The Reserve Bank of Australia raised the cash rate target in March 2026, and the immediate impact on everyday trading volumes was stark. Global policy shifts and mounting local economic pressures are forcing individual market participants to rapidly rethink their asset allocation strategies. Tracking current retail investor trends provides a clear view into how these macroeconomic triggers dictate broad market participation across the country. Many everyday participants are responding to the tightened monetary environment by rebalancing their holdings to manage geographic and sector concentration risks. This analysis dissects the specific transaction data behind these recent portfolio adjustments across different demographics. Examining these capital flows reveals a consistent behavioural pattern in modern financial markets. The data ultimately demonstrates why untouched, passive investment strategies frequently outperform reactive trading, even when domestic economic conditions feel highly uncertain.

Policy Shocks and the Immediate Retail Paralysis

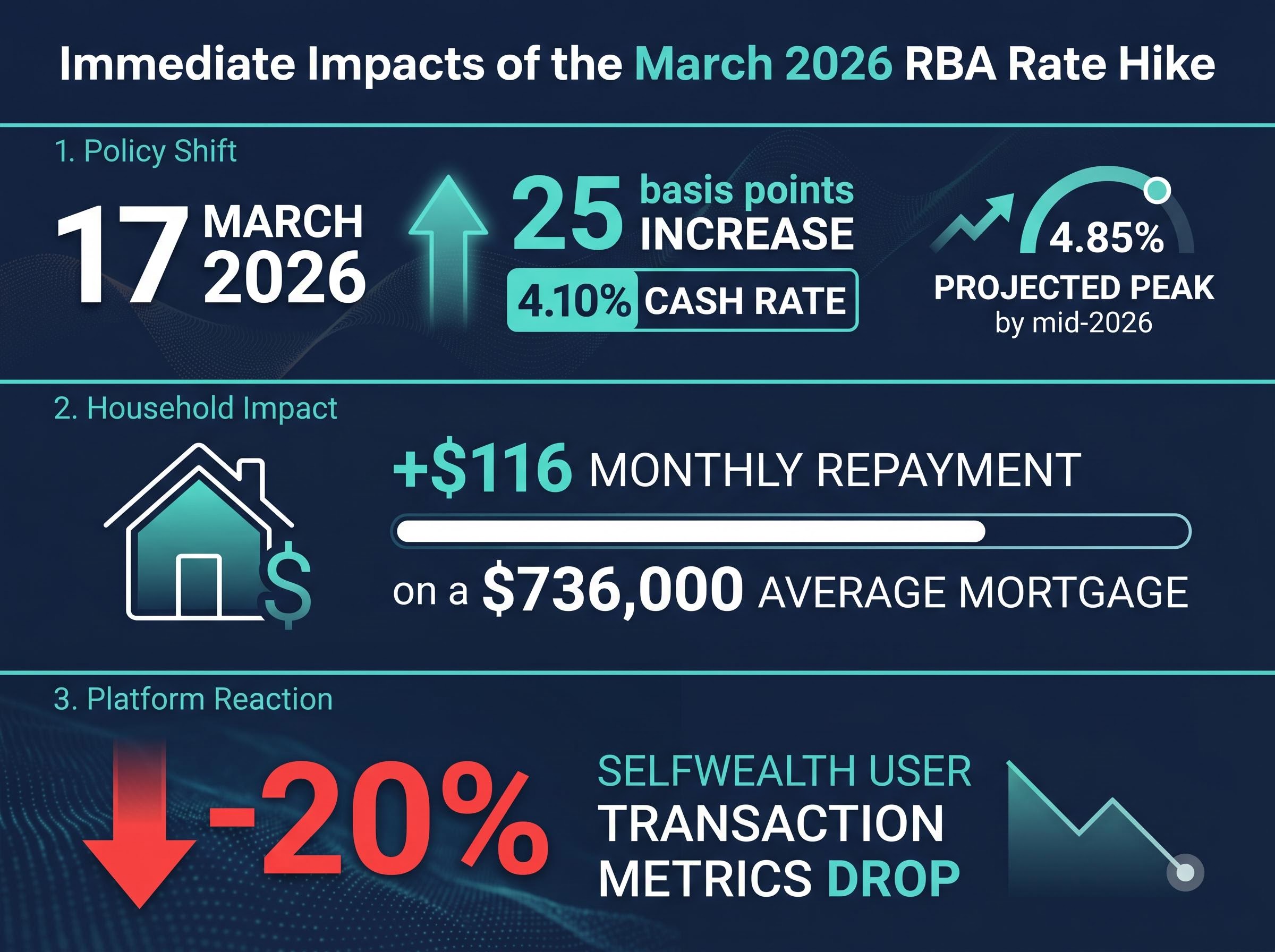

The macroeconomic reality shifted abruptly on 17 March 2026. The Reserve Bank of Australia increased the cash rate target by 25 basis points to 4.10%, with revised forecasts projecting a peak of 4.85% by mid-2026. This monetary policy tightening sent cascading effects through rate-sensitive sectors of the domestic economy.

The official RBA monetary policy decision emphasised that persistent inflation and capacity constraints necessitated this aggressive tightening approach, setting the stage for the broader market reaction.

Accelerated news cycles and rapid valuation fluctuations began generating heightened anxiety among individual market participants almost immediately. The tangible impact on everyday finances compounded this market uncertainty. The March hike added an estimated $116 in monthly repayments to an average $736,000 Australian mortgage.

Expert Perspective on Rate Impacts “The immediate pass-through of these rate decisions creates distinct pressure on rate-sensitive sectors like domestic banks and real estate investment trusts,” said Alice Shen, an analyst at VanEck.

Understanding the Volume Drop

This sudden constraint on household capital triggered a measurable shift in market participation. According to unverified platform data, internal statistics tracked by Selfwealth indicated a 20% drop in user transaction metrics immediately following the RBA interest rate adjustment.

This stark drop contrasts sharply with the typical surge in activity observed during global announcements. Participant anxiety frequently manifests as temporary market paralysis, where everyday investors pause their capital deployment to reassess their positions. The drop in transaction volume highlights how macroeconomic levers directly dictate everyday trading behaviour.

