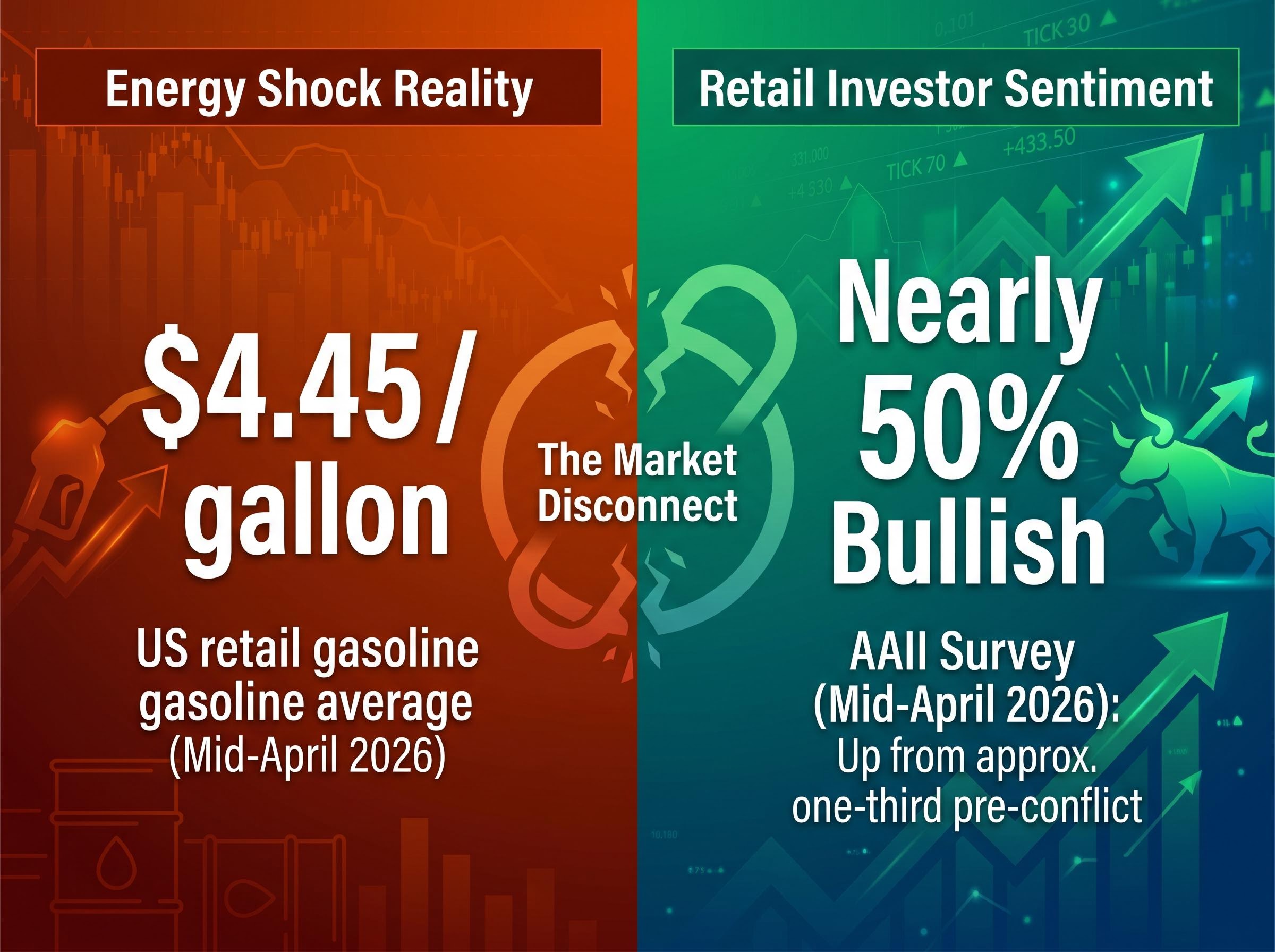

According to some reports, US consumer spending climbed at its fastest pace since early 2023 in April 2026, a headline that looks like economic vitality but may be concealing the opposite. With US retail gasoline prices averaging around $4.45 per gallon following the Iran conflict and Strait of Hormuz disruptions, UBS chief global economist Paul Donovan issued a pointed warning in late April 2026. Developed economies like the United States and the United Kingdom are spending as though nothing has changed, but the structural support is quietly eroding, and Donovan argues the reckoning is coming.

This analysis unpacks the paradox of surging consumer spending alongside diminishing purchasing power. It explains the savings drawdown mechanism masking the problem, and examines what the convergence of an oil shock, income divergence, and equity market complacency means for the US economic outlook in mid-2026.

