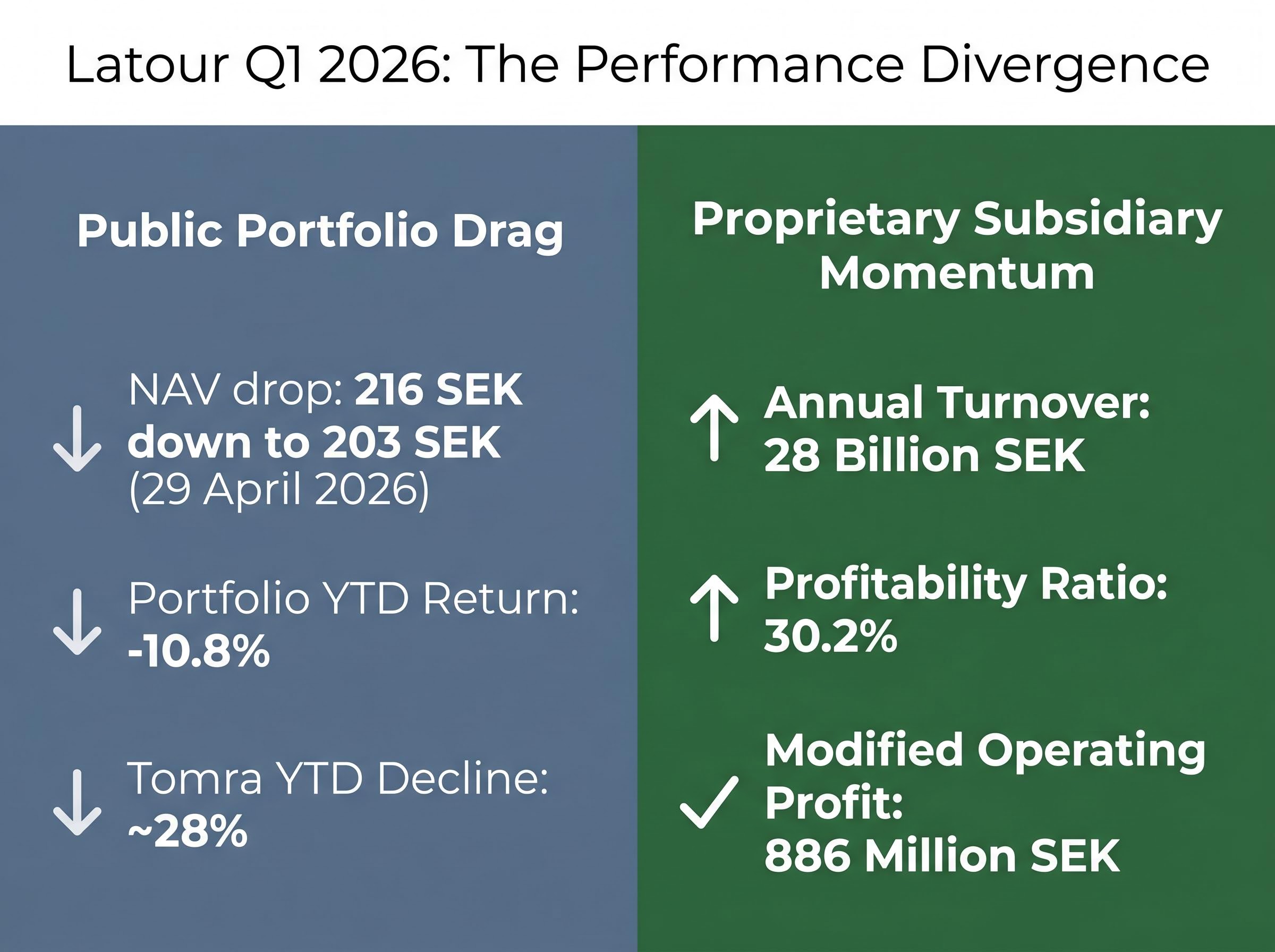

An investment Latour analysis of the first quarter of 2026 reveals a stark divergence between headline market reactions and foundational corporate health. Investment AB Latour reported a drop in its net asset value to 203 Swedish kronor per share on 29 April 2026, down from 216 SEK at the start of the year. This decline occurred against a severe macroeconomic backdrop of foreign exchange headwinds affecting European industrials.