The mechanism behind this 20% decline reflects a wait-and-see approach. Individuals are calculating the dual impact of higher mortgage repayments and lower corporate earnings before committing new capital. Market volatility functions as a systemic reaction rather than an isolated event, providing context for the anxiety currently observed among retail participants.

When big ASX news breaks, our subscribers know first

Capital Flight from Defensive Metals to Global Equities

As the initial paralysis subsided, a visible asset rotation pattern emerged across platform data. Capital began shifting away from the safe-haven physical commodities that dominated portfolios in late 2025.

Precious metal acquisition metrics declined significantly throughout the quarter. According to unverified estimates, these defensive assets now account for less than 70% of recorded platform transaction volumes.

This capital flight reallocated systematically toward the broader financial sector, global healthcare, and technology options. The Selfwealth by Syfe Quarterly Investor Pulse Index for first-quarter 2026 captured a clear transition from local Australian options to foreign-focused exchange-traded products.

These international index options became the most frequently acquired asset class during the quarter. This rotation represents a deliberate search for geographic diversification. Market participants are actively seeking protection against local concentration risks tied to the domestic rate-tightening cycle.

| Asset Class Focus | Late 2025 Allocation Preference | Early 2026 Allocation Preference | Primary Driver |

|---|---|---|---|

| Precious Metals | High (Dominant safe-haven) | Declining (Under 70% of peak volume) | Shift away from physical defensives |

| Domestic Equities | Moderate | Low | Local rate-tightening risks |

| Global/Tech ETFs | Low | High (Most acquired class) | Geographic diversification |

Analysing where smart capital is flowing allows participants to benchmark their own portfolio adjustments against broader diversification trends. The shift away from Australian equities indicates a growing awareness of the limitations inherent in a domestically concentrated portfolio. Investors are utilising foreign-focused exchange-traded products to access growth sectors that remain underrepresented on the Australian Securities Exchange. By rotating into global equities, everyday participants are attempting to insulate their capital from the immediate effects of local monetary tightening.

For readers interested in how these global allocations protect against domestic weakness, our detailed coverage of international ETFs as an inflation hedge explores the specific technology and healthcare funds that are currently replacing traditional safe havens.

The Psychology of Reactive Trading in Accelerated News Cycles

The data indicates that everyday investors are prone to over-trading the news cycle when faced with systemic market inefficiencies. Behavioural finance identifies several cognitive traps that trigger these sudden portfolio adjustments. Many individuals confuse frequent, reactive trading with effective risk management.

