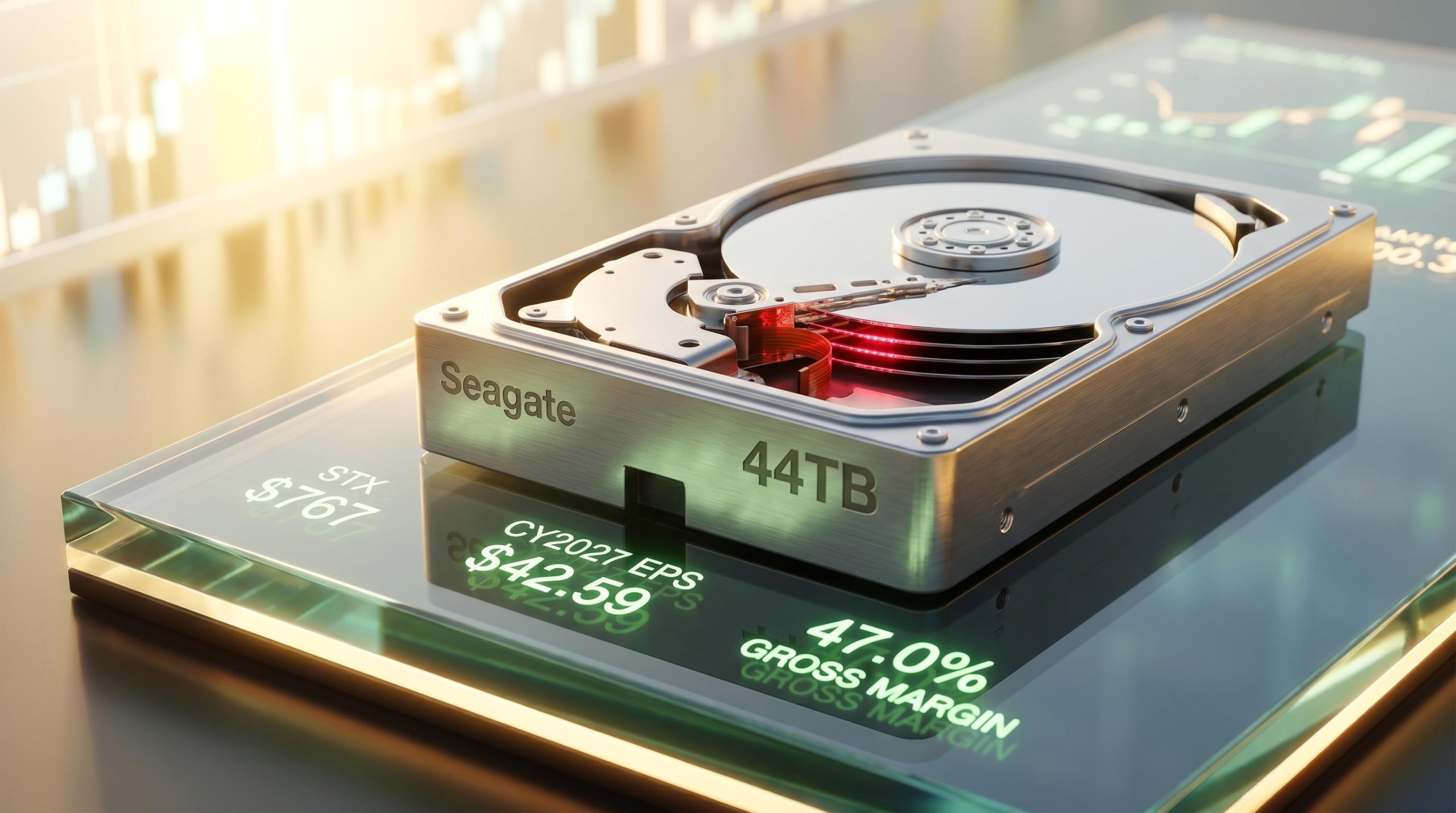

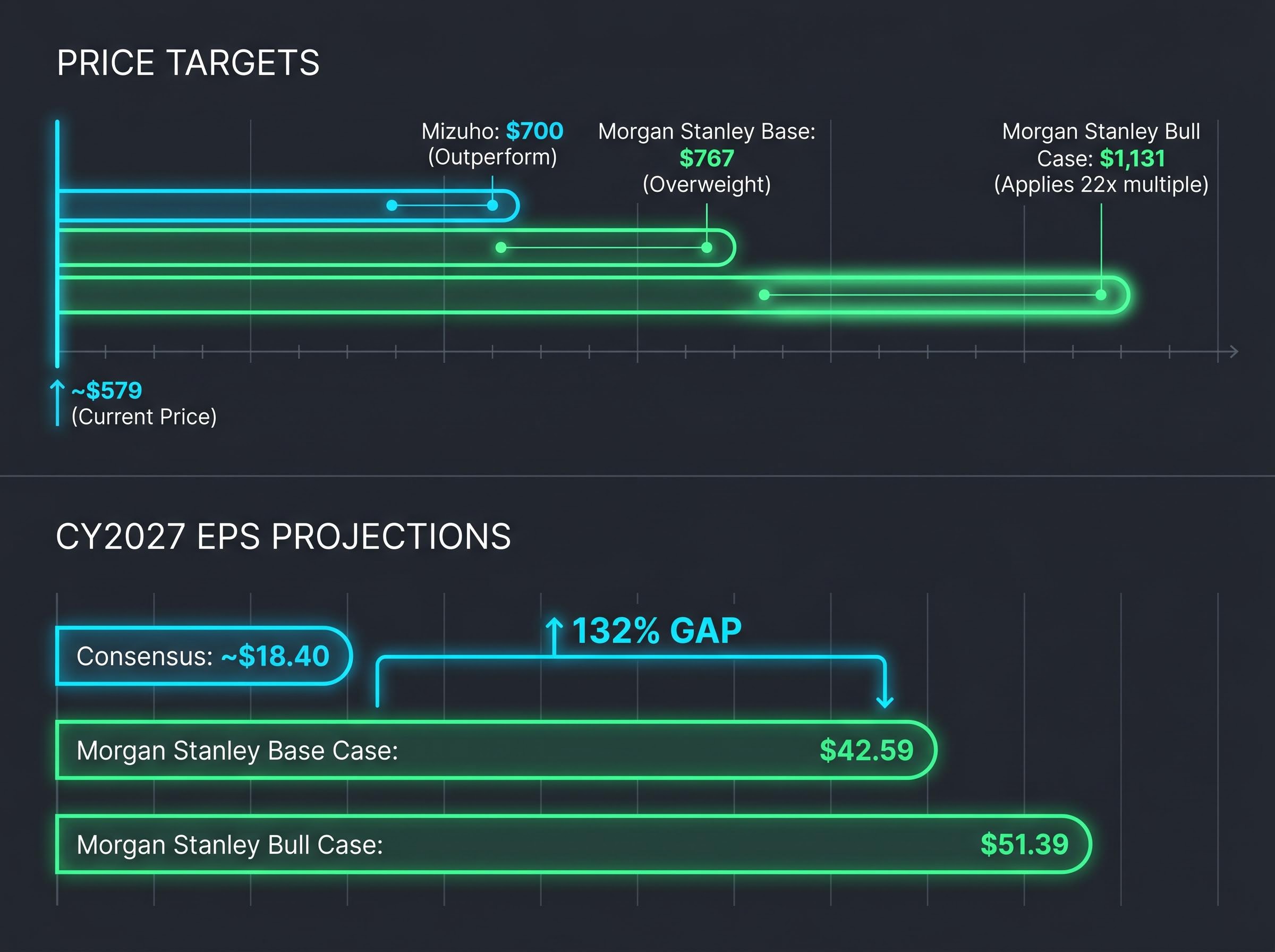

Morgan Stanley’s bull case for Seagate Technology (STX) has shifted from aspirational scenario to something analysts are treating as a plausible base trajectory. That is a remarkable repositioning for a company manufacturing spinning magnetic disks. Seagate reported fiscal Q3 2026 earnings on 28 April 2026, posting $3.11 billion in revenue and $4.10 non-GAAP EPS, both well ahead of consensus. The stock closed at approximately $579 on 29 April. Morgan Stanley responded by raising its price target to $767 and noting its previously held bull scenario had now become its base case, for the third consecutive quarter. The investment question is no longer whether the HDD upcycle is real. It is whether the structural forces sustaining it are durable enough to justify where valuations are heading. This analysis examines the architecture of that upcycle: what is driving it, why pricing is running ahead of expectations, where Seagate sits competitively, and what risks could interrupt the thesis.

Earnings that keep arriving ahead of the curve

The Q3 FY2026 result was not a single-quarter surprise. It was the seventh consecutive quarter of growth, and the pattern of execution is more telling than any individual number.

Management had guided approximately $2.9 billion for Q3 revenue. The actual figure came in at $3.11 billion. Non-GAAP EPS of $4.10 beat the consensus. Non-GAAP gross margin reached 47.0%, a figure that signals structural margin expansion rather than simple top-line leverage on a fixed cost base.

