The S&P 500 closed at an all-time high of 7,205.33 while oil trades at $99.89 a barrel, US consumer sentiment has collapsed to its lowest recorded level, and a shooting war between the United States and Iran has disrupted the Strait of Hormuz for more than eight weeks. That combination should unsettle equity investors. For the most part, it has not. VanEck’s Q2 2026 Investment Outlook, published 13 April 2026, argues this calm is not confidence but complacency: markets appear to be pricing in a swift resolution and a soft landing for growth, while macroeconomic data tells a more complicated story. For Australian investors, whose own consumer confidence has slipped to multi-year lows, the gap between equity valuations and economic reality deserves scrutiny. What follows is an examination of the specific signals that suggest risk is being underpriced, an explanation of how quality investing works as a defensive lens in this environment, and an outline of the ASX-listed options available to act on that analysis.

What the numbers reveal about today’s market disconnect

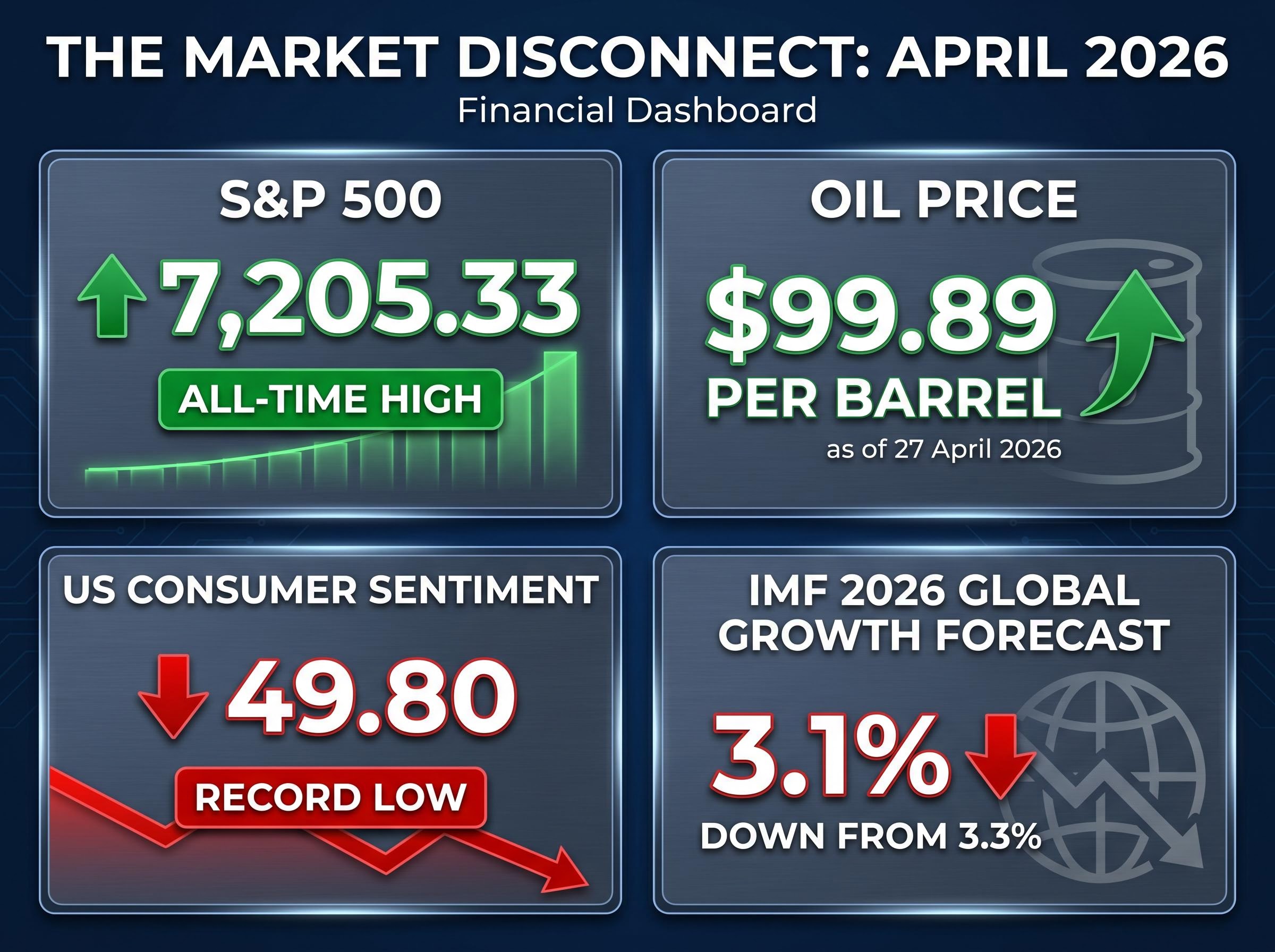

Place four data points side by side and the picture becomes difficult to reconcile.

