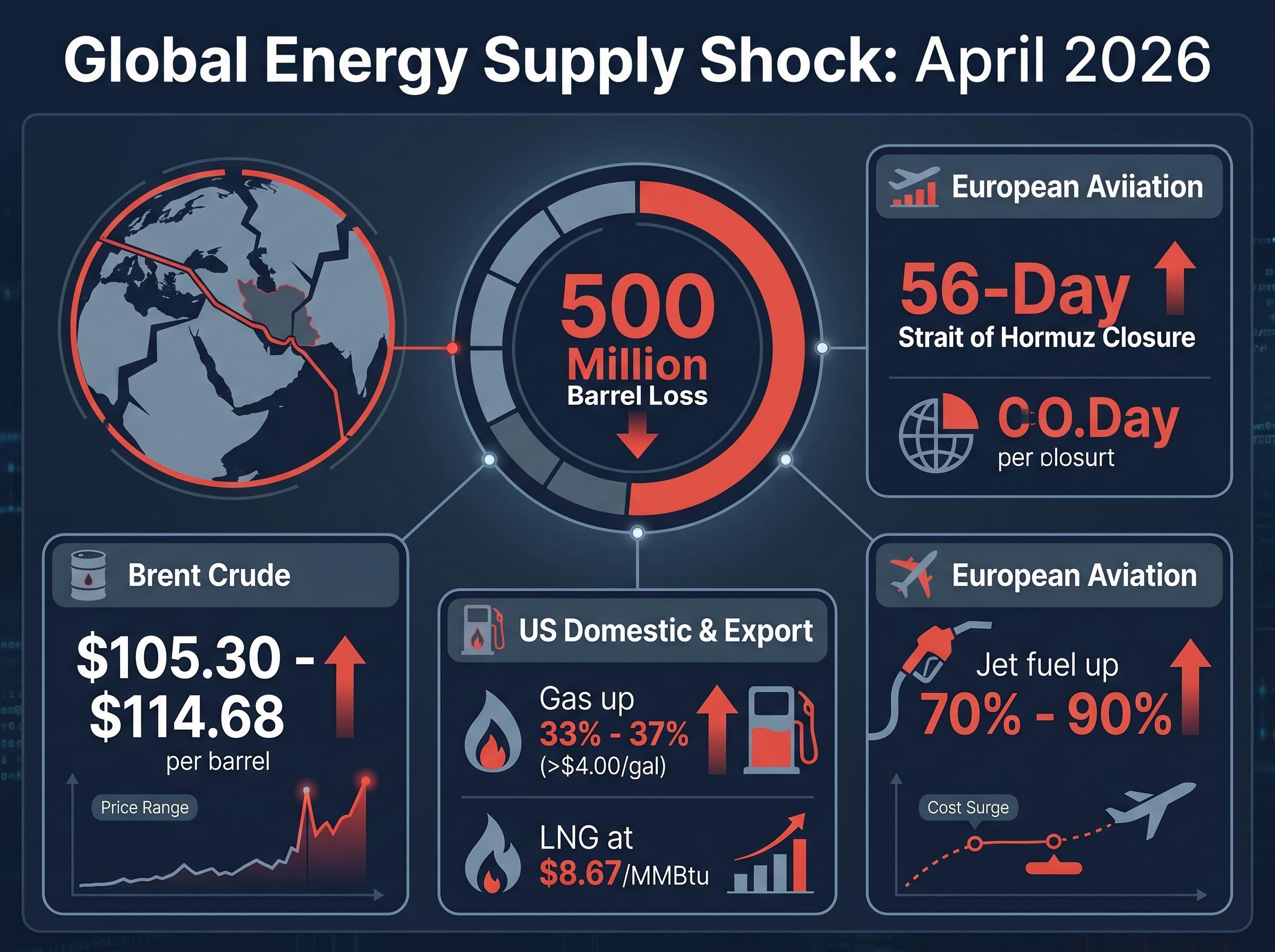

Fifty-six days into the commercial shutdown of the Strait of Hormuz, the global energy market has permanently absorbed a staggering loss of 500 million barrels of petroleum. This logistical disruption has triggered a severe structural shock across international supply chains as of April 2026, forcing inflation metrics back up and destabilising standard market behaviours. Investors relying on traditional safe haven investments are watching their wealth preservation strategies falter under the weight of simultaneous supply constraints and elevated borrowing costs.