The prior quarter told a similar story. Q2 FY2026 revenue of $2.83 billion represented 21.5% year-over-year growth, beating estimates by 2.6%, with EPS of $3.11 exceeding consensus by 9.6%. The beat-and-raise cadence has now repeated across multiple reporting periods, which changes how the forward estimates should be interpreted.

| Quarter | Revenue | Non-GAAP EPS | Gross Margin | YoY Revenue Growth |

|---|---|---|---|---|

| Q1 FY2026 | ~$2.33B (implied) | — | — | — |

| Q2 FY2026 | $2.83B | $3.11 | — | 21.5% |

| Q3 FY2026 | $3.11B | $4.10 | 47.0% | — |

What forward guidance implies about the second half of the upcycle

Q4 FY2026 guidance once again exceeded what the Street had anticipated before the print. When a company beats and raises for three or more consecutive quarters, the analytical implication is clear: sell-side models are systematically underestimating the pricing environment.

This systemic underestimation extends beyond hardware manufacturers to the infrastructure layer itself, with major data centre platform earnings recently receiving substantial guidance upgrades due to accelerating capacity demands across global markets.

Morgan Stanley’s CY2027 base case EPS sits above its own prior estimate and above where the broader consensus currently rests. That gap is either a signal that consensus has substantial ground to cover or that Morgan Stanley’s assumptions are too aggressive. The answer to that question depends on what is driving the upcycle and how long it can persist.

When big ASX news breaks, our subscribers know first

Why HDDs still dominate the storage layer, and why AI is amplifying that position

