Virtu Financial just posted quarterly revenue of $1,095.3 million, a figure that nearly doubled analyst expectations and made Q1 2026 the most profitable quarter in the firm’s history. The results, reported 29 April 2026, arrived at a moment when market volatility has become the defining feature of the 2026 trading environment, and investors in market-structure names are watching closely for evidence of structural earnings power versus a one-off windfall. What follows unpacks every layer of the beat: the headline Virtu Financial earnings, what drove them inside the business, how management is reinvesting the windfall, and what valuation metrics say about where the stock goes from here.

The numbers behind Virtu’s historic quarter

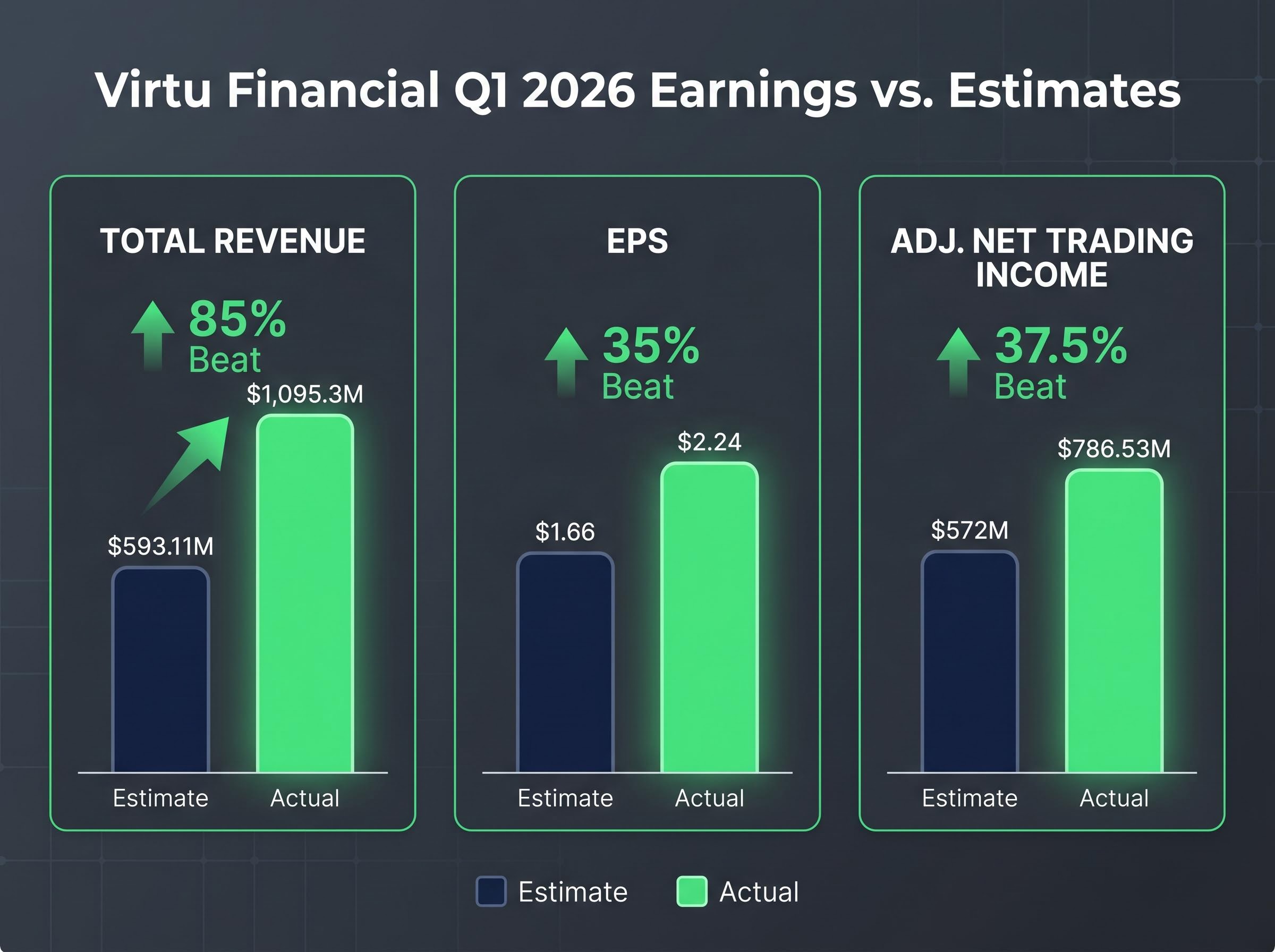

The scale of the outperformance is difficult to overstate. Total revenues of $1,095.3 million exceeded the $593.11 million consensus estimate by approximately 85 percent.

Revenue beat: approximately 85 percent above Wall Street consensus.

Earnings per share came in at $2.24 against a $1.66 estimate, a beat of more than 35 percent. Adjusted Net Trading Income (ANTI), which captures the firm’s core spread and fee income, reached $786.53 million, topping estimates by 37.5 percent. Adjusted EBITDA hit $521 million with a 66 percent margin.

Virtu’s 66 percent adjusted EBITDA margin reflects the economics of a fixed-cost technology platform: once the core execution infrastructure is built, incremental trading volume flows through at minimal marginal cost, which explains why a doubling of revenue can produce a near-tripling of profit relative to lower-volatility periods.

