Artificial intelligence infrastructure investment by just five technology corporations is projected to reach up to $700 billion in 2026. This unprecedented capital deployment represents nearly 2% of United States gross domestic product, elevating corporate spending to a primary macroeconomic driver. The late April 2026 earnings season has transformed the financial disclosures of Amazon, Alphabet, Meta, and Microsoft into a critical barometer for the entire hardware ecosystem.

These quarterly reports now dictate the immediate fortunes of semiconductor fabricators, energy providers, and industrial construction firms globally. What follows is a comprehensive breakdown of where this historic capital is flowing and how it single-handedly sustains the current semiconductor equity rally. The analysis also examines the structural limits of this expansion, detailing exactly when Wall Street expects a concrete return on these multi-billion-dollar outlays.

The unprecedented scale of 2026 hyperscaler capital expenditures

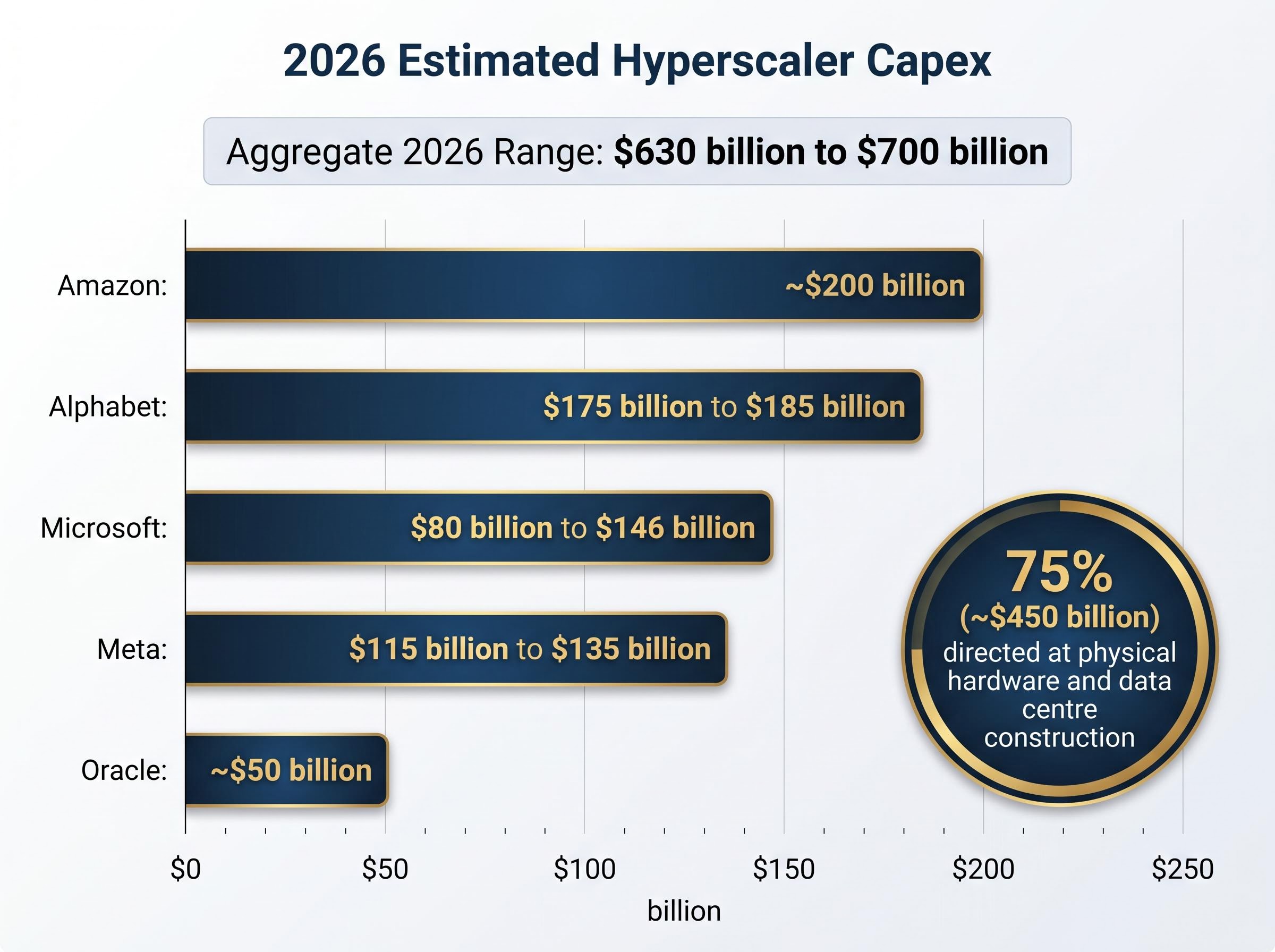

The aggregate 2026 capital expenditure forecasts for the top five hyperscalers reveal an environment completely detached from historical spending patterns. Estimates from Futurum Group and Yahoo Finance project that Alphabet, Amazon, Meta, Microsoft, and Oracle will collectively deploy between $630 billion and $700 billion this calendar year.

This is not a traditional software development cycle defined by engineering headcount. Approximately 75% of these funds, equating to roughly $450 billion, are directed exclusively at physical hardware and data centre construction. Corporate management teams are framing this spending not as cautious investment, but as a necessary sprint driven by the conviction that machine learning workloads will soon consume all available compute power.

Amazon alone is projected to allocate approximately $200 billion, predominantly targeting data centre expansion to protect its lead in cloud infrastructure. Microsoft has outlined a capital expenditure range between $80 billion and $146 billion for its 2026 fiscal year. These figures reflect an intense arms race where failing to secure hardware is viewed as a greater risk than overspending.

These massive capital requirements are uniquely supported by the underlying businesses generating them. According to unverified reports, the combined market valuation of the top four technology corporations now exceeds $10 trillion, providing the tangible cash flows required to sustain this historic hardware procurement cycle. This baseline proves to investors that current market valuations are backed by historic, verifiable capital commitments.

The sheer dominance of these megacap tech stocks introduces significant concentration risk to passive indices, transforming broad market investments into highly focused thematic bets on artificial intelligence infrastructure.

| Company | 2026 Estimated Capex Range | Primary Focus Area |

|---|---|---|

| Alphabet | $175 billion to $185 billion | Hardware and data centre expansion |