Hard disk drives account for cloud storage demand, according to Morgan Stanley’s April 2026 research. This is not legacy inertia. It reflects a cost-per-terabyte advantage that current solid-state drive pricing has not eroded.

HDDs hold approximately 80% of cloud storage demand, underpinned by a 6:1 total cost of ownership advantage over SSDs in nearline applications.

The distinction between the two recent phases of AI infrastructure spending helps explain why this advantage is accelerating rather than eroding:

- 2023-2024 (compute-centric phase): Capital expenditure concentrated on GPU procurement, training clusters, and compute density. Storage demand grew, but the primary bottleneck was processing power.

- 2025-present (data-centric phase): The focus has shifted to storage and inference workloads. Generative AI applications involving video and high-resolution imaging require disproportionately more storage per unit of compute than text-based large language models, driving exabyte demand toward high-capacity nearline drives specifically.

Industry-wide AI infrastructure spend is projected at approximately $720 billion for 2026. Amazon alone is planning approximately $200 billion in capital expenditure. AWS, Google, and Microsoft are collectively expected to drive approximately 67% of data centre capacity by 2031. The storage layer that serves those data centres runs on HDDs, and the workloads filling them are growing faster than the drives can be manufactured.

Independent global data centre expenditure forecasts validate this macroeconomic momentum, with analysts anticipating total infrastructure outlays to surpass $788 billion by year-end as hyperscalers rapidly expand capacity.