In initial trading following the earnings release, the corporate equity valuation stood at SEK 214.90, reflecting a -2.32% daily drop. However, this public portfolio turbulence masks the predictable, high-margin growth driven by the company’s niche industrial subsidiaries. These wholly-owned proprietary operations reported 28 billion SEK in annual turnover, maintaining stable underlying growth despite broader economic pressures.

While listed assets face temporary valuation compression, the core operating businesses demonstrate substantial pricing power and demand stability. This performance disconnect offers a foundational lens for evaluating the intrinsic value of the enterprise moving forward.

The Divergence Between Listed Assets and Proprietary Momentum

The publicly traded asset portfolio experienced significant drag through the early months of 2026, yielding a -10.8% year-to-date return. This sluggishness contrasts sharply with the SIXRX benchmark, which stood at -1.2% over the same period. The performance lag largely stems from consumer sector stagnation and severe exchange rate disadvantages impacting major holdings like Tomra, which experienced a roughly 28% year-to-date decline.

This initial Latour stock decline effectively erased the historical valuation premium the holding company commands, prompting market analysts to look closer at the true underlying operational metrics.

A sharp pivot to the proprietary industrial subsidiaries reveals a fundamentally different trajectory. These wholly-owned entities generated a 5% baseline expansion in incoming requests during the quarter. They achieved this momentum despite absorbing a 6% revenue hit from currency translations across European markets.

According to company data, this proprietary strength delivered a 30.2% profitability ratio, equating to an 886 million SEK modified operating profit. Executive management, led by Chief Executive Officer Johan Hjertonsson, maintains a long-term holding strategy that contextualises the current volatility. According to company reports, over a 15-year horizon, the traded portfolio has generated a 540% aggregate yield, demonstrating historical resilience through previous cyclical downturns.

| Performance Metric | Public Portfolio | Proprietary Subsidiaries |

|---|---|---|

| Year-to-Date Return | Negative 6.1% | Positive 5.0% baseline growth |

| Currency Impact | Severe valuation compression | Absorbed 6.0% translation hit |

| Key Drivers | Consumer stagnation, FX headwinds | Incoming requests, pricing power |

When big ASX news breaks, our subscribers know first

How Niche Industrial Consolidation Insulates Against Macro Shocks

Understanding the resilience of these subsidiary operations requires examining the mechanics of a niche industrial rollup strategy. This approach involves acquiring highly specialised, dominant players operating within fragmented secondary markets. By consolidating regional monopolies or technical leaders, industrial holding companies secure substantial pricing power across their supply chains.

This rollup methodology mirrors recent Bain strategic M&A analysis, indicating that acquiring specialized capabilities in fragmented secondary markets remains a primary driver for corporate growth.

This dominant market positioning protects operating margins during inflationary spikes or exchange-rate crises. When a subsidiary provides a specialised technical component that competitors cannot replicate, price increases can be passed directly to the end user without sacrificing volume. This structural advantage effectively decouples niche industrial suppliers from standard consumer discretionary spending patterns.

The strategy further benefits from an alignment with ongoing infrastructure upgrades and energy optimisation projects across Europe. These long-term capital deployments provide a predictable baseline of demand regardless of the broader economic cycle. Specialised manufacturers maintain consistent revenue generation because their products serve core infrastructure rather than cyclical consumer wants.

Three key defense mechanisms protect niche industrial subsidiaries during macroeconomic volatility: Substantial pricing power derived from technical leadership and regional market dominance Fragmented market consolidation that drives economies of scale and reduces competitive pricing pressure * Non-cyclical end-market demand anchored by infrastructure, defence, and energy transitions

