KOSPI Drops 10% as Crowded AI Trade Unwinds Across Global Markets

3 hrs ago

A single overnight military exchange in the Strait of Hormuz erased an estimated $100 billion in Australian market capitalisation on 8 May 2026, reversing the prior session’s gains entirely. The ASX 200 recorded its steepest single-session fall in seven weeks, dropping 181.1 points (2.04%) to close at 8,697, with declining stocks outnumbering advancers 217 to 69 across the ASX 300. The selloff is analytically interesting rather than routine: US equities had closed higher the night before, with the S&P 500 up 1.46% and the Nasdaq gaining 2.02%. What follows is an analysis of how a geopolitical event in the Middle East translated into selling pressure across Australian financials, real estate, and energy stocks, and which corners of the market held firm.

The S&P 500 closed at 7,365.12 on 7 May, up 1.46%. The Nasdaq added 2.02%. Ordinarily, that would set the ASX up for a positive session. Instead, the index fell 2.04% before lunch.

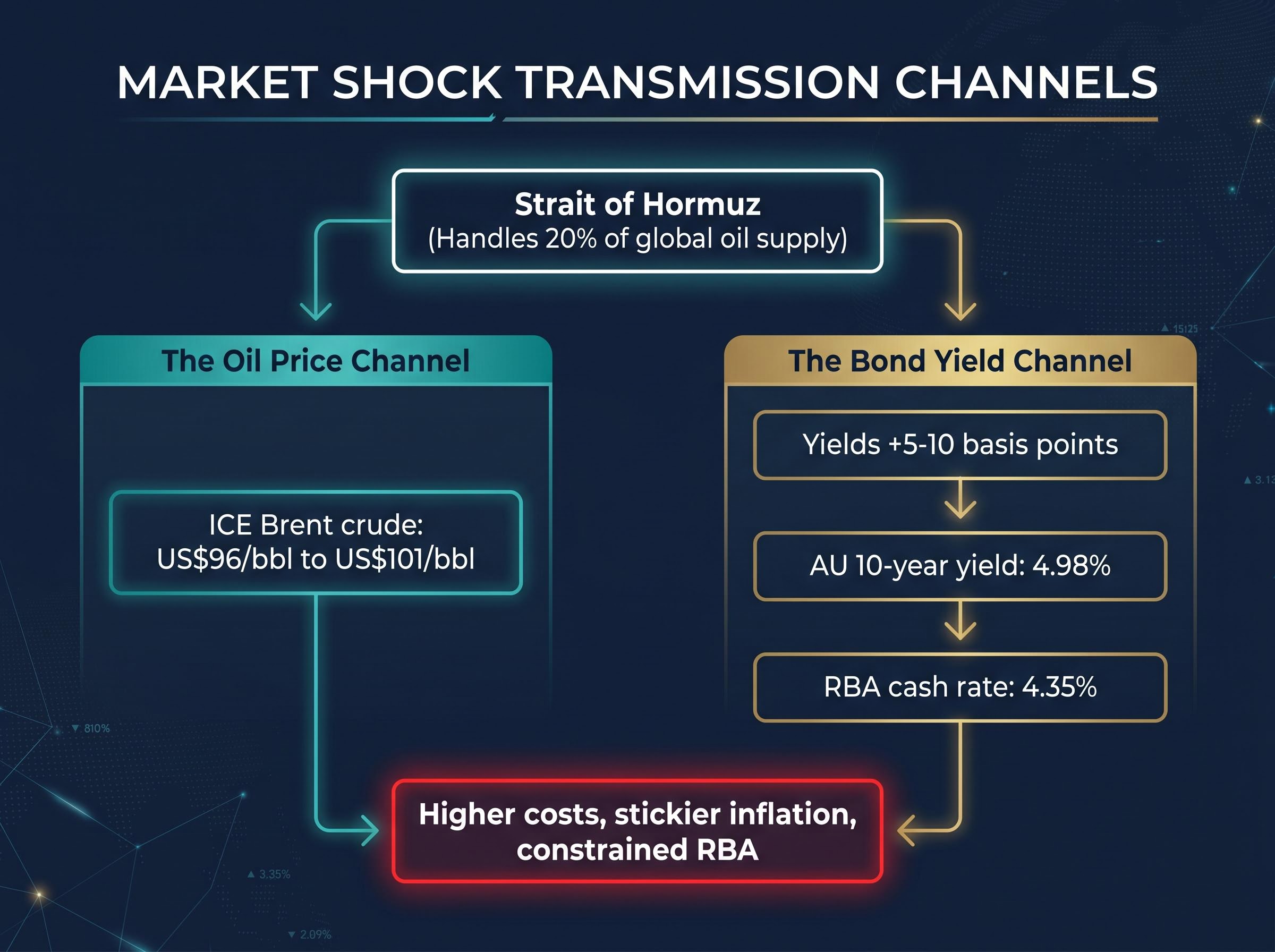

The disconnect traces to two transmission channels that activated simultaneously overnight. US interception of Iranian attacks was followed by retaliatory strikes on Iranian military infrastructure, reigniting tensions in the Strait of Hormuz, a chokepoint handling approximately 20% of global oil supply.