The spending surge that isn’t what it looks like

The April 2026 Bank of America Institute data presents a seemingly bullish picture of aggregate consumer expenditure. Spending climbed at its fastest pace since early 2023, suggesting households are easily absorbing higher energy costs. Spending persisted even after excluding fuel purchases from the calculation, making the paradox harder to dismiss as a simple gasoline price distortion.

However, this data serves as a warning signal rather than a green light.

Paul Donovan’s analysis shows consumers are making adjustments in response to higher energy costs, with behavioral changes oriented toward cutting consumption despite the rapid escalation in the national average gasoline price to approximately $4.45 per gallon in mid-April.

The latest macroeconomic assessment from UBS global economists suggests that the current environment resembles a temporary suspension of economic gravity, where households are liquidating assets to maintain an unsustainable standard of living.

“Developed economies are currently operating without recognising the absence of their underlying economic support.”

This disconnect between aggregate spending data and household reality forms the core of Donovan’s thesis. Resilient spending in the face of an energy shock does not indicate underlying economic health. Instead, it reflects households operating on financial momentum, entirely masking the structural erosion occurring beneath the surface.

When big ASX news breaks, our subscribers know first

How savings drawdowns are buying time, not solving the problem

Elevated energy costs are steadily eroding household purchasing power, yet this erosion has not visibly suppressed aggregate retail activity. Households are compensating for the price shock by drawing down their accumulated savings to maintain current consumption levels. This savings drawdown acts as a temporal displacement mechanism.

The behaviour shifts the economic pain forward into the future rather than eliminating it. US gasoline product supplied stands at 9.055 million barrels per day as of April 2026, matching 2019 levels. Motor fuel demand remains completely flat despite price surges above $4.00 per gallon, suggesting consumption has not yet responded to the price signal in expected ways.

The official EIA weekly petroleum status metrics confirm that physical fuel demand remains stubbornly inelastic, forcing households to reallocate their finite monthly budgets away from discretionary categories to cover essential transportation costs.

Donovan explicitly notes this behavioural pattern is unsustainable, as economic forces have simply not yet compelled the inevitable adjustment. The correction follows a clear sequence:

- Geopolitical disruptions force sustained increases in retail energy prices.

- Higher fuel costs quietly erode baseline household purchasing power.

- Consumers draw down finite savings buffers to compensate and maintain lifestyle habits.

- Buffer exhaustion eventually triggers a sharp, mandatory correction in aggregate spending.

Financial analysts are now waiting for the April-May 2026 Personal Consumption Expenditures and personal savings rate figures from the Bureau of Economic Analysis. These metrics will quantify how rapidly the buffer is depleting.

What the oil shock actually is and why developed economies are still catching up to it

The current oil price pressure is not a temporary spike, but the result of a structurally disrupted supply chain. The United States announced a blockade of the Strait of Hormuz on 13 April 2026. As of late April, shipping traffic through the strait remains muted with no full resolution in sight.

Ceasefire efforts have allowed only limited passages, while Iran continues to impose restrictions on oil shipments. Iranian attacks on industrial plants in the UAE and Bahrain throughout March and April 2026 have combined with continued Houthi activity in the Red Sea to threaten global trade flows. These compounding factors have driven severe insurance cost escalations for vessels transiting the region, keeping price pressure elevated regardless of daily traffic volumes.

| Disruption Source | Location | Status (Late April 2026) | Economic Impact |

|---|---|---|---|

| US Blockade & Iranian Restrictions | Strait of Hormuz | Muted traffic, limited ceasefire passage | Constrained global oil supply |

| Houthi Militant Activity | Red Sea & Suez Canal | Ongoing vessel threats | Rerouted global trade flows |

| Industrial Plant Attacks | UAE and Bahrain | Facilities damaged March-April | Regional production capacity strain |

| Maritime Insurance Syndicates | Middle East Corridors | Elevated premiums persist | Compounding freight cost escalation |

The timeline for resolution remains entirely unclear. This structural reality supports Donovan’s expectation that economic pain will intensify rather than dissipate as the year progresses.

The K-shaped divide and who is actually absorbing the oil shock

Aggregate spending figures look stable, but their distribution reveals a fractured economy. Elevated gasoline prices consume a disproportionately large share of lower-income household budgets relative to higher-income households. The aggregate spending growth recorded by Bank of America is highly concentrated in higher-income segments, meaning the headline figure overstates the breadth of economic health.