Fastening and Logistics Drive High-Margin Operational Surges

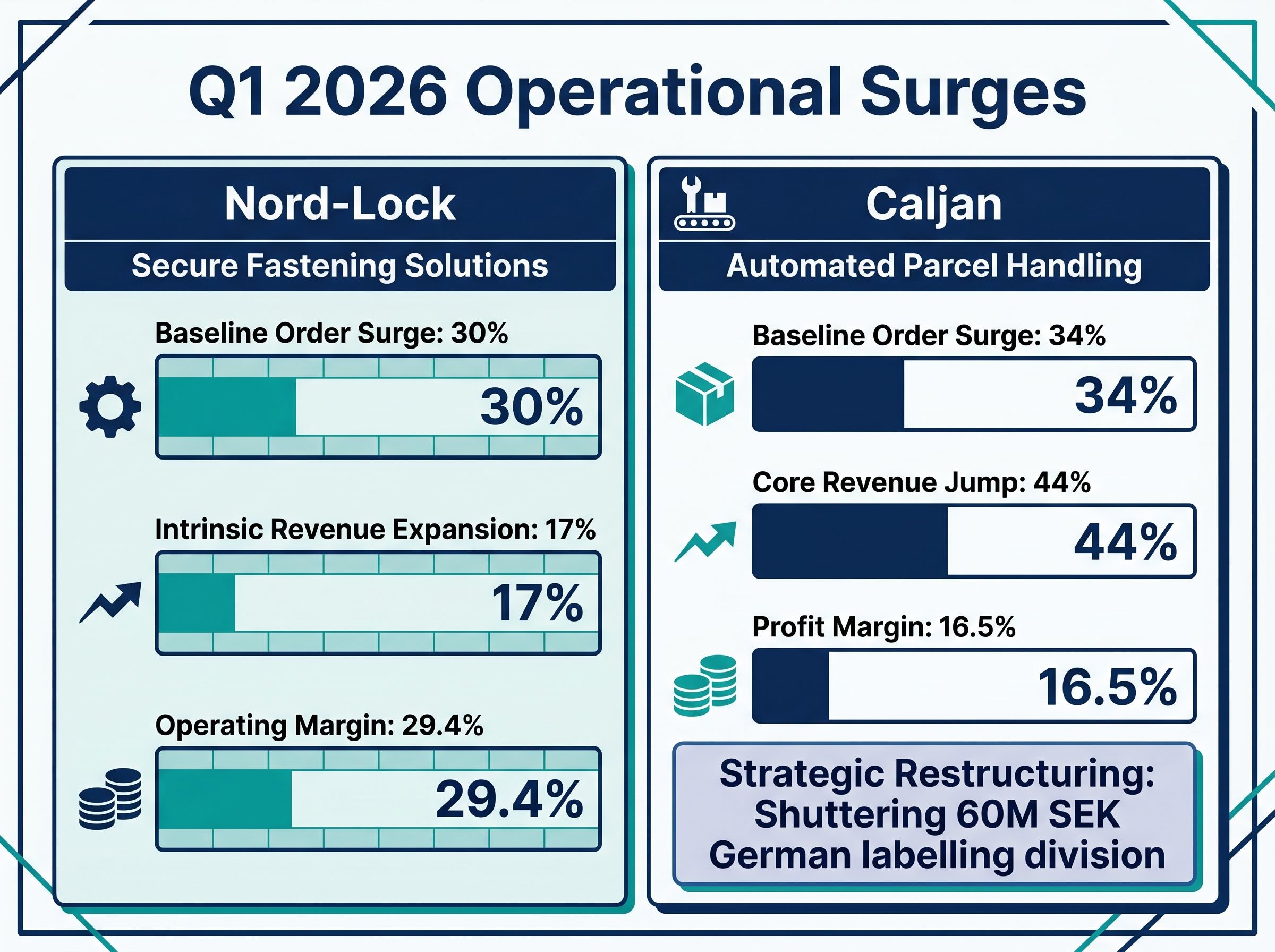

The exceptional performance of specific divisions validates the resilience of this specialised consolidation strategy. Nord-Lock, a proprietary subsidiary focused on secure fastening solutions, demonstrated remarkable momentum throughout the quarter. The division’s success is directly tied to an influx of infrastructure, defence, and railway projects across its target geographies.

According to company data, this strategic market positioning allowed Nord-Lock to achieve a 30% baseline order surge and a 17% intrinsic revenue expansion. These top-line gains translated into a highly lucrative 29.4% operating margin for the fastening division. Similarly, specialised logistics provider Caljan experienced a massive jump in demand for its automated parcel handling solutions.

