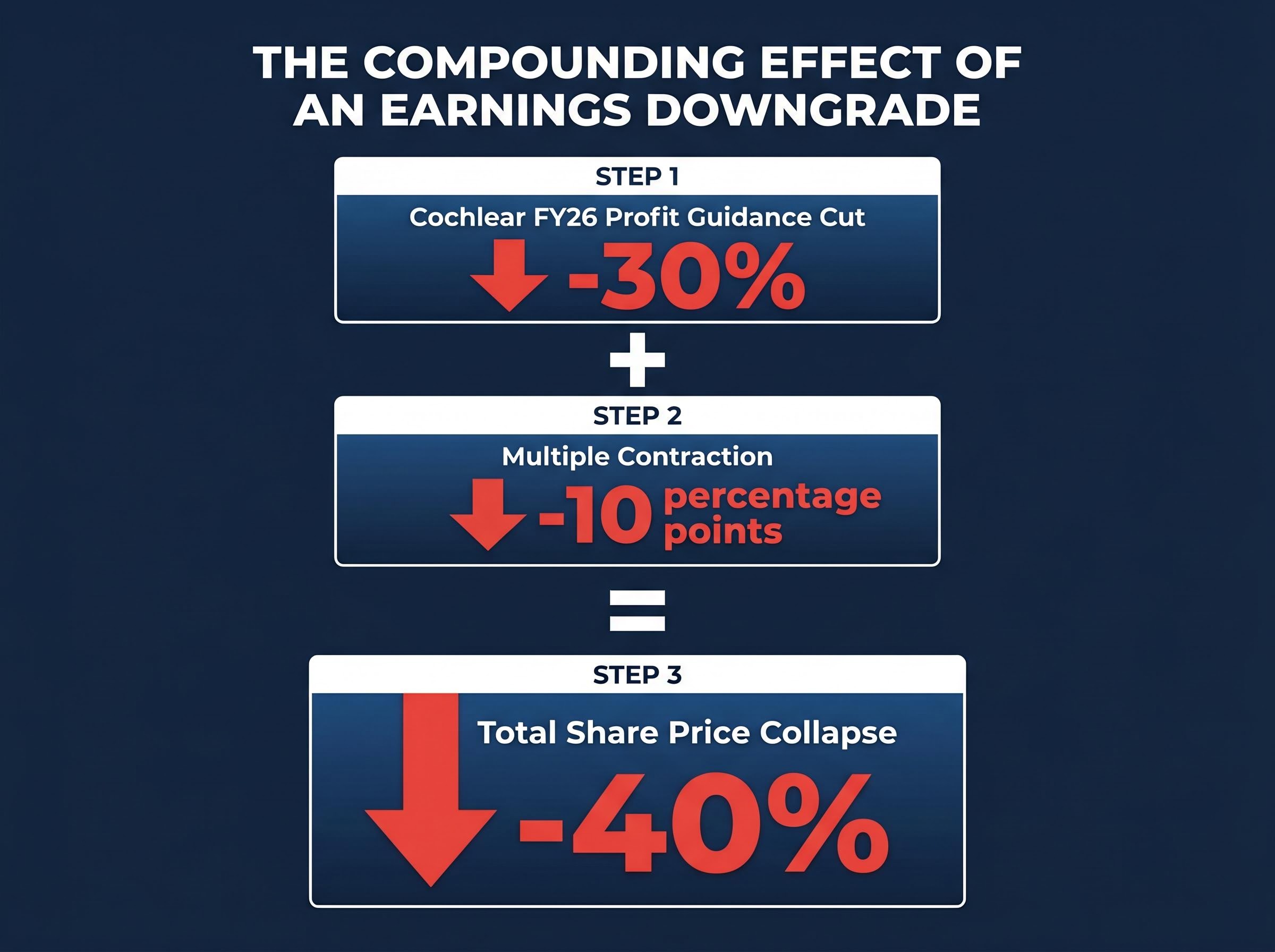

In healthcare, the damage has been severe. Cochlear cut its FY26 underlying profit guidance by approximately 30%, triggering a roughly 40% single-session share price collapse. CSL and Pro Medicus also featured in February 2026 downgrade commentary.

Financial sector names are not immune. Westpac cited weaker revenues from treasury margin compression and a larger impairment charge. NAB increased impairment charges on geopolitically exposed segments. Judo Capital maintained guidance at the lower boundary with an economic conditions provision, while Iress guided FY26 revenues toward the lower end of its range citing macro and geopolitical risks.

Across industrials and services, Cleanaway reduced guidance on 14 April, sending its $5 billion market cap to a 52-week low. Worley flagged clients deferring contract initiation. Orora issued materially reduced EBIT guidance. Fletcher Building noted Middle East exposure without yet quantifying the financial impact.