US finished motor gasoline product supplied remains at roughly 9.055 million barrels per day as of April 2026. Aggregate demand has not collapsed, but the most financially vulnerable households are already absorbing a disproportionate share of the real cost. This bifurcation extends the K-shaped recovery pattern that has characterised the post-pandemic period.

The divide manifests across three distinct household experiences:

Budget impact: Gasoline costs command a high percentage of disposable income for lower-earning demographics, forcing immediate trade-offs. Spending behaviour: Higher-income groups continue discretionary purchasing, effectively propping up aggregate national retail data. * Savings buffers: Wealthier households possess deeper accumulated reserves to fund the temporal displacement, while lower-income groups reach exhaustion faster.

“The aggregate resilience is a statistical illusion carried by the top quartile, while the bottom half of the economy is already in contraction.”

Relying solely on headline indicators risks misreading the true health of the US consumer base.

Investors exploring the broader implications for their portfolios can read our detailed coverage of historical gasoline price shocks, which examines how sustained periods above four dollars have traditionally impacted corporate earnings and equity valuations over a six-month horizon.

Equity markets are looking past the risk and that may be the most dangerous signal of all

Consumers are spending as though nothing is wrong, and equity markets are pricing risk with identical complacency. According to some reports, Craig Johnson, chief market technician at Piper Sandler, maintains a dual-signal view of the current environment. He remains long-term bullish on US equities, but flags significant near-term vulnerability tied directly to the Iran conflict and Strait of Hormuz disruptions.

Investors often discount geopolitical risks lacking quantitative pricing frameworks. This psychological blind spot has pushed equities to record levels during an active conflict. Retail investors have actually become more optimistic as the supply disruptions have progressed.

When major indices reach unprecedented highs while traditional stock market warning signals flash red across the energy and logistics sectors, the probability of an abrupt downward repricing increases substantially.

An AAII sentiment survey from mid-April 2026 showed that, according to some reports, nearly half of retail investors held a bullish outlook, up from approximately one-third immediately preceding the conflict.

“The market is pricing for a seamless resolution, ignoring the delayed economic transmission mechanism entirely,” Johnson noted in a recent assessment.

Johnson identified three downside catalysts for a rapid repricing:

Broader economic fallout as consumer savings buffers completely exhaust. Additional physical disruptions to Strait of Hormuz loading infrastructure. * A geographic widening of the ongoing conflict.

The convergence of consumer complacency and equity market optimism represents a compounding danger. If equities are priced for absolute resilience just as consumer spending is forced to contract, the resulting correction could be exceptionally sharp.

The delayed reckoning is a timing question, not an if question

Three distinct pressures are currently converging on the US economy. Household savings drawdowns are approaching exhaustion, lower-income consumers are already operating under acute financial strain, and equity markets remain priced for absolute optimism. Assessing the forward view requires treating this as a timing problem rather than a binary outcome.

The question is not whether the oil shock will transmit to US consumer behaviour, but exactly when the savings buffer runs out and how quickly the adjustment follows. Donovan frames the current pattern of savings-funded spending as mathematically unsustainable over time. United Kingdom motor fuel demand is already down approximately 3.5% from pre-pandemic levels.

Some major banks have already established specific institutional sell triggers based on Brent crude crossing predetermined price thresholds, which would mandate immediate portfolio derisking regardless of consumer resilience.

This European contraction serves as a leading indicator, suggesting the US may follow a similar trajectory with a slight behavioural lag. Rather than attempting to predict the exact date of the correction, financial analysts are monitoring specific leading indicators that will signal the turning point.

Key metrics to monitor include:

- BEA savings data: The April-May 2026 personal savings rate and PCE figures from the Bureau of Economic Analysis will reveal the true pace of buffer depletion.

- Consumer sentiment: The Conference Board and University of Michigan consumer confidence indices will capture the psychological shift before spending formally contracts.

- Energy demand: The EIA weekly petroleum status reports will show when US fuel consumption finally breaks from its current 9.055 million barrels per day plateau.

These indicators will determine the exact timeline of the coming contraction.

The bill the spending data isn’t showing yet

Consumer spending data in April 2026 shows statistical strength precisely because households are masking their financial weakness, not because that weakness has been resolved. Donovan’s warning remains a structural observation rather than a rigidly timed prediction. The severity and speed of the inevitable correction will depend entirely on the conflict’s duration and the remaining depth of household savings.

As these household buffers diminish and energy costs remain elevated, macroeconomic analysts have been forced to aggressively revise their recession probability forecasts upward for the remainder of the year.

“The reckoning is mathematically assured, even if the exact date of arrival remains obscured by the data.”

Attentive economic monitoring is the only appropriate response to this paradox. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions.