Eli Lilly at 40x Earnings: Expensive Stock, Underpenetrated Market

11 mins ago

Markets are pricing in a 45% chance of a rate cut at the June 2026 Federal Open Market Committee (FOMC) meeting, but the more consequential question for investors is not when Kevin Warsh cuts rates. It is what he does to the Federal Reserve’s balance sheet.

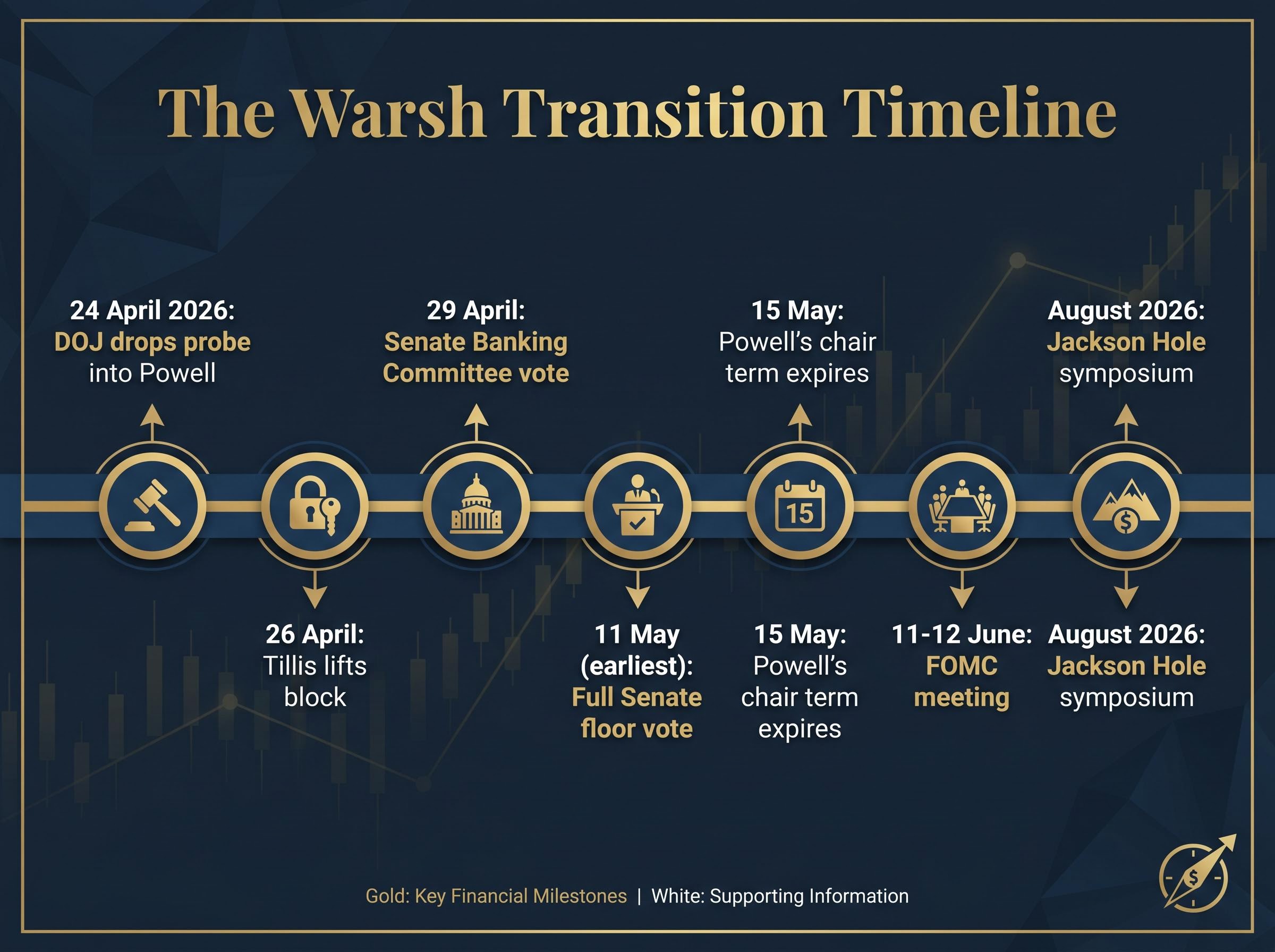

Warsh cleared the Senate Banking Committee on 29 April 2026, with a full Senate floor vote expected no earlier than 11 May. Jerome Powell’s chair term ends 15 May. The transition from confirmation to operational authority is now measured in days, and the policy debates that dominated Warsh’s hearing testimony are about to become decisions with market-moving consequences.

What follows identifies the three policy levers Warsh is most likely to pull as Fed chair, how each one affects different parts of the market, and which carries the greatest risk of surprising investors who remain focused on rate cuts alone.

The nomination nearly stalled before it reached a vote. Republican Senator Thom Tillis blocked the Banking Committee from advancing Warsh’s confirmation, attaching a single condition: the Department of Justice (DOJ) had to drop its investigation into Jerome Powell and the Fed headquarters renovation.

The sequence that followed compressed weeks of political manoeuvring into six days:

That timeline matters for investors. Warsh enters the role having depended on a political intervention (the DOJ decision) to reach a committee vote. His ability to pursue ambitious structural reforms at the Fed will depend partly on maintaining Republican Senate support, a dependency the confirmation fight made visible.

Powell’s governor term extends to 31 January 2028, meaning he could remain on the FOMC as a voting member after vacating the chair. In practice, this represents one vote among 12 on the committee, limiting his individual influence on policy outcomes.

Markets are expected to treat the resolution of Powell’s status as a marginal positive, removing uncertainty rather than creating new risk. The more consequential personnel question lies elsewhere on the committee.

The hearing produced a split verdict, and investors should resist the temptation to resolve it too neatly.

