Japan’s Ministry of Finance is estimated to have deployed as much as ¥11 trillion (approximately $72 billion) in yen-buying operations during the Golden Week holiday period in late April and early May 2026, yet the most consequential number for markets may not be the intervention size at all. It may be whether Japan has used two episodes or three.

The distinction matters because of a specific, little-understood constraint embedded in the International Monetary Fund’s exchange rate classification framework. That framework imposes limits on how frequently a free-floating economy like Japan can intervene before its regime designation faces formal scrutiny. Japan’s intervention episode count is now a live question, and the answer connects directly to the Bank of Japan’s room to manoeuvre on monetary policy at its June 2026 meeting.

What follows explains how the IMF’s free-floating framework operates, maps Japan’s current intervention activity against those rules, examines what comparable cases reveal about how the IMF actually enforces the threshold, and shows why the BoJ’s June rate decision is the policy lever that makes the entire system cohere.

Why the IMF cares about how often Japan intervenes

Japan owns the yen. The Ministry of Finance (MoF) controls the intervention apparatus. So why does the IMF get a say?

The answer lies in classification. The IMF assigns every member country an exchange rate regime designation, and “free-floating” sits at the top of the credibility hierarchy. It signals to international creditors, bond investors, and capital markets that the currency’s value is determined by supply and demand, not government targeting. That signal carries a measurable premium in sovereign risk pricing and institutional access.

Free-floating status is not unconditional. The IMF applies a surveillance benchmark that permits a maximum of three intervention episodes, each lasting up to three business days, within any six-month rolling window. Three conditions define compliance:

- Episode count: No more than three distinct intervention episodes within a six-month surveillance period.

- Duration per episode: Each episode may last up to three consecutive business days.

- Declared purpose: Interventions must aim to smooth disorderly market conditions, not steer the exchange rate toward a specific target.

“The IMF’s free-floating benchmark permits a maximum of three intervention episodes, each of up to three business days, within any six-month window.”

This benchmark is not a legally binding hard rule. It functions as a surveillance trigger. Breaching it does not produce automatic penalty, but it opens Japan to Article IV review scrutiny and potential reclassification, outcomes that carry real consequences for borrowing costs and institutional relationships. Japan’s April 2026 Article IV consultation classified the country as free-floating, and no formal IMF censure or warning has been issued regarding the 2026 interventions as of early May 2026.

For investors tracking intervention headlines, the framework transforms each new episode from a price-action event into a counting problem with institutional consequences.

When big ASX news breaks, our subscribers know first

What free-floating actually means, and why it matters to Japan

A free-floating exchange rate regime means the currency’s value is set by market supply and demand. Government intervention is permitted, but only to smooth disorderly conditions, not to push the exchange rate toward a predetermined level. The distinction between smoothing and targeting is where the IMF’s surveillance applies pressure.

Japan currently holds approximately $1.4 trillion in foreign exchange reserves, the second-largest reserve pool in the world. That figure affects the market’s assessment of intervention capacity, but it does not affect classification status. A country with limitless reserves can still lose its free-floating designation if the pattern of intervention crosses from episodic smoothing into sustained management.

Conventional safe haven mechanics break down when a supply shock forces central banks toward tightening rather than easing; the yen’s failure to appreciate during the Hormuz crisis illustrates exactly this dynamic, where energy import dependence turns a traditional safe haven currency into a conduit for pass-through inflation rather than a refuge from it.

The table below illustrates how three adjacent regime classifications differ in practical terms.

| Attribute | Free-Floating | Managed Float | Stabilised Arrangement |

|---|---|---|---|

| IMF definition | Market-determined rate; intervention limited to smoothing | Authorities influence rate without a specific target | Rate maintained within a narrow margin or peg |

| Intervention frequency permitted | Up to 3 episodes per 6-month window | More frequent; no strict episode cap | Continuous or near-continuous |

| Key examples | Japan, US, UK, Australia | India (periodically), Singapore | Switzerland (2011-2015), Denmark |

| Reclassification risk | Low if benchmark respected | Moderate; depends on pattern | Already classified; risk is inability to exit |

The credibility premium that free-floating status confers

Free-floating classification functions as a signal to bond markets and international investors about central bank independence. Countries holding this designation typically benefit from tighter sovereign credit spreads, stronger eligibility for IMF programme support, and a credibility premium that reinforces capital inflows.

Reclassification to a managed float or stabilised arrangement historically widens sovereign spreads and reduces IMF programme flexibility. Switzerland’s experience between 2011 and 2015 provides the cautionary case. The Swiss National Bank’s franc cap policy required approximately CHF 200 billion in sustained interventions before the regime became unsustainable. The IMF issued warnings in its 2014 Article IV consultation, and Switzerland was reclassified to “stabilised” in 2015.

