RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

3 hrs ago

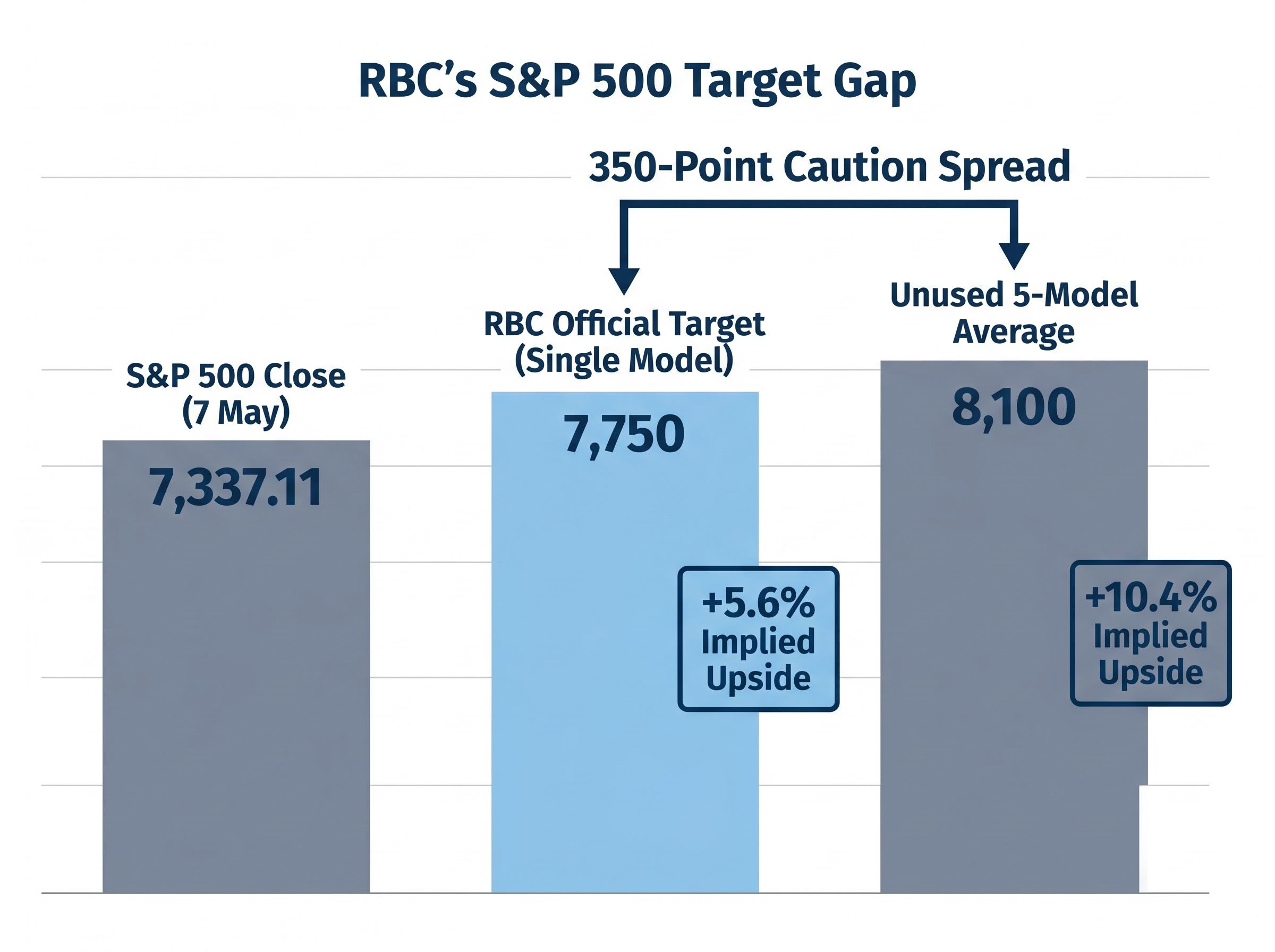

RBC Capital Markets set its S&P 500 price target at 7,750, established in December 2025/January 2026, but the number is less interesting than what the firm did to reach it. Strategist Lori Calvasina and her U.S. equity strategy team set aside four of the five forecasting models they normally average, anchoring the new target on a single valuation and earnings-per-share framework built for a market that is no longer moving as one unit. The full five-model average would have pointed to 8,100. RBC chose not to go there. With the index closing at 7,337.11 on 7 May, the revised target implies roughly 5.6% upside from current levels, arriving after a recovery of more than 16% from the 30 March low and a year-to-date gain of approximately 7.2%. What follows unpacks why one model beat five, what the AI-versus-non-AI earnings split means for the index level, which sectors win and lose under this framework, and which risks could collapse the case before year-end.

