Big Tech Earnings Face $600B AI Reality Check Today

1 min ago

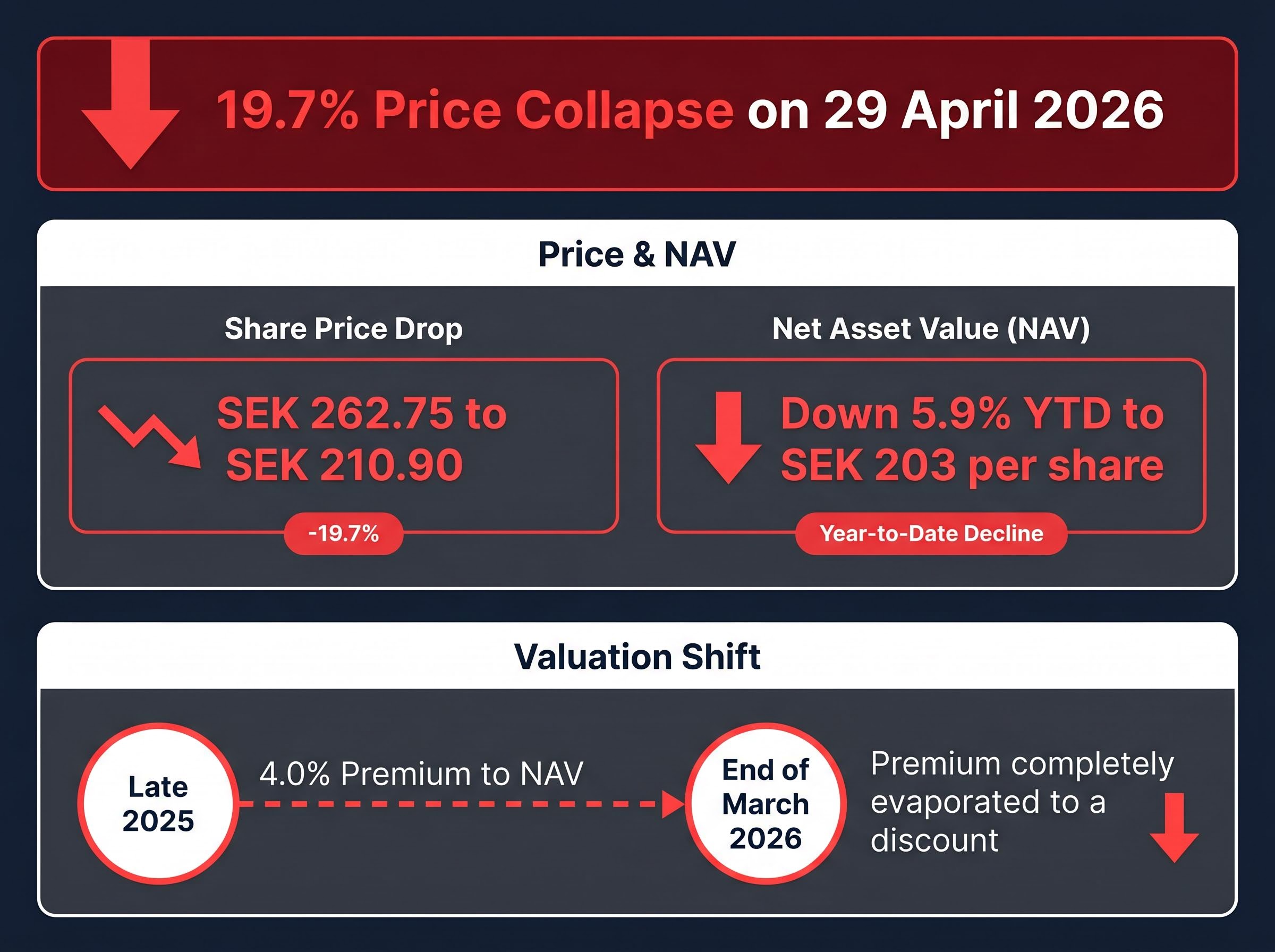

Investment AB Latour has maintained a stable dividend for 19 consecutive years, building a reputation for predictable capital compounding. That stability contrasted sharply with early trading action on 29 April 2026, when Investment AB Latour stock experienced a violent 19.7% price collapse following the release of its first-quarter earnings report. In a matter of hours, the equity shifted from trading at a clear premium to a discount against its Net Asset Value (NAV).