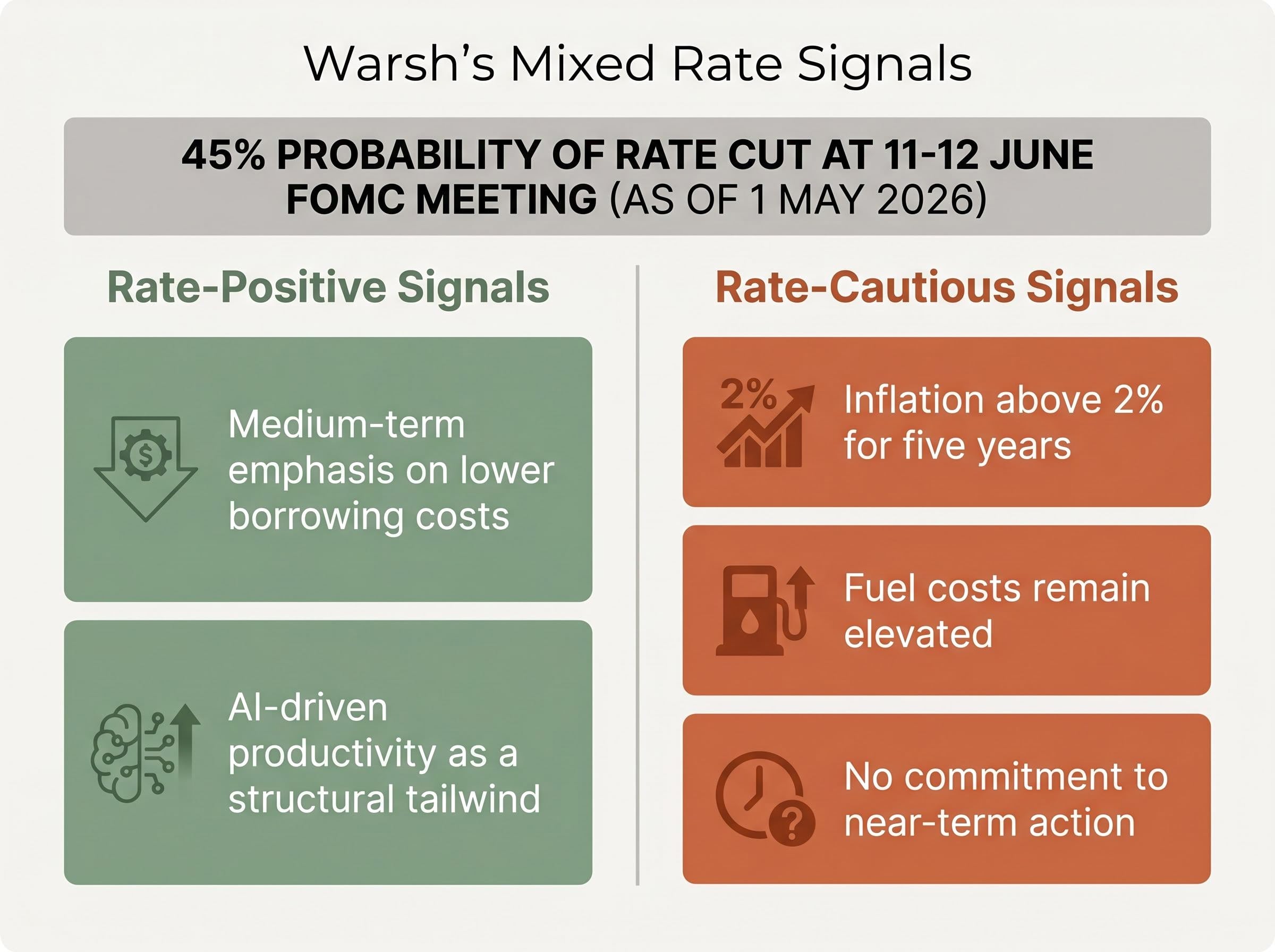

Some analysts characterised Warsh’s testimony as more dovish than his prior Fed tenure, pointing to his emphasis on lower borrowing costs over the medium term and his framing of artificial intelligence-driven productivity as a structural tailwind for the economy. Others read the same hearing as more hawkish than expected, particularly his comments on balance sheet reduction and inflation credibility.

As of 1 May 2026, markets are pricing in a 45% probability of a rate cut at the 11-12 June FOMC meeting. That figure implies near-coin-flip odds, yet much of the commentary treats a cut as a baseline rather than a conditional outcome.

The ambiguity is not accidental. Warsh is navigating a political triangulation between Treasury Secretary Scott Bessent, who has publicly supported delaying cuts, and President Trump, who favours immediate action. Late 2026 remains a plausible window for reductions if fuel prices fall, but the hearing offered conditionality rather than commitment.

The restrictive rate environment Warsh inherits reflects not just committee caution but the direct transmission of energy prices into core inflation, with oil above $100 per barrel creating persistent upward pressure through logistics, retail, and aviation costs that no rate committee can resolve through forward guidance alone.

The rate-relevant signals split cleanly:

Investors pricing in a near-certain June cut may be misreading the signal. The range of plausible outcomes for 2026 rate decisions is wider than current market pricing implies.

Warsh’s deregulatory agenda is directionally clear. The operational path to implementation is not, and that gap explains why bank stocks have not yet fully priced the upside.

On capital requirements, the Fed proposed reducing bank capitalisation thresholds earlier in 2026 to expand lending capacity and pull financing activity back from private credit markets. Agencies finalised changes to community bank leverage ratios on 23 April 2026, consistent with the November 2025 proposal. Additional capital rule modifications for larger banks were proposed in March 2026.

The finalised community bank leverage ratio changes announced on 23 April 2026 lowered the threshold from 9% to 8%, a concrete deregulatory step that illustrates both the direction of Warsh’s capital reform agenda and the incremental pace at which such changes move through interagency coordination.