The current geopolitical crisis demands a complete reassessment of portfolio protection. What follows is an analytical breakdown of why conventional safety nets are breaking down in a high-yield, energy-starved environment. By understanding the failure points of legacy crisis models, investors can restructure their portfolios to withstand persistent supply bottlenecks and capture the distinct opportunities emerging from this macroeconomic shift.

The Scale of the April 2026 Logistical Chokepoint

The sheer physical scale of the supply bottleneck dictates the macroeconomic gravity of the current crisis. The ongoing closure of the Strait of Hormuz has transformed from a temporary geopolitical event into a severe, prolonged structural shock. This disruption rippled immediately through global petroleum and natural gas availability, creating persistent upward pressure on international pricing.

The loss of approximately 500 million barrels of oil over the 56-day crisis period has fundamentally rewired commodity flows. This energy spike places immediate, undeniable pressure on central bank policy, complicating efforts to manage inflation while sustaining economic growth. The disparate regional price spikes illustrate the depth of this logistical chokepoint:

The severity of this dislocation aligns with IEA global supply risk assessments, which classify sustained impediments to transit volumes through this maritime corridor as a historic physical disruption.

Brent Crude: Futures are currently trading between $105.30 and $114.68 per barrel as of late April 2026, locking in elevated baseline costs for manufacturers. US Natural Gas and Fuel: Domestic gas prices have surged 33% to 37%, pushing past $4.00 per gallon, while US liquefied natural gas export prices have hit $8.67 per MMBtu. * European Aviation Transport: Continental jet fuel costs have spiked by 70% to 90%, severely degrading the margins of logistics and travel operators.

Recognising the strictly logistical nature of this crisis is the prerequisite for adjusting portfolio expectations. The financial fallout directly traces back to these physical constraints, proving that the energy inflation is a structural reality rather than a speculative distortion.

When big ASX news breaks, our subscribers know first

Why Historic Crisis Frameworks No Longer Apply

Market participants often assume all economic crises trigger identical deflationary patterns, but the current macroeconomic climate actively dismantles that framework. A standard demand shock, such as the 2008 financial crisis, creates deflation as consumer spending collapses and central banks cut rates to stimulate growth. The current environment mirrors the 1970s and 2022, where supply-driven shortages create temporary but severe headline inflation.