This severe market reaction requires careful unpacking to separate temporary reporting distortions from fundamental performance. While currency headwinds and steep drags in the listed portfolio dominated the headline figures, the operational health of the company’s industrial subsidiaries tells a different story. The following analysis examines why the market reacted so aggressively and evaluates the actual business metrics driving the firm’s unlisted operations.

The sheer scale of the sell-off became apparent immediately after the earnings release at 08:30 CEST. Shares fell sharply from SEK 262.75 to SEK 210.90, erasing months of steady gains in a single morning. Investors reacted swiftly to the listed investment portfolio’s severe underperformance against broader market benchmarks.

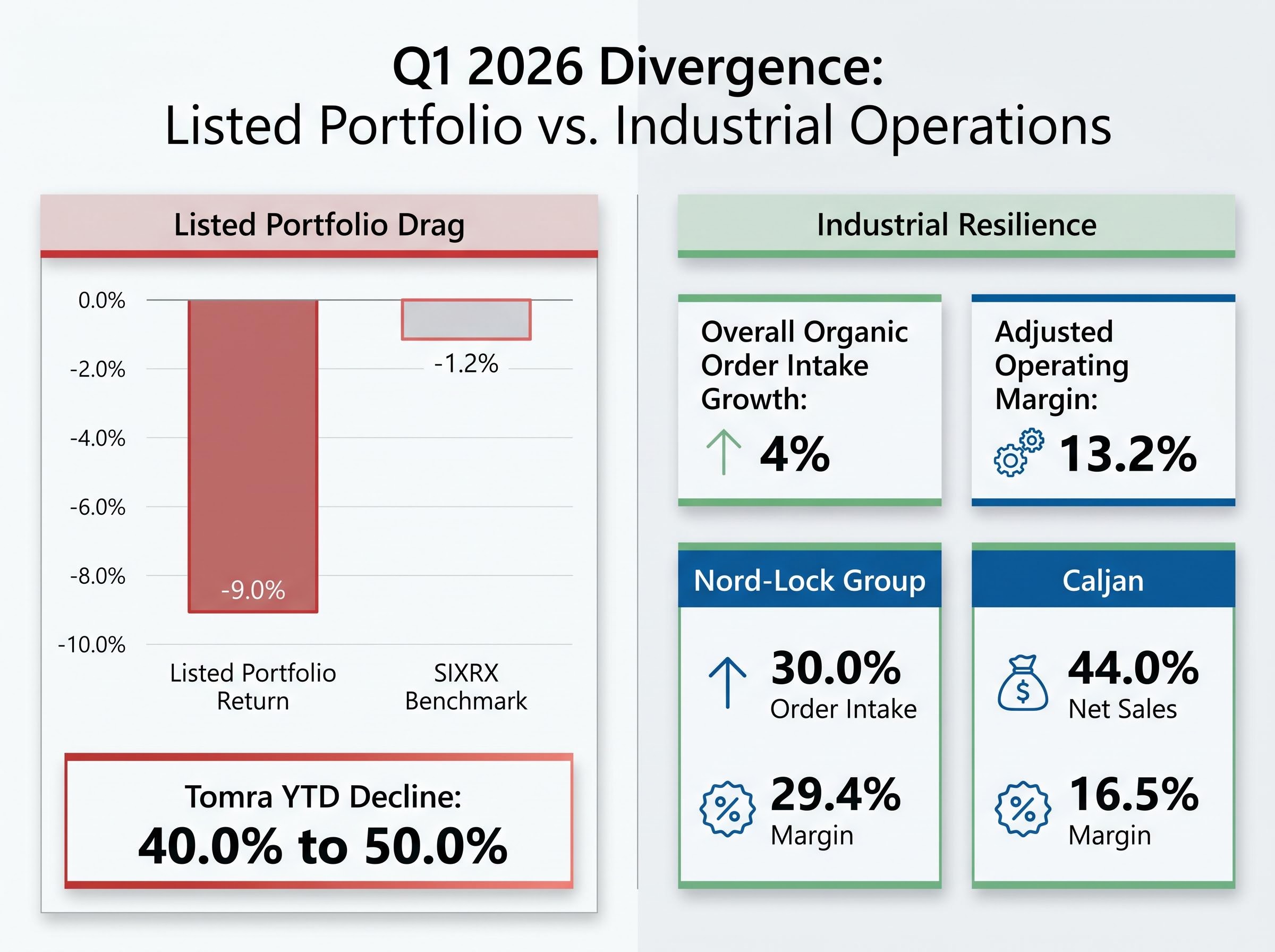

Latour reported a Q1 2026 listed portfolio return of negative 9.0%, lagging far behind the SIXRX benchmark decline of 1.2%. This poor equity performance directly impacted the broader balance sheet, driving NAV down 5.9% year-to-date to SEK 203 per share. The primary catalyst for this destruction in value was Tomra, a major holding that has become an outsized drag on the portfolio.

The MarketScreener tracking of the SIXRX index confirms that the broader Swedish market experienced only a mild contraction during the quarter, making Latour’s double-digit listed portfolio underperformance particularly noticeable to institutional investors.

Tomra shares hit a year-low of NOK 89.80 on 27 April 2026, marking an estimated year-to-date decline of 40.0% to 50.0%. Despite the severe pricing pressure on specific assets, management maintained a longer-term perspective on these holdings.

Management Commentary “The listed holdings remain quality businesses capable of gaining market share across economic cycles, regardless of current pricing pressures.”

The first quarter fundamentally altered how the market prices Latour’s assets. In late 2025, the stock commanded a clear 4.0% premium to NAV, reflecting investor confidence in management’s capital allocation strategies.