Understanding the HDD upcycle: what drives it and why this one is different

An HDD upcycle follows a recognisable sequence. Understanding its mechanics clarifies why the current cycle may behave differently from its predecessors.

- Underinvestment phase: Manufacturers reduce capacity during a demand downturn to preserve margins and cash flow. The 2022-2024 HDD downturn produced lasting reductions in manufacturing footprint.

- Demand surge: A catalyst, in this case AI-driven data centre expansion, creates a step-change increase in storage procurement.

- Supply shortfall: Reduced manufacturing capacity cannot scale quickly enough to meet the surge. Lead times extend. The current lead time on high-capacity drives exceeds 50 weeks.

- Pricing power transfer: With supply constrained and demand rising, pricing leverage shifts from buyers to manufacturers. Customers accept higher prices to secure allocation.

- Margin expansion: Rising average selling prices on a largely fixed manufacturing cost base expand gross margins, which is precisely what Seagate’s 47.0% Q3 gross margin reflects.

While hyperscale facilities dominate the current volume surge, memory requirements for ultra-edge AI applications in autonomous systems are simultaneously driving parallel development cycles for highly efficient, low-power retention technologies.

The industry is now seven quarters into a cycle that historically peaks at 8-10 quarters. That places the current cycle closer to its historical ceiling than its floor. The argument for extension rests on the structural nature of the AI demand driver, which did not exist in prior cycles, and on the depth of the preceding underinvestment.

HDD cost per terabyte rose quarter-over-quarter in Q1 CY2026, versus the increase that had been anticipated, according to Morgan Stanley. That divergence is the clearest signal that pricing dynamics are running ahead of what models had assumed.

Seagate’s capacity is sold out through 2026. For investors, the duration question is the central valuation variable. A cycle that extends two or three quarters beyond historical norms on the back of structural AI demand is meaningfully different from one that simply prolongs temporary post-downturn tightness.

Seagate’s HAMR technology moat and what it means for competitive positioning

The upcycle benefits all HDD manufacturers. Seagate’s specific advantage lies in a technology platform that positions it to capture a disproportionate share of the cycle’s economics.