When market conditions shift rapidly, the urge to act becomes a primary psychological driver. Historical data shows a transaction surge concurrent with previous United States import levy announcements. Financial experts consistently warn that these rapid responses to accelerated news cycles severely erode long-term capital generation.

Recognising the underlying biases helps participants actively prevent emotional decisions from damaging their long-term returns. The most common emotional triggers that prompt unnecessary portfolio adjustments include:

Loss aversion: Selling well-performing assets prematurely to protect minor gains during a broader market dip. Recency bias: Assuming that the negative market movement of the past week will continue indefinitely into the future. Action bias: Feeling a psychological need to execute trades during volatile periods to regain a sense of control. Information overload: Reacting to daily macroeconomic headlines rather than adhering to a long-term investment strategy.

Understanding these psychological mechanisms provides investors with a framework to evaluate their impulses. The data shows that emotional trading frequently results in selling at local minimums and buying at price peaks. Identifying these cognitive traps serves as a psychological mirror for the everyday market participant.

Generational Divides in Index Allocation Strategies

Different age cohorts are adopting varied approaches to handle ongoing market turbulence. Younger investors are heavily driving the unprecedented growth of the Australian index fund market. These participants are utilising exchange-traded vehicles as foundational building blocks for multi-national portfolios.

Industry projections indicate the Australian ETF market will reach $380 billion in assets under management by the end of 2026. Past performance does not guarantee future results, and these financial projections are subject to market conditions and various risk factors. Currently, 2.7 million Australians utilise these funds, with 80% planning to increase their holdings this year.

These State Street market projections identify Millennials and Generation Z as the dominant catalysts behind this surge, as they aggressively transition wealth into structural fund vehicles.

The demographic data reveals contrasting methodologies for managing risk exposure. According to unverified estimates, Millennial demographic users are dedicating approximately 70% of their total investment capital strictly to exchange-traded funds. Conversely, Generation Z and Generation X participants are maintaining a nearly even allocation split between specific company equities and pooled index structures.

| Demographic Cohort | Index Fund Allocation | Direct Equity Allocation | Primary Strategy Approach |

|---|---|---|---|

| Millennials | 70% | 30% | Aggressive index adoption |

| Generation Z | 50% | 50% | Balanced hybrid exposure |

| Generation X | 50% | 50% | Balanced hybrid exposure |

Reviewing these demographic splits provides a valuable reference point for adjusting risk exposure through structured index products. The aggressive index adoption by Millennials reflects a strong preference for passive, broad-market exposure over individual stock selection. Meanwhile, the balanced approach of Generation Z and Generation X suggests a hybrid strategy, combining the stability of index funds with the targeted growth potential of specific company equities.

The Dead Investor Paradigm and Wealth Erosion

The ultimate consequence of reactive portfolio adjustment is measurable, long-term wealth destruction. Behavioural finance researchers frequently cite the dead investors phenomenon to illustrate the power of passive management. This concept originated from studies showing that untouched accounts belonging to deceased individuals frequently beat the broader market.