BIS research on intervention and central bank credibility finds that the frequency and pattern of sterilised operations carry measurable consequences for sovereign risk pricing, with markets distinguishing between episodic smoothing and structural rate management even before any formal reclassification occurs.

Japan’s situation differs in structure, but the credibility mechanics are identical. Free-floating status is not a label. It is a credibility asset that affects borrowing costs, institutional relationships, and market confidence in policy independence.

Japan’s episode count in the 2026 intervention window

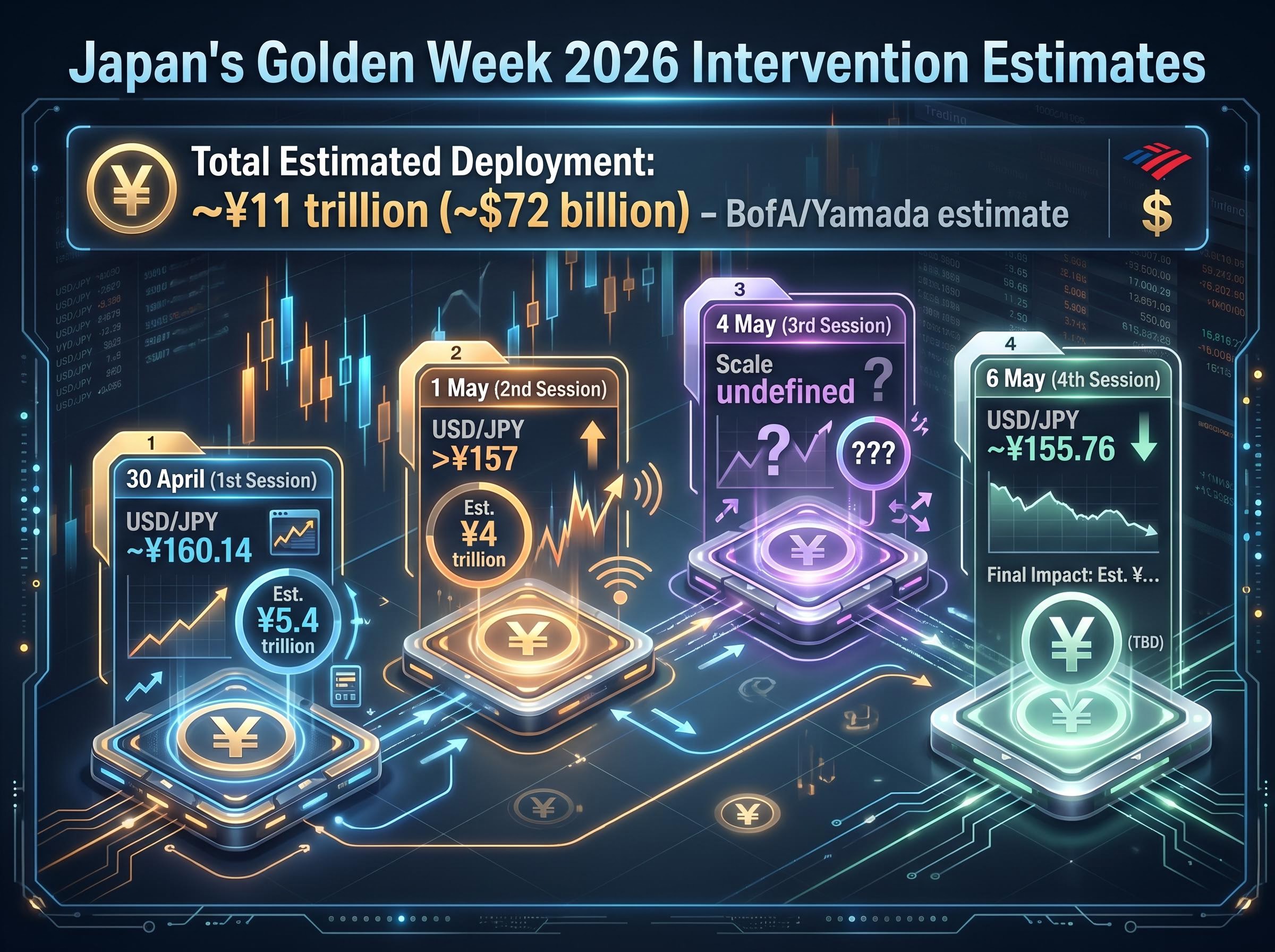

The counting exercise begins on 30 April 2026. USD/JPY reached approximately ¥160.14 that day, a level that has historically functioned as an informal trigger threshold for MoF intervention. What followed was a sequence of operations that stretched across the Golden Week holiday.