The activity is real. The friction is also real. Deregulatory initiatives have already encountered delays from internal board divisions, establishing a precedent for resistance even before Warsh takes the chair.

| Reform Area | Current State | Warsh’s Proposed Direction | Likely Market Impact |

|---|---|---|---|

| Community bank capital ratios | Finalised 23 April 2026 | Reduced leverage requirements to support lending | Modestly positive for regional bank equities |

| Large bank capital rules | Proposed March 2026; board divisions unresolved | Further reductions to expand credit availability | Positive for major banks if implemented; timeline uncertain |

| Fed communication framework | Quarterly dot-plot and press conferences in place | Eliminate dot-plot; reduce press conference frequency | Increased short-term volatility around FOMC dates |

Warsh has characterised the dot-plot forward guidance mechanism as having limited utility for policy signalling and has indicated interest in reducing the frequency of press conferences. The August 2026 Jackson Hole symposium represents an early public platform for Warsh to define his communication philosophy.

Eliminating forward guidance tools removes a source of market anchoring that investors have relied on for over a decade. Reduced predictability in Fed communication has historically increased short-term volatility around FOMC meeting dates, a dynamic that options-market participants and fixed-income traders would need to price.

Rate cuts attract the headlines. The balance sheet carries the larger market risk, and it affects more asset classes simultaneously.

Warsh stated at his confirmation hearing that the Fed’s ownership of US Treasuries blurs the line between fiscal and monetary policy. His position: a smaller balance sheet creates room for rate reductions without stimulative overhang, effectively separating the two policy tools that have become entangled since 2008.

The mechanics of the risk are straightforward. If the Fed accelerates the pace at which it allows Treasury holdings to mature without reinvestment, long-term bond supply increases. That supply pressure could steepen the yield curve rapidly, raising long-term borrowing costs even as the Fed cuts short-term rates.

Warsh explicitly acknowledged at his hearing that balance sheet reduction “cannot happen quickly,” requiring time, patience, and care given decades of buildup.

As of 24 April 2026, the 10-year Treasury yield stood at approximately 4.306% and the 2-year yield at approximately 3.793%. A steepening move from current levels would pressure multiple asset classes:

The Federal Reserve H.4.1 balance sheet data released on 23 April 2026 shows the current composition of securities holdings and reserve balances, providing the baseline against which any acceleration in quantitative tightening would be measured.

The Fed’s ability to transmit rate decisions into actual lending conditions depends on maintaining sufficient reserve levels in the banking system. Reserve levels refer to the cash that commercial banks hold at the Fed; when these drop too low, the connection between the Fed’s rate target and real-world borrowing conditions weakens.

Shrinking the balance sheet too aggressively risks impairing that transmission mechanism. The Fed’s internal consensus-building processes, including working groups and formal studies on reserve adequacy, would likely act as a structural brake on rapid changes, regardless of the chair’s stated preferences.

For investors wanting to understand the specific market mechanics around what a breach of the long-end yield threshold at 5% would trigger, our full explainer on the 30-year Treasury yield as a market tripwire covers the mortgage rate, corporate borrowing, and federal debt service implications, alongside Bank of America’s historical precedents from Japan 1989, the United States 1999, and China 2007.

The counter-intuitive finding is that Warsh’s arrival does not shift the FOMC’s ideological balance as much as the confirmation narrative suggests. Stephen Miran’s departure in May 2026 removes a Trump-appointed official who supported rate cuts. Warsh, also a Trump appointee, is expected to vote similarly on rates. This is effectively a Trump-for-Trump swap.

The more consequential shift has already happened elsewhere on the committee. Christopher Waller, who previously supported rate cuts and pursued the chair nomination himself, has moved to a more cautious stance. That repositioning reduces the effective dovish bloc on the FOMC independently of who holds the chair.

The divided FOMC dynamics heading into the Warsh era are more fractured than the headline rate probability implies: four members dissented at the April 2026 meeting, the highest count since 1992, with dissents pulling in opposite directions and signalling a committee without a coherent policy centre rather than a bloc moving toward cuts.