The S&P 500 sits at a record 7,205.33. Oil is at $99.89 per barrel as of 27 April 2026. US consumer sentiment fell to 49.80 in April, a record low. The International Monetary Fund (IMF) downgraded its 2026 global growth forecast to 3.1% from 3.3% in January, with an adverse scenario of just 2.5%. Equity markets have largely ignored that revision.

Gasoline at $4.25 per gallon carries weight as a stock market warning signal: in the six months following every prior breach of $4.00 since 1993, the S&P 500 has declined by an average of 11%, a pattern that adds a specific historical dimension to what current sentiment and growth data are already suggesting.

| Indicator | Current Reading | What It Signals |

|---|---|---|

| S&P 500 | 7,205.33 (all-time high) | Markets pricing in growth and resolution |

| Oil price | $99.89/barrel | Sustained energy supply disruption |

| US consumer sentiment | 49.80 (record low) | Consumer spending under pressure |

| IMF 2026 global growth forecast | 3.1% (down from 3.3%) | Growth expectations deteriorating |

VanEck’s Q2 2026 Investment Outlook describes the gap between record equity highs and deteriorating macroeconomic signals as a “dangerous disconnect,” warning that markets may be underpricing slowdown risks and underestimating lower growth potential.

None of this guarantees an imminent correction. But the configuration is unusual, and historically, configurations like it have rewarded investor attention more than investor indifference.

When big ASX news breaks, our subscribers know first

The geopolitical engine driving the risk: US-Iran and the Strait of Hormuz

The US-Iran conflict began with strikes on 28 February 2026. As of late April, the war is now past its eighth week. A US naval blockade on Iranian ports remains in effect. The Strait of Hormuz remains disrupted. Multiple rounds of peace negotiations have occurred without producing a breakthrough, and the United Nations has called for the strait to reopen.

Eight weeks is a long time for a conflict that many initial market assumptions may have treated as a short-duration event. Iran has described its situation as a “war situation.” The US is still examining Iran’s latest proposals. There is no ceasefire.

Oil rose to $99.89 per barrel within this disruption, well above pre-conflict levels, and the supply pressure has not eased.

Why the Strait of Hormuz matters to your portfolio

Approximately 20% of global oil supply transits through the Strait of Hormuz. Sustained disruption at that scale feeds directly into three pressure points:

- Energy costs: Higher crude prices raise input costs across the economy, compressing corporate margins

- Shipping rates: Rerouting around the strait increases freight costs, which pass through to consumer prices

- Inflation transmission: Energy-driven inflation erodes consumer spending power, which feeds into earnings pressure for equities globally

Australian consumers are not insulated. Global energy prices transmit into domestic fuel and electricity costs, and the local confidence data already reflects deterioration: the Westpac-Melbourne Institute consumer confidence index fell to 80.1 in April, while the ANZ-Roy Morgan measure dropped to 67.8.

Energy-driven inflation operating through a supply-side shock creates a specific policy trap: the Federal Reserve cannot cut rates to stimulate a slowing economy without risking a further acceleration in prices, a constraint that was absent in demand-driven inflation cycles and that materially changes the toolkit available to policymakers.

Identifying quality ETFs for Australian portfolios

Three ASX-listed ETFs offer distinct pathways into the quality factor, each with different construction methodologies and risk exposures.

The shift away from Australian home bias has accelerated structurally: international ETFs overtook domestic ETFs as the most purchased category on Selfwealth by Syfe in Q1 2026, with approximately 80% of Australian ETF investors planning to increase international holdings through the year, a trend that places products like QUAL and QHAL at the centre of a broader portfolio reorientation.

| ASX Code | Underlying Index | Portfolio Size | Currency Treatment | Key Distinguishing Feature |

|---|---|---|---|---|

| QUAL | MSCI World ex Australia Quality Index | 300 companies | Unhedged | Largest quality ETF on ASX; $7.75 billion net assets; 2.13% distribution yield |

| QHAL | MSCI World ex Australia Quality Index | 300 companies | AUD hedged | Identical factor exposure to QUAL with AUD currency hedging |

| QLTY | MSCI World ESG Leaders Quality Index | 150 companies | Unhedged | ESG screening overlay; emphasis on superior free cash flow metrics |

QUAL posted a year-to-date daily total return of -3.05% as of 31 March 2026, reflecting the broader market turbulence. QHAL provides the same quality factor exposure but removes foreign exchange variability. QLTY screens for quality through a narrower, ESG-filtered lens, holding 150 of the highest-ranked companies with a focus on free cash flow generation.

These are not interchangeable products. The portfolio size, screening methodology, and currency treatment create meaningfully different risk profiles.

Hedged vs unhedged: the currency question for Australian investors

With QUAL, AUD/USD movements directly affect returns. A falling Australian dollar boosts the value of unhedged international holdings; a rising Australian dollar reduces it. QHAL strips out that variable entirely, delivering pure quality factor exposure without a currency overlay.