In airlines, Air New Zealand withdrew its full-year earnings guidance entirely. Qantas and Virgin flagged near-term profit headwinds from higher jet fuel costs. Consumer staples saw a2 Milk revise FY26 NPAT guidance to similar to or below the prior year due to elevated air freight costs, while Woolworths indicated its FY26 Australian Food EBIT growth would miss the upper portion of its mid-to-high single-digit guidance range. In energy, LGI was downgraded by Bell Potter on 4 May citing falling energy prices, and EBOS lowered guidance the prior month.

| Company | Sector | Guidance Action | Stated Driver |

|---|---|---|---|

| Cleanaway | Industrials | Reduced guidance (14 Apr) | Cost inflation; share price hit 52-week low |

| Accent Group | Retail | Downgraded guidance (4 May) | Softer trading conditions |

| Cochlear | Healthcare | ~30% profit guidance cut | Operational miss; ~40% share price fall |

| Westpac | Financials | Weaker revenue guidance | Treasury margin compression; impairment charge |

| a2 Milk | Consumer Staples | NPAT guidance revised down | Elevated air freight costs |

| Woolworths | Consumer Staples | EBIT growth guidance trimmed | Fuel cost exposure in Q4 |

| Air New Zealand | Airlines | Full-year guidance withdrawn | Jet fuel cost uncertainty |

| Worley | Industrials | Flagged contract deferrals | Client caution on new awards |

| Orora | Industrials | Materially reduced EBIT guidance | Cost and demand pressures |

| Endeavour Group | Retail / Hospitality | Sales growth deceleration flagged | Consumer demand softness |

| EVT | Hospitality / Leisure | Emerging softness flagged | Consumer demand weakness |

| LGI | Energy | Broker downgrade (Bell Potter, 4 May) | Falling energy prices |

- Ridley Corp and Nufarm both reported minimal disruption to their operations, standing as notable exceptions within the broader downgrade cycle.

Why guidance is getting cut: the cost and demand forces driving the cycle

The company-level pattern points to a shared set of pressures rather than isolated corporate failures. Two structural forces are doing the damage, and they are reinforcing each other.

On the cost side, input prices have surged. The April 2026 S&P Global PMI showed Australian input costs climbed to their highest level since August 2022, driven primarily by fuel and shipping. Businesses have now faced rising input costs for three consecutive months. Charge inflation, the costs passed through to customers, reached its highest point in three and a half years.

Second-round fuel cost pass-through through freight, construction materials, and services is expected to become most visible in Q2 and Q3 CPI data, with new dwelling purchase costs already accelerating sharply in March 2026, suggesting the 4.6% headline figure may understate the breadth of underlying price pressures facing businesses.

On the demand side, consumers are pulling back. Consumer confidence sat at 80.10 points in April 2026, a reading that indicates deeply pessimistic sentiment and consistent headwinds for discretionary spending.

- Inflation: Annual CPI reached 4.6% as of March 2026, the highest since September 2023 and well above the RBA’s 2-3% target band

- Input costs: Three consecutive months of increases; fuel and shipping the primary drivers

- Consumer confidence: 80.10 points in April, deeply pessimistic

- Interest rates: The RBA is expected to raise the cash rate by 25 basis points to 4.35% on 5 May 2026, the third consecutive hike and a full reversal of the prior year’s rate reductions

Australia’s annual inflation reached 4.6% as of March 2026, the highest since September 2023 and well above the RBA’s 2-3% target band.

UBS has identified the Middle East conflict as the upstream cause, flagging stagflation risk as the central macro threat to 25 ASX 200 companies. Higher borrowing costs from the RBA’s rate path compound the problem, squeezing margins for leveraged businesses while simultaneously suppressing the discretionary spending that consumer-facing companies rely on.

What ASX earnings downgrades mean and how they move share prices

An earnings guidance downgrade occurs when a company tells the market it now expects to earn less than it previously communicated. On the ASX, these disclosures are governed by continuous disclosure obligations, meaning a company must inform the market as soon as it becomes aware of a material change to its expected financial performance.

ASX Listing Rules Guidance Note 8 on continuous disclosure sets out exactly when a company is required to notify the market of a material change to its earnings guidance, including the immediacy obligation that applies once management becomes aware of a significant deviation from previously communicated expectations.

How a guidance cut becomes a share price collapse

The share price reaction to a downgrade is often larger than the earnings cut itself. This happens through a compounding mechanism:

- The company announces a reduction in expected profit, and consensus earnings estimates across analyst coverage fall to reflect the new guidance

- At the same time, the price-to-earnings multiple that the market applies to those earnings contracts, because investors demand a discount for increased uncertainty

- The combined effect, lower earnings multiplied by a lower multiple, produces a share price decline that can significantly exceed the percentage earnings cut

Cochlear illustrated this precisely. A roughly 30% cut to FY26 underlying profit guidance produced an approximately 40% single-session share price collapse. The additional 10 percentage points of decline reflected the multiple contracting alongside the earnings base. Cleanaway’s 14 April downgrade sent its shares to a 52-week low despite the company’s $5 billion market capitalisation, demonstrating that size offers no insulation.