Both channels fed the same conclusion: higher costs, stickier inflation, and a more constrained Reserve Bank of Australia (RBA).

The Hormuz oil risk premium is not expected to snap back even under a ceasefire scenario; the IEA projects a two-year supply chain recovery timeline, and the near-total withdrawal of commercial war-risk insurance means commercial transit remains effectively closed even when physical passage is technically possible.

The RBA has characterised Middle East supply shocks as a “clear near-term inflationary impulse.”

That characterisation matters. It signals the central bank views these disruptions not as transient noise but as a factor weighing on its rate path.

The RBA May 2026 monetary policy decision explicitly flagged that developments in the Middle East are contributing to inflation, with higher fuel prices creating second-round effects on goods and services prices more broadly, providing the policy context behind market sensitivity to any further Hormuz escalation.

The overnight yield move, 5-10 basis points higher, may look modest in isolation. At an Australian 10-year government bond yield of 4.98%, with the RBA cash rate already at 4.35%, the incremental tightening lands on an already pressured rate structure. Understanding why this hits certain sectors disproportionately requires two related but distinct mechanisms.

The RBA rate decision on 5 May raised the cash rate to 4.35% with an 8-1 vote, making Australia’s central bank the most aggressive in the developed world by a margin of up to 235 basis points against peers that held steady; that divergence directly amplifies the yield sensitivity that made Australian financials and real estate the session’s weakest sectors.

Bond-proxy sectors are income-generating equities, banks, real estate investment trusts (REITs), and utilities, whose dividend yields compete directly with risk-free government bond yields. When those risk-free yields rise, the spread between a bank’s 5% dividend and a government bond’s return compresses, making the equity less attractive on a relative yield basis.