In calmer periods, the hedging decision is often secondary. In the current environment, with US-Iran uncertainty affecting USD safe-haven dynamics and the Australian dollar responding to shifting commodity and risk sentiment, the choice carries more weight. Investors who want to isolate the quality factor from currency noise may find the hedged option more appropriate. Those with a view on AUD weakness may prefer the unhedged exposure.

The enduring principles of quality investing

Quality investing targets companies that share a specific set of measurable financial characteristics. These are not abstract labels. They are balance sheet and income statement features that can be screened for:

- High return on equity (ROE)

- Low financial leverage

- Stable and consistent earnings growth

- High profit margins

- Low earnings variability

- Strong balance sheets

Companies that score highly on these metrics tend to sustain profitability through economic cycles. When growth slows, input costs rise, and uncertainty elevates, quality companies face less margin compression, carry less refinancing risk, and generate more predictable cash flows. The current macro backdrop, with slowing global growth, record-low consumer sentiment, energy-driven inflation, and unresolved geopolitical disruption, is precisely the type of environment the quality factor was designed for.

Russell Investments factor research on quality metrics across US recession cycles shows that companies with robust profitability and low leverage characteristics have historically delivered meaningful outperformance relative to the broader market during periods of economic contraction, providing empirical grounding for the defensive positioning case VanEck advances in its Q2 2026 outlook.

VanEck’s Q2 2026 outlook adds a valuation dimension to the case. According to VanEck, quality has delivered superior performance during economic contractions and over long horizons, and the factor’s valuations relative to the broader market have recently narrowed toward their 10-year average.

Quality stock valuations have narrowed toward their 10-year average relative to the broader market, according to VanEck, suggesting a more attractive entry point for investors considering defensive positioning.

Where quality investing has limits

Quality stocks frequently trade at valuation premiums. In broad market rallies, particularly low-rate environments that favour speculative assets, those premiums become a drag. Quality strategies can lag significantly when risk appetite is high and capital flows into higher-beta names.

Sector concentration is another consideration. Quality screens tend to overweight healthcare, consumer staples, and technology, which introduces its own risk profile. And quality positioning reduces drawdown exposure in severe dislocations; it does not eliminate it. Investors should treat the quality factor as a risk-management lens, not as full downside protection.

The signals worth watching before risk gets repriced

Identifying a potential mispricing is only useful if investors know what would confirm or contradict the thesis over coming weeks and months. Five specific signals deserve monitoring, ordered by proximity to the core risk:

- Strait of Hormuz status: Any confirmed reopening, partial or full, would materially reduce the energy supply premium and alter the risk calculus. Continued disruption reinforces the mispricing thesis.

- US-Iran negotiation progress: A ceasefire or framework agreement would be the single largest repricing catalyst. Continued stalemate extends the current uncertainty regime.

- Oil price trajectory relative to $100 per barrel: A sustained move above $100 would intensify inflation pressures globally. A decline below $90 would signal easing supply concerns.

- IMF adverse scenario tracking: The IMF’s 2.5% global growth adverse scenario serves as the downside benchmark. Actual economic data that trends toward that figure, rather than the baseline 3.1%, would validate the mispricing argument.

- Australian consumer confidence readings: The Westpac-Melbourne Institute (currently 80.1) and ANZ-Roy Morgan (currently 67.8) indices provide the most direct measure of domestic spillover. Further deterioration would strengthen the case for defensive positioning.

Brent crude sitting within $1.50 of Goldman’s sell-off trigger at approximately $108.50 per barrel adds a specific technical threshold to the monitoring framework; Goldman Sachs models a 5-10% S&P 500 decline if crude crosses that level on a sustained basis, a scenario that forward earnings estimates have not yet priced in.

The IMF’s adverse scenario projects global growth of just 2.5% in 2026. That figure serves as the benchmark against which incoming economic data should be measured for signs that the downside case is materialising.

VanEck has also flagged fiscal risk and rate pressure as secondary signals worth tracking, alongside gold as a portfolio hedge in the current environment.

Risk awareness is not pessimism. It is portfolio discipline.

The core tension is straightforward: equity markets are at record highs while consumer sentiment is at record lows, oil is approaching $100 a barrel, and an unresolved Middle East conflict has disrupted one of the world’s most important shipping lanes for more than eight weeks. Markets may be right that this resolves quickly. They may not be.

Quality investing offers a way to remain invested without absorbing the full downside of that potential mispricing. Companies with high returns on equity, low leverage, and stable earnings are better positioned to weather slowing growth and rising costs. Three distinct ASX-listed vehicles, QUAL, QHAL, and QLTY, now make that factor accessible to Australian investors with different currency and ESG preferences.

VanEck’s thesis could prove wrong. Markets can stay ahead of fundamentals for longer than most expect. The quality framework is not a market-timing call. It is a positioning tool for an environment where the conditions that make it relevant, slowing growth, elevated inflation, and geopolitical uncertainty, are unlikely to resolve quickly.

The goal is not to predict when repricing happens. It is to ensure the portfolio can withstand it if it does.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—