- 30 April: The first confirmed operation. Bloomberg estimates based on Bank of Japan current account data place this single session at approximately ¥5.4 trillion, making it one of the largest single-day yen-buying operations on record.

- 1 May: A second session, with order flow analysis suggesting approximately ¥4 trillion deployed. USD/JPY moved lower but remained above ¥157.

- 4 May: A third session during the holiday period, with scale estimates less precisely defined but consistent with continued MoF activity.

- 6 May: A fourth session that pushed USD/JPY to approximately ¥155.76, the low of the intervention window.

“BofA’s Shusuke Yamada estimates the entire Golden Week intervention series could total approximately ¥11 trillion, equivalent to roughly $72 billion.”

Yamada’s estimate uses a historical approximation of roughly ¥1 trillion per 1 yen of USD/JPY movement. The total remains unconfirmed pending official MoF disclosure, which typically arrives with a lag.

The unresolved question as of early May 2026 is how these four sessions translate into episodes under the IMF’s framework. A single continuous multi-day intervention counts as one episode if it runs across consecutive business days up to three. A break in activity followed by renewed intervention may constitute a separate episode.

ING analysts flagged this directly: if Golden Week constituted four or more distinct episodes, Japan would approach or exceed the three-episode benchmark, with any further action in the same surveillance period raising additional IMF scrutiny questions. The episode count is not just a compliance question. It tells investors how many remaining interventions Japan can conduct before the six-month benchmark is formally tested.

How the IMF has handled intervention breaches in comparable cases

Switzerland’s 2015 reclassification looms large in market memory, but it represents the extreme end of IMF enforcement, not the baseline. Four cases illustrate the actual range of institutional responses.

| Country and year | Number of episodes | IMF response | Classification outcome |

|---|---|---|---|

| South Korea 2022 | Multiple episodes | Reviewed in 2023 Article IV; tolerated as response to exceptional disorderly conditions | Free-floating retained |

| India 2018-2019 | Approximately 3 | 2020 Article IV deemed interventions non-disruptive | Free-floating retained |

| Mexico 2020 | 3 episodes | 2021 consultation praised transparency; no adverse findings | Free-floating retained |

| Switzerland 2011-2015 | Sustained (CHF 200bn+) | 2014 Article IV warning issued | Reclassified to stabilised in 2015 |

South Korea’s 2022 experience provides the closest parallel to Japan’s current situation. Korean authorities conducted multiple intervention episodes amid sharp USD/KRW moves driven by speculative flows. The IMF reviewed the activity in its 2023 Article IV consultation and tolerated it as a response to exceptional market conditions. No reclassification followed.

India and Mexico each approached the three-episode threshold without triggering adverse findings, in large part because both countries disclosed their operations transparently and framed them as smoothing measures.

Switzerland’s case was structurally different. The SNB maintained a continuous, target-based intervention regime for nearly four years. The interventions were not episodic responses to disorderly conditions; they were a sustained policy commitment to a specific exchange rate floor. That distinction, between episodic and structural, is what separated Switzerland’s reclassification from the tolerance extended to South Korea, India, and Mexico.

The IMF’s tolerance calculus mirrors the distinction markets themselves apply when processing crisis headlines: episodic versus structural shocks receive categorically different institutional responses, and Japan’s case rests almost entirely on its ability to present the Golden Week operations as the former.

The precedents suggest that the IMF’s three-episode benchmark functions as a threshold for scrutiny, not a tripwire for automatic penalty. The outcome depends on declared purpose, market conditions, transparency of disclosure, and whether the interventions appear structural or episodic.

Why the Bank of Japan’s June rate decision changes the entire equation

The structural tension underlying Japan’s intervention cycle is straightforward: yen weakness is driven by the interest rate differential between US rates and Japan’s policy rate. The BoJ held rates steady at 0.75% at its April 2026 meeting, with split votes among board members pointing toward a potential June move. MoF intervention buys time, but it does not close the gap that drives carry trades.

If the BoJ raises rates in June, it narrows the differential, reduces speculative yen selling pressure, and reduces the MoF’s need for further interventions. That sequence protects Japan’s remaining IMF episode allowance within the current surveillance window. Without a rate move, the differential persists, intervention demand rises, and the episode count risk compounds.

The structural persistence of elevated US yields matters for Japan’s intervention calculus because it means the rate differential driving yen carry trades will not resolve quickly even if geopolitical conditions ease; Wolfe Research attributes only a minority of the 40-basis-point yield surge to the Iran shock, with the remainder reflecting growth repricing that persists regardless of diplomatic outcomes.

