How the RBA’s Hawkish Pause Reshapes Australian Bank Shares

1 hr ago

Six stocks swung between 8% and 15% on 29 April 2026, in opposite directions, yet three of them actually beat their earnings estimates. The session unfolded against a cautious macro backdrop: the Federal Reserve’s rate decision loomed, the 10-year Treasury yield sat anchored near 4.35%, and traders showed little appetite for broad index bets. The S&P 500, Dow, and Nasdaq all finished in negative territory, but that restraint at the index level did nothing to dampen the violence of individual stock moves. The defining story was not what companies earned but what they told investors about what comes next. What follows identifies the six biggest stock market movers of the session, explains the specific trigger behind each swing, and draws out the single most important lesson for investors tracking earnings season.

Pre-FOMC positioning set the tone. With the Fed’s rate decision imminent, traders kept directional index bets small, and that restraint acted as a ceiling on optimism rather than a floor against losses. The result: a narrow, mildly negative day for broad benchmarks that left individual earnings catalysts as the only game worth playing.

The pre-FOMC positioning that suppressed index moves on 29 April sits within a broader rate environment shaped by macro headwinds from elevated oil prices, where Brent crude above $112 per barrel has complicated the Fed’s path toward easing and pushed derivative markets to price the next cut as late as 2027.

The three major indices closed lower:

Beyond rate expectations, two macro data points drew attention. Domestic oil inventories fell by approximately 1.8 million barrels, and the 10-year Treasury yield held steady.

The 10-year Treasury yield at 4.35% served as the session’s macro anchor, reinforcing that borrowing costs remain elevated and that the Fed is in no hurry to cut.

The FOMC rate decision statement confirmed the federal funds rate target range was held at 3-1/2 to 3-3/4 percent, reinforcing the elevated borrowing cost environment that made forward guidance the single most consequential variable for equity valuations across the session.

With macro risk priced but not resolved, every company-specific catalyst carried outsized weight. Stocks that delivered good news surged; those that disappointed were punished without a safety net of broader market momentum.