According to corporate data, Caljan saw baseline orders surge 34%, accompanied by a 44% jump in core revenues. This operational momentum generated a strong 16.5% profit margin for the logistics unit. To protect these aggregate margins, Caljan is currently executing strategic restructuring efforts, including the shuttering of an unprofitable 60 million SEK German labelling division.

Executive Insight “The extraordinary 30% to 34% order surges recorded across our fastening and logistics divisions serve as a key indicator of future revenue realisation, demonstrating strong underlying demand despite currency headwinds.”

Demographic Tailwinds Propel the Innovalift Vertical Mobility Play

While quarterly order surges provide immediate validation, long-term capital compounding relies on structural demographic shifts. Innovalift stands out as a massive revenue generator capitalising directly on an aging European population. The subsidiary addresses the escalating need for residential accessibility and vertical mobility solutions across the continent.

European market expansion aligns directly with Eurostat demographic projections, which forecast a significant acceleration in the elderly population across the continent by 2050.

The European vertical mobility market remains highly fragmented, allowing Innovalift to execute a precise strategy of consolidating established regional brands. According to company metrics, the division currently generates 3.4 billion SEK annually across eleven distinct trademarks. Production metrics highlight this scale, with the subsidiary manufacturing 10,000 elevating systems yearly.

The Recurring Revenue Engine

The true strength of the vertical mobility play lies in its predictable, recurring revenue streams. Innovalift currently maintains 15,000 existing installations, securing consistent capital inflows through service contracts and specialised part supplies. Supplying proprietary parts for these aging systems creates a continuous revenue loop that competitors cannot easily penetrate.

According to company figures, first-quarter metrics for 2026 show the subsidiary generating 70 million SEK in operating returns at a 9% margin. Management is concurrently future-proofing these operations through aggressive sustainability initiatives. The subsidiary targets absolute zero carbon outputs before 2050, aligning its demographic growth runway with stringent European environmental mandates.

M&A Execution and the Strategic Outlook for Late 2026

Executive management continues to deploy capital into targeted bolt-on acquisitions to accelerate operational momentum through the remainder of 2026. Swegon recently secured a Danish residential ventilation buyout while simultaneously executing the divestment of three non-essential divisions. This refined focus expands Swegon’s regional ventilation dominance and streamlines its operating structure.

This focus on streamlining operations mirrors other recent industrial technology acquisitions, where established holding groups rapidly integrate highly specialised technical divisions to instantly broaden their commercial market reach.

The broader industrial portfolio also integrated Alstor, a specialised manufacturer of forestry equipment. According to company projections, together, these newly integrated enterprises are projected to add roughly 500 million SEK toward annualised turnover. Alongside these acquisitions, executive projections suggest that the severe foreign exchange pressures experienced in the first quarter will begin to soften moving into the second quarter.

Despite this optimistic outlook, management acknowledges specific operating hazards that could impact short-term execution. Mature sector stagnation and the complexities of integrating new acquisitions require careful navigation. Anticipated earnings per share and top-line projections for 2026 and 2027 remain steady, assuming these risks are managed effectively.

The enterprise must navigate three specific operating hazards to realise these projections:

- Adverse monetary shifts that compress valuation multiples across European markets

- International disputes that disrupt global supply chain reliability

- Logistical bottlenecks that delay the fulfilment of record-breaking order books

The Enduring Value of Industrial Specialisation in Volatile Markets

The temporary drag of publicly listed assets obscures the fundamental strength embedded within proprietary industrial subsidiaries. Structural tailwinds, including broad infrastructure upgrades and inevitable demographic shifts, provide a highly predictable growth floor for these specialised operations. Niche market dominance allows these units to absorb currency fluctuations while maintaining exceptional profitability ratios.

Investors evaluating industrial holding structures during periods of macroeconomic stress must weigh short-term currency translation panics against this operational resilience. The capacity to generate record order surges in a constrained economic environment demonstrates the enduring value of strict industrial specialisation.

For readers wanting to contextualise this resilience against broader global headwinds, our deep-dive into underpriced stock market risks examines the geopolitical tensions, persistent inflation pressures, and broader vulnerabilities currently threatening global equity valuations.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.