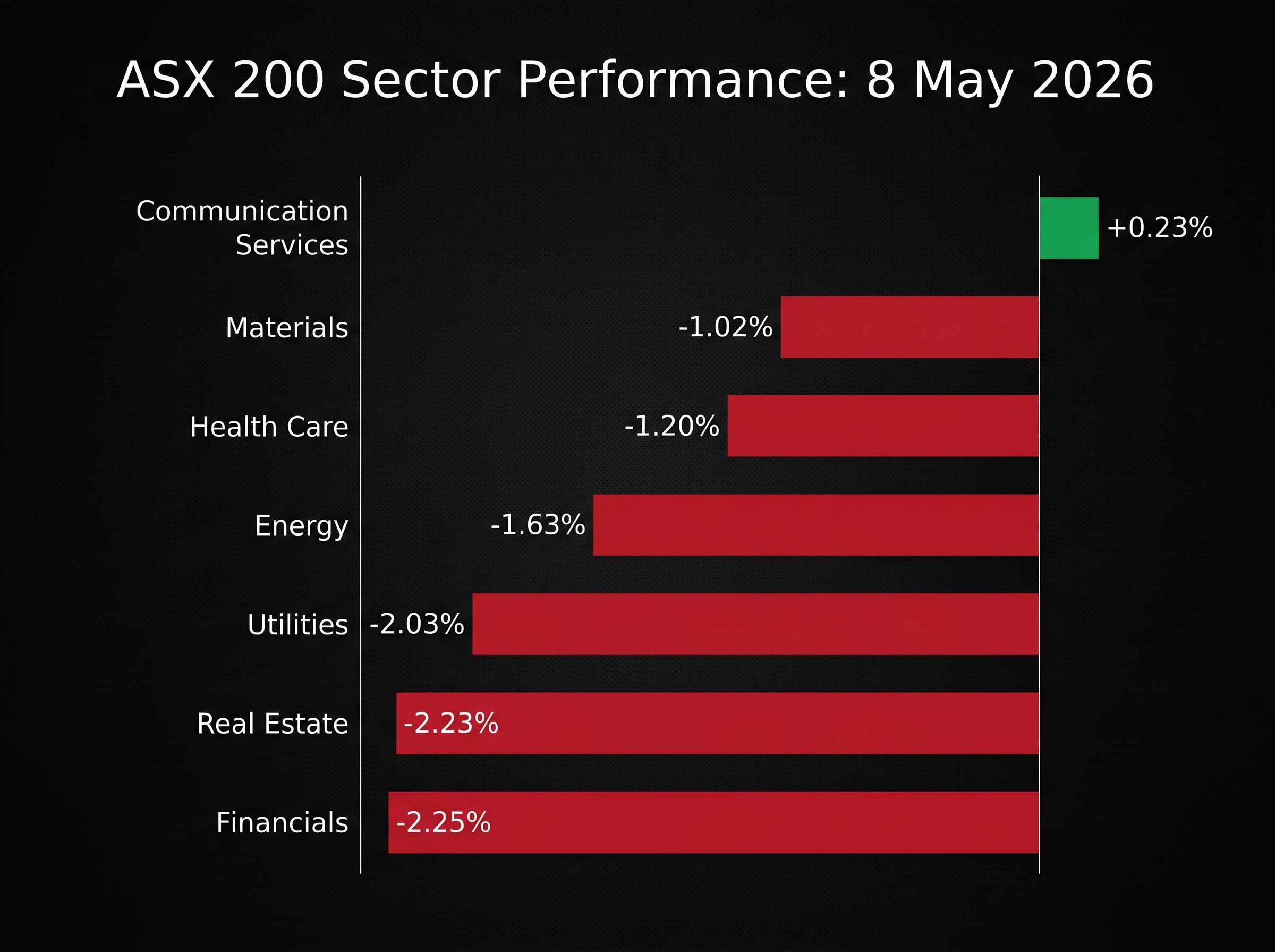

Financials and real estate were the joint-weakest sectors on 8 May, consistent with this mechanism.

High price-to-earnings technology and healthcare names with earnings projected years into the future suffer disproportionately because each future cash flow is worth less in present-value terms when the discount rate climbs. A 5-10 basis point move may appear small, but across a decade of projected earnings, the compounding effect on valuations is material.

The abstract mechanism showed up in concrete numbers across the session. Financials led the decline, followed closely by real estate and utilities, while energy fell despite the tailwind from higher oil prices.

Westpac dropped 4.8% to $37.44, the steepest fall among the major banks, though $0.77 of that decline reflects its ex-dividend adjustment (fully franked). Even adjusting for that, the move was disproportionate. NAB shed 2.9%, CBA fell 1.9%, and ANZ lost 1.5%. Wealth platforms were not spared: HUB24 declined 3.1% and Netwealth dropped 2.5%.

Real estate mirrored the damage. Stockland fell 3.2%, GPT lost 3.1%, and Goodman Group slipped 1.9%. In utilities, Origin Energy declined 2.3%, APA Group fell 2.0%, and AGL shed 1.1%.

Health care added a structural concern. CSL fell 1.7% on the day, extending a rolling 12-month decline of more than 50%. Healius dropped 6.6%, now down 57.1% over 12 months.

Energy’s decline was the session’s most counterintuitive result. Woodside and Santos each fell 1.4%, while Whitehaven Coal lost 2.7%, despite Brent crude recovering above US$101. Risk-off equity flows overpowered the commodity tailwind.

The oil price and supply disconnect visible in the 8 May session, where energy stocks fell despite Brent above US$101, has a counterpart in the broader crude market: WTI fell 1.86% on 6 May even as the Strait of Hormuz remained effectively closed, a pattern driven by ceasefire sentiment overriding physical supply data in futures pricing.

| Sector | Index move | Key stocks affected | Primary pressure driver |

|---|---|---|---|

| Financials | -2.25% to 9,514.0 | Westpac -4.8%, NAB -2.9%, CBA -1.9% | Bond proxy yield compression |

| Real Estate | -2.23% to 3,538.9 | Stockland -3.2%, GPT -3.1%, Goodman -1.9% | Bond proxy yield compression |

| Utilities | -2.03% to 10,031.2 | Origin Energy -2.3%, APA Group -2.0% | Bond proxy / rate sensitivity |

| Energy | -1.63% to 10,223.8 | Woodside -1.4%, Santos -1.4%, Whitehaven -2.7% | Risk-off equity flows despite commodity support |

| Health Care | -1.20% to 24,633.0 | CSL -1.7%, Healius -6.6% | Discount rate effect on growth valuations |

Communication Services was the sole sector to finish in positive territory, gaining 0.23% to 1,736.8. The outperformance was anchored by company-specific earnings catalysts rather than macro tailwinds.