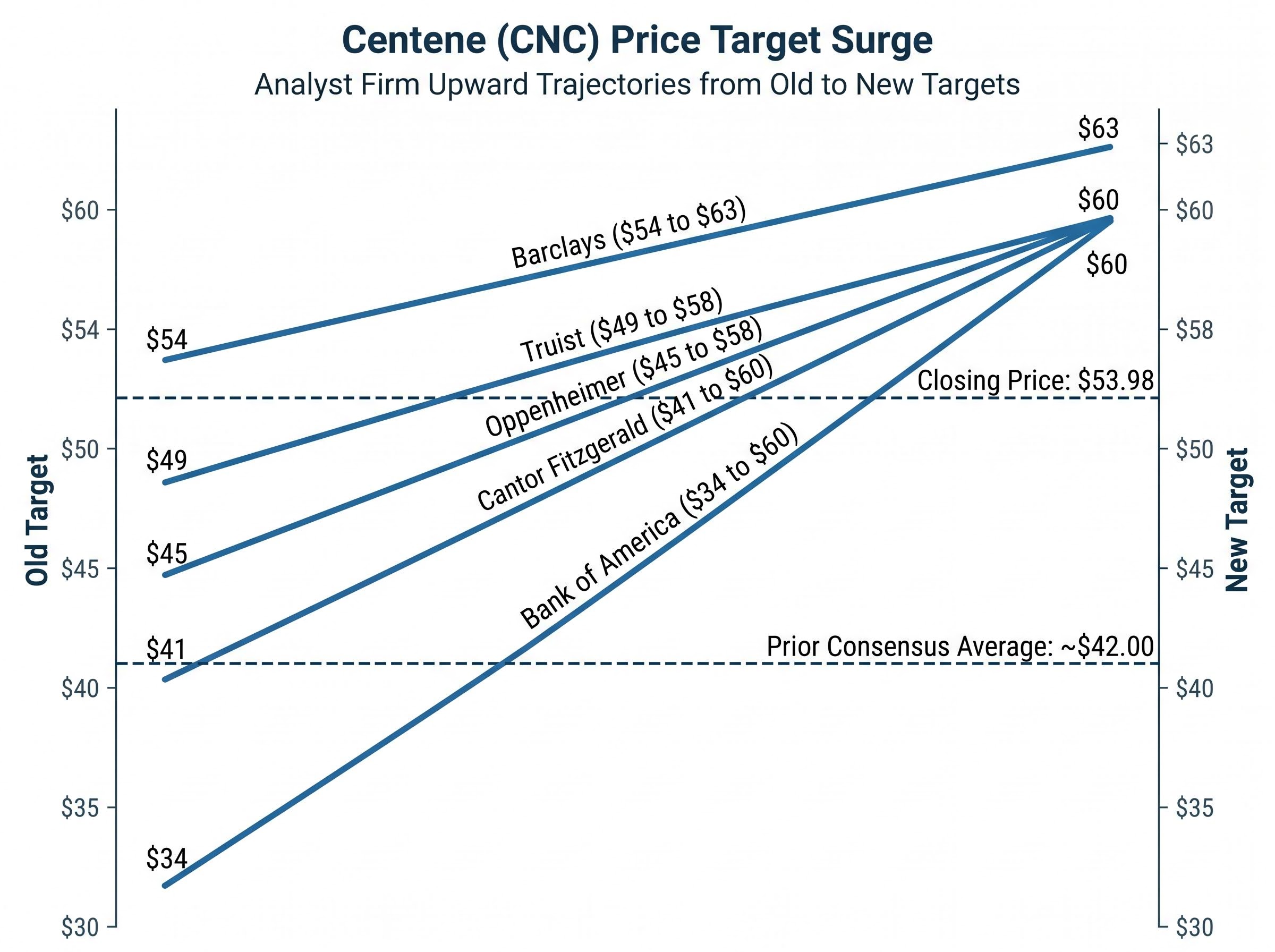

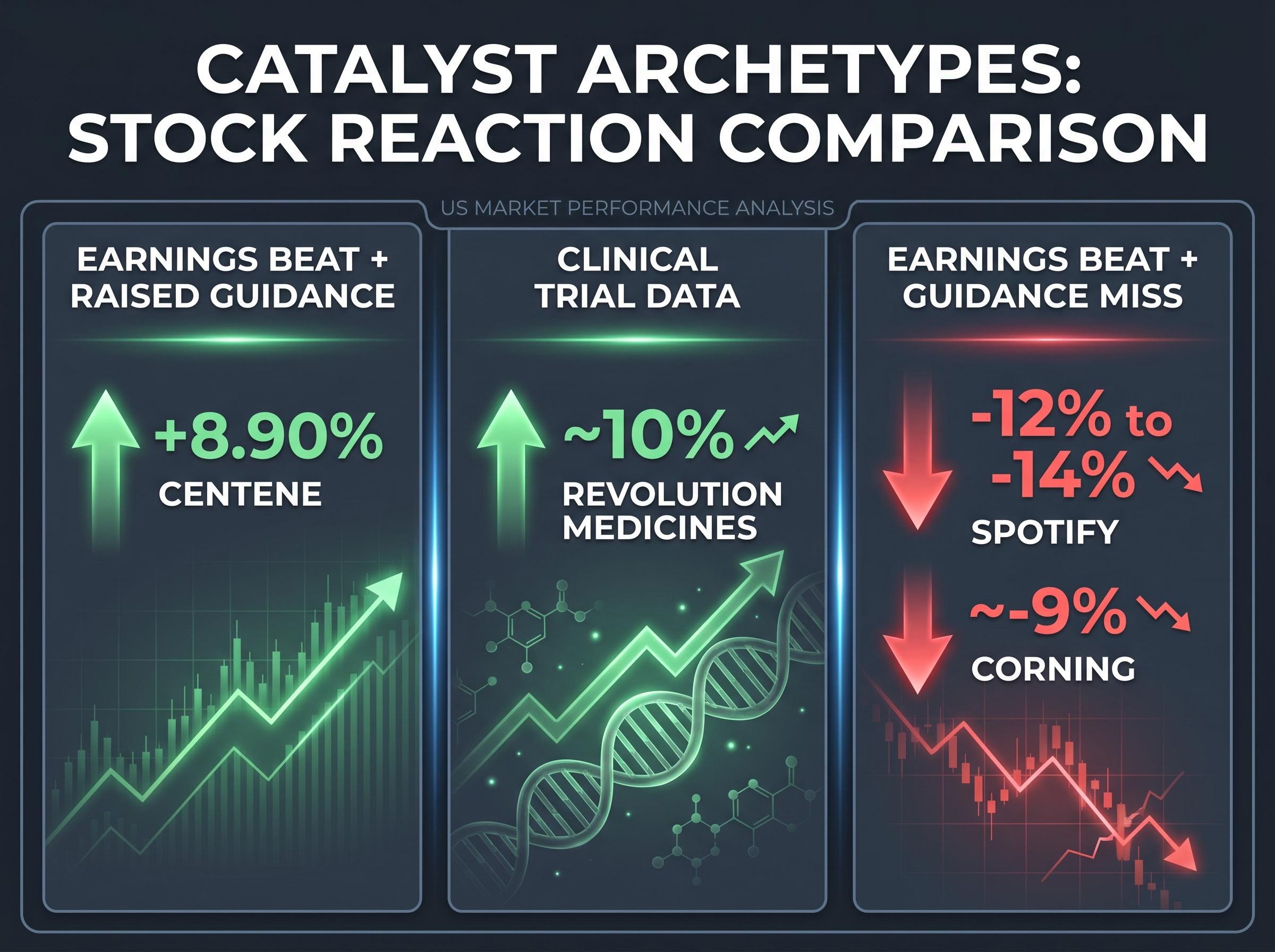

For quarters, elevated medical costs had been the persistent worry hanging over Centene Corporation (CNC) and the managed care sector broadly. On 29 April, that worry began to lift. The company’s Q1 2026 adjusted earnings per share of $3.37 beat expectations, but the catalyst that sent the stock up 8.90% to close at $53.98 was the guidance raise: full-year adjusted EPS was lifted to above $3.40, a signal that cost controls across Medicaid and managed care segments were producing tangible results.

The post-earnings close of $53.98 exceeded the prior consensus average price target of approximately $42.00, meaning Centene had, in a single session, repriced past the average level at which Wall Street had collectively valued it.

The guidance raise triggered a wave of price target revisions from at least five named firms. Two, Cantor Fitzgerald and Bank of America, upgraded their ratings to Buy-equivalent stances.

| Analyst Firm | Action | New PT | Old PT | Rating |

|---|---|---|---|---|

| Barclays | Raised PT | $63 | $54 | Overweight |

| Cantor Fitzgerald | Upgraded + Raised PT | $60 | $41 | Overweight (from Neutral) |

| Oppenheimer | Raised PT | $58 | $45 | Outperform |

| Truist | Raised PT | $58 | $49 | Buy |

| Bank of America | Upgraded | $60 | $34 | Buy |

The stock’s close above the prior consensus average of $42.00 signals a broad repricing event, not merely a single-firm revision. When five analysts raise targets simultaneously, the resulting buying pressure and media attention compound the initial move.

Positive clinical trial data from Revolution Medicines’ (RVMD) oncology pipeline drove the stock up approximately 10% on 29 April, opening the session at $144.83. In biotech, efficacy signals from a lead drug programme function as an earnings event, and this session illustrated that dynamic clearly.

Bank of America raised its price target on RVMD to $170 from $115, a $55 increase that reflected heightened conviction in the company’s drug development trajectory.

The revised target of $170 sits well above the analyst average of $136.84, though the high-end target among covering analysts reaches as high as $263. Three data points frame the opportunity:

For investors tracking biotech movers, the lesson is straightforward: trial readout calendars deserve the same attention as earnings calendars. Pre-revenue companies can re-rate sharply when efficacy data exceeds expectations, independent of revenue or profit metrics.

Implied volatility signals in the options market had already priced in substantial post-earnings movement for Revolution Medicines before the clinical data landed, with derivatives premiums reflecting the binary nature of trial readouts for pre-revenue biotechs in a way that pure price-target models do not capture.

Spotify (SPOT) reported Q1 2026 earnings per share of $3.45, a beat. Corning (GLW) reported adjusted EPS of $0.70, also a beat. Both stocks fell sharply anyway.

The market was not scoring the past quarter. It was pricing the next one.

Spotify guided for approximately 17 million net subscriber additions, a figure that fell short of market expectations. The shortfall prompted Barclays to cut its price target to $500 from $600, and the stock dropped 12-14% in a single session. Corning guided Q2 revenue at $4.6 billion against a consensus estimate of $4.67 billion; the $70 million gap was enough to trigger an approximately 9% decline.

| Company | Earnings vs Estimate | Guidance vs Consensus | Daily Change |

|---|---|---|---|

| Spotify (SPOT) | $3.45 EPS (beat) | ~17M subscribers (miss) | -12% to -14% |

| Corning (GLW) | $0.70 adj. EPS (beat) | $4.6B revenue vs $4.67B (miss) | ~-9% |

Both stocks illustrate the same pattern: a past-quarter beat paired with a forward-quarter miss produced a sharp negative reaction. Stock prices represent a discounted sum of future cash flows, not a scorecard of historical performance. When guidance disappoints, the market reprices accordingly, regardless of what the last quarter delivered.

The six moves from 29 April fit neatly into three catalyst archetypes, each mapping to a predictable market response. Understanding these patterns converts a single session’s events into a repeatable analytical framework.