The current committee dynamic breaks down as follows:

All FOMC decisions remain data-dependent. White House officials who previously called for cuts have adopted a similar wait-and-see framing. The mid-June economic data picture, which will shape the first FOMC meeting under Warsh’s leadership, is not yet visible.

Three risks deserve more attention than current positioning suggests. Ranked from most to least acute:

The distinction matters. The first two risks carry event-driven triggers (the mid-June FOMC meeting, Jackson Hole in August). The third is structural and slow-moving, likely to disappoint on timeline rather than direction.

Warsh’s rate intentions are the most visible variable in the transition. His balance sheet philosophy is the most consequential one.

Inflation has remained above 2% for five years, with fuel costs as an active variable. Long-term inflation expectations remain contained, and markets are not currently pricing significant concerns about Fed independence. That base-case assumption is worth monitoring rather than assuming.

Rate cut timing is the most discussed variable in the transition, but the balance sheet question carries the largest potential market impact across multiple asset classes simultaneously. Investors positioned for a clean dovish pivot face a policy environment that is likely to be more conditional, more gradual, and more structurally uncertain than a simple rate-cut narrative implies.

The regulatory reform outlook is directionally positive for bank equities but operationally slow. Jackson Hole in August 2026 represents the next meaningful signalling event for Warsh’s communication and deregulatory agenda.

For investors wanting to stress-test the rate cut timeline against the geopolitical variables that could extend higher-for-longer conditions beyond the 2026 window Warsh has left open, our dedicated guide to geopolitics and Fed interest rates through 2027 maps the specific transmission channels from Middle East conflict through oil prices and core inflation to the projected easing horizon, including sector-level impacts on aviation, consumer spending, and corporate credit.

The first 90 days of Warsh’s tenure, from confirmation through the August symposium, will define how much of his structural agenda represents real policy intent versus confirmation positioning. Three developments warrant close monitoring: the Senate floor vote outcome and timing, Warsh’s first post-chair public communication (or its notable absence), and the July inflation and employment prints that will frame the data picture for subsequent FOMC decisions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding Federal Reserve policy, rate decisions, and balance sheet actions are speculative and subject to change based on economic conditions and committee deliberations.

Kevin Warsh is a former Federal Reserve governor nominated by President Trump to replace Jerome Powell, whose chair term expires on 15 May 2026. Warsh cleared the Senate Banking Committee on 29 April 2026 after a politically complicated confirmation process that included a DOJ investigation into Powell being dropped as a condition of advancing the nomination.

The Federal Reserve balance sheet refers to the trillions of dollars in US Treasuries and other securities the Fed has accumulated since 2008; reducing it increases the supply of bonds in the market, which can push long-term yields higher and simultaneously pressure fixed income, equities, and real estate. Warsh has signalled a smaller balance sheet is a priority, making this the highest-impact policy lever investors should monitor beyond rate cut timing.

As of 1 May 2026, markets were pricing in approximately a 45% probability of a rate cut at the 11-12 June FOMC meeting, reflecting near-coin-flip odds rather than a near-certain outcome. Warsh's hearing testimony was conditional on inflation and fuel price trends rather than a commitment to near-term action.

The dot-plot is a chart published quarterly showing where each FOMC member expects interest rates to be in future years, and it has served as a key market-anchoring tool for over a decade. If Warsh eliminates it alongside reducing press conference frequency, investors would face greater uncertainty around FOMC meeting dates, historically increasing short-term volatility in fixed income and equities.

Warsh's deregulatory agenda is directionally positive for bank equities, with community bank leverage ratio thresholds already lowered from 9% to 8% on 23 April 2026 and larger bank capital rule changes proposed in March 2026. However, internal Federal Reserve board divisions have already produced delays, meaning investors pricing in rapid implementation may face a longer timeline than headline announcements suggest.