Repeated interventions without a corresponding rate move risk signalling a policy lag. Some analysts argue this dynamic increases pressure on the BoJ to act, demonstrating central bank independence rather than reliance on fiscal-side operations. If Japan halted intervention and sustained cash balances through maturing securities, implied US Treasury asset sales would range between approximately $40 billion and $50 billion.

Three scenarios capture the range of outcomes:

- BoJ hikes in June: The differential narrows, carry trade pressure eases, and the MoF’s intervention runway is preserved.

- BoJ holds: The differential persists, intervention demand rises, and Japan’s episode count risk increases within the IMF window.

- BoJ hikes and MoF intervenes simultaneously: Both policy channels reinforce the yen signal, producing the strongest short-term stabilisation effect.

What markets are pricing and why it may be conservative

Market pricing as of early May 2026 assigns approximately 70% probability to a BoJ rate hike at the June meeting. BofA’s Shusuke Yamada has noted that a scenario where large-scale intervention drove June hike probability down to approximately 40% would represent a strategic entry opportunity, not a signal of changed BoJ direction.

The implication is that the base case for a June hike is structurally intact. Factors that could push the probability higher include stronger inflation data, continued wage growth, and further yen weakness. A temporary intervention-driven yen rally could reduce the perceived urgency, but the underlying conditions favouring normalisation remain in place.

The next major ASX story will hit our subscribers first

The institutional logic that connects currency policy and central banking

Three separate institutions govern Japan’s currency and monetary framework, each with a distinct mandate.

The MoF controls intervention operations. The BoJ sets monetary policy. The IMF classifies the regime and conducts surveillance. These actors operate independently, but their decisions interact through a feedback loop that shapes Japan’s policy space.

The BoJ’s primary mandate is price stability and contribution to sound economic development. It does not hold an official mandate encompassing external stability, which means yen stabilisation is an indirect objective achieved through the rate differential, not a direct operational goal.

The feedback loop operates as follows:

“Yen weakness drives imported inflation, inflation strengthens the case for BoJ rate normalisation, normalisation reduces carry trade pressure, and reduced intervention need protects Japan’s free-floating classification.”

Japan’s 2022 intervention cycle deployed approximately ¥9.2 trillion, ultimately followed by policy tightening. Analysts at Goldman Sachs cite this as the structural parallel to 2026, where interventions again precede an anticipated rate move. ING’s analysis reinforces the urgency: if Golden Week constituted four or more distinct episodes, Japan approaches the three-episode benchmark with limited remaining IMF runway in the current six-month window.

For readers encountering future Japan intervention headlines, three questions provide a durable analytical framework:

- Episode count versus IMF benchmark: How many episodes have occurred within the current six-month surveillance window, and how many remain before the three-episode threshold is tested?

- Rate differential size: What is the current gap between US and Japanese policy rates, and is the BoJ signalling movement?

- Surveillance window timing: How many months remain in the current six-month window, and when is the next Article IV consultation scheduled?

Japan’s tightrope walk has an institutional timer, not just a price level

The ¥160 level is the visible trigger. It draws the headlines and prompts the MoF to act. But the less-visible constraint, the IMF’s six-month episode count, is what shapes how long Japan can sustain intervention activity without institutional consequences.

Three interlocking dynamics warrant monitoring. The episode count in the current surveillance window determines Japan’s remaining intervention capacity. The June BoJ rate decision and its differential implications determine whether that capacity needs to be used. Any IMF Article IV commentary that signals shifting tolerance will indicate whether the institutional framework itself is tightening.

If the BoJ raises rates in June and the episode count remains at or below three, Japan exits this cycle with its free-floating classification intact and its credibility benchmark preserved. If neither condition is met, the IMF’s scrutiny window opens.

Readers seeking to track Japan’s intervention activity in real time can monitor daily Bank of Japan current account data releases, which allow analysts to back-calculate intervention volumes on a next-day basis. The IMF’s Article IV consultation for Japan (the April 2026 edition is publicly available) provides the baseline classification and the criteria Japan must satisfy to retain free-floating status.

For readers wanting to understand how the oil shock is reshaping rate expectations across all major central banks simultaneously, our dedicated guide to central bank rate repricing maps the Fed, ECB, and Bank of England policy shifts alongside the BoJ, including Morningstar’s three fixed income scenarios that show why the duration of the Hormuz supply disruption is the single variable determining bond portfolio outcomes in 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding the BoJ’s June rate decision and IMF classification outcomes are subject to change based on evolving market conditions and institutional developments.