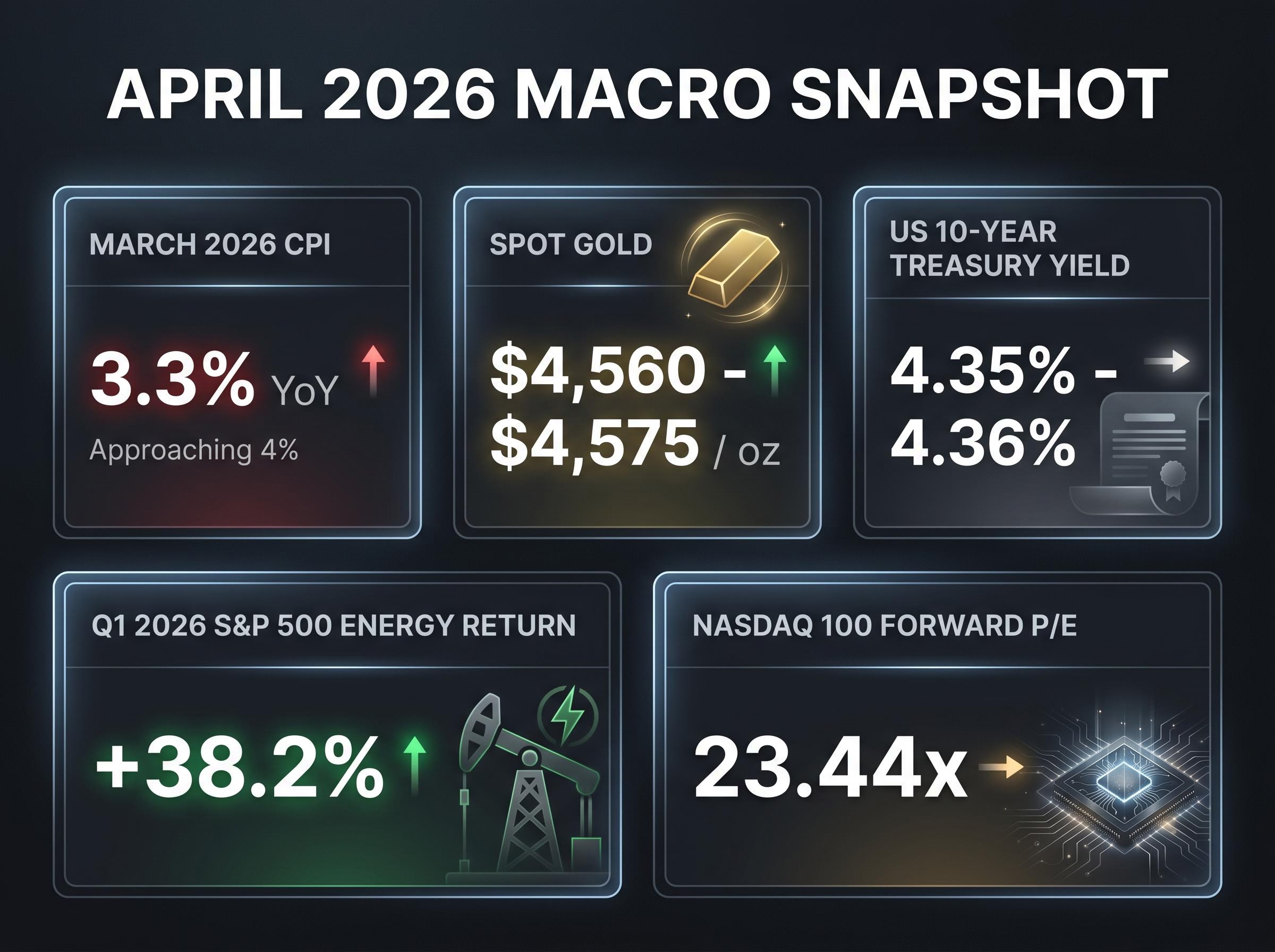

Higher energy prices force monetary tightening at the exact moment corporate expansion slows, creating a complex stagflation threat. With US inflation approaching 4% and the March 2026 CPI reported at 3.3% year-over-year, central banks remain constrained. They cannot easily lower rates to support falling equities while energy costs continue driving up the baseline cost of living.

Macroeconomic Outlook “The global economy is facing higher inflation, tighter financial conditions, and growing economic uncertainty,” reports the Economic Times. Hancock Whitney projects this is driven by infrastructure damage that will ensure “higher energy prices for an extended period.”

Understanding these stagflation mechanics helps everyday investors diagnose why holding cash or standard government debt is uniquely punishing right now. Deflationary crises reward cash, but supply shock stagflation steadily erodes purchasing power while depressing equity multiples.

The Stagflation Threat

The 1970s inflation cycle was characterised by stagnant commercial expansion combined with relentless price increases, a dynamic visible in today’s supply-constrained economy. However, current central bank constraints are more pronounced due to significantly higher baseline global debt levels. This reality means tightening financial conditions rapidly limit corporate borrowing capabilities, forcing companies to absorb elevated energy costs directly into their margins.

Because heavily indebted companies will struggle to absorb these sustained borrowing costs, rigorous equity selection in a capital-constrained environment must prioritize low leverage and demonstrably strong pricing power.

The Devaluation of Traditional Wealth Preservation Assets

Sustained inflation and high borrowing costs are systematically breaking down the mechanics of trusted portfolio safety nets. In a typical recession, capital automatically rotates into long-duration government debt and precious metals to wait out the volatility. The current high-yield environment, however, severely punishes these historical allocations.

There is a stark inverse relationship between elevated interest rates and zero-yield assets. Spot gold is currently trading at nominally high levels of $4,560 to $4,575 per ounce, but its strength is highly vulnerable to the commanding posture of the US dollar. Analysts at Argent Financial state that persistently tight policy rates naturally diminish the bid for traditional bond safe havens, as yields climb to match inflation expectations.

Long-duration government debt faces intense pressure from expectations of massive future deficits meant to fund prolonged geopolitical conflicts. With the US 10-Year Treasury yield climbing to 4.35% to 4.36%, investors holding legacy bond portfolios are experiencing significant capital depreciation. The automatic rotation into traditional safety nets is currently a flawed strategy that erodes wealth rather than protecting it.