| Amazon | ~$200 billion | Data centre expansion and cloud scaling |

| Meta | $115 billion to $135 billion | Scalable facilities and compute silicon |

| Microsoft | $80 billion to $146 billion | AI infrastructure and Azure capacity |

| Oracle | ~$50 billion | Enterprise cloud and physical infrastructure |

When big ASX news breaks, our subscribers know first

Decoding the physical reality of the AI boom

Investors often view cloud computing as an invisible, locationless service hosted in the digital ether. The reality of the current expansion is fundamentally physical, requiring vast tracts of land, massive industrial cooling systems, and dedicated energy infrastructure. Grounding the abstract concept of artificial intelligence in these physical realities is essential for evaluating emerging supply chain constraints.

Meta provides a clear example of this geographic footprint with its ongoing construction of a 1-gigawatt data facility in Ohio and a highly scalable centre in Louisiana. These are not traditional server rooms, but advanced industrial facilities designed specifically to handle the extreme thermal output of modern graphics processing units.

Beyond advanced processing units, these hyperscale data centers require immense cold and warm storage arrays, driving a structural supercycle that has substantially elevated the earnings potential for specialized hard disk drive manufacturers.

According to unverified financial projections, these infrastructure investments will consume nearly 90% of hyperscaler operating cash flow by 2027. This represents a dramatic escalation from the 50% allocation recorded in 2024, underscoring how resource-intensive the sector has become.

The physical reality of this boom rests on three core infrastructure pillars:

Compute silicon, comprising the advanced processors and memory chips that physically execute the algorithmic calculations. Data centre facilities, which provide the highly specialised thermal management and physical architecture required to house thousands of server racks. * Power generation requirements, encompassing the dedicated utility connections and local grid enhancements necessary to supply uninterrupted gigawatt-scale electricity.

Fueling the historic April 2026 semiconductor supercycle

This multi-billion-dollar corporate spending directly engineered the historic spring semiconductor rally. As hyperscalers committed to these massive infrastructure budgets, equity markets immediately priced the guaranteed revenue into the valuations of hardware suppliers.

The Philadelphia SE Semiconductor Index (SOX) serves as the clearest metric of this downstream financial impact. The index posted a 38% gain by mid-April, ultimately peaking at an unprecedented 10,564.01 on 23 April 2026.

While the SOX experienced a minor pullback to close at 9,979.17 on 28 April 2026, the broader trajectory remains firmly established. According to unverified reports, the index has achieved growth exceeding 100% over the trailing twelve-month period, rewarding investors who positioned themselves ahead of the capital expenditure announcements.