Company downgrades vs broker downgrades: what each signals

A company-issued guidance cut is management telling the market directly that conditions have deteriorated. A broker-issued downgrade, such as Bell Potter’s calls on Adairs and LGI on 4 May, signals that an external analyst has concluded current consensus earnings estimates are too optimistic. Broker downgrades often precede or anticipate a formal company guidance revision, making them an early warning signal for investors monitoring portfolio exposure.

The FY26 earnings outlook: where growth is hiding and where it is not

Macquarie forecasts 10.5% FY26 ASX earnings growth, a figure that looks healthy until the composition is examined. The headline is concentrated overwhelmingly in resources and banking, sectors that are not experiencing the same downgrade dynamics as industrials and consumer-facing businesses.

Macquarie’s 10.5% FY26 ASX earnings growth forecast is led by the resource sector, with elevated copper prices, steady iron ore, sharply higher gold year-on-year, and broad energy complex strength providing the tailwind.

| Sector Group | FY26 Earnings Outlook | Key Companies or Drivers |

|---|---|---|

| Resources | Positive | Elevated copper, gold, iron ore; broad energy strength |

| Banking | Cautious positive | Margin pressure but stable overall; impairment charges rising |

| Industrials | Negative | Worley, Orora, Cleanaway; cost inflation, contract deferrals |

| Consumer Discretionary | Negative | Accent Group, EVT, Endeavour Group; demand softness |

| Healthcare | Negative | Cochlear guidance cut; CSL and Pro Medicus under pressure |

Morningstar offers a more constructive longer-term view, noting that FY26 growth follows three consecutive years of earnings declines and that the February 2026 results season came in broadly in line with historical averages. That said, UBS flags 25 ASX 200 stocks at risk of further downgrades amid stagflation and geopolitical pressures, suggesting the deterioration in industrials, consumer, and healthcare sectors may not yet be fully reflected in consensus numbers.

Investors tracking the index through passive strategies may find the resources and banking concentration provides a buffer. Stock-pickers in industrials and consumer sectors face a materially different earnings environment than the headline growth number implies.

NAB’s H1 FY26 cash earnings beat of 7.1% illustrates the risk of reading headline results at face value, with credit impairment charges simultaneously surging 45.6% to $706 million, a pattern of earnings quality deteriorating beneath a surface beat that repeats across the current reporting season and carries direct implications for how investors should read consensus growth forecasts.

The downgrade cycle still has room to run, and here is what to watch

UBS has been unambiguous: it is “too early to buy the ASX 200 dip.” With 25 ASX 200 companies still flagged as downgrade risks, the weight of near-term evidence sits on the side of further deterioration rather than stabilisation.

Three forward indicators will most directly signal whether the cycle is broadening or peaking:

- RBA rate decision and forward guidance: The expected 25 basis point hike to 4.35% on 5 May is largely priced in, but the accompanying forward guidance will determine whether markets need to price further tightening

- Freight and fuel cost trajectory: Resolution or escalation of the Middle East conflict will directly influence the input cost pressures that have driven margin compression across multiple sectors

- May consumer confidence reading: The April figure of 80.10 points was deeply pessimistic; the direction of the May reading will indicate whether consumer demand headwinds are stabilising or intensifying

The RBA’s forward guidance accompanying the May decision is the primary market-moving element, not the hike itself: with Westpac forecasting a terminal rate of 4.85% via further hikes in June and August and derivative markets implying close to 5.00% by year-end, the gap between consensus and hawkish scenarios represents a live risk for rate-sensitive portfolios across the industrials, consumer, and healthcare sectors already under earnings pressure.

Datt Research has specifically warned that small-cap ASX stocks face amplified downgrade risk in the energy shock environment, giving investors in sub-index strategies an additional consideration.

The next CPI reading will also clarify whether the 4.6% March inflation figure represents a peak or a continued climb, a distinction with direct implications for the RBA’s rate path and the earnings cycle that depends on it.

The earnings season scorecard is still being written

The wave of ASX earnings downgrades sweeping retail, healthcare, financials, industrials, and consumer staples reflects an overlapping set of macro pressures, from 4.6% inflation to Middle East-driven cost shocks to an RBA hiking into demand weakness, that are unlikely to resolve quickly. The headline 10.5% FY26 earnings growth forecast conceals material sector divergence: resources and banking are the growth anchors, while industrials, consumer discretionary, and healthcare face ongoing compression.

The three indicators outlined above, the RBA’s forward guidance, the freight and fuel cost trajectory, and the May consumer confidence reading, offer the clearest signals for when conditions may stabilise. As the RBA’s 5 May decision and its accompanying commentary become public, the next chapter of this downgrade cycle will begin to take shape.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.