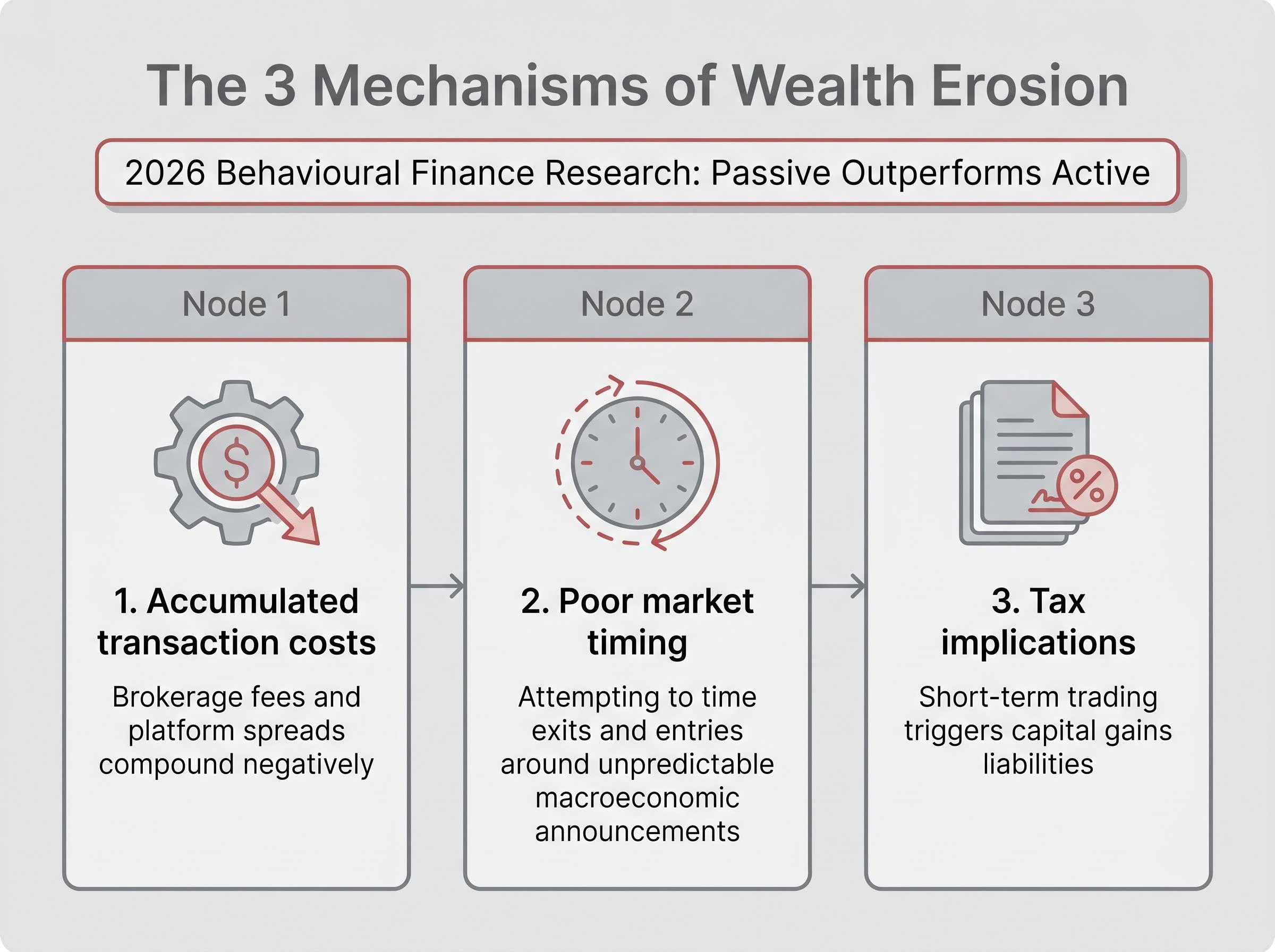

These dormant portfolios succeed by simply avoiding the active trading penalty. Recent 2026 behavioural finance research confirms that passive, inactive strategies consistently outperform active trading during periods of macroeconomic turbulence.

Frequent trading systematically erodes long-term capital generation through three specific mechanisms:

- Accumulated transaction costs: Every portfolio adjustment incurs brokerage fees and platform spreads that compound negatively over time.

- Poor market timing: Retail participants consistently underperform the index by attempting to time exits and entries around unpredictable macroeconomic announcements.

- Tax implications: Short-term trading triggers capital gains liabilities that reduce the total compounding base of the portfolio.

This data validates inaction as a legitimate and highly profitable long-term strategy. Doing nothing during market volatility often yields the strongest financial outcomes. Embracing the dead investor paradigm empowers everyday participants to leave their capital untouched while the broader market absorbs short-term shocks.

However, market participants must still monitor extreme index concentration within global benchmarks, as passive exposure to a highly concentrated market can inadvertently amplify portfolio risk during systemic technology downturns.

By recognising the damage caused by frequent trading, investors can reframe their perspective on market turbulence. The ability to endure temporary valuation drops without executing a trade is a measurable advantage in long-term wealth generation.

Sustaining Wealth Beyond the Macroeconomic Noise

Macroeconomic triggers, such as the RBA rate hikes, will continue to dictate short-term market sentiment and volatility. However, the data confirms that reactionary trading in response to these events ultimately destroys wealth over an extended timeline.

The broad shift toward global diversification and index products represents a healthier alternative to chasing volatile commodity trends or attempting to time the news cycle. Investors are encouraged to review their asset allocation for long-term resilience rather than short-term news cycle reactivity.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.