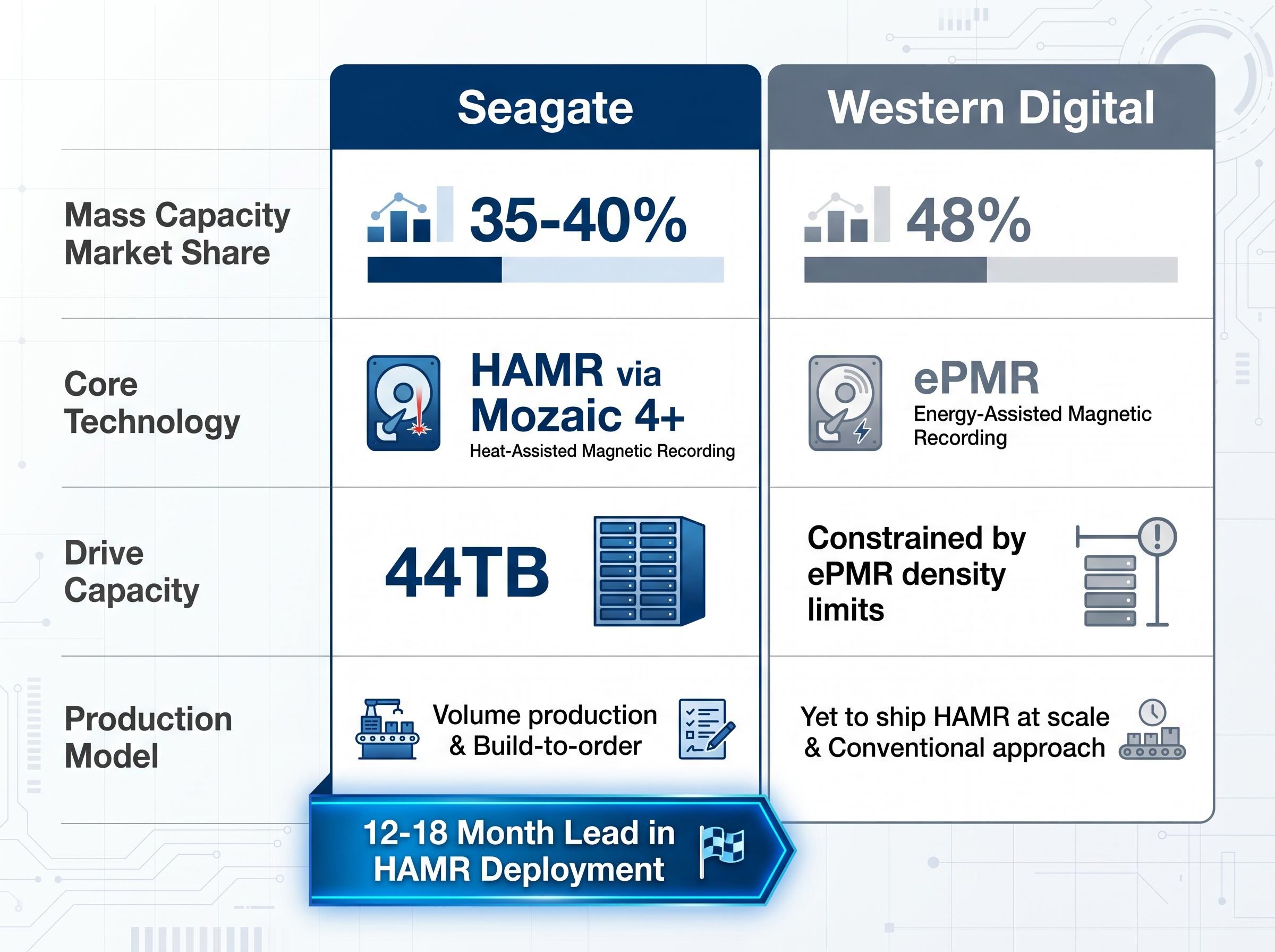

The Mozaic 4+ platform uses heat-assisted magnetic recording (HAMR), a technology that uses a laser to momentarily heat the disk surface during writing, allowing data to be stored at higher densities than conventional methods permit. The platform supports up to 44TB capacity per drive and is in volume production, shipping to hyperscale data centres as of April 2026.

The commercial validation of visible laser technology for enterprise applications represents a major shift in hardware supply chains, prompting specialised photonics companies to forge lucrative development partnerships with global mass-capacity storage leaders.

Seagate holds an estimated 12-18 month lead over competitors in HAMR volume deployment. Western Digital, which holds approximately 48% of the mass capacity HDD market compared to Seagate’s estimated 35-40%, continues to rely on energy-assisted perpendicular magnetic recording (ePMR) technology that is approaching its density limits.

The competitive comparison across three dimensions:

- HAMR deployment: Seagate in volume production; Western Digital yet to ship HAMR at scale

- Capacity ceiling: Seagate at 44TB via Mozaic 4+; Western Digital constrained by ePMR density limits

- Business model: Seagate operates a build-to-order model; Western Digital maintains a more conventional production approach

The build-to-order model as a structural cycle stabiliser

Seagate’s build-to-order approach locks in customer commitments before production begins. This structurally reduces exposure to the spot-market demand collapses that have historically ended HDD upcycles abruptly. During the 2022-2024 downturn, open-market production models contributed to inventory gluts that compressed pricing across the industry.

The combination of a technology timing advantage and a demand-commitment model means Seagate has structural mechanisms to sustain its pricing power even if the broader cycle eventually softens.

What the analyst community sees from here, and where the disagreements lie

Morgan Stanley raised its price target following the Q3 FY2026 print, but the specific architecture of its upgrade reveals where analytical consensus ends and disagreement begins.