Analyst price target revisions serve as signal amplifiers. A single upgrade may move a stock modestly; five simultaneous target raises, as seen with Centene, create both institutional buying pressure and media coverage that compounds the initial catalyst.

Beat-and-raise earnings dynamics played out in parallel on 29 April across multiple sectors: Starbucks reported a 6.2% comparable sales increase and a 16.3% EPS beat, prompting Evercore and Wolfe Research to revise multi-year profit models upward through fiscal 2028 in a pattern that mirrors the simultaneous target revisions seen with Centene.

When a stock moves sharply after reporting, three questions cut through the noise. Did the company raise or lower forward guidance? Did multiple analysts revise price targets in the same direction? Is the move driven by a company-specific catalyst or broader macro sentiment? Answering these in sequence separates signal from noise and helps investors avoid reacting to a headline before understanding its context.

AvalonBay Communities (AVB) gained 5.29% after reporting Q1 2026 results that beat estimates across the board. Revenue came in at $770.28 million, funds from operations (FFO, a measure of cash generated by real estate operations) exceeded expectations on lower expenses and development net operating income, and full-year Core FFO guidance was reaffirmed.

Capital return figures underscored the result:

In a rate-sensitive sector like REITs, where elevated borrowing costs weigh on valuations, capital return programmes and cost discipline can offset the macro headwind. AvalonBay’s combination of an earnings beat and aggressive buyback activity delivered exactly that message.

Credo Technology (CRDO) moved in the opposite direction, declining approximately 15% following a mixed quarterly report. Key data points on Credo:

The selloff contributed to broader weakness in AI-adjacent semiconductor names. The AI trade, once forgiving of aggressive valuations, is increasingly holding companies to the same guidance standard applied to the rest of the market.

Guidance quality separated winners from losers on 29 April. Companies that beat current-quarter estimates and raised forward outlooks were rewarded; those that beat but guided below expectations were punished. The magnitude of moves in both directions was amplified by pre-FOMC caution keeping broad index bets off the table.

Guidance quality, not whether a company beat or missed on the current quarter, is the variable separating winners from losers this earnings season.

The earnings calendar for late April through early May brings a fresh wave of high-profile reports:

With the 10-year yield near 4.35% and rates expected to hold, companies that raise guidance despite elevated borrowing costs are positioned to be disproportionately rewarded. The Fed’s rate decision, imminent as of this writing, will set the macro tone for whether the market’s appetite for risk broadens or narrows further.

Investors who carry the guidance-over-results framework into the next wave of reports are better equipped to anticipate which post-earnings moves will be sharp and which will be muted. The pattern from 29 April is clear: tell the market you can grow through this rate environment, and it will reward you. Hesitate on forward guidance, and no backward-looking beat will save the stock.

Investors who want to stress-test the guidance-over-results framework against the broader market backdrop will find our deep-dive into S&P 500 warning signals examines how an all-time high index close on 27 April coexisted with a closed Strait of Hormuz, oil above $112, and Goldman Sachs assigning a 30-35% recession probability, surfacing the structural fragility that rate-sensitive guidance misses could accelerate.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Stock market movers are individual stocks that experience unusually large price swings in a single session, often triggered by earnings reports, clinical trial data, or guidance revisions. They matter because they reveal which catalysts the market is actually pricing, helping investors separate noise from actionable signals.

Both companies beat their current-quarter earnings estimates but issued forward guidance that fell short of market expectations, with Spotify guiding for roughly 17 million net subscriber additions below consensus and Corning projecting Q2 revenue of $4.6 billion against a $4.67 billion estimate. Because stock prices reflect future cash flows rather than past performance, the guidance misses triggered declines of 12-14% and approximately 9% respectively.

Centene beat Q1 2026 adjusted EPS estimates and raised its full-year adjusted EPS guidance above $3.40, signalling that cost controls across its Medicaid and managed care segments were producing tangible results. At least five analyst firms raised their price targets simultaneously, compounding the buying pressure and pushing the stock past its prior consensus average target of $42.00.

Investors should ask three questions in sequence: Did the company raise or lower forward guidance, did multiple analysts revise price targets in the same direction, and is the move company-specific or macro-driven? This framework, illustrated by the six movers on 29 April, helps distinguish durable re-ratings from short-term reactions.

With the 10-year Treasury yield anchored near 4.35%, borrowing costs remain elevated and the Federal Reserve has signalled no urgency to cut rates. This environment means companies that raise forward guidance despite high rates are rewarded disproportionately, while those that miss on guidance face sharper selloffs because there is no broad market momentum to cushion the drop.