The clearest single expression of the quarter’s scale sits in the net profit line: $346.6 million, nearly double the prior comparable period.

| Metric | Reported | Estimate | Beat (%) |

|---|---|---|---|

| Total Revenue | $1,095.3M | $593.11M | ~85% |

| EPS | $2.24 | $1.66 | ~35% |

| Adj. Net Trading Income | $786.53M | $572M | ~37.5% |

| Net Profit | $346.6M | Prior period ~$175M | ~98% |

For investors in market-structure names, the breadth of the beat matters as much as the magnitude. When outperformance spans revenue, EPS, and margin simultaneously, it signals operational leverage rather than a single favourable line item.

When big ASX news breaks, our subscribers know first

What volatility actually means for a market-maker’s bottom line

Understanding why Virtu thrives in turbulent markets requires a brief look at what the firm actually does. Virtu earns income by acting as a counterparty on both sides of millions of daily transactions, capturing the spread between bid and ask prices. It does not bet on whether markets rise or fall. It profits from being the intermediary regardless of direction.

Across the broader HFT sector, firms like Jane Street and Citadel Securities have invested heavily in market-making infrastructure, including co-located servers, custom execution platforms, and low-latency network architecture, to ensure they can process millions of transactions at the speeds required to reliably capture spread income during volatile sessions.

Three conditions amplify market-maker income:

- Wider bid-ask spreads, which expand during periods of uncertainty

- Higher trading volumes, as more participants enter and exit positions

- Faster price movement, which creates more frequent opportunities to capture spread