Institutional guidance from BlackRock portfolio construction research reinforces that long duration bonds can no longer function as reliable buffers when persistent fiscal pressures unmoor historical inflation expectations.

| Asset Class | Historical Crisis Role | April 2026 Status | Primary Vulnerability |

|---|---|---|---|

| 10-Year US Treasuries | Capital preservation and fixed yield | Yields surging to 4.36% | Duration risk amid sustained rate hikes |

| Precious Metals (Gold) | Zero-counterparty inflation hedge | Trading at $4,575 per ounce | Opportunity cost against high cash rates |

| Cash Equivalents | Absolute liquidity and volatility shield | Eroding against 4% inflation | Purchasing power destruction |

| Utility Stocks | Defensive dividend generation | Underperforming broad market | High debt loads and rising borrowing costs |

Fossil Fuel Dependency and the Currency Realignment

Reliance on imported energy has completely rewired international currency strength, establishing energy independence as the primary metric for sovereign valuation. The Japanese yen serves as the primary cautionary tale of this dynamic. As an industrial economy heavily dependent on petroleum imports, Japan has seen its purchasing power collapse under the weight of soaring dollar-denominated energy costs.

The dominance of the US dollar is currently sustained by a powerful combination of domestic energy self-sufficiency and high Federal Reserve borrowing costs. This dynamic starkly contrasts energy-importing nations with resource-exporting nations, highlighting distinct pockets of geographic resilience for international investors. Currency valuations impact everything from international stock returns to local purchasing power, making geographic exposure a vital portfolio consideration. The specific performance factors defining this realignment include:

While this resource exporter resilience provides a natural currency buffer for nations like Australia, investors must still navigate elevated domestic inflation and sovereign bond yield pressures that complicate fixed-income allocations.

The US Dollar: Dominant and resilient, supported by domestic liquefied natural gas production and aggressive monetary policy that attracts global capital. The Japanese Yen: Collapsing to an exchange rate of 159.55 against the dollar, purely driven by the extreme cost burden of importing baseline energy needs. The Canadian Dollar: Demonstrating resource exporter resilience, holding steady at approximately 1.35 against the US dollar due to domestic petroleum production. The Australian Dollar: Benefiting from significant commodity export volumes, maintaining stability at an exchange rate of 1.46 against the greenback.

Tactical Portfolio Maneuvers for Sustained Volatility

Translating this complex macroeconomic environment into clear asset allocation requires abandoning static defense for tactical deployment. Wealth professionals and institutional advisory boards, including Confluence Financial Partners, suggest a decisive shift away from traditional fixed-duration debt towards yield-generating alternatives and sectors directly benefiting from current constraints.

The immediate strategic priority is an active energy sector overweight. Energy equities led the S&P 500 with a +38.2% return in Q1 2026, successfully absorbing the shock while the broader market compressed. Conversely, forward price-to-earnings multiples for the Nasdaq 100 are hovering around 23.44x, suggesting technology equities remain fully priced despite the elevated cost of capital. Investors should consider the following portfolio adjustments to manage the structurally altered market:

- Prioritise Direct Inflation Hedges: Reallocate capital from long-duration bonds into Treasury Inflation-Protected Securities or real asset infrastructure funds that contractually pass rising costs to consumers.

- Overweight Energy Producers: Increase exposure to domestic oil and natural gas equities, which inherently benefit from the ongoing 500 million barrel supply deficit.

- Audit Geographic Exposure: Reduce allocations to unhedged equities in energy-importing jurisdictions, specifically targeting markets severely exposed to currency devaluation.

Liquidity and Deployment Tactics

Maintaining adequate liquidity is vital to acquiring discounted securities during periodic market drawdowns. Investors must hold sufficient cash equivalents to manage immediate living expenses, ensuring they are not forced to liquidate equities into a volatile tape. Establishing regular, automated contribution schedules allows investors to naturally capture equity discounts as market sentiment fluctuates.

Investors exploring how to pair these defensive energy hedges with long-term growth opportunities will find our comprehensive walkthrough of barbell investment strategies for 2026, which details methods for balancing immediate commodity exposure against structural disinflationary megatrends like artificial intelligence.

Securing Capital in an Era of Logistical Constraints

The supply-driven shocks defining April 2026 demand entirely different wealth preservation strategies than typical consumer recessions. Conventional portfolio defense mechanisms are deeply compromised by the combination of sticky inflation and restrictive central bank policy. Strategic positioning in energy assets, resilient resource-backed currencies, and direct inflation hedges offers the most viable path forward for capital protection.

Investors must urgently audit their holdings for hidden vulnerabilities tied to duration risk and international energy dependence. A proactive realignment that acknowledges the physical constraints on global commerce will ultimately outperform static reliance on outdated macroeconomic assumptions.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. Investors should conduct their own research and consult with financial professionals before making investment decisions.