By the end of March 2026, that premium had completely evaporated, giving way to a discount. Market sentiment regarding Nordic investment companies trading above NAV has shifted, forcing a strict recalibration of expectations for holding companies that fail to beat regional benchmarks.

Beyond the listed portfolio’s failure, the factory floor paints a highly contrasting picture of corporate health. Latour’s wholly-owned industrial operations achieved organic order intake growth of 4% and an organic net sales decline of 1% during the first quarter. These divisions absorbed macroeconomic pressures effectively, holding their adjusted operating margin steady at 13.2%.

This resilience mirrors broader trends where strong industrial sector demand continues to drive robust earnings for specialized manufacturers despite wider macroeconomic uncertainties.

Specific business areas delivered record numbers, proving that underlying demand remains strong across key global markets. Nord-Lock Group reported exceptional momentum, growing organic order intake while maintaining a high operating margin. Caljan followed suit with an increase in organic net sales, driven by expanding international logistics requirements.

| Business Area | Organic Growth | Operating Margin | Key Driver |

|---|---|---|---|

| Nord-Lock Group | 30.0% (Order Intake) | 29.4% | Strong industrial demand |

| Caljan | 44.0% (Net Sales) | 16.5% | Logistics expansion |

| Hultafors Group | Positive | Stable | Professional product demand |

| Innovalift | Platform Growth | Consistent | Regional consolidation |

By observing the operational success of these unlisted subsidiaries, investors can identify the fundamental floor supporting the stock’s intrinsic value. The strong order backlog within the industrial segment suggests that the headline earnings miss was primarily a function of public equity volatility rather than a structural deterioration of Latour’s core businesses.

Evaluating multinational holding companies requires distinguishing between an actual business miss and a currency translation effect. A strengthening Swedish Krona (SEK) heavily penalises Nordic companies with heavy international sales. When revenues earned in foreign currencies are repatriated into a stronger SEK, the reported top-line figures artificially shrink, even if the volume of goods sold remains identical.