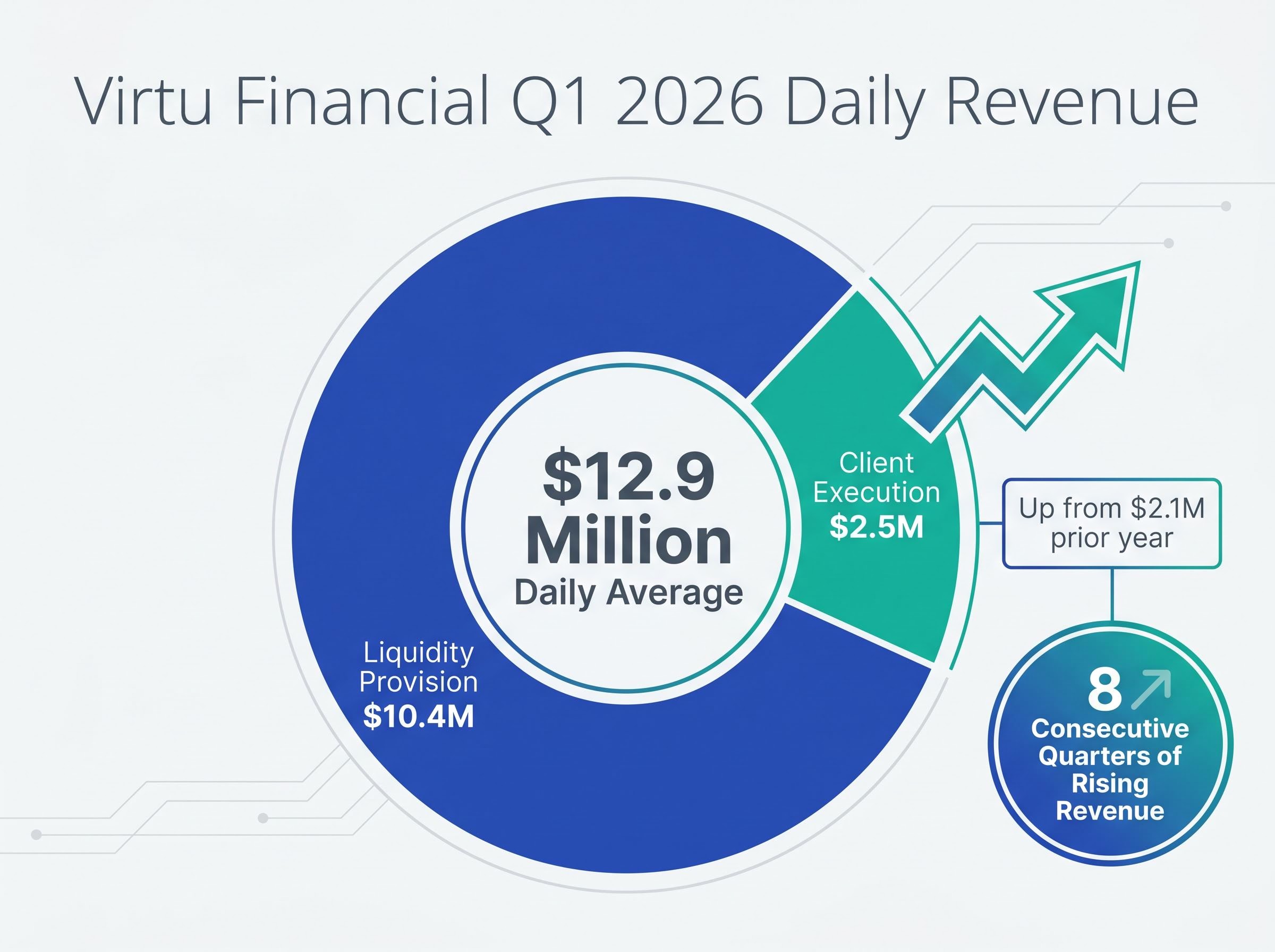

Daily adjusted net trading income averaged $12.9 million in Q1, up 33-34 percent year-over-year. The aggregate ANTI of $787 million for the quarter, and a trailing twelve-month return on deployed capital of 107 percent, are the quantitative expression of this volatility tailwind, as Finance Magnates and the firm’s own earnings commentary attributed.

This mechanic reframes the earnings beat. It is not luck; it is a structural feature of the business model that rewards elevated market uncertainty, which makes Virtu a distinctive holding in turbulent macro environments.

Divisional breakdown: where the $12.9 million daily average came from

The $12.9 million daily figure breaks into two distinct revenue engines. The liquidity provision segment, Virtu’s core market-making arm, generated $10.4 million per day. The client execution division contributed $2.5 million daily.

| Segment | Daily Revenue Q1 2026 | Daily Revenue Prior Year | Change |

|---|---|---|---|

| Liquidity Provision | $10.4M | — | Primary growth driver |

| Client Execution | $2.5M | $2.1M | +~19% |

Client execution’s eight-quarter streak

The execution division’s $2.5 million daily figure compares favourably to its $2.1 million daily average over the prior year, representing momentum that extends beyond the volatility cycle. CFO Cindy Lee and Co-President Joseph Molluso have both pointed to this division’s trajectory in earnings commentary.