According to unverified data, a curated portfolio of 50 artificial intelligence equities recorded a 27.2% valuation increase between late March and late April 2026 alone. These valuations remain hypersensitive to any news regarding end-user commercial expansion targets, as current share prices explicitly assume the hyperscaler spending sprint will continue uninterrupted.

Post-earnings volatility and derivatives pricing

Options markets are actively pricing in the potential for significant stock swings following these simultaneous financial disclosures. Institutional investors use these derivatives to hedge against the volatility that occurs when multi-billion-dollar capital expenditure plans are officially confirmed or revised.

Historical data complicates the current pricing models. According to unverified estimates, Meta has recorded an 8.4% average post-earnings valuation shift historically, yet current options pricing implies a more conservative move of 7.1%. This gap suggests options traders are pricing in slightly more stability than historical patterns would typically justify.

The revenue clock and Wall Street tolerance thresholds

Wall Street has temporarily accepted the necessity of these infrastructure outlays, but investor patience operates on a strict timeline. The underlying tension of the current market cycle is the inevitable demand for these physical assets to generate concrete top-line growth.

Robust cloud division growth is currently keeping investor anxiety at bay and validating the initial capital outlays. First-quarter 2026 expectations show Google Cloud projecting revenue expansion of 28% to 48%.

Similar cloud monetization metrics are appearing across the sector, with Amazon Web Services reaching a massive annualised AI run rate that proves to institutional investors enterprise clients are actively deploying capital for these new capabilities.

Microsoft Azure is similarly expected to post growth between 32% and 39%, capturing up to a 58% year-over-year traffic share gain. These immediate returns prove that the hardware is actively servicing paying commercial clients rather than sitting idle in newly constructed facilities.

However, market strategists warn this grace period is highly finite, with tolerance levels heavily dependent on sustained macroeconomic stability.

Analyst Consensus Outlook Institutional analysts expect Wall Street will only tolerate heavy infrastructure spending without matching proportional revenue growth for a few quarters. According to some estimates, this tolerance window is projected to close within twelve months, after which aggressive capital expenditures must translate directly into sustained margin expansion.

Financial experts consistently note that the market’s current leniency is an anomaly driven by the undeniable profitability of the hyperscalers’ legacy businesses. Unlike previous technological booms, these corporations possess the robust cash flows necessary to self-fund this expansion without immediately diluting shareholder value.

This twelve-month window provides investors with a critical metric to watch in all upcoming earnings reports. It shifts the analytical focus from the raw scale of current spending to the specific revenue thresholds that will trigger the next major market correction if missed.