This shift in institutional pricing power analysis highlights a growing conviction that gross margin expansions will persist well beyond historical cyclical patterns.

| Firm | Prior Target | Revised Target | Rating | Key Rationale |

|---|---|---|---|---|

| Morgan Stanley | $582 | $767 | Overweight | Bull case migrated to base case for third consecutive quarter; CY2027 EPS revised to $42.59 |

| Mizuho | $565 | $700 | Outperform | Pricing power and nearline demand durability support continued re-rating |

Morgan Stanley noted that its bull case had migrated to its base case for the third consecutive quarter, a pattern that captures the pace at which the earnings trajectory is outrunning even the most optimistic prior models.

The Morgan Stanley bull case applies a 22x multiple to $51.39 in CY2027 EPS, producing a $1,131 price target. The base case of $42.59 EPS sits approximately 132% above where the broader Street consensus currently rests (implied consensus of approximately $18.40).

That 132% gap between Morgan Stanley’s base case and consensus is the most important single number for investors to interrogate. If consensus remains that far below a well-evidenced bull thesis, the stock has a long runway even at elevated current prices. If consensus proves closer to correct, the premium embedded at $579 is not supportable on a forward earnings basis.

Even among bulls, the $67 spread between Morgan Stanley’s $767 target and Mizuho’s $700 target shows meaningful disagreement about the magnitude of upside remaining.

The risks that could end or interrupt the thesis

Why SSD substitution is the risk that demands the closest monitoring

The entire HDD investment case rests on a cost-per-terabyte advantage. HDDs currently hold a 6:1 total cost of ownership advantage over SSDs in nearline applications. That ratio is the structural floor of the thesis.

If NAND flash pricing declines substantially, whether through a cyclical oversupply in the NAND market or through unexpected density improvements in SSD technology, the competitive floor for HDDs in cloud storage could erode faster than the bull case assumes. NAND flash pricing is inherently cyclical, and a sustained price decline would be the clearest early warning signal for investors to monitor.

The remaining risk categories carry distinct profiles:

- Upcycle duration: At seven quarters into a cycle that historically peaks at 8-10 quarters, any slowdown in hyperscaler capital expenditure commitments could compress the timeline. AI tailwinds may extend the cycle, but that extension is an assumption, not a certainty.

- Regulatory and compliance: Seagate is operating under a $300 million BIS penalty with compliance audits running through late 2026. U.S. export controls on 30TB-plus drives to China restrict access to one of the largest potential markets for high-capacity drives.

- Supply chain and geopolitical: Approximately 90% of rare earth processing is concentrated in China, creating a dual exposure where U.S.-China trade tensions could simultaneously pressure supply chain inputs and end-market access.

Investors who distinguish between which risks are existential (SSD substitution at scale), which are near-term cyclical (upcycle duration), and which are structural overhangs with defined timelines (BIS compliance, export controls) are better positioned to size and monitor a position than those treating all risk factors as equivalent.

Investors exploring the broader landscape of disruptive semiconductor architectures will find our deep-dive into emerging ReRAM technology highly relevant, as it examines how independent chip developers are advancing alternative memory frameworks and in-memory compute solutions.

The upcycle has legs, but the easy money required less conviction than what comes next

The structural case for Seagate is well-evidenced. The HAMR moat is real, pricing power is documented in the results, capacity is sold out, and margin expansion is accelerating. These are genuinely differentiated features relative to prior HDD cycles.

STX at approximately $579, reflecting roughly 104% year-to-date appreciation, is not a question of whether the upcycle is real. It is a question of whether the duration and earnings magnitude assumptions embedded in the price are achievable. Morgan Stanley’s base case of $42.59 CY2027 EPS implies approximately 32% upside to its $767 target, but reaching that requires the cycle to extend and margins to hold at levels that have no historical precedent in this industry.

Two metrics will determine whether the thesis plays out:

- Gross margin trajectory through the remainder of 2026: Any compression from the 47.0% Q3 level would signal that pricing power is peaking before earnings estimates have fully adjusted.

- Hyperscaler capital expenditure commitments: Any sign of deceleration in the $720 billion industry spend projection would shorten the demand runway.

The 12-18 month HAMR lead remains the most durable element of the bull case regardless of cycle timing, because it is a company-specific advantage that does not depend on macro conditions persisting.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.