The headline is straightforward: 7,750, with implied upside of approximately 5.6% from the 7 May close of 7,337.11. It is among the more bullish year-end targets currently sitting on a major Wall Street desk.

The methodology beneath it is not straightforward at all. RBC’s standard practice runs five separate forecasting models and averages their output. In the current environment, averaging all five would have produced a target of 8,100, roughly 10.4% above the 7 May close.

According to RBC’s modeling, averaging all five of RBC’s models would have pointed to 8,100. The firm chose not to go there.

Calvasina’s team made a deliberate editorial call: the single valuation and EPS model designed to capture a bifurcated earnings environment was the only framework they trusted to reflect what is actually happening in corporate profits. Four models were set aside not because they were broken, but because they were built for a market moving in one direction. This one is not.

The index breadth data from April 2026 reinforces why a blended five-model average was not the right tool: only 23% of S&P 500 constituents outperformed the benchmark in a month that produced a 98th-percentile return, with a 5-percentage-point gap between cap-weighted and equal-weighted index performance confirming that headline gains were being driven by the same narrow AI and semiconductor cohort that sits at the centre of RBC’s single-model framework.

The gap between 7,750 and 8,100 is where the caution lives. It tells investors exactly how much upside RBC sees but is not yet prepared to endorse. That 350-point spread is, in effect, a built-in hedge against a thesis that has not yet been proven durable.

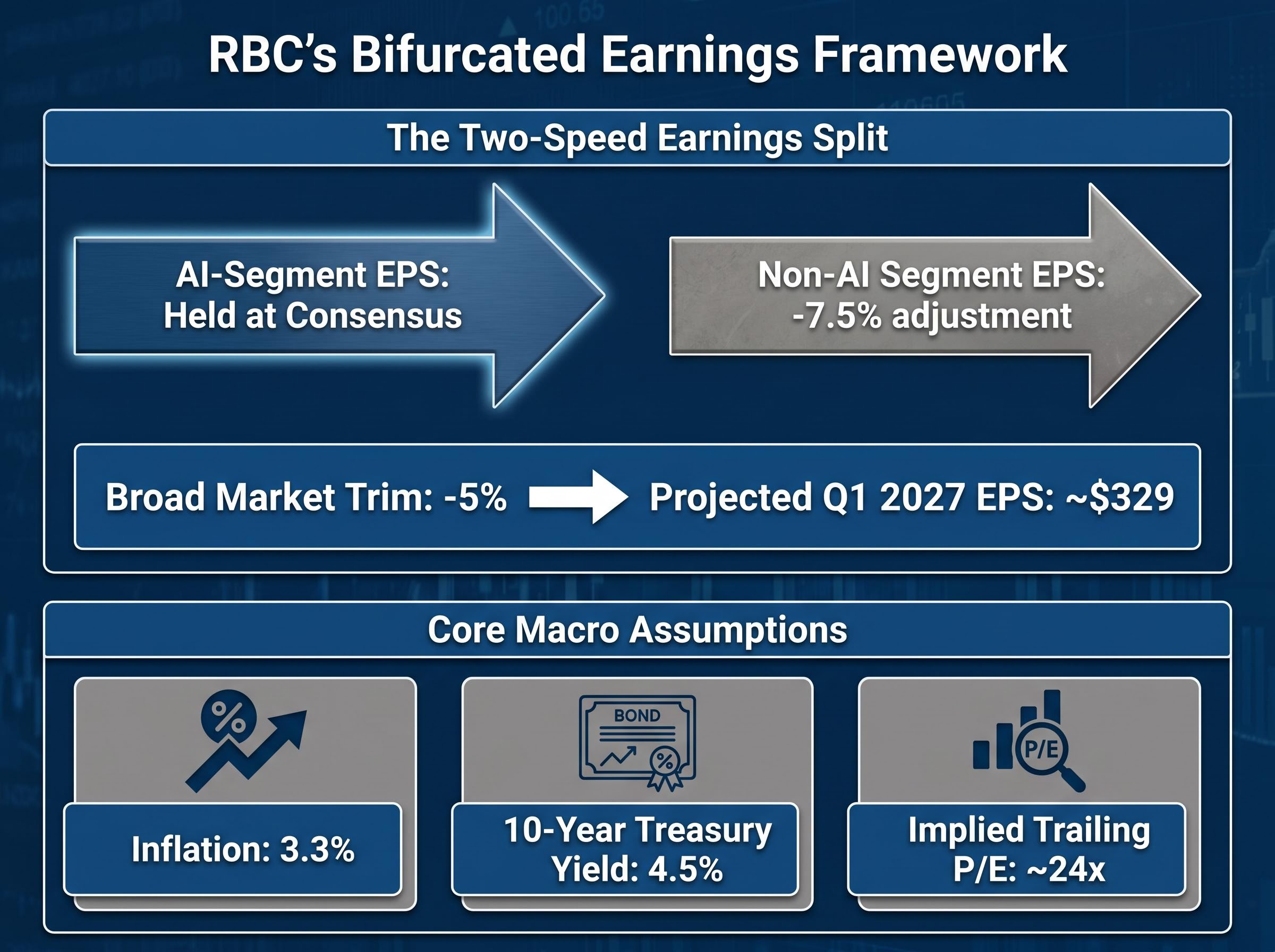

The logic behind the single-model choice comes down to a two-speed earnings environment. AI-linked companies are expected to deliver earnings broadly in line with consensus estimates. Everything else is under pressure.

Markets are now applying a strict AI monetisation evidence filter to hyperscaler results, rewarding Alphabet and Amazon for cloud revenue that demonstrably converted AI capex while punishing Meta nearly 10% for raising full-year spending guidance without a near-term return roadmap, a live-market confirmation that the two-speed earnings environment RBC is modelling is already pricing in at the stock level.

RBC’s framework reflects this directly. The team applied a 7.5% downward adjustment to non-AI earnings while holding AI-segment earnings at consensus levels. The result, after a 5% broad trim to bottom-up consensus, is a projected Q1 2027 EPS of approximately $329 per share.

Three macro assumptions underpin the model:

| Model Input | RBC Single-Model Assumption | Standard Blended Approach |

|---|---|---|

| Non-AI EPS Adjustment | -7.5% from consensus | Uniform trim across all segments |

| AI-Segment EPS | Held at consensus | Blended with broader market |

| Implied Trailing P/E | ~24x | Higher (reflects full five-model average) |

The distinction matters. A blended model treats corporate America as a single earnings stream. RBC’s chosen framework treats it as two streams moving in opposite directions, with Brent crude at approximately $106 per barrel in early May 2026 amplifying the cost pressure on the non-AI side. Readers who understand this bifurcation can interrogate any S&P 500 target they encounter by asking a single question: which side of the split does the model favour?

The two-speed framework produces immediate consequences at the sector level, and the sharpest of them landed on Health Care.

RBC downgraded Health Care from Overweight to Market Weight, citing deteriorating earnings revision trends, notable fund outflows, and weak performance in the firm’s internal analyst survey. For a sector often treated as a defensive anchor, losing its overweight status signals that even traditional safe havens carry revision risk in this environment.

The downgrade is a direct extension of the bifurcation thesis. If non-AI earnings face a 7.5% haircut and AI-linked names hold at consensus, the sectors sitting on the wrong side of that divide are exposed regardless of their historical defensive qualities. Health Care’s revision trajectory placed it firmly on the pressured side.

Beyond Health Care, RBC’s broader positioning remained intact:

For investors building portfolios around the RBC thesis, these calls are where the 7,750 target becomes actionable. The number sets the ceiling; the sector work determines which holdings are positioned to reach it.

RBC’s bullish target carries three explicitly flagged risks, each with a different probability profile and a different mechanism for pulling the number lower.

RBC characterises the prolonged Middle East conflict as the principal tail risk, with the potential to push the U.S. economy into recession if disruptions intensify or persist beyond current expectations.

Of these three, the conflict risk is the least controllable and the most capable of invalidating the thesis entirely. Semiconductor multiples and EPS revisions can adjust gradually. A conflict escalation reprices everything at once.

Readers wanting to model the full downside scenario should explore our full explainer on S&P 500 recession risk, which examines the Goldman Sachs, JPMorgan, and Moody’s recession probability estimates in detail, quantifies the historical average equity drawdown across recessionary periods since 1957 at approximately 32%, and traces the specific transmission mechanism from sustained Brent crude above $100 per barrel through to corporate margin compression and index-level repricing.

RBC’s target of 7,750 sits within the current peer cluster, which is concentrated in the 7,600-7,800 range for year-end 2026.

| Firm | Target | Implied Upside (from 7 May close) | Rationale |

|---|---|---|---|

| Goldman Sachs | ~7,600 (Apr 2026) | ~+3.6% | EPS of ~$309; bullish but measured |

| Morgan Stanley | ~7,800 (Apr 2026) | ~+6.3% | Constructive on earnings growth |

| JPMorgan | ~7,600 (Apr 2026) | ~+3.6% | Broadly aligned with Goldman |

| Barclays | 7,650 (Mar 2026) | ~+4.3% | Industrial super-cycle thesis |

| RBC | 7,750 (May 2026) | ~+5.6% | Single-model; AI/non-AI bifurcation |

The consensus is broadly constructive, with no verified evidence of significant downward revisions from major firms. RBC’s directional call is supported by the wider analytical environment. What separates the 7,750 figure from its peers is not the direction but the methodology: Calvasina’s team is the only major desk anchoring its target on a framework explicitly designed for earnings divergence rather than earnings consensus.

Bank of America’s sentiment indicator for April 2026 implied an approximate 13% S&P 500 return over the next 12 months, sitting just 1.9 percentage points from a historic sell signal while the underlying breadth data told a more cautious story, a tension that mirrors the 350-point gap between RBC’s endorsed target and its own five-model average.

That distinction matters more than the 100-200 points of difference between targets. It signals a view that the market’s internal structure has shifted, and that models built for a unified earnings cycle are no longer fit for purpose.

The most significant element of RBC’s update is not the 7,750 number. It is the firm’s willingness to set aside four of five models, an implicit acknowledgment that standard frameworks struggle to capture a market this structurally divided between AI winners and everything else.

Three variables will determine whether the target holds: the trajectory of semiconductor valuations, the direction of incoming 2027 EPS revision cycles, and the duration of Middle East hostilities. Each is independently capable of pulling the number lower.

The gap between 7,750 and the five-model average of 8,100 is itself the disclaimer. The upside exists in RBC’s own models. The firm is simply not prepared to fully endorse it until the bifurcated earnings story proves durable across at least another quarter of reported results. For now, the caution is the call.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

—

RBC Capital Markets set its S&P 500 price target at 7,750 for year-end 2026, implying approximately 5.6% upside from the 7 May close of 7,337.11.

RBC strategist Lori Calvasina chose a single valuation and EPS model because the standard five-model average, which would have produced a target of 8,100, was built for a market moving in one direction; the current earnings environment is split between AI-linked companies meeting consensus and non-AI companies facing a 7.5% downward adjustment.

RBC projects Q1 2027 EPS of approximately $329 per share, arrived at by holding AI-segment earnings at consensus, applying a 7.5% downward adjustment to non-AI earnings, and then applying a further 5% broad trim to bottom-up consensus estimates.

RBC downgraded Health Care from Overweight to Market Weight, citing deteriorating earnings revision trends, notable fund outflows, and weak performance in its internal analyst survey, placing the sector on the pressured side of the AI versus non-AI earnings divide.

RBC flagged three key risks: compression in stretched semiconductor valuations (with Nvidia near $198 and Broadcom near $412), further downward revisions to 2027 EPS estimates beyond the already-trimmed $329 per share, and a prolonged Middle East conflict escalating into a recession trigger, which RBC characterises as the principal tail risk.