Within the broader Materials sector (which fell 1.02% to 24,161.3), critical and strategic minerals names diverged sharply from the index. Iperionx surged 7.2%, Alpha HPA added 4.6%, Metals X gained 3.6%, and Develop Global rose 2.6%, reflecting defence supply chain demand and copper’s strength. COMEX copper climbed 1.7% to US$6.28/lb, its highest since late January.

COMEX gold rose 0.22% to US$4,721.20/oz, yet the ASX 200 Gold Sub-Index still fell 0.5%. The divergence illustrates how risk-off equity selling can override even a supportive commodity price.

Uranium stocks tracked Cameco’s overnight 4% decline on the New York Stock Exchange: Deep Yellow fell 4.7%, Boss Energy dropped 4.1%, Paladin Energy shed 3.5%, and NexGen lost 3.4%.

Company-specific catalysts cut across the broader selloff, producing some of the session’s largest individual moves in both directions.

Tabcorp (TAH) fell 14.2% to $0.755, the session’s sharpest individual decline. AUSTRAC disclosed an investigation into potential money laundering and terrorism financing compliance failures. Jefferies downgraded Tabcorp to Hold, cutting its target to $0.93 from $1.25. JPMorgan downgraded to Underweight with a target of $0.80, down from $0.90.

The Tabcorp result is a reminder that regulatory risk can deliver single-session damage that dwarfs any macro-driven decline.

The ASX 200 closed at 8,697, below its 200-day moving average of 8,803. Reclaiming that level would be the first signal of stabilisation. Three technical levels frame the near-term range:

Two scheduled data releases could move sentiment before Monday’s open:

The Australian dollar traded at $0.7229 against the US dollar, up 0.31%, providing a modest buffer against imported inflation pressures. One analyst maintained a 50% capital allocation stance as of 8 May, reflecting meaningful caution without outright bearishness.

The Strait of Hormuz remains the variable that overrides all others. Further escalation would likely sustain oil above $100 and amplify yield and inflationary pressure on Australian equities.

The 8 May session demonstrated a structural vulnerability in Australian equities: when Middle East tensions flare, the bond yield channel and the oil price channel activate simultaneously, and Australian markets, heavily weighted toward yield-sensitive financials and real estate, absorb disproportionate pressure. Communication Services and critical minerals showed the most resilience because their drivers, corporate earnings and defence supply chain demand, are not negated by rising yields.

Three variables will determine whether this selloff deepens or stabilises: the 8,621 support level, the US Non-Farm Payrolls print, and developments in the Strait of Hormuz. Investors positioned in bond-proxy sectors face the highest near-term concentration risk if any of those three catalysts deteriorate further.

For investors wanting to translate the 8 May sector analysis into concrete portfolio positioning, our comprehensive walkthrough of ASX ETF strategies for Australian inflation covers six funds across fixed income, global equities, and liquid capital reserves, with specific yield data and a three-layer framework designed for the current environment of negative real rates and an elevated RBA cash rate.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and forward-looking statements are subject to market conditions and various risk factors.

—

A bond proxy stock is an income-generating equity, such as a bank, REIT, or utility, whose dividend yield competes directly with government bond yields. When bond yields rise, the spread between the stock's dividend and a risk-free government bond compresses, making the equity less attractive and pushing its price lower.

The ASX 200 dropped 2.04% on 8 May 2026 despite the S&P 500 gaining 1.46% and the Nasdaq rising 2.02% the prior session, because an overnight military exchange in the Strait of Hormuz activated two simultaneous transmission channels: a spike in oil prices reinforcing inflationary pressure, and a 5-10 basis point rise in bond yields that compressed the relative attractiveness of Australia's heavily yield-weighted equity market.

Communication Services was the only sector to finish in positive territory, gaining 0.23%, driven by earnings beats from News Corp, CAR Group, and Life360. Within the Materials sector, critical and strategic minerals stocks such as Iperionx and Alpha HPA also outperformed, supported by defence supply chain demand and rising copper prices.

After closing at 8,697, the ASX 200 sits below its 200-day moving average of 8,803, which is the first level to reclaim for stabilisation. Critical demand support sits at 8,621, and a close below that level would signal a likely return of selling pressure, while overhead supply resistance is at 9,022.

The Strait of Hormuz handles approximately 20% of global oil supply, so disruptions push up oil prices and increase Australian import costs, creating what the RBA has characterised as a clear near-term inflationary impulse with second-round effects on goods and services prices. This makes it harder for the RBA to cut rates and amplifies the yield sensitivity that pressures Australian equities, particularly financials and real estate.