Macroeconomic shockwaves and emerging physical roadblocks

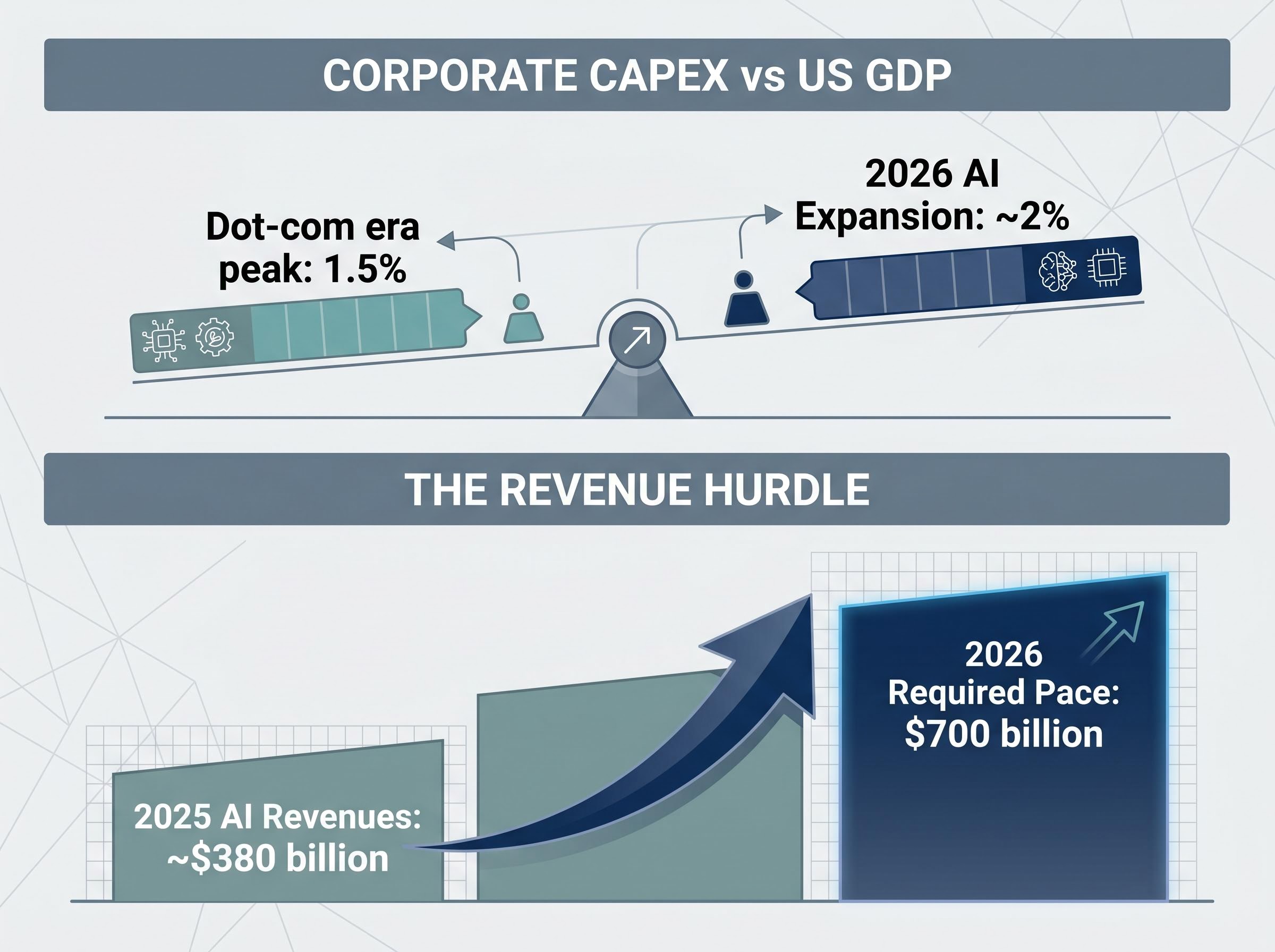

The scale of corporate technology investment has now grown large enough to fundamentally distort the broader United States economy. Estimates place hyperscaler capital expenditures at approximately 2% of United States gross domestic product for 2026.

This explicitly surpasses the 1.5% peak recorded during the height of the dot-com era, marking a new historical threshold for corporate capital deployment. Fidelity data indicates that infrastructure deals tied to this expansion have recently fueled up to 60% of United States economic growth, making the wider economy highly vulnerable to any sector-specific slowdown.

Structural risks are emerging that could force an involuntary spending deceleration, independent of corporate desires. The industry must successfully double its artificial intelligence revenues from roughly $380 billion in 2025 to match the $700 billion spending pace in 2026.

Failure to hit this target will expose the sector to three primary physical and economic roadblocks:

- Local grid limitations, as regional utilities struggle to provision the gigawatt-scale electricity required by concentrated facility builds.

- Hardware obsolescence timelines, where rapid advancements in chip architecture force premature depreciation of billion-dollar server clusters.

- Lagging end-user adoption rates, creating a potential scenario where commercial clients cannot consume the vast compute capacity being constructed.

These constraints represent the contrarian bear case for the technology sector. Identifying these early warning signs allows investors to anticipate an industry slowdown before it fully materialises in the financial markets.

Readers interested in mapping these sector-specific risks against wider macroeconomic headwinds will find our full explainer on broader US consumer vulnerabilities, which breaks down how depleting household savings and rising oil prices could independently trigger the spending deceleration Wall Street fears.

A new economic gravity for the technology sector

The technology sector is currently defined by the core tension between massive capital requirements and a rapidly compressing revenue generation timeline. While 2026 represents peak construction for these hyperscale facilities, the true financial reckoning is scheduled for 2027.

By next year, the corporations deploying these historic sums must demonstrate that their investments have permanently elevated their earning power, rather than merely maintaining competitive parity. The broader technology ecosystem remains completely tethered to the capital expenditure decisions of just five corporations.

As long as the compute hardware is ordered, the semiconductor rally continues on its current trajectory. The moment those orders slow, the entire supply chain will be forced to recalibrate to a new, harsher economic reality.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.