More telling is the streak itself: eight consecutive quarters of rising total trading revenue in the execution division. That pattern signals structural client-acquisition progress, not a one-period spike. Investors tracking whether Virtu’s growth is concentrated in a single volatile-dependent segment will find reassurance in a secondary business line expanding on its own terms.

Capital expansion and the talent war Virtu is choosing to win

Virtu deployed additional trading capital during the quarter, bringing total deployed capital to a significantly expanded base. With a trailing twelve-month return on deployed capital of 107 percent, the rationale for putting more money to work is straightforward: every incremental dollar is generating more than a dollar of return annually.

The firm is scaling three operational pillars simultaneously:

- Deployed capital: Increased by approximately $500 million to $2.6 billion

- Headcount: Targeting 1,100 employees, up from 1,027 at end-2025

- Compensation framework: Compensation represented 22 percent of total revenue in Q1, reflecting an explicit decision to pay above-market rates

CEO Aaron Simons has stated that outbidding competitors for elite engineering and quantitative talent generates superior shareholder value, a position that frames elevated compensation as investment rather than expense.

CFO Cindy Lee reinforced this view by connecting the talent strategy directly to the firm’s ability to capture trading opportunities at scale. The capital and talent expansion signals that management views Q1 as a platform to build from, not a peak to protect, which carries direct implications for cost structure and future earnings potential.

Valuation, analyst sentiment, and what the forward numbers imply

Shares rose approximately 5.81 percent in pre-market trading to roughly $51.75 following the announcement, extending a year-to-date gain of approximately 52.5 percent from the 31 December 2025 close of $33.32.

Despite that run, the valuation metrics suggest the market is still pricing Virtu at a discount to its forward earnings trajectory:

- P/E multiple: 9.5x

- PEG ratio: 0.13

- Return on equity: 31 percent

- Full-year 2026 EPS consensus: $10.16 (following six upward revisions)

A PEG ratio of 0.13: conventionally, a PEG below 1.0 signals undervaluation relative to growth. At 0.13, the gap between price and expected earnings expansion is unusually wide.

Zacks upgraded Virtu to a Rank 1 Strong Buy on 9 April 2026, citing favourable estimate revisions and four consecutive quarterly beats. Six analysts raised their forward earnings estimates following the Q1 results. A stock already up more than 50 percent year-to-date that still carries a single-digit P/E and a PEG well below 1.0 is an unusual combination, one that makes the valuation picture worth examining rather than assuming the run has played out.

For investors wanting to quantify the market’s expectation for Virtu’s future price movement, our dedicated guide to options pricing during earnings season walks through a 5-step framework for reading implied volatility signals, comparing front-month straddle costs to historical volatility norms, and translating earnings event risk into actionable position sizing decisions.

Virtu’s record quarter signals more than a good three months for one firm

Virtu occupies a unique position in public markets. It is the only major HFT and market-making firm with publicly disclosed earnings, which makes its results a proxy for understanding how volatility translates into income across the broader category.

The strategic signals from Q1 reinforce a firm doubling down on its core model. Capital deployment at scale, an eight-quarter execution streak, and management’s explicit rejection of directional trading or asset management expansion, as stated by Co-President Joseph Molluso and CEO Aaron Simons, all point in the same direction.

The Q4 2025 EPS beat of $1.85 versus a $1.24 estimate provides additional context: Virtu has now delivered consecutive quarters of significant outperformance. The forward analyst consensus of $10.16 for full-year 2026 EPS is the market’s current answer to the sustainability question.

Three forward-looking questions investors should monitor:

- Volatility persistence: Whether Q1 2026 trading conditions carry into subsequent quarters

- Capital deployment returns: Whether the expanded $2.6 billion base continues to generate triple-digit returns on capital

- Execution division trajectory: Whether the eight-quarter revenue streak extends, confirming structural growth independent of volatility

These statements are speculative and subject to change based on market developments and company performance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.