In early 2026, the SEK appreciated between 2.3% and 3.8% against major currencies like the EUR and USD. This single macroeconomic factor reduced Latour’s overall Q1 results by approximately 6.0%. Understanding this mechanical margin compression provides the technical grounding necessary to grasp why management expressed frustration with the market’s severe reaction to the earnings report.

Recent Bank of America foreign exchange analysis highlighted the Swedish Krona as a top-performing currency driven by strong domestic economic data, which mechanically pressures export earnings when translated back into the local denomination.

Several domestic tailwinds are currently driving this currency strength across the Nordic region:

Lower domestic inflation relative to European peers Swedish government fiscal stimulus measures totalling SEK 80 to 130 billion * Shifting global rate expectations favouring regional stability

This fiscal expansion supports the domestic outlook and bolsters the currency, creating a temporary headwind for export-heavy industrial firms. By separating these translation effects from organic order growth, investors can more accurately evaluate the true operational momentum of Latour’s subsidiaries.

While public market investors sold off the listed portfolio, Latour actively deployed capital to acquire growth assets. Management utilised the company’s strong balance sheet to execute strategic purchases at potentially depressed valuations. According to company data, the firm’s net debt stands at SEK 15.3 billion, representing roughly 11.0% of the market value of its investments, leaving ample financial headroom for further consolidation.

Recent and pending acquisitions are projected to add approximately SEK 500 million in annualised net sales. This offensive strategy focuses specifically on positioning subsidiaries like Innovalift and Swegon as global and regional consolidators within fragmented industries. Management remains focused on long-term capital compounding, using the current volatility as an opportunity to expand market share rather than retreating to defensive posturing.

The Innovalift segment has emerged as a key growth engine for the broader holding company. The division now operates 10 distinct companies and 11 proprietary brands, generating SEK 3.4 billion in annual revenues. This targeted expansion capitalises on specific macroeconomic trends, including ageing populations, rapid urbanisation, and stricter sustainability requirements for building access.

For readers wanting to examine other companies leveraging macro trends through acquisitions, our detailed coverage of structural profitability inflections explores how strategic bolt-on purchases can successfully transform recurring revenue profiles.

The stark contrast between listed portfolio struggles and unlisted industrial strength requires investors to carefully calibrate expectations for the remainder of 2026. Management maintains a stance of cautious optimism, noting that currency headwinds in the second quarter are expected to be considerably lower than the 6.0% drag experienced in Q1. The underlying order backlog provides clear visibility for the industrial division’s revenue generation in the coming months.

Despite the recent volatility, the company’s historical ability to compound capital offers necessary context for current valuations. The listed portfolio has delivered a trailing 15-year cumulative return of 540.0%, significantly outpacing the 350.0% return of the SIXRX benchmark. Supported by a dividend yield of 2.38% and 19 consecutive years of payouts, the fundamental floor beneath the operations remains stable.

Companies with formalised dividend distribution policies often attract a highly resilient shareholder base, ensuring that temporary earnings shocks do not trigger a complete collapse in equity value.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Investment AB Latour stock fell 19.7% on 29 April 2026 due to its listed investment portfolio reporting a negative 9.0% return, significantly lagging the SIXRX benchmark's 1.2% decline, and a 5.9% reduction in Net Asset Value.

Latour's wholly-owned industrial operations showed resilience, achieving 4% organic order intake growth and maintaining an adjusted operating margin of 13.2%, with specific areas like Nord-Lock Group and Caljan reporting strong momentum.

A strengthening Swedish Krona (SEK), appreciating 2.3% to 3.8% against major currencies, reduced Latour's overall Q1 results by approximately 6.0% due to adverse translation effects on international sales.

Yes, Investment AB Latour has maintained a stable dividend for 19 consecutive years, providing a dividend yield of 2.38%, indicating consistent shareholder returns despite recent market volatility.